MNI US Employment Insight: Resilience To Keep Fed On Sidelines

Jul-03 19:36By: Tim Cooper and 1 more...

Employment+ 1

Download Full Report Here

EXECUTIVE SUMMARY

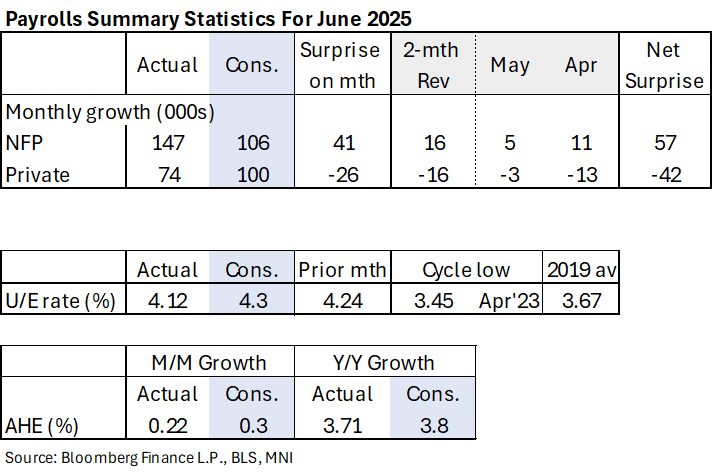

- Nonfarm payrolls growth comfortably beat expectations in June with 147k (cons 106k) along with small upward revisions of +16k after a string of releases with large downward revisions.

- Arguably an even bigger surprise was the pullback in the unemployment rate, which at 4.117% unrounded is the lowest since January, down from 4.244% prior and well below the rounded 4.3% consensus.

- This suggests a faster-than-expected deterioration will be required for the final 6 months of the year to reach the FOMC's latest Q4 median projection of 4.5%.

- But it was far from an unambiguously strong report. Private payroll gains missed expectations at 74k (cons 100k), leaving government payrolls surging by 73k for the largest increase since Mar 2024.

- That may in turn have been supported by seasonal factors in public education employment, and in addition, private sector job creation remains extremely reliant on the large and cyclically insensitive health & social assistance category (adding 59k in June after 81k in May) – not exactly signs of underlying strength.

- Average hourly earnings growth was softer than expected at 0.22% M/M (cons 0.3), with lower revisions.

- And the continued decline in the size of the labor force and participation rates suggests that concerns about diminishing labor supply may be increasingly well-founded.

- On the whole though, the labor market appears to be in solid enough shape to keep the Fed on the sidelines. Payroll growth has averaged 150k over the latest three months, comfortably above long-run breakeven estimates thought to be around 100k, although with private payrolls less elevated at 115k.

- Most focus was on the degree to which this effectively closed the door to a July Fed cut, with implied pricing falling to just 1bp (ie under 5% probability of a cut) from 6.5bp. And it brought down implied 2025 cuts to 2, versus an evenly split pricing between 2 and 3 cuts.

- Analyst expectations had been firmly focused on September or later in 2025 for the resumption of Fed easing. There was nothing in this report to shift those expectations, with the Fed set to take the summer off before assessing the totality of the data to decision day on Sept 17th (2x more payrolls, 3x more CPI).