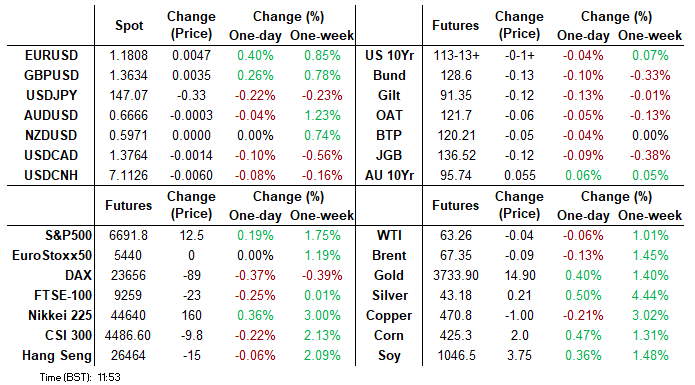

MNI US MARKETS ANALYSIS: Another Fresh All-Time High For Gold

Highlights:

- USD remains on the defensive

- Gold registers another all-time high.

- Today’s focus will fall on US retail sales and Canada CPI data, with US import prices and industrial production also scheduled.

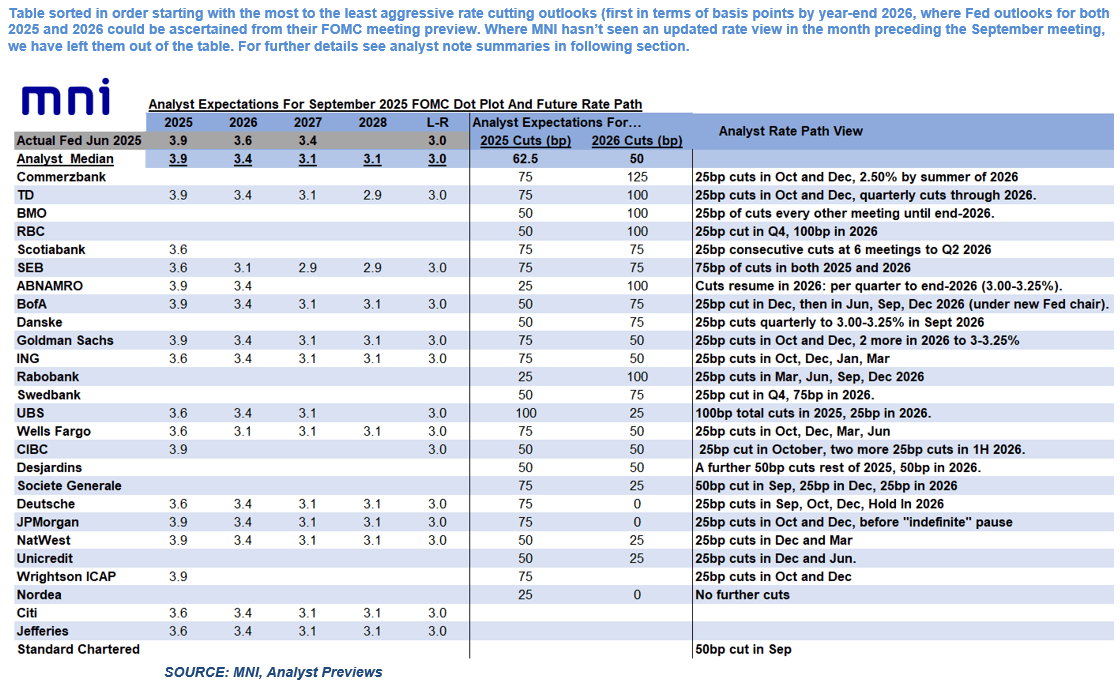

FED: MNI Fed Preview-September 2025: Analyst Outlook

We've published our updated Fed preview, with analyst expectations - Download Full Report Here

September 2025 FOMC Analyst Views: 2 Or 3 Cuts This Year

All but 2 analysts expect a 25bp cut at the September FOMC, based on 32 sell-side previews MNI saw.

- Standard Chartered and Societe Generale expect the FOMC to cut by 50bp.

