MNI US MARKETS ANALYSIS - Awaiting Full Data Schedule

Highlights:

- Awaiting full data schedules as BLS needs more time to assess before finalizing revised dates

- UK market whipsaw shows acute sensitivity of GBP, Gilts to fiscal risk into the Budget

- EURCHF breaks to new multi-year lows as key support zone gives way

US TSYS: Limited UK Fiscal Spillover Enough To Help Extend Recent Steepening

- Treasuries trade modestly bear steeper on the day, with only limited spillover to Gilts sliding on latest fiscal concerns (UK 10Y +10.5bps). Treasuries outperform EGBs which see closer linkages to the UK.

- The steepening helps build on moves that were helped yesterday by a weak 30Y auction, with its 1bp tail and the second lowest bid-to-cover since Nov 2023.

- There’s no discernible haven bid from equity futures remaining under pressure after yesterday’s larger losses.

- Cash yields are unchanged to 2.5bp higher, with increases led by 30s.

- 5s30s at 102.9bps (+2.1bp) for highs since Nov 7 and before that Oct 17.

- TYZ5 trades at 112-21+ (-03) off an earlier low of 112-19, on reasonable overnight volumes of 355k.

- Wednesday saw 113-02+ in a probe of a key near-term resistance at 113-02 (Nov 5 & 7 joint highs), after which lies 113-18+ (Oct 28 high). To the downside, support at 112-10 (100-dma) which sits above a reversal trigger at 112-06 (Sep 25 low).

- Data: We don’t expect any major releases today

- Fedspeak: KC Fed’s Schmid (1005ET), Dallas Fed’s Logan (1430ET), Atl Fed’s Bostic (1520ET)

- Politics: Trump departs for Florida (1800ET)

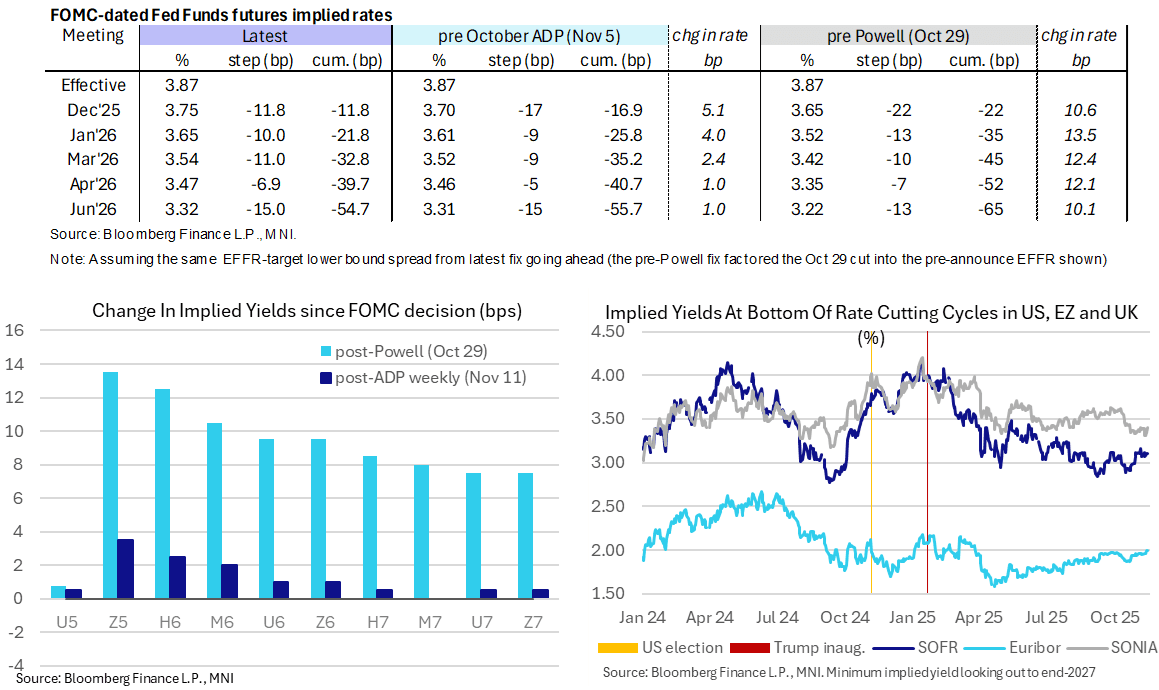

STIR: US Rates Consolidate Hawkish Near-Term Shift, More Hawkish Fedspeak Ahead

- Fed Funds implied rates are unchanged overnight for the next two meetings and only 0.5-1bp lower for those out to mid-2026 after yesterday pushing to ~50/50 odds of a pause next month.

