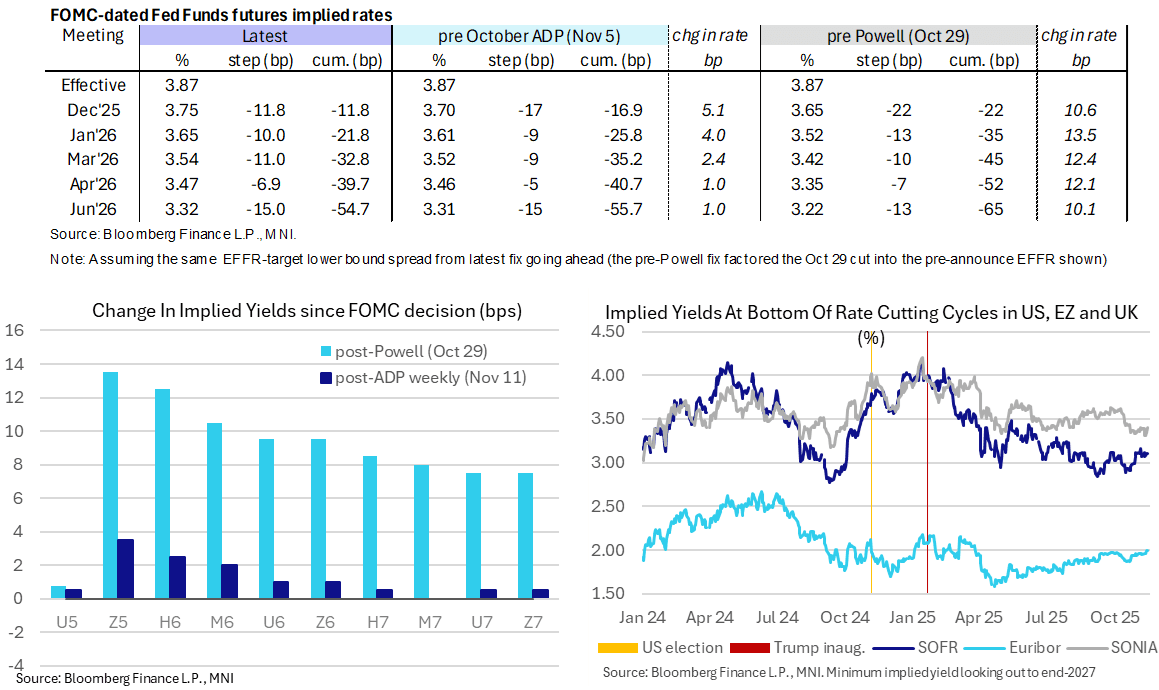

STIR: US Rates Consolidate Hawkish Near-Term Shift, More Hawkish Fedspeak Ahead

- Fed Funds implied rates are unchanged overnight for the next two meetings and only 0.5-1bp lower for those out to mid-2026 after yesterday pushing to ~50/50 odds of a pause next month.

- Cumulative cuts from 3.87% effective: 12bp Dec, 22bp Jan, 33bp Mar, 39.5bp Apr, 54.5bp Jun.

- SOFR futures are broadly unchanged, with the front end still clearly leading volumes but

- The SOFR implied terminal yield holds at 3.105% (SFRH7). It’s +4bp from Tuesday’s close having digested the soft weekly ADP print but still off the multi-month high close of 3.16% from last Wednesday after more encouraging monthly ADP and especially ISM Services data.

- Today’s Fedspeak comes from those at the hawkish end of the FOMC, notably Schmid and Logan but also Bostic who has recently called for holding rates until inflation is moving to 2% whilst seeing price pressures persist until mid-to-late 2026.

- 1005ET – Kansas City Fed’s Schmid ('25) on mon pol and outlook (text tbd). These will be his first remarks since his dissenting statement having last month voted to keep rates on hold. He judges that a rate cut can’t address the structural changes in the job market and that policy is only modestly restrictive.

