MNI EUROPEAN OPEN: Trade & Geopolitics In Focus Again

EXECUTIVE SUMMARY

- WALLER: 10% TARIFFS WOULD ALLOW FED RATE CUTS LATER IN 2025 - MNI

- TRUMP ANNOUNCES 50% STEEL & ALUMINIUM TARIFFS - BBC

- CHINA REBUKED THE US OVER ITS TRADE POLICY - BBG

- BESSENT: US WILL NEVER DEFAULT - BBG

- UKRAINE ATTACKED AIRBASES ON RUSSIAN TERRITORY - BBC

- OPEC TO HIKE OUTPUT 411KBD IN JULY - BBG

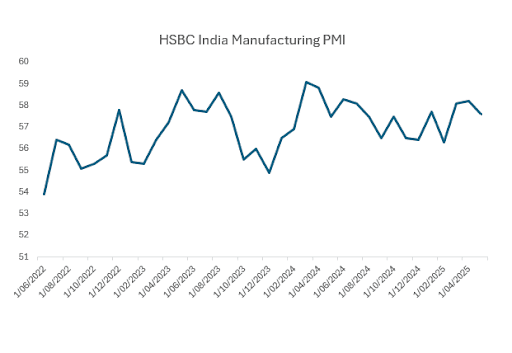

Fig 1: India's manufacturing PMI holding up

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

POLICY (BBC): “Tough choices are "unavoidable" as the government finalises spending plans for areas ranging from the NHS and defence, to schools and the criminal justice system, a think tank has warned. The Institute for Fiscal Studies (IFS) said the level of spending on health would dictate whether cuts were made to "unprotected" areas.”

DEFENCE (BBC): “The UK will build up to 12 new attack submarines, the prime minister will announce as the government unveils its major defence review on Monday. The review is expected to recommend the armed forces move to "warfighting readiness" to deter growing threats faced by the UK.”

DEFENCE (BBC): “There is "no doubt" that UK defence spending will rise to 3% of GDP by 2034 at the latest, Defence Secretary John Healey has said. In February, Prime Minister Sir Keir Starmer set out plans to increase defence spending to 2.5% by April 2027, with a "clear ambition" to reach 3% by 2034, economic conditions allowing.”

EU

TRADE (BBC): “The EU has said it "strongly" regrets Donald Trump's surprise plan to double US tariffs on steel and aluminium in a move that risks throwing bilateral trade talks into chaos.”

UKRAINE/RUSSIA (BBC): "Ukraine says it completed its biggest long-range attack of the war with Russia on Sunday, after using smuggled drones to launch a series of major strikes on 40 Russian warplanes at four military bases."

UKRAINE (BBC): “Ukraine's president has questioned Russia's commitment to progressing peace talks after Moscow confirmed it was sending a team to talks in Istanbul on Monday.”

NATO (BBC): “Members of the Western alliance Nato need to prepare for a possible attack from Russia within the next four years, according to Germany's chief of defence. General Carsten Breuer told the BBC that Russia was producing hundreds of tanks a year, many of which could be used for an attack on Nato Baltic state members by 2029 or even earlier.”

GERMANY (POLITICO): “German Chancellor Friedrich Merz will travel to Washington next week to meet United States President Donald Trump for the first time since taking office earlier this month. The leaders will meet in the White House on Thursday and are expected to discuss the war in Ukraine, the Middle East and trade policy, German government spokesperson Stefan Kornelius said in an emailed statement.”

FRANCE (BBC): “France's President Emmanuel Macron warned the US and Europe risked losing their credibility and being accused of "double standards" if they do not resolve the wars in Ukraine and Gaza soon. He also appealed to Asian countries to build a new alliance with Europe to ensure they do not become "collateral damage" in the struggle for power between the US and China.”

FRANCE (POLITICO): “China denounced comments by French President Emmanuel Macron comparing Beijing’s dispute over Taiwan to Moscow’s aggression in Ukraine. Macron had made the link in a speech at the Shangri-La Dialogue security conference in Singapore Friday night, warning that unchecked Russian aggression in Ukraine could set a precedent in Asia.”

