MNI EUROPEAN OPEN: RBA Holds Steady, Surprising Market

EXECUTIVE SUMMARY

- TRUMP ISSUES NEW TARIFF RATES, STILL OPEN TO NEGOTIATIONS - BBG

- US OFFERS EU 10 PERCENT TARIFF DEAL - WITH CAVEATS - POLITICO

- TRUMP PROMISES MORE WEAPONS FOR UKRAINE AND CRITICIZES PUTIN - BBG

- JAPAN WILL CONTINUE TRADE TALKS WITH US FOR MUTUALLY BENEFICIAL DEAL, ISHIBA SAYS - RTRS

- RBA BOARD VOTES 6-3 TO LEAVE RATE AT 3.85% - MNI BRIEF

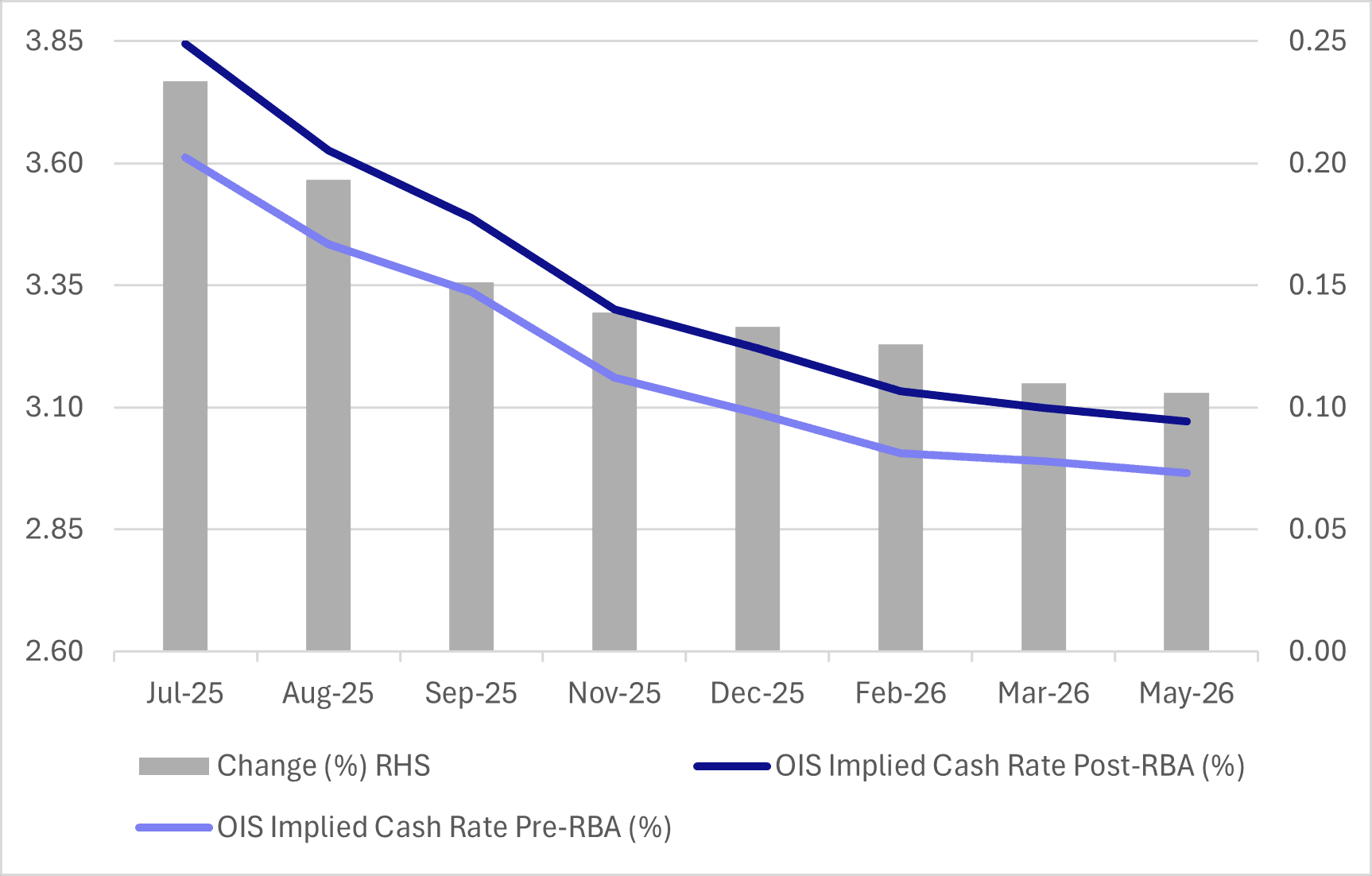

Fig 1: RBA Surprises Market With On Hold Decision

Source: Bloomberg Finance L.P./MNI

EU

TRADE/TARIFFS (POLITICO): “The United States has offered an agreement to the European Union that would keep a 10 percent baseline tariff on all EU goods, with some exceptions for sensitive sectors such as aircraft and spirits, an EU diplomat and a national official told POLITICO.”

UKRAINE (BBG): “ President Donald Trump said he’d ship more weapons to Ukraine, marking an apparent reversal after the Pentagon halted flows of some air-defense missiles and artillery shells to the country.”

ECB (BBG): “The European Central Bank’s best unconventional instrument for steering monetary policy is large-scale asset purchases, according to Governing Council member Francois Villeroy de Galhau.”

RUSSIA (BBG): "Soon after President Vladimir Putin launched his full-scale war on Ukraine, a little-known Russian company thousands of miles away hatched a plan to partner with Chinese firms and solve one of the most urgent challenges faced by the invading army — the need for combat drones that were radically reshaping the battlefield."

US

TARIFFS (BBG): “President Donald Trump unveiled the first in a wave of promised letters that threaten to impose higher tariff rates on key trading partners, but suggested that he was still open to additional negotiations and pushed off increased duties until at least Aug. 1.”

FED (MNI): The risks that the Federal Reserve's policy rate will be pinned at the zero lower bound remains significant over the medium to long-term due to recent elevated uncertainty, according to a blog published Monday by the president of the Federal Reserve Bank of New York, John Williams, and two other Fed system economists.

FED (MNI INVITE): INVITE: Join MNI Connect Livestream with Fed Mary Daly July 10. You are invited to listen to a Livestreamed MNI Connect Video Conference with the San Francisco Fed President Mary Daly.

OTHER

MIDDLE EAST (RTRS): “U.S. President Donald Trump, hosting Israeli Prime Minister Benjamin Netanyahu at the White House on Monday, said the United States had scheduled talks with Iran and indicated progress on a controversial effort to relocate Palestinians out of Gaza.”

