MNI US MARKETS ANALYSIS - 3y Tsy Supply the Focus

Highlights:

- BoE pricing eases, GBP slips as UK jobs data takes turn for the worse

- US-China trade talks resume in London, seen lasting all day

- Calendar light of speakers and data, keeping focus on US 3y Treasury supply

US TSYS: Mildly Richer Amidst Thin Volumes; 3Y Supply And Headline Watching

- Treasuries are modestly firmer across the curve, broadly close to earlier highs that have been helped on balance by some intraday weakness in equities in late Asia/early London trading that appears light on drivers.

- Today’s Treasury market focus will be on 3Y supply at the usual 1300ET in what’s otherwise a headline-watching session amidst a blank data docket.

- Today is the second day of US-China trade talks in London (“We are doing well with China. China’s not easy,” Trump told reporters at the White House on Monday. “I’m only getting good reports”). Trump is also set to deliver remarks at Fort Bragg at 1600ET. The WSJ reported that roughly 700 marines are deploying to LA in immigration-related protests.

- Cash yields are 2-3bp lower across the curve.

- Curves sit close to Friday’s recent flats, including 5s30s at 85.5bp vs Friday’s 82.8bps.

- TYU5 trades close to an earlier high of 110-12 (+ 06+) on very low cumulative volumes of 220k.

- The move extends Monday’s lift off Friday’s low of 109-28 as it starts to eye resistance at 110-20 (50-day EMA). A bear threat is still present though with support at 109-26 (May 29 low).

- Data: NFIB small business survey (98.8 vs 96.0 cons after 95.8)

- Coupon issuance: US Tsy to sell $58bn 3Y note - 91282CNH0 (1300ET). Last month’s 3Y saw a small stop (0.2bp) and the bid-to-cover tick up from 2.47x to 2.56x but the indirect take-up retreated.

- Bill issuance: US Tsy to sell $55bn 6-W and $48bn 52-W (1130ET)

STIR: Fed Implied Rates A Touch Softer One Day Out From CPI

- Fed Funds implied rates are up to 1.5bp lower on the day for 2025 meetings, following a pullback off overnight highs in US equity futures following weakness in China and HK equities.

- US-China talks in London have entered a second day today.

- Cumulative cuts from 4.33% effective: 0bp Jun (next week), 3.5bp Jul, 18bp Sep, 30bp Oct and 46bp Dec.

- The SOFR implied terminal yield of 3.355% (SFRZ6, -2bp) is back closer to ~100bp of cuts having closed Friday at ~90bp of cuts ahead.

- Markets will be on headline watch today with a blank data docket after the earlier release of the NFIB small business survey. US CPI is in focus tomorrow (MNI Preview).

US INFLATION: MNI US CPI Preview: An Important Pre-FOMC Steer

- We have published and e-mailed to subscribers the MNI US CPI Preview.

- Please find the full report including MNI analysis plus detailed analyst estimates, here: https://media.marketnews.com/USCPI_Prev_Jun2025_a86717a017.pdf

- Analyst unrounded estimates see core CPI inflation accelerating mildly to 0.27% M/M (median, 0.28% average) in May after 0.24% M/M in April.

- We’ve seen an unrounded range of 0.23-0.34% M/M, with some sizeable discrepancies in used cars and lodging away from home as well as a CPI-specific airfares.

- The broad assumption is that May could have started to see a greater tariff impact than April but that firmer increases are more likely to show in summer months.

- Both headline and core CPI Y/Y inflation should firm one to two tenths after lows since early 2021, whilst the six-month core rate should see a similar print after four months running hotter than the Y/Y.

- We have seen preliminary core PCE estimates center on 0.22% M/M for May (median, 0.24% average), due the usual updates after Wednesday’s CPI and Thursday’s PPI. One area to watch in the latter will the extent of a bounce in portfolio management and investment advice after sliding with equities in April.

- The Fed rate path is close to its most hawkish since February, with a next cut fully priced for October.

- A dovish surprise could see a more limited reaction on the assumption that strength is yet to come for consumer prices, unless it’s seen across some of the less volatile services components. On the flipside, an upside surprise can see a further kicking out of rate cut expectations and could tee up a hawkish Fed SEP.