NETHERLANDS (POLITICO): “Beijing’s espionage on Dutch semiconductors and other high-tech areas is “intensifying,” Ruben Brekelmans tells Reuters at Shangri-La Dialogue security forum.”

POLAND (BBG): “Karol Nawrocki, a nationalist candidate backed by Donald Trump, won Poland's presidential election with 50.9% of the vote, defeating centrist Rafal Trzaskowski.”

US

FED (MNI): “Federal Reserve Governor Chris Waller said Sunday the U.S. central bank could resume its trajectory of normalizing interest rates later this year if tariffs overall settle closer to 10% with higher country and sector specific taxes negotiated down over time.”

TRADE (BBC): “President Donald Trump has announced the US will double its current tariff rate on steel and aluminium imports from 25% to 50%, starting on Wednesday.”

TRADE (BBC): “US President Donald Trump is not planning to extend the pause to his sweeping global tariffs, Commerce Secretary Howard Lutnick said.”

TRADE (POLITICO): “Commerce Secretary Howard Lutnick insisted Sunday a court fight over President Donald Trump’s tariff power won’t blunt the administration’s leverage as it works on trade deals with key partners ahead of a July deadline.”

TRADE (BBG): “US President Donald Trump expressed confidence a talk with Chinese President Xi Jinping could ease fresh trade tensions, after White House officials vented anger over Beijing’s pace of issuing promised export licenses.”

TRADE (BBG): “A legal argument known as the "major questions doctrine" is threatening President Donald Trump's sweeping tariffs, after the US Court of International Trade ruled that many of Trump's import taxes exceeded the authority Congress had given him. The doctrine, which was used to block Joe Biden's climate change and student debt initiatives, states that federal agencies can't decide sweeping political and economic matters without clear congressional authorization.”

FISCAL (BBG): “Treasury Secretary Scott Bessent said the US “is never going to default” as the deadline for increasing the federal debt ceiling gets closer.”

USD (BBG): “The US Dollar Index is predicted to fall around 9% to 91 by next year, driven by interest rate cuts and slowing growth, according to Morgan Stanley strategists. The euro, yen, and Swiss franc are expected to benefit from dollar weakness.”

DEFENCE (BBG): “US Defense Secretary Pete Hegseth urged Asian partners to increase defense spending to 5% of GDP, citing the need to prepare for a potential Chinese invasion of Taiwan.”

BANKING (POLITICO): “Trump-appointed regulators are nearing completion of a proposal that would relax rules on how much of a capital cushion the nation’s largest banks must have to absorb potential losses and remain solvent during periods of economic stress.”

OTHER

OPEC (BBG): “OPEC+ agreed to increase oil output by 411,000 barrels a day in July, despite reservations from Russia and other members, marking a historic policy shift to drive prices lower.”

JAPAN (MNI): “Combined capital investment by non-financial Japanese companies excluding software rose 1.8% quarter-on-quarter in Q1, up from a 1.3% increase in Q4, a quarterly survey released Monday by the Ministry of Finance showed.”

JAPAN (BBG): “Japan's top trade negotiator Ryosei Akazawa says the latest round of discussions with the Trump administration on tariffs are on track toward a deal. “Japan and the US have confirmed that discussions toward reaching an agreement are making progress, while fully recognizing each other’s positions,” Akazawa told reporters in Washington. “We agreed to further accelerate coordination toward a bilateral summit in June.””

JAPAN (BBG): “Japan’s top trade negotiator Ryosei Akazawa is considering returning to the US for another round of trade negotiations this week as expectations mount for a deal as early as this month.”

AUSTRALIA (BBG): “US Secretary of Defense Pete Hegseth asked Australia to increase its military spending to 3.5% of gross domestic product "as soon as possible". Prime Minister Anthony Albanese said Australia will determine its own levels of military expenditure, pointing out the government has invested an additional A$10 billion in defense.”

