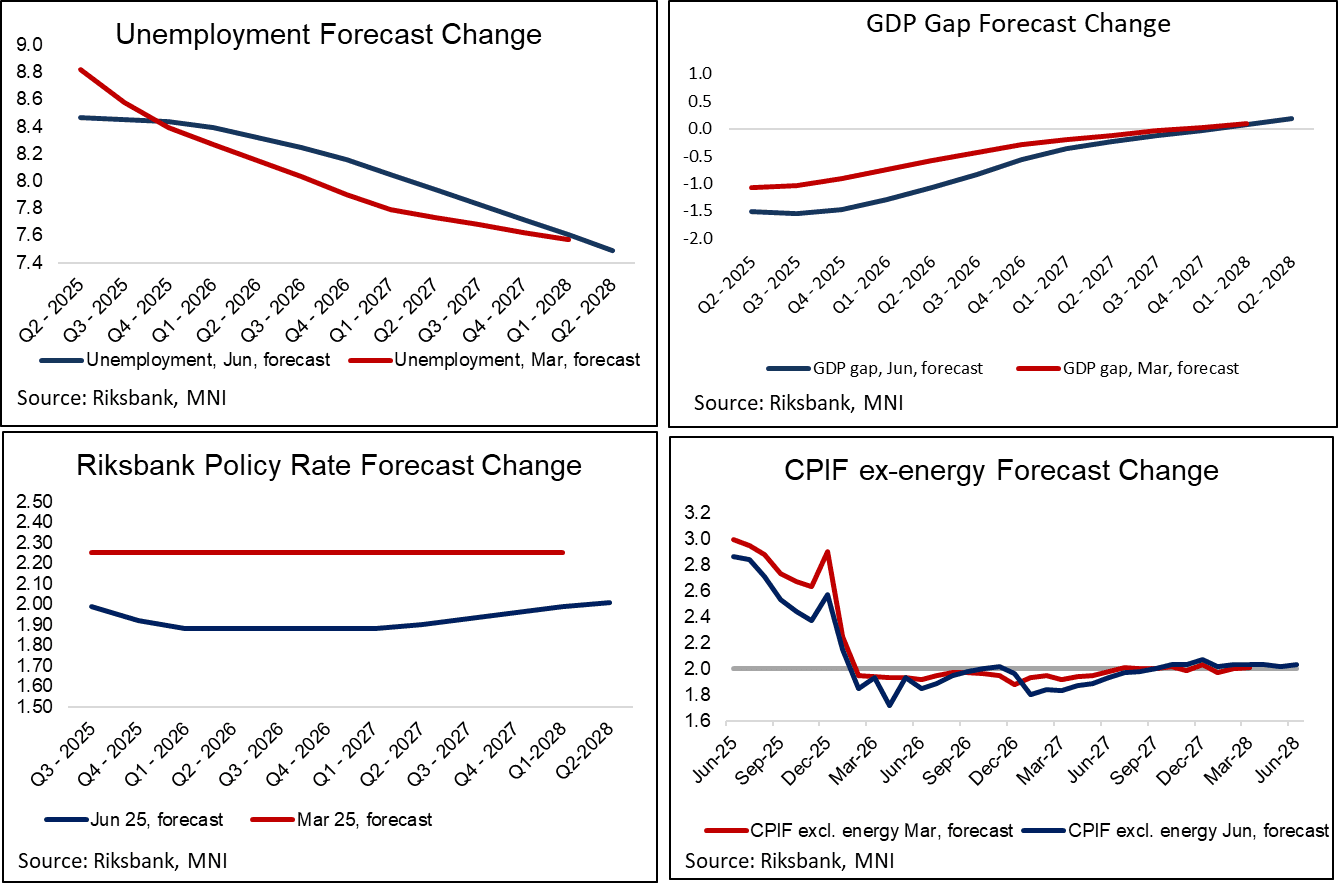

RIKSBANK: Long-end Rate Path Revision More Dovish In Context Of Other F'casts

SEK weakness has extended since this morning’s Riksbank decision, where rates were cut to 2.00% as expected but the signals in the policy statement and June MPR rate path leant dovish. In the press conference, Governor Thedeen tried to play down the dovish signal from the front-end of the June rate path (which assigns a ~50% probability of another cut this year). However, markets may be paying some attention to the downward rate path revision in 2026-2028. The “terminal” point of the rate path in Q1 2028 was 2.01%, well below the 2.25% level that had anchored long-end projections since the September 2024 decision (when the Riksbank’s revised 1-3% nominal neutral estimate was announced).

- A reminder that the first three quarters of the rate path represent the Executive Board's best assessment of policy rates, while further out the path is an output of staff's macroeconomic models.