- Most analysts who expressed an opinion believe that Gov Miran (if confirmed in time for the decision) will dissent in favor of a 50bp or greater cut, with potential for 2 or 3 total dovish dissents (Waller/Bowman).

- Risks of a dissent toward a hold are seen as limited (candidates: Schmid, Goolsbee, Musalem).

- SEP/Dot Plot: Analysts see a slightly lower “dot” profile in the Fed funds medians vs the last edition in June. For 2025 the median is narrowly in favor of a 3.9% (unchanged) end-year median, though many see 3.6%. For 2026 most see 3.4% (down from 3.6% in June), moving to 3.1% by end 2027 (down from 3.4% in June). No analyst sees the longer-run rate changing (3.0%).

- Analysts see the macroeconomic projections remaining relatively unchanged.

- Statement: The statement is widely expected to revise the language around the characterization of the labor market, to reflect the rise in unemployment and slowdown in payrolls growth.

- There are no expectations that the Fed will change the language re the description of inflation, or the 2nd paragraph’s balance of risks. However we saw one expectation that the Fed could alter the forward guidance sentence (Citi: To remove “and timing”).

- Future action: Expectations for total easing in 2025 (including September’s rate cut) ranges from 25bp (ABN Amro, Rabobank, Nordea) to 100bp (UBS). However, the median is 62.5bp, implying a split between 50 and 75bp of easing in 2025 – mirroring expectations of the Dot Plot.

- The median for total cuts by end-2026 is 125bp, ranging from 25bp to 200bp.

US TSYS: Monday Gains Held Ahead Of Retail Sales, Import Prices and 20Y Supply

- Treasuries broadly consolidate yesterday’s modest, headline-light rally, having pared earlier gains that saw 5s to 10s push above yesterday’s range before retreating.

- Today sees a solid data docket headlined by retail sales and import prices, potential comments from President Trump as he departs for the UK after yesterday’s appeals court ruling re his attempt at firing Fed Governor Cook, and 20Y supply.

- Cash yields range from 0.8bp lower (2s) to 0.5bp higher (20s), with upcoming supply possibly behind that modest underperformance for 20s.

- TYZ5 trades at 113-13+ on another tepid overnight session with cumulative volumes at 190k.

- An earlier high of 113-16+ nudged above yesterday’s range although it hasn’t troubled resistance at 113-29 (Sep 5 high), continuing the bullish trend sequence.

- Data: Retail sales Aug (0830ET), Import prices Aug (0830ET), NY Fed services Sep (0830ET), IP/Cap Util Aug (0915ET), NAHB Sep (1000ET), Business inventories Jul (1000ET)

- Coupon issuance: $13bn 20Y re-open - 912810UN6 (1300ET). Last week’s 30Y auction was on the screws but with stronger details. That’s in contrast to last month’s 20Y auction which was in-line but with the bid-to-cover slipping from 2.79 to 2.54 and indirect take-up dropping from 67.4% to 60.6%.

- Bill issuance: $85bn 6W bills (1130ET)

- Politics: Trump departs the White House for London (0830ET, open press pool), Trump lands in London (1520ET)