AUSTRALIA (BBC): “Australia's defence minister Richard Marles has called on China to explain why it needs to have "such an extraordinary military build-up". He said Beijing needs to provide greater transparency and reassurance as it is the "fundamental issue" for the region.”

CHILE (BBG): “Chile center-right presidential candidate Evelyn Matthei held a small lead over more conservative contender Jose Antonio Kast atop two polls published on Sunday, reflecting an open race for the nation’s top job.”

CHINA

TRADE (BBG): “The Chinese Ministry of Commerce rebuked the US president's claim that Beijing breached the consensus reached in Geneva last month, citing new discriminatory restrictions introduced by the US. Trump expressed hope to speak with Chinese President Xi Jinping, but tensions between the world's largest economies are increasing again after the tariff thaw in May.”

ECONOMY (MNI): “China's Manufacturing Purchasing Managers Index rose by 0.5 points to 49.5 in May, but remained below the breakeven 50 mark for the second month, data from the National Bureau of Statistics showed Saturday.”

US (BBG): “China lodged a protest over Defense Secretary Pete Hegseth's speech at a defense forum in Singapore, where Hegseth chided China for not sending a high-profile representative to the gathering.”

MARKET DATA

AUSTRALIA COTALITY HOME VALUES MAY +0.5% M/M; APR. +0.2%

AUSTRALIA S&P GLOBAL MAY FINAL MANUFACTURING PMI 51; PRE. 51.7; APR. 51.7

AUSTRALIA MI INFLATION GAUGE MAY -0.4% M/M & 2.6% Y/Y; APR. +0.6% & 3.3%

AUSTRALIA MAY ANZ JOB ADVERTISEMENTS -1.2% M/M; APR. -0.3%

JAPAN Q1 CAPITAL SPENDING +6.4% Y/Y; EST. +3.8%; Q4 -0.2%

JAPAN Q1 CAPITAL SPENDING EX-SOFTWARE +6.9% Y/Y; EST. 5.3%; Q4 +3.1%

JAPANESE COMPANIES Q1 PROFITS +3.8% Y/Y; EST. +6.0%; Q4 +13.5%

JAPANESE COMPANIES Q1 SALES +4.3% Y/Y; EST. +3.0%; Q4 +2.5%

JAPAN JIBUN BANK MAY MFG PMI 49.4; PRE. 49.0; APR. 48.7

SOUTH KOREA S&P GLOBAL MAY MFG PMI 47.7; APR. 47.5

MARKETS

US TSYS: Asia Wrap - Long-End A Little Higher

The TYM5 range has been 110-22 to 110-30 during the Asia-Pacific session. It last changed hands at 110-25, up 0-01 from the previous close.

- The US 2-year yield is unchanged, trading around 3.9%, unchanged from its close.

- The US 10-year yield is a little higher, trading around 4.414%, up 0.01 from its close.

- This has seen the yield curve steepen in Asia - 2s10s +1.17 at 50.843, 5s30s +1.71 at 98.14.

- (Bloomberg) - “Federal Reserve Governor Christopher Waller said he continues to see a path to interest-rate cuts later this year amid his expectations that tariffs will boost unemployment and temporarily increase inflation.”

- “Asset managers heavily unwound net long positioning in Treasury futures, with positioning in ultra-long bond futures heavily cut in the week ending May 27, CFTC data show. Hedge funds covered short positions across the curve, taking the other side, with a big short unwind seen in ultra-long bonds.”(BBG)

- AFR via BBG - “JPMorgan chief executive Jamie Dimon on Friday night predicted that a crack in the bond market is “going to happen” - and it will scare the pants off everyone.”

- The 10-year has come back down to test its support around 4.35/40%, likely aided by month-end rebalancing. Yields need to hold above this area to continue to build for a move higher.

- Data/Events : S&P Global US Man PMI, ISM Man, Powell to talk.

