MNI RBNZ WATCH: MPC To Cut, Eyes 50 Basis Points

The Reserve Bank of New Zealand’s monetary policy committee is expected to cut the official cash rate from 3% when it meets next Wednesday, with a 50-basis-point reduction seen as highly likely, to stimulate household spending following weaker-than-expected Q2 GDP data.

With only one meeting remaining this year in November before the RBNZ’s extended summer break, the committee is expected to take decisive action to support the economic recovery amid slower-than-anticipated growth. The MPC cut the OCR 25bp at its last meeting in August, taking its cumulative easing this cycle to 250bp and signaled that it wants to move cautiously toward a 2.5% rate. (See MNI RBNZ WATCH: MPC Makes Dovish 25BP Cut, Eyes 2.5% OCR)

Markets have now fully priced in about 33bp of easing next week and a 2.25% OCR by Q1, reflecting comments Chief Economist Paul Conway made to MNI in August that the Bank would seek a lower rate on weaker growth. (See MNI INTERVIEW: RBNZ's Conway Sees Lower OCR On Weak Growth)

LOWER GDP

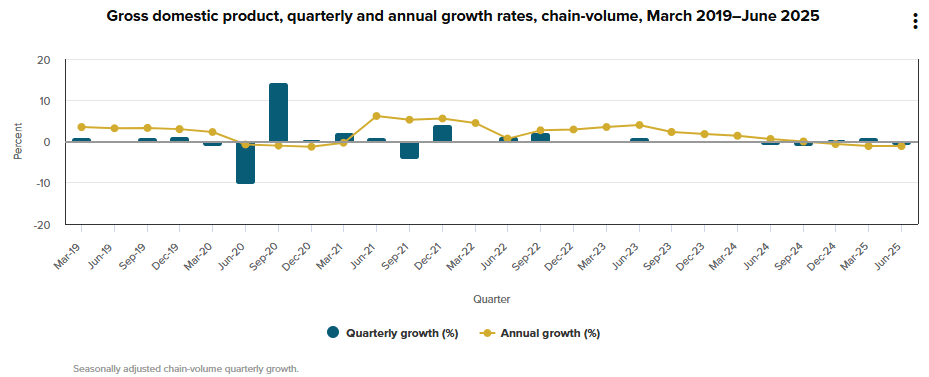

Q2 GDP contracted by 0.9%, significantly steeper than the RBNZ’s forecast 0.3% decline. Ten of 16 industries shrank during the quarter. The fall followed a 0.9% rise in Q1, leaving GDP down 1.1% y/y in the year to June 2025. Manufacturing was the largest drag, down 3.5% on weaker transport equipment, food, and metal products, while construction fell 1.8%. Business NZ's September manufacturing and services surveys also point to flat or contracting activity, reinforcing concerns about slowing growth.

EASING STRATEGY

The weak recovery points to significant spare capacity, strengthening calls for deeper OCR cuts. A former assistant governor recently told MNI that the RBNZ may have kept rates too high for too long, implying a period of below-neutral policy could be needed to stabilise both output and inflation. In this view, the OCR could fall as much as 100bp to around 2% over the near term.

However, other former officials caution that the Bank may be reluctant to push rates below 2.5%, citing sticky inflation this year. Much of this is driven by temporarily elevated food prices, alongside non-market costs such as council rates and OCR-resistant sectors like energy and insurance.

Political uncertainty, falling house prices, and negative wealth effects on households could also restrain business investment, despite some mortgage relief. Regional and sectoral performance remains uneven, with sectors such as dairy and regions like Canterbury showing relative strength. As a result, the MPC faces a delicate balancing act, weighing support for growth against the need to contain inflation risks as it sets the OCR in the months ahead.