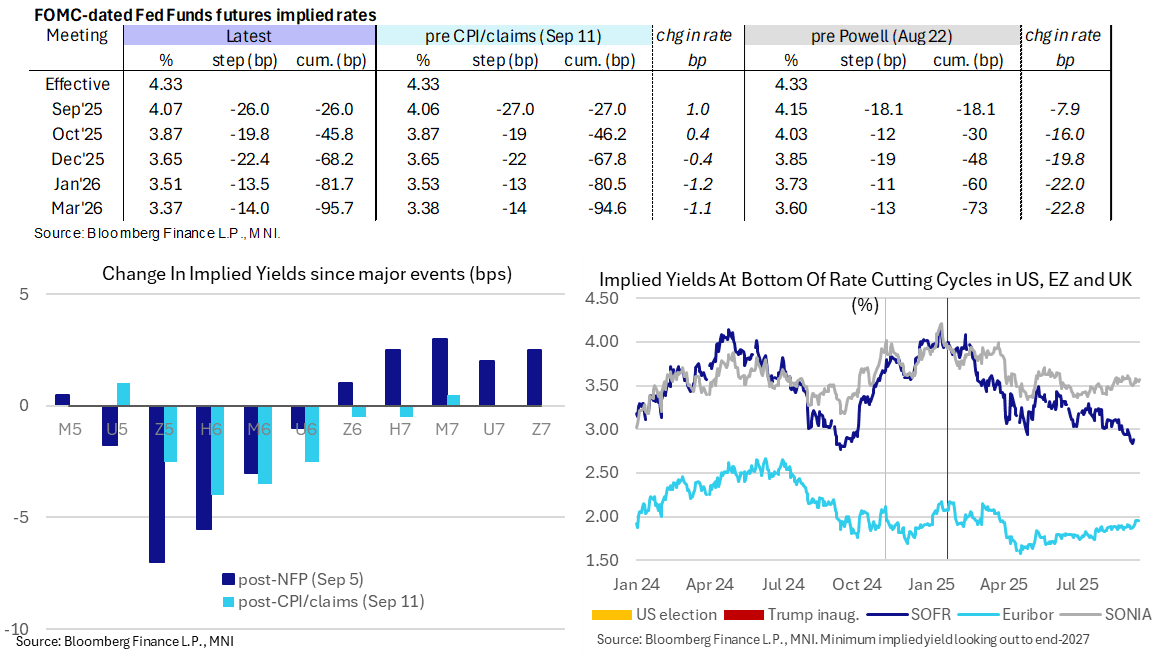

STIR: Holding Off Fully Pricing Three Consecutive Fed Cuts Ahead Of Retail Sales

- Fed Funds implied rates are near unchanged ahead of a solid docket including retail sales for August and a potential final tweak to core PCE tracking from import price data.

- Cumulative cuts from 4.33% effective: 26bp Sep, 46bp Oct, 68bp Dec, 81.5bp Jan and 95bp Mar.

- SOFR futures are near unchanged on the day, including an implied terminal yield of 2.915% eyeing a little more than 140bp of cuts from here.

- CEA’s Miran was confirmed as a Fed Governor in the senate vote yesterday (48-47), serving the final four months of a 14-year term vacated by Kugler. He should be at the FOMC meeting starting today with attention on his likely dissent and just how dovish his dot plot entry will be.

- Trump cannot fire Gov. Cook, according to the U.S. Court of Appeals for the D.C. Circuit, a ruling the Justice Department will likely appeal to the Supreme Court. We take that to mean she will be at this week’s meeting for a full contingent of voters. We should know for sure when the Fed announces that the meeting is underway.

- That said, we re-up yesterday’s MNI interview with administrative law expert Richard Pierce with a warning over Cook’s odds once the case gets to the Supreme Court (MNI INTERVIEW: Cook Could Face Long Odds Before Supreme Court - Sep 15).

US TSY FUTURES: Mix Of Long Setting & Short Cover On Monday

OI data points to a mix of net short cover in the front end of the curve (TU & FV) and net long setting further out (TY, UXY, US & WN) as Tsys ticked higher on Monday, with the latter slightly more prominent in DV01 terms.

| 15-Sep-25 | 12-Sep-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,460,001 | 4,486,120 | -26,119 | -1,057,998 |

FV | 6,784,160 | 6,818,531 | -34,371 | -1,528,906 |

TY | 5,377,833 | 5,372,264 | +5,569 | +381,788 |

UXY | 2,372,083 | 2,365,591 | +6,492 | +594,068 |

US | 1,811,494 | 1,804,632 | +6,862 | +984,802 |

WN | 2,015,269 | 2,010,800 | +4,469 | +845,638 |

|

| Total | -37,098 | +219,392 |

SOFR: Fresh Positions Set Across Much Of Futures Strip On Monday

OI data points to net short setting dominating in the whites, before net long setting came to the fore in the reds, greens and blues, as the SOFR futures strip twist flattened on Monday. Instances of net cover were relatively limited.