JAPAN (RTRS): “Japanese Prime Minister Shigeru Ishiba said on Tuesday that he would continue negotiations with the U.S. to seek a mutually beneficial trade deal, after President Donald Trump announced 25% tariffs on goods from Japan starting August 1.”

JAPAN (BBG): “- Japan will continue to seek a trade agreement while protecting its national interests, Prime Minister Shigeru Ishiba says. Ishiba speaks at the government tariff headquarters meeting on Tuesday morning, after the Trump administration said the US will impose 25% tariffs on imports from Japan starting on Aug. 1."

AUSTRALIA (MNI BRIEF): The Reserve Bank of Australia’s monetary policy board decided on Tuesday to leave the cash rate unchanged at 3.85%, citing the need for more data to confirm inflation is falling sustainably toward the 2.5% midpoint.

CHINA

STIMULUS (BBG): “ China can fully hedge against adverse external effects, and is fully confident of maintaining sustained and healthy economic development, state-run Xinhua News Agency reports, citing Premier Li Qiang as saying. “

BOND FLOWS (BBG): “China is considering doubling an investment channel local investors use to buy bonds overseas, according to people familiar with the matter, a major step in its efforts to loosen restrictions on financial flows.”

EVS (21st Century Business Herald): “Provincial governments need forward planning to address the development goals and construction tasks of high-power charging facilities for electric vehicles, according to a document by the National Development and Reform Commission.”

FX RESERVES (SAFE): “China’s reserve assets accounted for just 33.0% of its external financial assets by the end of Q1 2025, the lowest on record, according to Guan Tao, former senior official at the State Administration of Foreign Exchange (SAFE).”

MNI: PBOC Net Drains CNY62 Bln via OMO Tuesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY69 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY62 billion after offsetting the maturity of CNY131 reverse repo today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4474% at 09:40 am local time from the close of 1.4660% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 49 on Monday, compared with the close of 45 on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.1534 Tues; +1.17% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1534 on Tuesday, compared with 7.1506 set on Monday. The fixing was estimated at 7.1796 by Bloomberg survey today.

