FED: MNI Fed Preview-September 2025: Analyst Outlook

We've published our updated Fed preview, with analyst expectations - Download Full Report Here

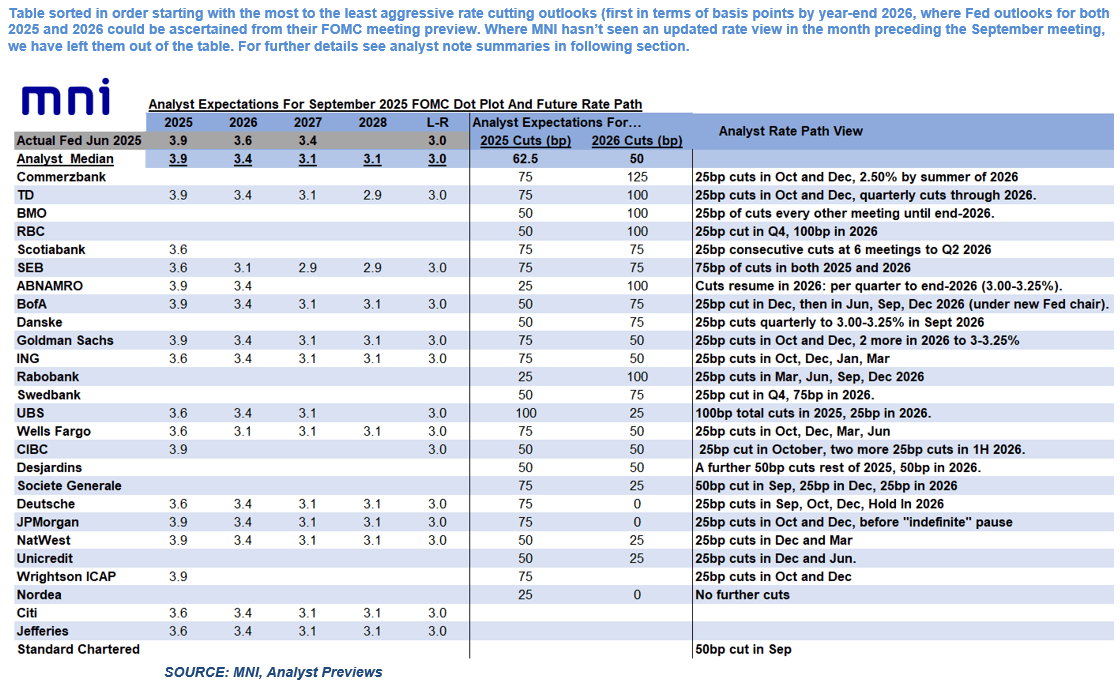

September 2025 FOMC Analyst Views: 2 Or 3 Cuts This Year

All but 2 analysts expect a 25bp cut at the September FOMC, based on 32 sell-side previews MNI saw.

- Standard Chartered and Societe Generale expect the FOMC to cut by 50bp.

- Most analysts who expressed an opinion believe that Gov Miran (if confirmed in time for the decision) will dissent in favor of a 50bp or greater cut, with potential for 2 or 3 total dovish dissents (Waller/Bowman).

- Risks of a dissent toward a hold are seen as limited (candidates: Schmid, Goolsbee, Musalem).

- SEP/Dot Plot: Analysts see a slightly lower “dot” profile in the Fed funds medians vs the last edition in June. For 2025 the median is narrowly in favor of a 3.9% (unchanged) end-year median, though many see 3.6%. For 2026 most see 3.4% (down from 3.6% in June), moving to 3.1% by end 2027 (down from 3.4% in June). No analyst sees the longer-run rate changing (3.0%).

- Analysts see the macroeconomic projections remaining relatively unchanged.

- Statement: The statement is widely expected to revise the language around the characterization of the labor market, to reflect the rise in unemployment and slowdown in payrolls growth.

- There are no expectations that the Fed will change the language re the description of inflation, or the 2nd paragraph’s balance of risks. However we saw one expectation that the Fed could alter the forward guidance sentence (Citi: To remove “and timing”).

- Future action: Expectations for total easing in 2025 (including September’s rate cut) ranges from 25bp (ABN Amro, Rabobank, Nordea) to 100bp (UBS). However, the median is 62.5bp, implying a split between 50 and 75bp of easing in 2025 – mirroring expectations of the Dot Plot.

- The median for total cuts by end-2026 is 125bp, ranging from 25bp to 200bp.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (U5) Follows Fade in Treasuries

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.960 - High Apr 7

- PRICE: 95.710 @ 15:17 BST Aug 15

- SUP 1: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.707 - 1.0% 10-dma envelope

Aussie 10-yr futures received a boost from the US Treasury rally that followed both the recent poor NFP print as well as Tuesday’s inflation number. While this impact faded into the close of the week, 10-year futures remain toward the top end of the recent range. To the upside, next resistance is at 96.207, a Fibonacci retracement point. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition.

FOREX: USD Index Pinned to 50-dma as Putin Shakes Hands with Trump

- USD slipped against all others Friday, with a poor set of retail sales and Uni of Michigan sentiment numbers meeting a higher-than-expected import price index to further stimulate concerns over a stagflarionary phase in the US economy. The USD Index trades either side of the 50-dma which, notably, has begun to flatten out after maintaining a solid downtrend throughout 2025.

- JPY is the strongest currency in G10, extending the breakout and bearish conclusion of the consolidation phase in USD/JPY. Recent weakness puts the price through support drawn off the early August lows as well as 146.71, a key retracement. Price action this week marks a full reversal of the previously overbought condition, keeping the downside argument in focus.

- Anticipation ahead of the Putin-Trump meeting has reached fever pitch. Footage showing the Presidents shaking hands in Alaska has helped ease concerns over a hostile meeting, but it's the outcomes that will matter to markets - particularly as equities hold at alltime highs. Any signs of progress toward a ceasefire would be warmly received by risk sentiment - although both Trump and Putin cautioned against a optimistic outcome in comments to press.

- We noted earlier in the week the pressure building on USD/HKD, with price action not matching the pattern of HKMA intervention. That move extended overnight, and is still building at typing, putting spot down to new pullback lows of 7.8119 shortly after the European open. Overnight swap rates have surged further still Friday (hitting 1.7% at typing), well ahead of the 0.3% prevailing rate mid-week and should continue to support a recovery in HIBOR fixes ahead. Today's 1m HIBOR fixed higher by 41bps, hitting 1.45% for the highest fix since mid-May. It's these factors that should work against the HKD carry trade (selling HKD, buying USD), evident in the further tightening of the HKD forward discount today: down 975 points from as high as 1270 this month.

- Focus in the coming week shifts to Jackson Hole and Powell's comments on Friday. With the September meeting still in flux - any conviction toward tipping the board toward a rate cut at the next FOMC will be carefully watched, but it's a hawkish outturn that could be more consequential for markets, as OIS prices a near 90% chance of easing on September 17th.

MNI: US TSY TICS NET FLOWS IN JUN +$77.8B

- MNI: US TSY TICS NET FLOWS IN JUN +$77.8B

- US TSY TICS NET L-T FLOWS IN JUN +$150.8B