| 15-Sep-25 | 12-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,226,388 | 1,231,587 | -5,199 | Whites | +36,849 |

SFRU5 | 1,460,296 | 1,445,541 | +14,755 | Reds | +113,651 |

SFRZ5 | 1,687,814 | 1,661,741 | +26,073 | Greens | +1,475 |

SFRH6 | 1,193,610 | 1,192,390 | +1,220 | Blues | +24,843 |

SFRM6 | 1,015,538 | 997,991 | +17,547 |

|

|

SFRU6 | 939,719 | 908,441 | +31,278 |

|

|

SFRZ6 | 1,031,355 | 1,015,659 | +15,696 |

|

|

SFRH7 | 759,079 | 709,949 | +49,130 |

|

|

SFRM7 | 821,609 | 823,158 | -1,549 |

|

|

SFRU7 | 679,741 | 685,106 | -5,365 |

|

|

SFRZ7 | 694,945 | 690,926 | +4,019 |

|

|

SFRH8 | 452,127 | 447,757 | +4,370 |

|

|

SFRM8 | 368,093 | 361,590 | +6,503 |

|

|

SFRU8 | 262,818 | 251,246 | +11,572 |

|

|

SFRZ8 | 265,019 | 259,301 | +5,718 |

|

|

SFRH9 | 183,370 | 182,320 | +1,050 |

|

|

EUROPEAN & UK ISSUANCE UPDATE:

2.20% Oct-30 Bobl Results

E4.5bln (E3.491bln allotted) of the 2.20% Oct-30 Bobl. Avg yield 2.29% (bid-to-offer 1.35x; bid-to-cover 1.74x).

6/10-year RFGB Results

E628mln of the 0.75% Apr-31 RFGB. Avg yield 2.572% (bid-to-cover 1.69x).

E874mln of the 3.00% Sep-35 RFGB. Avg yield 3.067% (bid-to-cover 1.48x).

SlovGB Results

E97mln of the 3.625% Jun-33 SlovGB. Avg yield 3.1858% (bid-to-cover 5.09x).

E229mln of the 3.75% Feb-35 SlovGB. Avg yield 3.4175% (bid-to-cover 4.30x).

E81mln of the 0.375% Apr-36 SlovGB. Avg yield 3.5381% (bid-to-cover 3.72x).

E105mln of the 4.00% Feb-43 SlovGB. Avg yield 4.04% (bid-to-cover 3.85x).

4.375% Jan-40 Gilt Results

Relatively soft auction of the 4.375% Jan-40 gilt with a 0.9bp tail seeing the LAP (lowest accepted price) come in at 93.090 - below the pre-auction mid-price of 93.144 (a price that was exaggerated a little itself by a move higher into the end of the bidding window. Prior to that the prevailing level had been around 93.116.

- Either way this short 15-year auction will be seen as slightly disappointing and the price fell immediately after to 93.051 (before moving back to broadly in line with the auction LAP at writing).

GBP3bln of the 4.375% Jan-40 Gilt. Avg yield 5.048% (bid-to-cover 2.95x, tail 0.9bp).

FOREX: EUR Wrap – EURJPY Grinding Towards Double Top Resistance

EURUSD’s steady approach to cycle highs at 1.1829 is garnering attention as we approach the Fed. SocGen have noted that the relatively low RSI compared to the move earlier in the year is a good sign and that the chances of a move to 1.20 this month have improved. They highlight that relative growth forecasts, relative rates, and the overall market backdrop are all on the euro’s side, for now.