MARKET DATA

AUSTRALIA JUNE NAB BUSINESS CONFIDENCE 5; PRIOR 2

AUSTRALIA JUNE NAB BUSINESS CONDITIONS 9; PRIOR 0

JAPAN JUNE BANK LENDING INCL TRUSTS Y/Y 2.8%; PRIOR 2.4%

JAPAN MAY BIP CURRENT ACCOUNT ADJUSTED ¥2818.1bn; MEDIAN ¥2580.6bn; PRIOR ¥2306.8bn

JAPAN MAY TRADE BALANCE BOP BASIS -¥522.3bn; MEDIAN -¥517.2bn; PRIOR -¥32.8bn

JAPAN MAY BOP CURRENT ACCOUNT BALANCE ¥3436.4bn; MEDIAN ¥3006.4bn; PRIOR ¥2258.0bn

JAPAN JUNE ECO WATCHERS SURVEY CURRENT xx; MEDIAN 45; PRIOR 44.4

JAPAN JUNE ECO WATCHERS SURVEY OUTLOOK xx; MEDIAN 45.3; PRIOR 44.8

MARKETS

US TSYS: Asia Wrap - Quiet Session

The TYU5 range has been 110-29+ to 111-01+ during the Asia-Pacific session. It last changed hands at 111-00, up 0-02 from the previous close.

- The US 2-year yield has moved lower trading around 3.884%, down 0.01 from its close.

- The US 10-year yield is relatively unchanged trading around 4.38%.

- The 10-year yield has seen a strong bounce in reaction to the better NFP print. This 4.35/40% area offers those who would like to express a long the opportunity to fade. A sustained close back above 4.45% area though would not be great for the bulls and would see more of the longs prepared back.

- Per Politico: "The United States has offered an agreement to the European Union that would keep a 10 percent baseline tariff on all EU goods, with some exceptions for sensitive sectors such as aircraft and spirits, an EU diplomat and a national official told POLITICO."

- (Bloomberg) -- “Scott Bessent told CNBC that he’ll meet with his Chinese counterpart within the next couple of weeks.”

- Data/Events: Bond investors will be focusing on the Fed Minutes and the demand for 10 & 30-year maturities this week. NFIB Small Business Optimism tonight

JGBS: Aggressive Bear-Steepening

JGB futures are weaker but sitting in the middle of today’s range, -12 compared to settlement levels.

- (Bloomberg) -- "Japan's super-long bonds extended their recent declines, pushing the yield on 30-year debt back above 3% and within sight of a record high. The moves come as investors weigh the impact of a new Aug. 1 deadline for US tariffs and as concern mounts that an upper house election in Japan on July 20 will usher in higher government spending."

- Cash US tsys are slightly cheaper in today's Asia-Pac session.

- Politico: "The United States has offered an agreement to the European Union that would keep a 10 per cent baseline tariff on all EU goods, with some exceptions for sensitive sectors such as aircraft and spirits, an EU diplomat and a national official told POLITICO."

- Cash JGBs have twist-steepened across benchmarks, with yields 1bp lower to 14bps higher. The benchmark 5-year yield is little changed after today's supply.

- Today’s 5-year JGB auction showed mixed signals on demand. The low price came in line with expectations, but the bid-to-cover ratio declined to 3.5411x.

- Swap rates are also showing a twist-steepener, with rates 1bp lower to 7bps higher.

- Tomorrow, the local calendar will see M2 & M3 Money Stock and Machine Tool Orders(P).

AUSSIE BONDS: Cheaper After RBA Surprise Market With No Cut

ACGBs (YM -12.0 & XM -8.0) are 3-6bps cheaper after the RBA surprised the market by leaving the cash rate at 3.85%. A 25bp rate cut today was given a 92% probability ahead of the decision by the market.

- The RBA Board sees inflation risks as more balanced and the labour market as strong, but remains cautious due to uncertainty in demand and supply. It will await more data to confirm inflation is tracking toward 2.5%.

- Policy remains flexible to global developments. A 6–3 majority supported today’s decision, and future statements will include an unattributed record of votes. The Board remains focused on price stability and full employment.

- Cash ACGBs are 6-8bps cheaper after the decision with the AU-US 10-year yield differential at -11bps.