- Cumulative cuts from 3.87% effective: 12bp Dec, 22bp Jan, 33bp Mar, 39.5bp Apr, 54.5bp Jun.

- SOFR futures are broadly unchanged, with the front end still clearly leading volumes but

- The SOFR implied terminal yield holds at 3.105% (SFRH7). It’s +4bp from Tuesday’s close having digested the soft weekly ADP print but still off the multi-month high close of 3.16% from last Wednesday after more encouraging monthly ADP and especially ISM Services data.

- Today’s Fedspeak comes from those at the hawkish end of the FOMC, notably Schmid and Logan but also Bostic who has recently called for holding rates until inflation is moving to 2% whilst seeing price pressures persist until mid-to-late 2026.

- 1005ET – Kansas City Fed’s Schmid ('25) on mon pol and outlook (text tbd). These will be his first remarks since his dissenting statement having last month voted to keep rates on hold. He judges that a rate cut can’t address the structural changes in the job market and that policy is only modestly restrictive.

- 1430ET - Dallas Fed’s Logan ('26) in fireside chat (no text)

- 1520ET - Atlanta Fed’s Bostic (non-voter) in moderated discussion (no text)

US DATA: Still Awaiting Revised Schedules

- In case missed late yesterday, the BLS will provide an updated post-shutdown data schedule when it becomes available, here: https://www.bls.gov/bls/2025-lapse-revised-release-dates.htm

- “We appreciate your patience while we work to get this information out as soon as possible, as it may take time to fully assess the situation and finalize revised release dates."

- Yahoo Finance's Schonberger had reported earlier yesterday that the BLS will produce an updated release schedule "in the coming days".

- There's no word from the BEA or Census Bureau on their updated releases – they are likely to come after the BLS emerges with their new release schedule.

- MNI re-opening guide: Hidden PDF

- Since we published that guide on Nov 11, NEC’s Hassett said the September NFP report could be released next week and said the October jobs report will be released without the unemployment rate, which we take to mean it will only release the establishment survey details in a split that we had thought was likely.

- MNI data methodology cheat sheet: Hidden PDF

US TSY FUTURES: Meaningful Long Cover On Thursday

OI data points to net long cover dominating across all contracts as Tsy futures sold off on Thursday.

- The most meaningful move came in FV futures.

- Just under $10mln of DV01 equivalent was removed across the curve (in net terms).

| 13-Nov-25 | 12-Nov-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,565,890 | 4,598,569 | -32,679 | -1,216,464 |

FV | 6,842,105 | 6,914,251 | -72,146 | -3,083,055 |

TY | 5,449,706 | 5,458,132 | -8,426 | -561,926 |

UXY | 2,500,149 | 2,506,317 | -6,168 | -552,585 |

US | 1,834,862 | 1,849,519 | -14,657 | -1,856,843 |

WN | 2,160,552 | 2,174,845 | -14,293 | -2,649,640 |

|

| Total | -148,369 | -9,920,513 |

SOFR: Net Short Setting Dominates On Thursday

OI data suggests that net short setting dominated through the greens as SOFR futures sold off on Thursday (theme only broken by not long cover in SFRZ5).