US TSY FUTURES: Short Cover Seemed To Dominate On Monday

OI data points to a mix of net long setting (TU, UXY & WN) and short cover (FV, TY & US) in Tsy futures as the contracts ticked higher on Monday.

- Net short cover provided the more meaningful impulse in curve-wide terms.

| 09-Jun-25 | 06-Jun-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 3,956,555 | 3,919,482 | +37,073 | +1,463,769 |

FV | 6,782,892 | 6,828,544 | -45,652 | -1,989,750 |

TY | 4,773,364 | 4,812,773 | -39,409 | -2,604,935 |

UXY | 2,300,994 | 2,293,709 | +7,285 | +634,159 |

US | 1,722,226 | 1,731,668 | -9,442 | -1,295,726 |

WN | 1,889,366 | 1,887,856 | +1,510 | +274,246 |

|

| Total | -48,635 | -3,518,237 |

STIR: Net Long Setting Most Prominent In SOFR Futures On Monday

OI data points to net long setting dominating in most SOFR futures as the strip saw some light bull flattening on Monday. Only modest rounds of net short cover were seen.

| 09-Jun-25 | 06-Jun-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,068,096 | 1,067,105 | +991 | Whites | +4,738 |

SFRM5 | 1,431,932 | 1,428,926 | +3,006 | Reds | +32,678 |

SFRU5 | 1,153,856 | 1,149,852 | +4,004 | Greens | +3,778 |

SFRZ5 | 1,132,241 | 1,135,504 | -3,263 | Blues | +2,883 |

SFRH6 | 867,535 | 836,398 | +31,137 |

|

|

SFRM6 | 826,474 | 829,154 | -2,680 |

|

|

SFRU6 | 750,132 | 748,572 | +1,560 |

|

|

SFRZ6 | 864,252 | 861,591 | +2,661 |

|

|

SFRH7 | 676,560 | 679,168 | -2,608 |

|

|

SFRM7 | 590,191 | 587,139 | +3,052 |

|

|

SFRU7 | 422,241 | 417,480 | +4,761 |

|

|

SFRZ7 | 406,580 | 408,007 | -1,427 |

|

|

SFRH8 | 302,377 | 300,789 | +1,588 |

|

|

SFRM8 | 219,274 | 216,317 | +2,957 |

|

|

SFRU8 | 168,860 | 169,592 | -732 |

|

|

SFRZ8 | 170,954 | 171,884 | -930 |

|

|

US-CHINA: Lutnick-'Expect Talks To Go On All Day Today'

With the second day of talks in London between senior US and Chinese trade delegations starting at 10:43BST, US Commerce Secretary Howard Lutnick says on entering Lancaster House that talks are "going well" and that he expects them "to go all day today". Talks are not centred on US 'reciprocal' or other tariffs, but instead at working to mitigate Chinese export controls on rare earths and other critical minerals that are seen to threaten US supply chains.

- Alongside Lutnick, Treasury Secretary Scott Bessent and USTR Jamieson Greer are present, while the Chinese side is led by Vice Premier He Lifeng. As Reuters reports, "The inclusion of Lutnick, whose agency oversees export controls for the U.S., is one indication of how central rare earths have become. China holds a near-monopoly on rare earth magnets, a crucial component in electric vehicle motors...[After call, President Trump said President Xi] agreed to resume shipments to the U.S. of rare earths minerals and magnets, and Reuters reported that China has granted temporary export licenses to rare-earth suppliers of the top three U.S. automakers. But tensions remain high over the export controls, after factories around the world started to fret that they would not have enough of the materials they need to keep operating."

EUROPE ISSUANCE UPDATE:

Gilt syndication: Priced

- GBP5.5bln (MNI expected GBP3.5-5.0bln nominal) of the new 1.75% Sep-38 I/L gilt. Reoffer: 100.061 to yield 1.7449%. Spread set at 1.125% Nov-37 I/L gilt +11.75bp (guidance was +11.75/+12.25bps), books closed in excess of GBP61bln.

ESM syndication: Final terms

- E2bln WNG (MNI expected a transaction today with a E1-3bln size) of the new Nov-28 ESM-Bond. Spread set at MS+12 (guidance was MS+15 area), books above EU15bln.