- The bills strip has shunted cheaper, with pricing -5 to -12 after the decison.

- RBA-dated OIS pricing is 11-23bps firmer across meetings after the decision. A cumulative 64bps of easing priced by year-end versus 75bps pre-RBA

- Tomorrow, the local calendar will see a speech by RBA Hauser.

- The AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond tomorrow and A$1000mn of the 2.75% 21 November 2029 bond on Friday.

BONDS: NZGBS: Closed Modestly Cheaper Ahead Of RBNZ Decision Tomorrow

NZGBs closed modestly cheaper, with benchmark yields 2-3bps higher.

- The NZ-US and NZ-AU 10-year yield differentials closed slightly tighter. It is noteworthy, however, that the local market was closed at the time of the RBA decision. Tomorrow’s open is likely to reflect both post-RBA decision trading as well as any overnight fluctuations in US tsys.

- Swap rates closed 1-3bps higher, with the 2s10s curve steeper.

- Tomorrow, the local market will see the RBNZ Policy Decision. The sell-side consensus is for the RBNZ to remain on hold tomorrow, which is also consistent with market pricing.

- There are some sell-side forecasters looking for a rate cut tomorrow, whilst most of those who see the RBNZ on hold, see risks of further cuts as we progress through 2025. For this meeting, our own bias is for the central bank to hold policy rates steady. Recent inflation outcomes arguably provide the strongest signal that the RBNZ should hold pat at tomorrow's policy meeting. (See MNI RBNZ Preview here)

- RBNZ dated OIS pricing closed little changed across meetings. 3bps of easing is priced for this week's meeting, with a cumulative 30bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 3.00% Apr-29 bond and NZ$200mn of the 4.50% May-35 bond.

AUD: Asia Wrap - RBA Surprises Market Helping The AUD To Bounce

The AUD/USD has had a range of 0.6491 - 0.6558 in the Asia- Pac session, it is currently trading around 0.6540, +0.75%. The pair has popped higher as the RBA surprised the market by holding rates at 3.85% when a cut was almost fully priced in by the market. This has seen the AUD/USD almost completely erase all its losses from yesterday, where it trades from here will now depend on the fortunes of the USD going forward.

- ”The Board continues to judge that the risks to inflation have become more balanced and the labour market remains strong. Nevertheless it remains cautious about the outlook, particularly given the heightened level of uncertainty about both aggregate demand and supply. The Board judged that it could wait for a little more information to confirm that inflation remains on track to reach 2.5% on a sustainable basis.” - (BBG)

- (Bloomberg) -- Japanese investors bought the largest amount of Australian sovereign bonds in two years in May, according to the Asian nation's latest balance-of-payments data. Net purchases totaled ¥213.6 billion, the most since April 2023, and followed four months of selling

- The AUD/USD has bounced strongly off its support around 0.6500, back to the 0.6500 - 0.6600 range for now as it will now take its cues from the USD, a break of 0.6600 could signal a move back towards 0.6900/0.7000.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6435(AUD904m), 0.6375(AUD 722m), 0.6545(AUD 493m). Upcoming Close Strikes : 0.6425(AUD700m July 9), 0.6300(AUD866m July 8)

- CFTC Data shows Asset managers pared back their shorts slightly -35992, the Leveraged community maintained their shorts -22903.