JGBS: Futures Weaker, 10Y Supply & BoJ Ueda Speech Tomorrow

JGB futures are holding weaker, -15 compared to the settlement levels, hovering near Tokyo session lows. Geopolitical headlines have been in focus.

- "Ukraine attacked Russian airbases with drones, destroying 40 bomber planes, according to the BBC. It appears in response to larger Russian attacks on Ukraine recently, including Kyiv. Talks are due to start Monday." (BBG)

- " Japan's bond market faces challenges with debt sales on Tuesday and Thursday, which may pressure the government to adjust its borrowing plans and calm investor nerves. The finance ministry and BoJ Governor Kazuo Ueda are considering actions to address the issue, including reducing bond issuance and monitoring the impact of rising yields on debt with shorter maturity." – BBG

- Cash US tsys have bear-steepened, with yields 1-3bps higher, in today's Asia-Pac session. Monday's US calendar sees ISM Manufacturing data and an appearance by Fed Chair Powell, with the June employment report looming at the end of next week.

- Cash JGBs are 1bp richer to 2bps cheaper across benchmarks, with the 5-7-year zone underperforming and the 30-40-year outperforming.

- Swap rates are 2-3bps higher. Swap spreads are wider.

- Tomorrow, the local calendar will see Monetary Base data alongside 10-year supply and a speech by BoJ Ueda.

AUSSIE BONDS: Subdued Session, RBA Minutes & RBA Hunter Speech Tomorrow

ACGBs (YM flat & XM -0.5) sit little changed after a subdued session with limited newsflow. Today’s domestic data drop was second tier in nature (Home Values, S&P Global PMI Mfg, Melbourne Institute Inflation and ANZ-Indeed Job Advertisements) and so provided limited directional guidance for the local market.

- Cash US tsys have bear-steepened, with yields 1-3bps higher, in today's Asia-Pac session. Monday's US calendar sees ISM Manufacturing data and an appearance by Fed Chair Powell, with the June employment report looming at the end of next week.

- Cash ACGBs are little changed with the AU-US 10-year yield differential at -14bps.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in July is given a 72% probability, with a cumulative 77bps of easing priced by year-end.

- Tomorrow, the local calendar will see Q1 Company Operating Profits, Inventories, Current Account Balance alongside RBA Minutes of May Policy Meeting and a speech by the RBA's Sarah Hunter, Assistant Governor (Economic), titled ‘Joining the Dots: Exploring Australia’s Links with the World Economy’.

- This week, the AOFM plans to sell A$1200mn of the 3.75% 21 April 2037 bond tomorrow and A$800mn of the 1.50% 21 June 2031 bond on Friday.

FOREX: Asia FX Wrap - USD Back Under Pressure

The BBDXY has had a range of 1213.45 - 1216.54 in the Asia-Pac session, it is currently trading around 1215. MNI: Italy Eyes Transition To New NATO Target-Treasury Sources: The Italian government is confident that changes in both European Commission and NATO frameworks will allow for a smoother transition towards a higher defence spending target expected to be announced after the transatlantic summit on June 24, Treasury sources told MNI. Rome believes that a defence spending target of 5% of GDP – a figure currently circulating in policy discussions – would be “almost impossible to meet” given the country’s tight public finances. MNI SOURCES: ECB Set To Lower 2026 Inflation Projection: The European Central Bank is likely to lower its inflation projection for 2026 to 1.7% or 1.8% in its June exercise, one or two tenths below the 1.9% seen in March, Eurosystem sources told MNI, adding that there could be a pause in rate cuts after a further 25-basis-point reduction next week.

- EUR/USD - Asian range 1.1347 - 1.1382, Asia is currently trading 1.1365. EUR has drifted higher during the Asian session as US stock futures trade weaker. Dips should continue to find support, the demand back towards 1.1200 proved to be solid last week.