Netherlands auction results

- E2.45bln of the 2.50% Jul-35 DSL. Avg yield 2.749%.

German auction results

- E4bln (E3.078bln allotted) of the 2.40% Apr-30 Bobl. Avg yield 2.14% (bid-to-offer 1.41x; bid-to-cover 1.83x).

Finland auction results

- E733mln of the 1.50% Sep-32 RFGB. Avg yield 2.677% (bid-to-cover 1.53x).

- E758mln of the 0.50% Apr-43 RFGB. Avg yield 3.365% (bid-to-cover 1.63x).

FOREX: GBP Dip Bottoms Out Ahead of Key EMA Support

- GBP has broken lower on the back of a poorer-than-expected labour market report. Average weekly earnings came in softer-than-expected at 5.3% vs. Exp. 5.5% and the monthly change in payrolled employees dropped sharply: to -109k vs. Exp. -20k, with the April figure also subject to a downward revision. As a result, the UK jobs picture and the latest insight into wage growth have been marked lower relative to the Bank of England's projections, raising the odds of a more activist approach from the MPC.

- As a result, BoE OIS markets have returned closer to 2 x 25bps rate cuts for this year, with September close to fully priced for the next cut. Risks to this position, however, include revisions to these numbers in subsequent releases, which have a track record in correcting data outliers.

- Weakness in GBP came in two phases this morning, first on the soft payrolls data, and then again on the SONIA open, with GBPUSD nearing 1.3462, its 20-day EMA. A clear break of this average would suggest potential for a

deeper correction and expose the 50-day EMA for direction, at 1.3299. EURGBP meanwhile has cleared 0.8440, its 50-day EMA and key resistance, exposing 0.8541, the May 2 high. - The USD trades firmer against broader G10, with the corrective relief for the USD Index isolating the downtrendline drawn off the early February high as next resistance, today at 99.575.

- There are no remaining key data releases due Tuesday, and no further central bank speakers (the Fed remain inside the pre-decision media blackout period), keeping focus on the resumption of trade talks between US and Chinese trade negotiation teams in London.

GBP: Corrective Phase Lower Hinges on BoE Pricing, DXY Downtrend

GBP/USD's post-data sell-off is holding, but the sustainability of a corrective phase lower will hinge on conviction in BoE pricing and a nascent downtrendline in the USD Index.

- Weakness in GBP came in two phases this morning, first on the soft payrolls data, and then again on the SONIA open, with GBPUSD nearing 1.3462, its 20-day EMA. A clear break of this average would suggest potential for a deeper correction and expose the 50-day EMA for direction, at 1.3299. EURGBP meanwhile has cleared 0.8440, its 50-day EMA and key resistance, exposing 0.8541, the May 2 high.

- The sustainability of the move hinges in the short-term on BoE pricing: we note that OIS markets are returning closer to a further 2 x 25bps rate cuts this year: 46bp of cuts priced through December, with the next 25bp step almost fully priced at the September MPC.

- Should this pricing stick (or extend), the USD Index will come into sharper focus, with today's USD relief rally prompting the DXY to narrow the gap with a key downtrendline drawn off the early February highs - today at 99.575, a level across which markets were rangebound in the aftermath of Trump's Liberation Day announcement. This level could prove key into the US CPI print tomorrow.

Figure 1: Sustainability of GBP/USD Dip Could Hinge on USD Index Downtrendline

Source: Bloomberg Finance L.P. / MNI

GBP: Sterling Crosses in Focus Given Significance of US Inflation Release

- Given the importance of the greenback trajectory in determining the depth of GBPUSD’s correction (as mentioned earlier in our 0904 bullet), and the close proximity to US CPI data on Wednesday, it is worth highlighting some important technical levels for sterling crosses, potentially providing a more direction signal following the soft labour market data this morning.

- The brief pop higher for GBPJPY on BOJ Ueda comments overnight saw the cross broadly match the April highs around 196.40. Since then, the cross has now sits 130 pips off these highs, currently down 0.38% on the session. There have been continued failed attempts to breach the trendline drawn from the October highs, and today’s reversal lower could signal scope for a deeper pullback. The 50-day EMA has remained technically significant across May, and would be an obvious target for the move. The average currently intersects at 193.05.