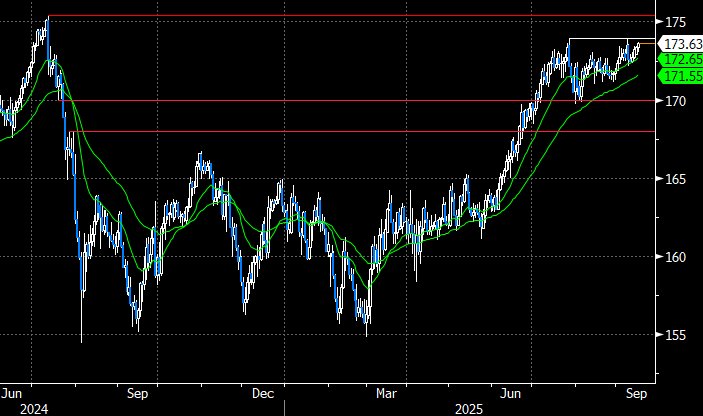

- Wednesday’s Fed decision will keep short-term dollar sentiment as the primary driver for currency markets, however, the plethora of other major central bank decisions places heightened attention on a number of EUR crosses and their significant chart levels this week.

- As noted earlier, EURJPY (shown below) has been grinding towards double top resistance just below the 174 handle. Moving average studies are in a bull-mode position too, highlighting a primary uptrend. A break of 173.97 would open 174.86 (Fib projection) before 175.43, a key medium-term level. Japan’s leadership race heating up and the Bank of Japan decision due Friday provide obvious catalysts to a breakout.

- UK CPI data and the BOE decision Thursday will likely keep the market’s attention on GBP. For EURGBP specifically, the latest pullback in EURGBP appears corrective. Support to watch lies at 0.8597, the Aug 14 low. Clearance of this level would cancel a bull theme and reinstate a recent bearish threat.

- Fresh cycle highs for EURCAD on Monday continue to place the cross at the highest level since 2009. 1.6329 provides the next horizontal resistance point as we approach today’s Canada CPI and tomorrow’s BOC decision, where the central bank is expected to cut by 25bps.

Source: Bloomberg Finance L.P. / MNI

FOREX: US Dollar Extending Lower, EUR & JPY Lead Gains

Following a similar theme to Monday’s session, the USD index is down 0.2% today, extending its grind lower to reach the lowest levels since early July. The index is now within 1% of the multi-year lows as we approach tomorrow’s Fed decision, which reside at 96.38. Continued strong performance for major equity indices and the more activist approach to Fed personnel management from the White House are providing greenback headwinds.

- In slight contrast today, it’s the majors which are outperforming, led by the likes of EUR and JPY. This has prompted a EURUSD (+0.40%) print above 1.18, as the pair narrows the gap to the cycle highs and key resistance at 1.1829. Clearance of this hurdle would confirm a resumption of the primary uptrend and immediately target the Sep 10 2021 high at 1.1851.

- Unsurprisingly, action has been centred around the Japanese yen, with USDJPY trading a 146.70-147.54 range already on Tuesday. The Yen was supported overnight by agricultural minister Koizumi’s intention to run for LDP leader. Finance Minister Kato is set to run his election campaign, providing a more hawkish (with respect to both fiscal and monetary policy) option compared to opinion poll leader Takaichi. USDJPY has subsequently settled back at 147.00 and key short-term support to watch remains at 146.21, the Aug 14 low and a bear trigger.

- In line labour market data from the UK has allowed GBP to continue its ascent against the dollar this morning, following yesterday’s breach of key resistance at 1.3595. The break strengthens bullish conditions and opens 1.3681, the July 4 high.

- It’s worth highlighting that AUDNZD briefly broke to the highest level since 2022 at 1.1191, however, momentum quickly stalled with the cross reversing back to 1.1160. New Zealand GDP is due Thursday local time, shortly before Australian employment data for August.

- Today’s focus will be on US retail sales and Canada CPI data, with US import prices and industrial production also scheduled.

FOREX OPTIONS: Expiries for Sep16 NY cut 1000ET (Source: DTCC)

- EURUSD: 1.1700 (322mln), 1.1710 (542mln), 1.1715 (727mln), 1.1725 (292mln), 1.1730 (231mln), 1.1750 (1.59bn), 1.1760 (895mln), 1.1800 (1.59bn).

- GBPUSD: 1.3600 (368mln).

- USDJPY: 146.50 (360mln), 146.60 (543mln), 147.00 (568mln), 147.50 (470mln).

- AUDUSD: 0.6600 (550mln).