- GBP/USD - Asian range 1.3454 - 1.3506, Asia is currently dealing around 1.3490. The GBP could not hold above the pivotal 1.3500 area last week, the market is likely to give it another try. Look for an opportunity to buy again back towards the 13300/3400 area.

- USD/CNH - Asian range 7.2016 - 7.241, Asia is currently dealing around 7.2170. Sellers should be around from here all the way back to the 7.2500 area.

- Cross asset : SPX -0.45%, Gold $3315, US 10-Year 4.41%, BBDXY 1215, Crude oil $62.47

- Data/Events : Spain, Italy, Germ, France, ECB HCOM Manu PMI’s

JPY: Asia Wrap - JPY Bounces As Safe Havens Are Bought

The Asia-Pac USD/JPY range has been 143.44 - 143.99, Asia is currently trading around 143.55. USD/JPY has been under pressure in our sessions as the market's focus returns to buying the JPY as a safe haven once more as US Stocks futures move lower. This was due to increased trade tension between the US and China and the rise in geopolitical risk as Ukraine launches an unprecedented attack deep inside Russia.

- “Ukraine attacked Russian airbases with drones destroying 40 bomber planes, according to the BBC. It appears in response to larger Russian attacks on Ukraine recently including Kyiv. Talks are due to start Monday.”(BBG)

- There is lots of speculation as to what the response from Russia may be to what some are calling its “Pearl Harbor”. https://www.newsweek.com/retired-us-commanders-react-ukraines-pearl-harbor-attack-russia-2079551

- "*JAPAN'S AKAZAWA ARRANGING US VISIT FROM THURS.: KYODO" - BBG

- US Equity futures are off around 0.5% in Asia and this has seen the JPY outperform across the board.

- The market seems very confident of a move lower in USD/JPY but with positioning quite large now we have seen the risks of pullbacks increase. Resistance around the 146.00 area held perfectly and the JPY bulls would be quite relieved as well as vindicated by the price action. The next pivotal trigger points look to be below 140.00 on the downside and above 146.50 on the topside.

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.00($670m). Upcoming Close Strikes : 140.00($1.88b June 5), 142.00($884m June 5).

CFTC data shows Asset managers maintained their already extensive JPY longs, and leveraged funds reduced their longs that had just started to be built up.

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg

AUD: Asia Wrap - AUD Gets a Bump Higher

The AUD/USD has had a range of 0.6433 - 0.6473 in the Asia- Pac session, it is currently trading around 0.6455. The AUD popped higher as the USD and US Equity futures came under pressure from a combination of increased trade tension between the US and China and the rise in geopolitical risk as Ukraine launches an unprecedented attack deep inside Russia.

- AUSTRALIA DATA: "S&P Global Australia May Manufacturing PMI 51 vs 51.7 Prior" - BBG

- "Australia’s inflation gauge fell 0.4% from a month earlier in May bringing annual rate 2.6% y/y from 3.3%, according to the Melbourne Institute Monthly Inflation Gauge and Cost of Living report." - BBG

- “Ukraine attacked Russian airbases with drones destroying 40 bomber planes, according to the BBC. It appears in response to larger Russian attacks on Ukraine recently including Kyiv. Talks are due to start Monday.”(BBG)

- The AUD has struggled to hold onto its early gains and has underperformed in the crosses as US Equity futures stay under pressure.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend. A break above 0.6550 and the move higher could begin to accelerate.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6400(AUD586m), 0.6425(AUD454m), 0.6575(AUD445m). Upcoming Close Strikes : 0.6490(AUD 787m June 5)

- CFTC Data shows Asset managers pared back their shorts ever so slightly, the Leveraged community though added to their shorts quite aggressively over the week.

AUD/JPY - Today's range 92.53 - 92.85, it is trading currently around 92.60. Range looks 92.00 - 94.00 for now, a sustained break sub 91.50/92.00 will bring focus back to towards the lows again.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg

NZD: Asia Wrap - The NZD Benefits From Tension

The NZD/USD had a range of 0.5960 - 0.6009 in the Asia-Pac session, going into the London open trading around 0.5995. The NZD popped higher as the USD and US Equity futures came under pressure from a combination of increased trade tension between the US and China and the rise in geopolitical risk as Ukraine launches an unprecedented attack deep inside Russia.