- This long-end revision is particularly notable in the context of the June MPR's updated macroeconomic projections. The medium-term forecasts for unemployment, the GDP gap and CPIF ex-energy are all relatively unchanged compared to March. Meanwhile, the long-term KIX effective exchange rate forecast is actually higher than before (which indicates a weaker exchange rate and all else equal would be a hawkish rate path input).

- Overall, the June projections suggest the Riksbank staff’s macroeconomic framework is structurally more dovish compared to March, with uncertainty-related weakness in the next year or two needing to be compensated with lower rates through the projection horizon. The June meeting minutes (released June 25) will provide insight on whether such an outlook is echoed by Executive Board members.

- EURSEK is now up 0.5% on the session, through the May 27 high of 10.9937 and narrowing the gap to the next resistance at 11.0850 (April 28 high).

- The decision has reinforced bullish technical conditions in NOKSEK, with the cross up 0.3% today and approaching clustered resistance around 0.9646 (March 21 high) and 0.9651(trendline drawn from the March 2022 high).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUROZONE DATA: Q1 Negotiated Wages Seen Around 2.5-2.7% Y/Y On Friday

Although Thursday's May flash PMIs headline this week's Eurozone data calendar, there will also be interest in the ECB’s Q1 negotiated wages print on Friday. There isn’t a solid consensus for the data, but the ECB’s forward looking wage tracker alongside some sell-side estimates we have seen suggest a reading around 2.5-2.7% Y/Y. This should be viewed as consistent with existing ECB projections, and have limited impact on rate cut pricing.

- Q4 ‘24 negotiated wages were 4.13% Y/Y, down from 5.43% in Q3. This indicator can be volatile quarter-to-quarter, as it includes one-off payments in wage agreements.

- The ECB’s forward looking wage tracker, which is publicly released the Wednesday after each monetary policy decision, currently tracks wages with unsmoothed one-off payments at 2.51% Y/Y.

- The smoother ex-one-off payments tracker is currently at 4.43% Y/Y for Q1.

- The March Eurozone Indeed wage tracker was 2.67% Y/Y (vs 2.86% in February).

- The ECB projects Q1 compensation per employee growth at 3.8% Y/Y (vs 4.09% in Q4). This data will be released on June 6 alongside the final Q1 national accounts, the day after the ECB’s June decision.

- Summarising a few recent sell side views on negotiated wage growth:

- Morgan Stanley: “In January and February, euro area negotiated wages were running around 3.1%Y. As per preliminary data from Destatis, the year-on-year growth rate of German negotiated wages in March could be very low, maybe even negative, because of base effects from very large one-off payments in the same month last year (mostly in the public sector). If confirmed (we will have German March data from Bundesbank on Thursday), this would push down the quarterly reading for the euro area to, we think, 2.7%Y in 1Q25”.

- Nomura: “We forecast euro area negotiated wage growth to slow to 2.6% y-o-y in Q1 2025”…”Our euro area aggregate forecast is based on 65% of country-level data that are already available and our expectations for the remaining data. The main elements not yet published are German data for March 2025 and French data for the entirety of Q1 2025”.

FOREX: CHF, JPY Fail to Benefit as Global Bonds Backtrack

- Both JPY and CHF underperform against EUR, GBP and Scandi FX, failing to benefit from equity weakness and the risk-off tone following the Moody's US downgrade. - However, CHF and JPY's relative underperformance is consistent with higher yields and steeper curves across bond markets, and further questions around US credit worthiness could keep the pressure on low-yielding currencies.

- Moves are most apparent against the Euro, with EURJPY at 163.27 after clearing its 20-day EMA. Initial resistance is clustered at a set of highs just above 164.00 ahead of the key 165.21 level, the May 13 high and bull trigger.

- EURCHF continues to trade within recent ranges, and just below resistance at 0.9447, the highs seen on April 25. A break of that level would open up a set of highs slightly above the 0.95 handle.

EFSF ISSUANCE: New E3bln WNG 7-year syndication: Allocations out

- Spread set earlier at MS+34bps (guidance was MS+36bps area)

- Size: E3bln WNG

- Books closed in excess of E9.5bln (inc E700mln JLM interest)

- HR 102% vs 1.70% Aug-32 Bund

- Maturity: 27-Sep-2032

- Settlement: 26-May-2025 (T+5)

- Coupon: Short first to 27-Sep-2025

- Bookrunners: DB(B&D/DM)/DZ/GSBE SE

- ISIN: EU000A2SCAU4

- Timing: Hedge deadline 12:10BST / 13:10CET

From market source