EQUITIES: S&P E-Minis Bull Cycle Extends

A bull cycle in S&P E-Minis remains intact and the contract has started this week on a bullish note. Fresh cycle highs reinforce current bullish conditions. The move higher confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on the 6700.00 handle next and 6712.33, a 1.764 projection of the Aug 20 - 28 - Sep 2 price swing. Initial support to watch is 6559.62, the 20-day EMA.

- EUROSTOXX 50 futures remain firm. The contract has recently traded through the 20-day EMA - a bullish development. The move higher undermines a recent bearish theme and signals potential for a climb towards 5522.0, the Aug 26 high and a bull trigger. On the downside, support has been defined at 5292.00, the Sep 2 low. Clearance of this level is required to reinstate a bearish theme.

COMMODITIES: Gold Bulls Still In Charge

Gold remains in a clear bull cycle and has started the week on a firmer note - yesterday the metal traded to a fresh all-time high, once again. The break higher confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is the $3700.00 handle and $3705.2, a 1.382 projection of the May 15 - Jun 16 - 30 price swing. Initial firm support lies at $3532.8, the 20-day EMA.

- In the oil space, the trend condition in WTI futures is unchanged - a bear cycle remains intact and short-term gains are considered corrective. The pullback from the Sep 2 high highlights a possible recent reversal and the end of a corrective phase between Aug 13 - Sep 2. Initial resistance to watch is $66.03, the Sep 2 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would open $57.71, the May 30 low.