- “China on Monday accused the US of violating their recent trade deal by unilaterally introducing new discriminatory restrictions, rebuking Donald Trump’s claim that Beijing breached the consensus reached in Geneva last month. The rhetoric dims the prospect of a call with Chinese President Xi Jinping this week to further bilateral talks" (BBG)

- MNI BRIEF: China May Manufacturing PMI Remains In Contraction: China's Manufacturing Purchasing Managers Index rose by 0.5 points to 49.5 in May, but remained below the breakeven 50 mark for the second month, data from the National Bureau of Statistics showed Saturday.

- The NZD continues to trade in a 0.5850/0.6050 range, the hawkish slant from the RBNZ last week has only seen a slight paring back of short positions.

- The support back towards 0.5800/50 has held very well, and while this continues to hold expect buyers to be around on dips. A break above 0.6050 is needed to provide the spark for the next leg higher.

- CFTC Data showed Asset managers maintaining their shorts, while the leveraged community pared back only a small portion of the decent short they had initiated the week before.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6100(NZD375m June 3), 0.5900(NZD401m June 4), 0.5725(NZD600m June 4)

AUD/NZD range for the session has been 1.0758 - 1.0791, currently trading 1.0765. A top looks in place now just above 1.0900, the market will have been looking for a more dovish tone from the RBNZ last week and AUD/NZD could now see supply on bounces. The sell zone is back towards 1.0825/50 with the first target being around 1.0650.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Tariff Headlines Drive Major Bourses Lower

With China closed today, it was left to the Hang Seng to give an indication as to sentiment and it was definitely a risk off day. With uncertainty prevailing around the trade war, the US President had said over the weekend that China had violated a big part of the agreement made in Geneva whilst China hit back Beijing called on the US to correct 'discriminatory' measures and uphold the consensus reached in Geneva. Adding further to the uncertainty is the news of further tariffs on steel and aluminium and plans to target China's tech sector.

- With mainland bourses closed, the Hang Seng had centre state and fell -2.20%to be the worst performer out of its regional peers.

- The KOSPI had tried to rally early on but that faded away to be down by -0.35%.

- In Singapore the FTSE Straits Times fell by -0.50% whilst the PSEi in the Philippines was one of the few gainers, up +0.35%

- After a negative week last week, the NIFTY 50 in India is opening weak again, down -0.65% despite better than expected GDP figures out for Q1.

OIL: Crude Higher As OPEC Hikes Output As Expected & Geopolitics Worsen

Oil prices have defied the pullback in risk appetite from the increase in trade tensions and have rallied in relief that OPEC increased output as expected. There had been fears that it would be larger than the previous rises. The increase in geopolitical friction may also be providing some support with the relaxation of sanctions against Russia looking unlikely anytime soon.

- WTI has trended higher through the session and is up 2.8% to $62.50/bbl, close to the intraday high of $62.70, holding around initial resistance at $62.54, 50-day EMA. Brent is 2.5% higher at $64.33/bbl after reaching $64.49 earlier (50-day EMA $65.41). The USD index is down 0.1%.

- OPEC agreed on Saturday to increase output 411kbd from July, the third increase of this size which is believed to be a message to overproducers. Apparently Russia, Oman and Algeria wanted a pause in output normalisation, according to Bloomberg. The next meeting is on July 6.

- Bloomberg reported that Morgan Stanley expects OPEC to increase production three more times. It is forecasting Brent to average $57.50 in H2 2025 and $55 in H1 2026. Goldman Sachs though is forecasting only one more output rise. They both continue to project excess supply.