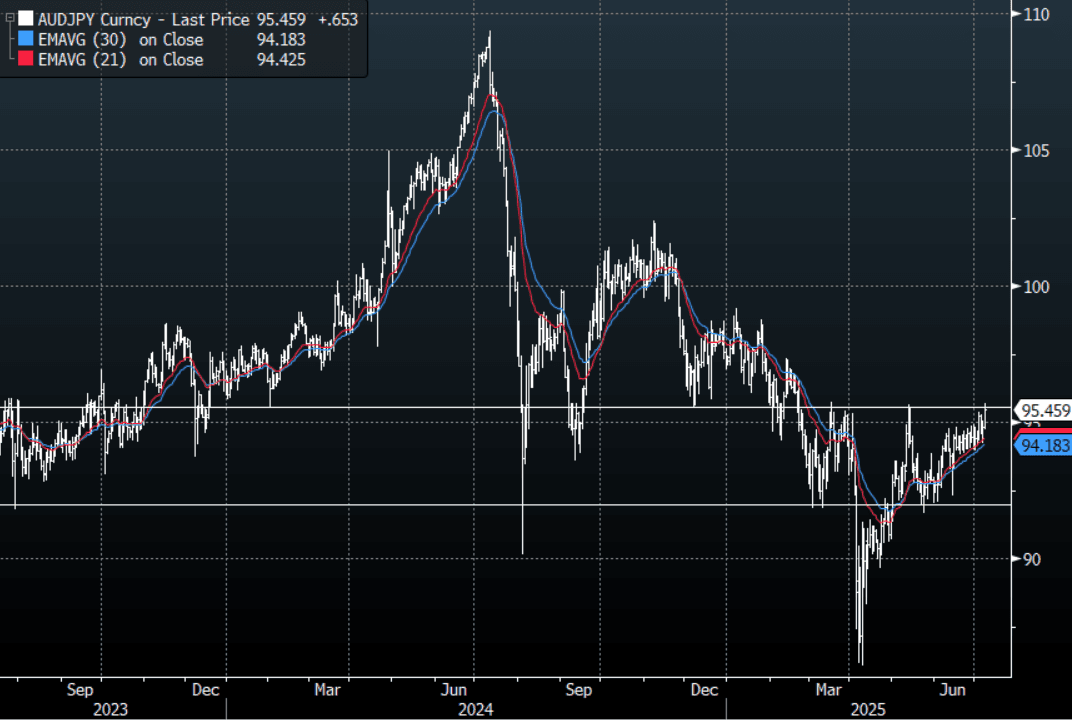

- AUD/JPY - Today's range 94.73 - 95.69, it is trading currently around 95.50, +0.70%. The pair found solid demand back towards 94.00 which stands out considering risk traded lower overnight. The range looks to be 93.50 - 96.00 a break above 96.00 could see a further paring back of AUD/JPY shorts.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

FOREX: Asia FX Wrap - The USD Drifting Lower

The BBDXY has had a range of 1193.81 - 1196.62 in the Asia-Pac session, it is currently trading around 1194. The USD has drifted lower in a quiet Asia-Pac session, -0.18%, giving back a little of its overnight gains. “Asian equities are holding up in the face of tariff angst as markets appear to be leaning into a familiar playbook: President Trump blusters, then backpedals. Many of the early jitters have faded, replaced by hopes of flexibility. Traders are latching onto signs that the Aug. 1 deadline may not be set in stone and that the White House remains open to negotiation. A proposed 10% tariff deal with the EU is also feeding that optimism." BBG

- EUR/USD - Asian range 1.1709 - 1.1749, Asia is currently trading 1.1745. The pair got a nice bounce on the news of a proposed deal with the US. The price is starting to look a little stretched in the short term and is vulnerable to any correction in the USD, first support is back towards 1.1600.