- 1430ET - Dallas Fed’s Logan ('26) in fireside chat (no text)

- 1520ET - Atlanta Fed’s Bostic (non-voter) in moderated discussion (no text)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

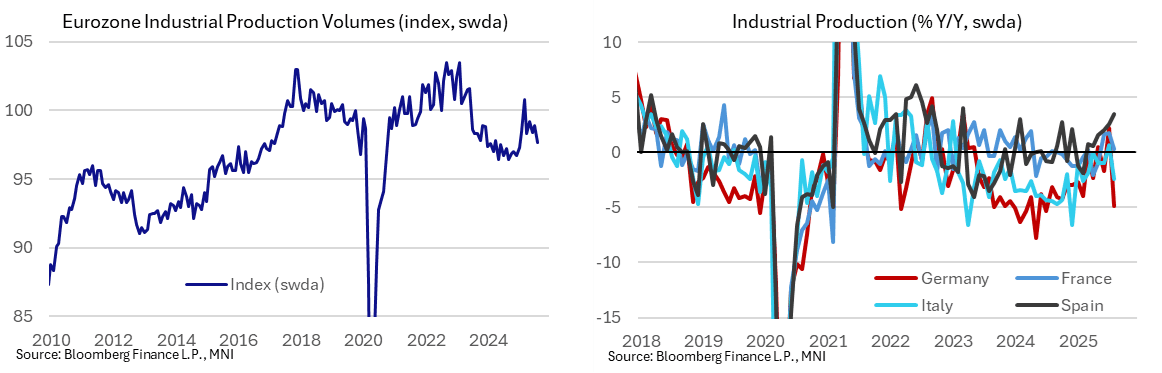

EUROZONE DATA: Ireland Boosts August IP But Weakness Broad Across Big 4, Sectors

Euro area industrial production fell -1.2% M/M in August, albeit not as weak as the -1.6% expected after all 'big 4' countries contracted. While a July revision (0.5% from 0.3% unrevised) underpins the upward surprise, Ireland had an outsized positive impact this time, at 9.8% M/M. Sequential weakness was broad-based in August with all main categories except non-durable consumer goods down M/M.

- All four main Eurozone countries saw M/M declines in August, with Germany standing out negatively at -5.2% (auto slump at least in part attributed to holiday closures and production changeovers), France at -0.7%, Italy at -2.4%, and Spain at -0.1%. These compare to July prints of 1.5%, -0.1%, 0.4% and -0.5%, respectively.

- Eurostat added an explicit comment on Ireland's 9.8% M/M print, saying "the high weight of subcontracted production makes the Irish industrial production index volatile, monthly changes can be higher than in other countries". The volatility of the series suggests a risk of reversing in September.

- August weakness was broad-based across sectors, with energy at -0.6% M/M (-1.7% prior), intermediate goods at -0.2% (0.5% prior), capital goods at -2.2% (1.7% prior), durable goods at -1.6% (1.2% prior), and only non-durable goods marginally positive at 0.1% (1.8% prior). Also on a Y/Y comparison, all sectors except non-durable consumer goods (8.2% Y/Y, not unusually high for recent months) saw declines in August.

- The Eurozone Manufacturing PMI dipped back into contraction zone amid lower factory orders in September: "September’s contraction in the headline [Manufacturing] PMI was driven by a reduction in new order inflows and a sharper rate of job shedding. Production volumes continued to expand, although the pace of growth slowed markedly from August’s near three and-a-half-year high."

OPTIONS: Larger FX Option Pipeline

- EUR/USD: Oct15 $1.1600(E1.8bln); Oct16 $1.1500-20(E1.5bln), $1.1580-00(E3.5bln); Oct17 $1.1510-15(E1.7bln), $1.1670-80(E1.0bln)

- USD/JPY: Oct15 Y143.00($1.8bln)