- Positioning was more balanced in the blues, with a single line of net long cover (SFRZ8) offsetting the net short setting seen across the rest of the pack.

| 13-Nov-25 | 12-Nov-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,358,144 | 1,366,159 | -8,015 | Whites | +82,576 |

SFRZ5 | 1,448,251 | 1,412,291 | +35,960 | Reds | +28,028 |

SFRH6 | 1,255,044 | 1,214,048 | +40,996 | Greens | +24,152 |

SFRM6 | 1,108,918 | 1,095,283 | +13,635 | Blues | +44 |

SFRU6 | 1,125,862 | 1,116,408 | +9,454 |

|

|

SFRZ6 | 1,200,520 | 1,192,831 | +7,689 |

|

|

SFRH7 | 853,156 | 845,467 | +7,689 |

|

|

SFRM7 | 815,997 | 812,801 | +3,196 |

|

|

SFRU7 | 775,279 | 771,952 | +3,327 |

|

|

SFRZ7 | 815,225 | 809,952 | +5,273 |

|

|

SFRH8 | 436,547 | 434,547 | +2,000 |

|

|

SFRM8 | 424,137 | 410,585 | +13,552 |

|

|

SFRU8 | 355,817 | 350,045 | +5,772 |

|

|

SFRZ8 | 326,743 | 334,958 | -8,215 |

|

|

SFRH9 | 204,604 | 202,370 | +2,234 |

|

|

SFRM9 | 187,850 | 187,597 | +253 |

|

|

UK FISCAL: Latest Reports Suggest Reeves Will Not Lower Income Tax Thresholds

Gilts and GBP tick lower as tweets from the BBG and Guardian editors suggest that Chancellor Reeves will not lower the income tax thresholds (although note that she is set to extend the freeze on the thresholds).

- Market moves fairly modest, with pre-existing session lows in cable and gilts unchallenged.

UK FISCAL: Some thoughts on freezing the income tax threshold (and not lowering)

- It was already expected to happen even if there had been an income tax hikes

- It backloads the fiscal tightening (putting it beyond the timeframe that the BOE is looking at re inflation forecasting etc.

- It means that more taxes elsewhere need raising... And as yet we have no idea what those will be or how front-loaded they will be or whether they will be inflationary or disinflationary.

- The markets clearly think that this is another example of the government not being able to make the big decisions and being pushed around by backbenchers. More fiscal uncertainty. More concern the fiscal headroom won't be increased. Gilts aren't a fan of those conditions.

BOE: Will Governor Bailey vote for a December cut if income tax isn't raised?

- SONIA markets this morning are seeing the probability of a December cut moving from around 20bp priced at yesterday's close to around 19bp now with the curve seeing around 5bp less priced in in around a year's time (see STIR: Reports Re: Walk Back Of Income Tax Hike Drives Hawkish BoE Repricing at 7:43GMT).

- We think that if the data comes in line on the inflation side and we don't see a big reversal in the labour market print just ahead of the MPC decision that unless there is something explicitly inflationary in the Budget that there would still be enough evidence for Governor Bailey to vote for a December cut irrespective of any changes to income tax.

- And also note - the FT story isn't fully ruling out any changes to income tax, it is noting that the changes could be more via thresholds than explicitly via rates.

- As we noted earlier, moving the higher rate threshold by 10% would not hit the "working person" definition used by Treasury and would still raise GBP7bln (if not offset by NIC). That would still be a substantial tax increase, albeit the marginal propensity to consumer of those with higher incomes is less than that of lower incomes - so it would have less of an impact.

- Further out, it does slightly reduce the probability of rate cuts down the line - so the market is right to price a slightly higher terminal rate on this news. And there is still the elephant in the room of if this policy raises less money, what is going to raise money instead...?

FOREX: GBP Vol Shows How Sensitive Markets are to Fiscal Risk

- GBP is comfortably the most active currency in G10 so far Friday, with acute volatility accompanying several mixed stories on UK fiscal risk - reinforcing the link between GBP & Gilt markets to the incoming Budget on November 26th. An overnight report that Chancellor Reeves has scrapped any income tax rate rises triggered a sell-off in UK assets, which had become accustomed to a settled tax plan to shore up fiscal headroom. The resultant GBP weakness (and, to a lesser extent, Gilt weakness) was then briefly reversed as Bloomberg reported the U-turn was due to "improved" OBR forecasts, reducing her need for action on tax-and-spend.

- The recovery rally in GBP was short-lived, however, suggesting markets will remain unsteady and await the details at the end of the month for a more convictive move in either direction. Reeves may plug some of the remaining fiscal hole with income tax threshold changes, but what remains is that the market may be less convinced of Labour's willingness to put UK finances on stable footing now, undermining confidence in GBP.