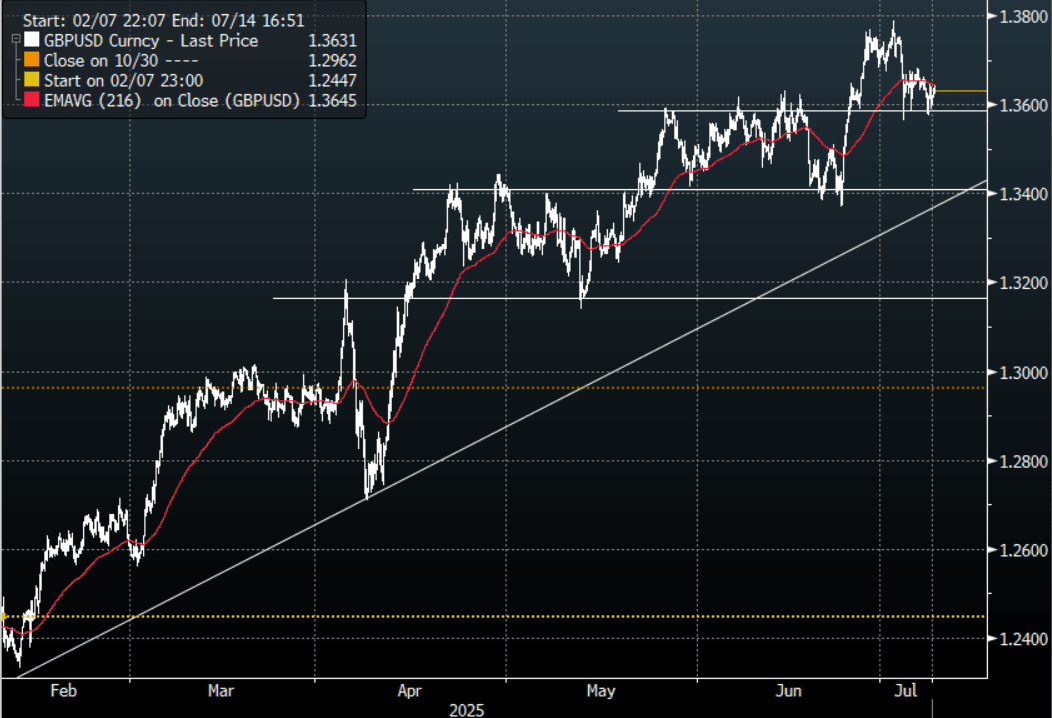

- GBP/USD - Asian range 1.3599 - 1.3639, Asia is currently dealing around 1.3635. Strong demand was again seen below 1.3600 helping the support to hold. A sustained move sub 1.3550 needed to signal a deeper correction.

- USD/CNH - Asian range 7.1706 - 7.1796, the USD/CNY fix printed 7.1534, Asia is currently dealing around 7.1720. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX +0.01%, Gold $3331, US 10-Year 4.39%, BBDXY 1194, Crude oil $67.52

Data/Events : France Trade Balance, Germany Trade Balance

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

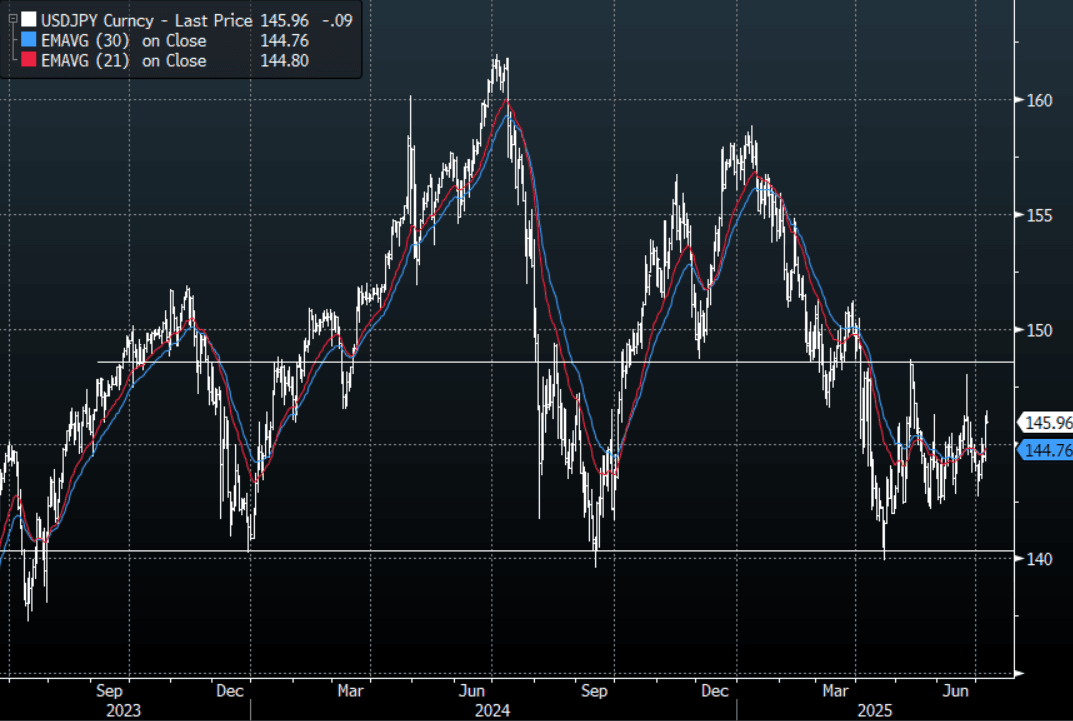

JPY: Asia Wrap - USD/JPY Finds Supply Towards 146.50

The Asia-Pac USD/JPY range has been 145.83 - 146.45, Asia is currently trading around 146.00, +0.05% having found decent supply towards the 146.50 area in our session. USD/JPY price action was telling overnight as it marched relentlessly higher challenging a market positioned the wrong way. Price is still well within the wider 142.00 - 148.00 range and the pair will probably continue to take its cue from the US rates market.