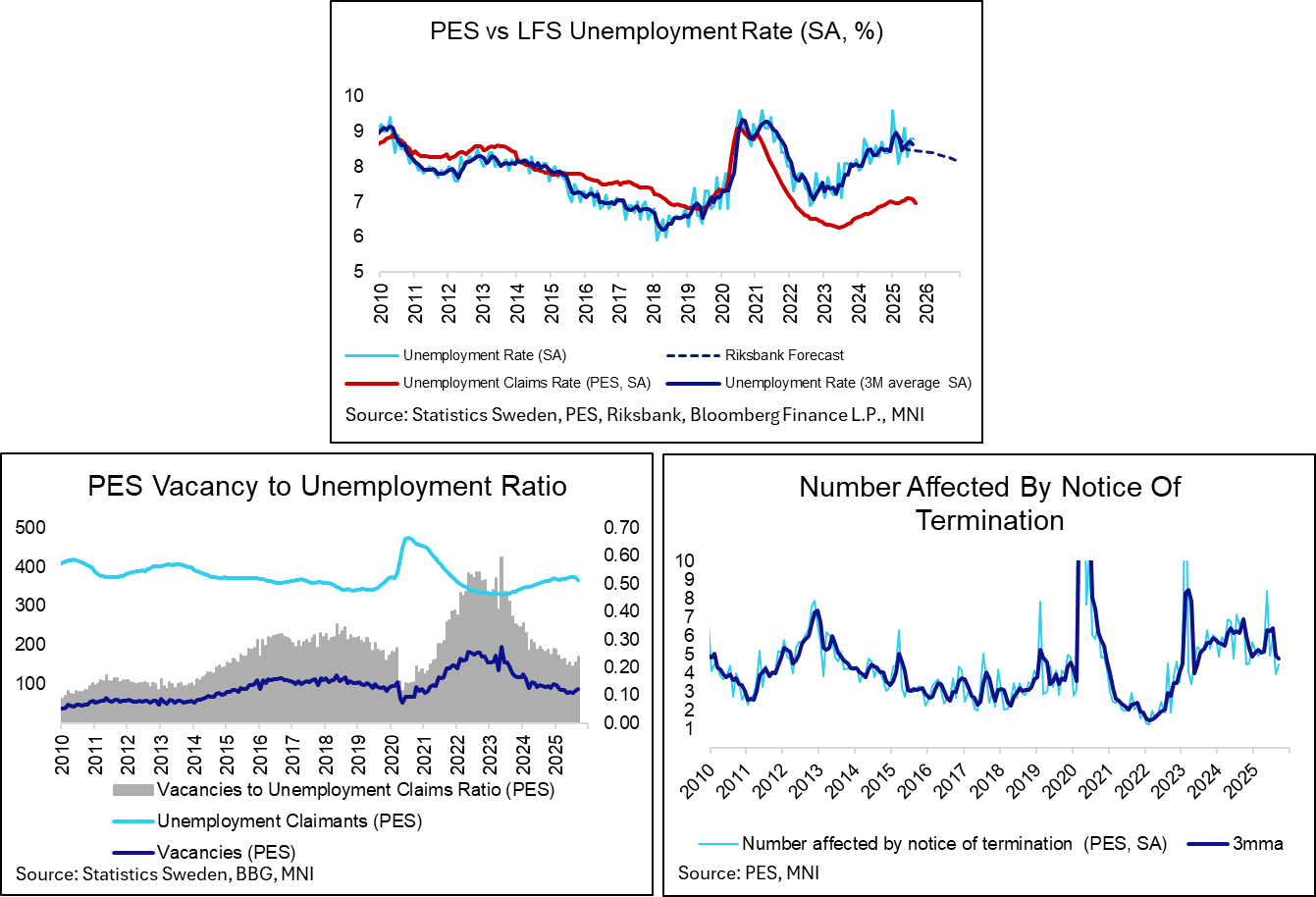

SWEDEN: Stabilising Developments In September PES Labour Market Data

Labour market data from the public employment service (PES) pointed to stabilising developments in September. The Riksbank expects labour market conditions to improve from the start of 2026, so a stabilisation in Q3/Q4 is a necessary first step. LFS unemployment data is due on Friday, with the median analyst expecting an 8.7% unemployment rate (vs 8.8% prior).

- The PES unemployment claims rate eased for the second consecutive month to 6.95% in September (vs 7.06% in August, 7.10% in June and July).

- The stock of vacancies and vacancy growth may have started to bottom out. In September, there were 87k vacancies, up from 81.5k in August for the highest since February. On an annual basis, vacancy growth remains negative a -6% Y/Y, but this is still above August’s -14% and July’s -22%.

- The 3mma of redundancy notices fell to 4,775, down from 4,922 in August for the lowest in over two years.