- Ukraine attacked Russian airbases with drones destroying at least 40 bomber planes, according to the BBC. It appears to be in response to larger Russian attacks on Ukraine including Kyiv. Talks are due to take place today.

- Later the Fed’s Logan, Goolsbee and Chair Powell appear as well as ECB President Lagarde, BOE’s Mann & Greene. US May manufacturing PMI/ISM and April construction and European May manufacturing PMIs print. The focus this week will be on Friday’s US payrolls.

GOLD: Weekend’s Deterioration In Trade & Geopolitical Situation Boost Gold

Gold is benefiting from safe haven flows today after a deterioration in the geopolitical picture with US President Trump announcing a doubling of tariffs on steel & aluminium from Wednesday and saying that China had broken the conditions of the trade truce, which China has rebuked. Also increased defence spending was discussed at a security conference in Singapore, while Ukraine attacked Russian airfields. The USD and US yields are little changed.

- Gold prices fell 0.9% to $3289.25/oz on Friday to be flat in May. It hasn’t unwound all of Friday’s loss today though with bullion up 0.7% to $3313.3 and off the intraday high of $3316.77 made early in the session. A bullish theme remains intact but gold is trading between initial resistance at $3365.9, 23 May high, and support at $3213.6, 50-day EMA.

- Ukraine attacked Russian airbases with drones destroying at least 40 bomber planes, according to the BBC. It appears to be in response to larger Russian attacks on Ukraine including Kyiv. Talks are due to take place today.

- The pullback in risk is also reflected in today’s equity sell off with the S&P e-mini down 0.5% and the Hang Seng -2.2%. China is closed for a holiday. Oil prices are higher though with WTI +2.9% to $62.54/bbl. Copper is 3.9% higher but iron ore is lower at around $96/t. Silver is +0.2% to $33.06.

- Later the Fed’s Logan, Goolsbee and Chair Powell appear as well as ECB President Lagarde, BOE’s Mann & Greene. US May manufacturing PMI/ISM and April construction and European May manufacturing PMIs print. The focus this week will be on Friday’s US payrolls.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 02/06/2025 | 0630/0830 | ** | Retail Sales | |

| 02/06/2025 | 0700/0900 | *** | GDP | |

| 02/06/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 02/06/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 02/06/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 02/06/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 02/06/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 02/06/2025 | 0830/0930 | ** | BOE Lending to Individuals | |

| 02/06/2025 | 0830/0930 | ** | BOE M4 | |

| 02/06/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 02/06/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 02/06/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 02/06/2025 | 1400/1000 | * | Construction Spending | |

| 02/06/2025 | 1400/1000 | * | Construction Spending | |

| 02/06/2025 | 1400/1000 | Dallas Fed's Lorie Logan | ||

| 02/06/2025 | 1400/1500 | BOE's Mann fireside chat at Fed's IF 75th anniversary conference | ||

| 02/06/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/06/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 02/06/2025 | 1630/1830 | ECB Lagarde Video Message at Women In Finance Event | ||

| 02/06/2025 | 1645/1245 | Chicago Fed's Austan Goolsbee | ||

| 02/06/2025 | 1700/1300 | Fed Chair Jerome Powell | ||

| 02/06/2025 | 1700/1800 | BOE Greene Fireside Chat | ||

| 03/06/2025 | 0130/1130 | Business Indicators | ||

| 03/06/2025 | 0130/1130 | Balance of Payments: Current Account | ||

| 03/06/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI | |

| 03/06/2025 | 0630/0830 | *** | CPI | |

| 03/06/2025 | 0700/0300 | * | Turkey CPI | |

| 03/06/2025 | 0900/1100 | *** | HICP (p) | |

| 03/06/2025 | 0900/1100 | ** | Unemployment | |

| 03/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 03/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 03/06/2025 | 0915/1015 | BOE Bailey, Breeden, Dhingra, Mann At TSC | ||

| 03/06/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 03/06/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/06/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 03/06/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 03/06/2025 | 1400/1000 | ** | Factory New Orders |