- (Bloomberg) -- “Japan’s super-long bonds extended their recent declines, pushing the yield on 30-year debt back above 3% and within sight of a record high. The moves come as investors weigh the impact of a new Aug. 1 deadline for US tariffs and as concern mounts that an upper house election in Japan on July 20 will usher in higher government spending.”

- Zerohedge on X: - “Impact of new tariff on Japan (if remains unchanged): JPM strategist Rie Nishihara expects a reciprocal tariff of 24% will lead to 0.4%-0.9% drag in Japan GDP and 7% decline in TOPIX 2025 EPS. The downside scenario estimated by Rie for NKY is 34,000.”

- (Bloomberg) -- Japanese Finance Minister Katsunobu Kato says that he’s not planning to hold talks specifically on currencies with US Treasury Secretary Scott Bessent in the near future.

- USD/JPY has lost all downside momentum for now and is back in its wider 142.00 - 148.00 range. The Market is long JPY and should the USD manage to follow through with yesterday's price action the risk is a move back to the top end of the range to further challenge the conviction of the shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.60($948m).Upcoming Close Strikes : 144.50($860m July9).

- CFTC data shows Asset managers increased their JPY longs slightly +94753, while leveraged funds maintained their longs they have tried to rebuild +15798.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

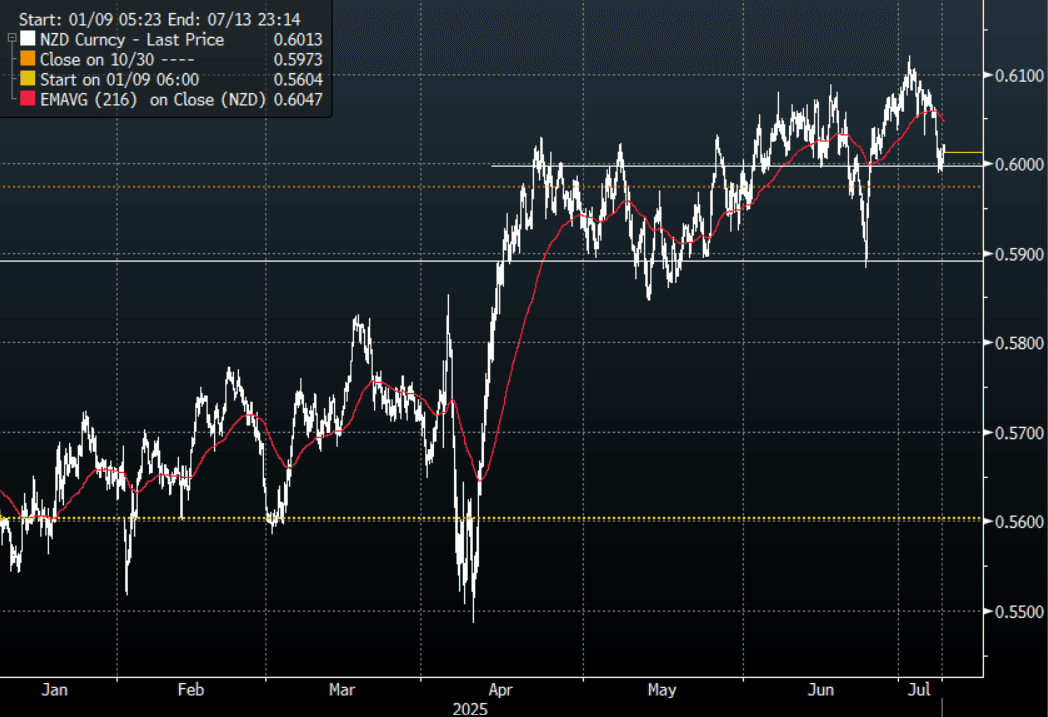

NZD: Asia Wrap - NZD/USD Demand Seen Just Below 0.6000

The NZD/USD had a range of 0.5995 - 0.6021 in the Asia-Pac session, going into the London open trading around 0.6015, +0.32%. The pair has drifted higher for most of our session as the market tries to view the Europe trade deal as a potential playbook and hopes that the Aug.1 deadline has not been set in stone. US Equity futures turned positive after opening lower in Asia, ESU5 +0.04%, NQU5 +0.20%. We have seen this ‘movie’ before and it normally ends with the USD faltering and moving lower again, is this time different ? The NZD found support again around the 0.6000 area as it tries to build a base from which to move higher, a sustained break below here though would risk a deeper correction back to 0.5850/0.5900.

