MNI RBNZ WATCH: MPC Faces Difficult Choice To Hike Or Hold

The Reserve Bank of New Zealand would have strong arguments to either raise or hold the Official Cash Rate at next week’s policy meeting, with the outcome appearing more uncertain than market pricing suggests.

The Monetary Policy Committee has held the OCR at 2.25% since November as economic activity has slowed following the easing cycle that began in August 2024. (See MNI RBNZ WATCH: MPC Discussed Front-Loading Hikes) However, the Middle East conflict and oil price shock have increased the risk of stagflation, forcing policymakers to balance rising inflation pressures against weakening growth and potentially compelling the MPC to hold a formal vote on its policy decision, with individual positions to be disclosed for the first time under the new transparency framework.

Markets have priced in only a 20% chance of a move higher on May 27. But some former RBNZ officials and advisors have warned against complacency, arguing the risk of a hike is materially higher than markets imply. (See MNI INTERVIEW: Market Underpricing RBNZ Hike - Fmr Asst Gov)

DATA UPDATES

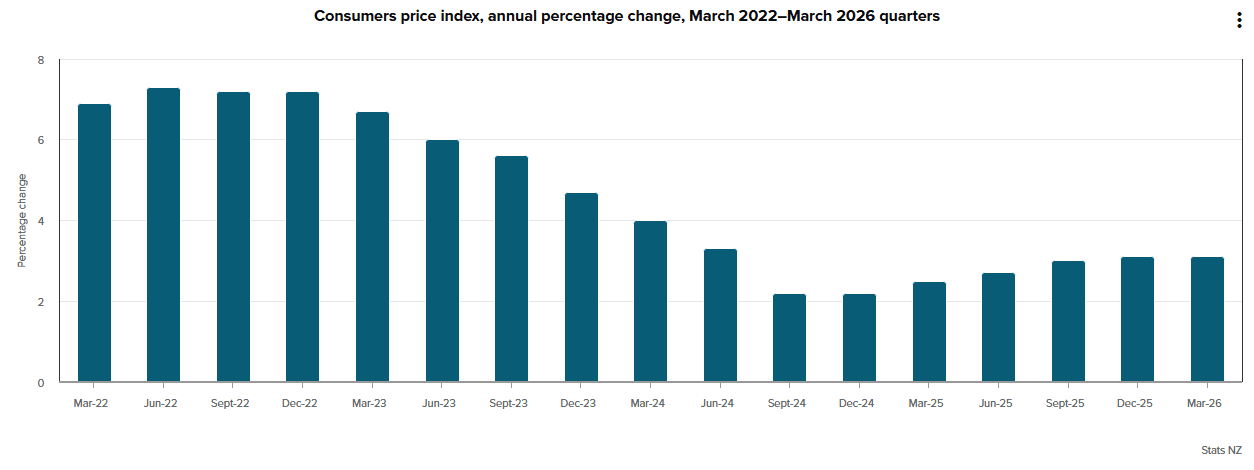

Inflation and inflation expectations remain elevated above the Bank’s 1-3% target band.

Annual CPI inflation was unchanged at 3.1% y/y in the March 2026 quarter, after first moving back above the band in the December quarter, and above the Bank's February 2.8% forecast. While non-tradables inflation was only marginally above forecast, tradables inflation surprised more significantly to the upside, partly reflecting sharp rises in fuel prices during March.

Measures of core inflation generally eased in the March quarter, though most remained in the upper half of the target range.

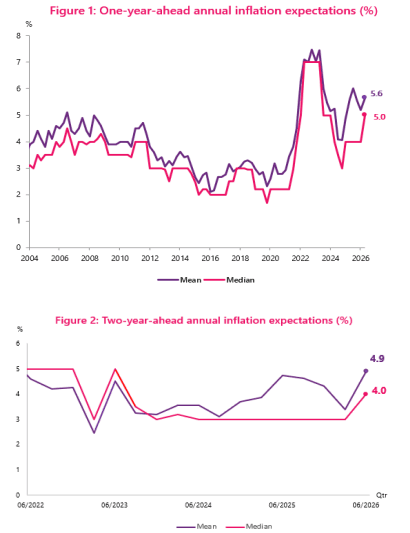

Inflation expectations also rose sharply. Mean household expectations for one-year-ahead inflation increased to 5.6% from 5.2%, while the median rose to 5.0% from 4.0%. Mean two-year-ahead inflation expectations climbed to 4.9% from 3.4%, and the median increased to 4.0% from 3.0%.

However, economic growth remains weak. The December quarter GDP report showed the economy expanding just 0.2%, around 0.3 percentage points below the RBNZ’s expectations, while the level of GDP was estimated to be 0.4% below forecasts after accounting for revisions. The RBNZ had expected cumulative growth of 1.6% over the first half of 2026. While the unemployment rate edged lower in the March quarter, it remained elevated at 5.3%, broadly in line with RBNZ projections.

VARIED OPINIONS

Former RBNZ staffers and economists see a difficult policy decision ahead, with both hold and hike cases carrying substantial weight.

Former Assistant Governor John McDermott said the risk of a move was considerably higher due to inflationary pressure stemming from oil supply disruptions. Meanwhile, Michael Reddell, a former special advisor, argued New Zealand’s large negative output gap should give the Bank more time, with any rate hikes more likely later this year.

Pointing to first-quarter core inflation of 2.6%, alongside elevated domestic and headline inflation pressures, Cameron Bagrie, managing director and chief economist at Bagrie Economics, said that while the Bank is still likely to leave the OCR unchanged at next week’s meeting, the growing risk of stagflation argues for moving rates more quickly toward the estimated neutral level near 3% in order to absorb the inflationary impact of the oil shock.