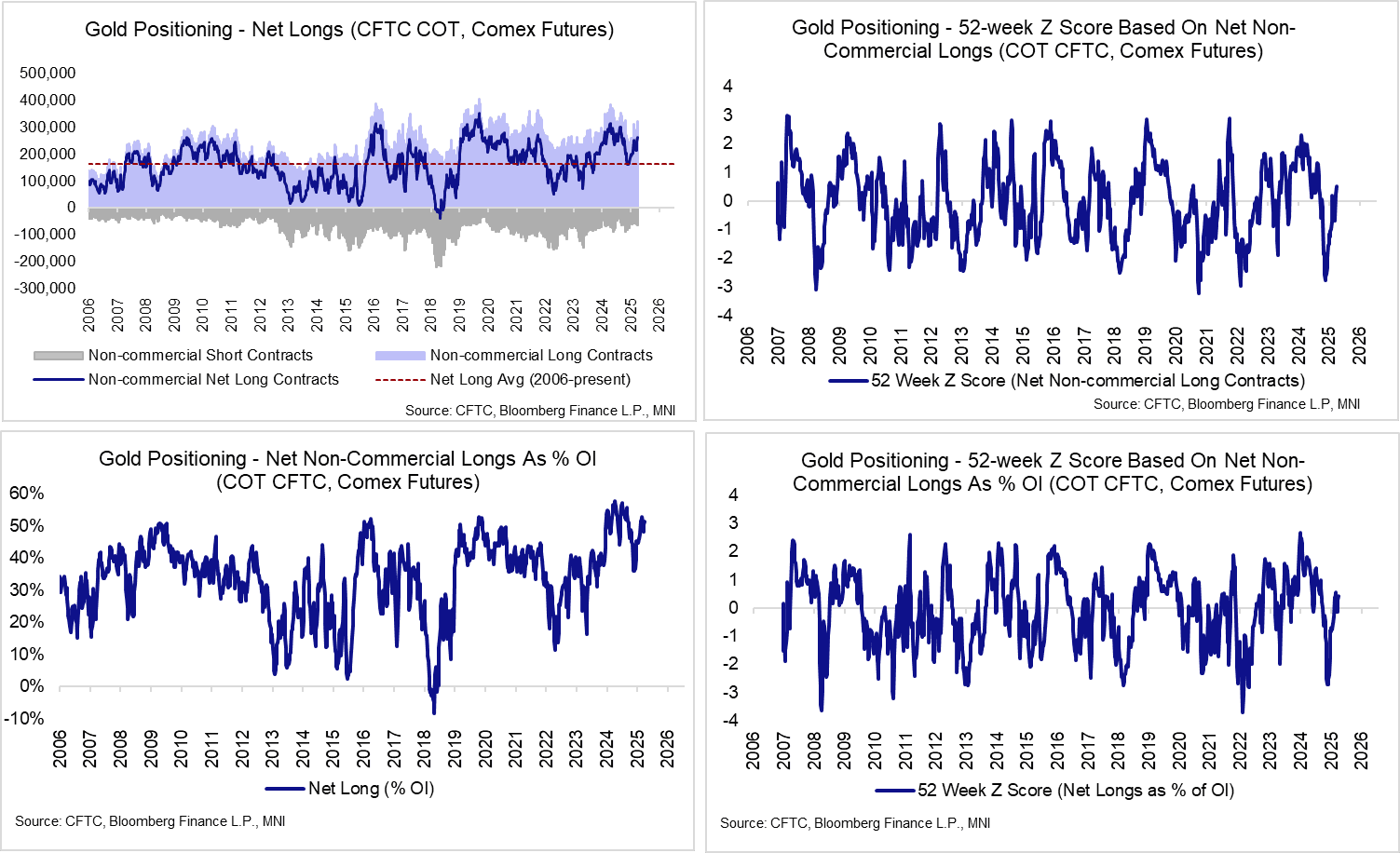

GOLD: Spot Approaching Round Number Resistance At $3,700

Spot gold is approaching round number resistance at $3,700, clearance of which would expose Fibonacci projection levels of $3,705.2 (1.382 proj) and $3,744.2 (1.500 proj). A clear bull cycle remains intact, with initial support not seen till $3,614, the Sep 11 low.

- The sharp rally in gold since mid-August has been a combination of Fed independence concerns (amid the ongoing Lisa Cook saga and the more activist approach to Fed personnel management from the White House) and expectations for the resumption of Fed easing. These tailwinds come alongside a backdrop of persistent, relatively price-insensitive, central bank demand.

- Spot has been in overbought territory on a 14-day RSI basis since the start of September, but this has not restricted the recent rally so far.

- Positioning metrics (as of last Tuesday) are unsurprisingly extending further into net long territory, but the indicators we track are still not at historically stretched levels (see charts).

- The signals emanating from tomorrow’s Fed decision present the main near-term risk for gold. Although spot price action has diverged from real US rates since 2022, lower yields should benefit non-yielding bullion on a relative basis going forward.

| Date | GMT/Local | Impact | Country | Event |

| 16/09/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/09/2025 | 1230/0830 | *** | CPI | |

| 16/09/2025 | 1230/0830 | *** | Retail Sales | |

| 16/09/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 16/09/2025 | 1230/0830 | *** | Retail Sales | |

| 16/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 16/09/2025 | 1315/0915 | *** | Industrial Production | |

| 16/09/2025 | 1400/1000 | * | Business Inventories | |

| 16/09/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 16/09/2025 | 1400/1000 | * | Business Inventories | |

| 16/09/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 16/09/2025 | - | Bank of Canada Meeting | ||

| 17/09/2025 | 0600/0800 | ** | Unemployment | |

| 17/09/2025 | 0600/0700 | *** | Consumer inflation report | |

| 17/09/2025 | 0730/0930 | ECB Lagarde at ECB Annual Research Conference | ||

| 17/09/2025 | 0800/1000 | ECB Cipollone At Associazione Bancaria Italiana EC Meeting | ||

| 17/09/2025 | 0900/1100 | *** | EZ HICP Final | |

| 17/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 17/09/2025 | 1115/1315 | ECB Cipollone Speaks at Netherlands Central Bank Resilience Conference | ||

| 17/09/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/09/2025 | 1230/0830 | *** | Housing Starts | |

| 17/09/2025 | 1230/0830 | *** | Housing Starts | |

| 17/09/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 17/09/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 17/09/2025 | 1430/1030 | BOC press conference | ||

| 17/09/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 17/09/2025 | 1800/1400 | *** | FOMC Statement | |

| 18/09/2025 | 2245/1045 | *** | GDP |