- MNI RBNZ Preview-July 2025: Likely On Hold. The sell-side consensus is for the RBNZ to remain on hold tomorrow, which is also consistent with market pricing. There are some sell-side forecasters looking for a rate cut tomorrow, whilst most of those who see the RBNZ on hold, see risks of further cuts as we progress through 2025. For this meeting, our own bias is for the central bank to hold policy rates steady.

- RBNZ dated OIS pricing is little changed across meetings today, ahead of tomorrow's RBNZ Policy Decision. 3bps of easing is priced for this week's meeting, with a cumulative 32bps by November 2025.

- The NZD/USD has lost all its upward momentum and is back testing its support around the 0.6000 area. If risk has a deeper correction and the USD can find some upward momentum the risk is a move back towards the 0.5850/0.5900 area.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6075(NZD519m July 9), 0.6000(NZD407m July 10), 0.6025(NZD373m July10).

- CFTC Data shows Asset Managers have reduced their newly built longs in NZD +8515, the Leveraged community reduced their short last week -8424.

- AUD/NZD range for the session has been 1.0820 - 1.0839, currently trading 1.0830. The cross is struggling to get any momentum for now. It looks to be in a 1.0750 - 1.0850 range for now as it awaits a catalyst to provide some direction. Can the RBA today and RBNZ tomorrow give this pair the energy it needs to move higher again ?

Fig 1: NZD/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Stocks Advance on Hope of Further Negotiations

The headlines overnight focused on the imposition of tariffs on Japan and Korea and the sending of letters to other countries. However markets today focused on President Trump's suggestions that he remains open to further negotiations, further delaying tariffs until August. These comments eased earlier concerns .

- China's major bourses were strong with the Hang Seng leading the way with gains of +0.79%, CSI 300 up +0.74%, Shanghai Comp up +0.58% and Shenzhen rising +1.07%

- In Taiwan, the TAIEX was one of the few fallers, down -0.61% today.

- The KOSPI had a slow start to the day but things improved on Trumps comments and it has gained +1.40% to be one of the best performers of the major bourses.

- The FTSE Malay KLCI is down -0.54% and the Jakarta Comp down just -0.05%.

- The FTSE Straits Times in Singapore is up +0.45% and the PSEi in the Philippines down -0.17%

- The NIFTY 50 is doing very little following yesterday finishing flat.

OIL: Supply Concerns Re-assert as Oil Falls

- The realities of the August increase in supply and the potential further increase in September saw oil take a tumble in the Asia trading day.

- Down -0.46% at US$67.62 WTI remains at the mid-point between the 200-day EMA of $68.45 and the 20-day EMA of $66.93.

- Brent is down -0.43% at $69.30, sitting atop the 100-day EMA of $69.22

- The push pull of tariff headlines has increased volatility today as investors decipher the latest from the US and what the potential impact on global growth may be.

- There are looming supply chain risks in the Red Sea as Houthis rebels targeted a vessel near Yemen.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 08/07/2025 | 0600/0800 | ** | Trade Balance | |

| 08/07/2025 | 0645/0845 | * | Foreign Trade | |

| 08/07/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 08/07/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 08/07/2025 | - | ECB de Guindos At ECOFIN Meeting | ||

| 08/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 08/07/2025 | 1400/1000 | * | Ivey PMI | |

| 08/07/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/07/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 08/07/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 08/07/2025 | 1900/1500 | * | Consumer Credit | |

| 09/07/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 09/07/2025 | 0130/0930 | *** | CPI | |

| 09/07/2025 | 0130/0930 | *** | Producer Price Index | |

| 09/07/2025 | 0200/1400 | *** | RBNZ official cash rate decision | |

| 09/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 09/07/2025 | 0930/1030 | BOE Financial Stability Report | ||

| 09/07/2025 | 1000/1100 | BOE FSR Press Conference | ||

| 09/07/2025 | 1045/1245 | ECB Lane At House of the Euro | ||

| 09/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 09/07/2025 | 1100/1300 | EC De Guindos Closing Remarks At Conference |