- GBPAUD stands out on the chart, showing nascent signs of breaking an uptrend line, drawn from the February lows. Furthermore, the cross has breached the 50-day EMA, extending the pullback from the May highs to 1.6%. A cluster of daily lows just below the 2.05 mark provides the initial target for the move. Below here, the December high provides next support at 2.03.

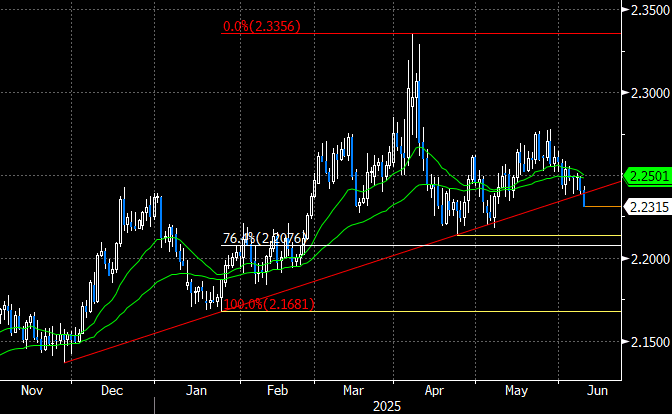

- In similar vein, GBPNZD (shown below) is now threatening a trendline break, drawn from the November lows seen following the US election. While the trendline was moderately pierced in early May, a daily close below would provide a more bearish signal. This may signal scope for a move towards the April low at 2.2140 and a Fibonacci projection at 2.2076.

OPTIONS: Expiries for Jun10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1300-20(E1.5bln), $1.1370-75(E920mln), $1.1400-25(E2.1bln)

- USD/JPY: Y143.90-00($1.1bln), Y144.85-00($805mln)

- AUD/USD: $0.6420(A$771mln), $0.6460(A$529mln)

- USD/CAD: C$1.3695($869mln)

EQUITIES: Fresh Cycle Highs for E-Mini S&P Affirm Bullish Conditions

- The trend cycle in Eurostoxx 50 futures is bullish and the contract is trading closer to its recent highs. Moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Clearance of this level would strengthen a bull theme. Key support to watch lies at 5205.88, the 50-day EMA. A clear break of this average would signal a possible reversal.

- The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract has again traded to a fresh cycle high, today. The recent break of 5993.50, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. A continuation would open 6057.00 next, the Mar 3 high. Key support lies at 5798.36, the 50-day EMA.

COMMODITIES: Medium-Term Trend Signals for Gold Remain Bullish

- WTI futures are trading higher this week, extending the current bull cycle. The contract has cleared the 50-day EMA and this signals scope for an extension towards $65.82 next, the Apr 4 high. It is still possible that the recovery since early May is a correction. MA studies are in a bear-mode position, highlighting a dominant medium-term downtrend. Support to watch lies at $59.74, the May 30 low. A break would highlight a potential bearish reversal.

- A bullish theme in Gold remains intact and the latest pullback appears corrective. Medium-term trend signals are bullish - moving average studies remain in a bull-mode position, highlighting a dominant uptrend. A resumption of gains would refocus attention on $3435.6 next, the May 7 high. A break of this hurdle would strengthen bullish conditions. On the downside, the next support to monitor is $3242.4, the 50-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 10/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 10/06/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 10/06/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 11/06/2025 | 0630/0730 | BOE Saporta Speech At Bank of Finland and SUERF Conference | ||

| 11/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 11/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 11/06/2025 | 0930/1130 | ECB Lane At 2025 Government Borrowers Forum | ||

| 11/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 11/06/2025 | 1130/1230 | Chancellor Reeves presents Spending Review to Parliament | ||

| 11/06/2025 | - | *** | Money Supply | |

| 11/06/2025 | - | *** | New Loans | |

| 11/06/2025 | - | *** | Social Financing | |

| 11/06/2025 | 1200/1400 | ECB Cipollone On Digital Payments Panel | ||

| 11/06/2025 | 1230/0830 | * | Building Permits | |

| 11/06/2025 | 1230/0830 | *** | CPI | |

| 11/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 11/06/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/06/2025 | 1800/1400 | ** | Treasury Budget |