- From a technical perspective, bullish conditions in EURGBP remain intact and fresh cycle highs reinforce current conditions. A break of 0.8865 would put attention on 0.8893, a Fibonacci projection. For GBPUSD, immediate support stands at 1.3085, the Nov 12 low, a break of which would open up 1.3010, the Nov 4 & 5 low and the bear trigger.

- EURCHF meanwhile has pierced significant support during this morning's volatility, with the 0.9206-0.9211 zone having held prices well just last month, as well as twice last year. As a result, prices hit the lowest levels since the withdrawal of the 1.20 floor in 2015 but have since recovered back above 0.9200. Markets will be closely watching both the formation of the daily candle (as well as the weekly candle) for any evidence prices are trying to find a bottom.

- Markets await any firm schedules for data releases from US statistics agencies after the government reopen following yesterday's BLS announcement they are working to release information "as soon as possible". Canada manufacturing / wholesale sales are on the calendar for today next to ECB's Lane and a set of Fed speakers. Further UK fiscal headlines would also be met with attention.

OPTIONS: Expiries for Nov14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1625(E1.5bln), $1.1650(E760mln)

- GBP/USD: $1.2970(Gbp639mln)

- AUD/USD: $0.6600(A$670mln), $0.6750(A$2.2bln)

- AUD/NZD: N$1.1350-60(A$753mln)

- USD/CAD: C$1.4015-35($1.9bln)

EQUITIES: Thursday's Sell-Off in E-Mini S&P Appears Corrective

- A medium-term bull trend in Eurostoxx 50 futures remains intact and this week’s gains reinforce bullish conditions. Note that the sharp pullback Thursday appears to be a correction - for now. A resumption of gains would signal scope for a climb towards 5853.50 next, the top of a bull channel drawn from the Aug 1 low. On the downside, initial firm support is seen at 5676.84, the 20-day EMA.

- The trend condition in S&P E-Minis remains bullish and Thursday’s selloff appears corrective - for now. Attention is on support at the 50-day EMA, at 6729.38. A clear break of the EMA, and of support at 6655.50, the Nov 7 low, would highlight a short-term reversal and signal scope for a deeper correction. Initial firm resistance to watch is 6900.50, the Nov 12 high. A breach of this hurdle would be a bullish development.

COMMODITIES: Continuation Lower for WTI Could Expose Bear Trigger at $55.96

- A sell-off in WTI futures on Tuesday strengthened a bearish theme. A continuation lower would pave the way for a move towards key support and the bear trigger at $55.96, the Oct 20 low. Clearance of this level would confirm a resumption of the downtrend. Note that it is still possible a bullish corrective cycle remains in play. Resistance to watch is $62.59, the Oct 24 high. Clearance of this hurdle would signal scope for a stronger correction.

- Gold is trading closer to this week’s high. The downleg since Oct 20 appears to have been a correction and has allowed an overbought condition to unwind. Recent gains suggest that correction is over. Key support lies at the 50-day EMA, at $3921.1. Clearance of this EMA would signal scope for a deeper retracement. For bulls, a continuation higher would pave the way for a test of $4381.5, the Oct 20 high and bull trigger.

| Date | GMT/Local | Impact | Country | Event |

| 14/11/2025 | 1330/0830 | ** | Monthly Survey of Manufacturing | |

| 14/11/2025 | 1330/0830 | ** | Wholesale Trade | |

| 14/11/2025 | 1330/0830 | *** | Retail Sales | |

| 14/11/2025 | 1330/0830 | *** | PPI | |

| 14/11/2025 | 1330/0830 | *** | PPI | |

| 14/11/2025 | 1330/1430 | ECB Elderson Remarks at COP30 Finance Day | ||

| 14/11/2025 | 1500/1000 | * | Business Inventories | |

| 14/11/2025 | 1500/1600 | ECB Lane Panel at Workshop on International Macroeconomics and Finance | ||

| 14/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 14/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/11/2025 | 1930/1430 | Dallas Fed's Lorie Logan | ||

| 14/11/2025 | 2020/1520 | Atlanta Fed's Raphael Bostic | ||

| 15/11/2025 | 1330/1430 | ECB Schnabel Chairs Panel at Econ/FinStab Conference |