MNI: Zero Bound Remains A Medium‑Term Risk - Fed's Williams

The risks that the Federal Reserve's policy rate will be pinned at the zero lower bound remains significant over the medium to long-term due to recent elevated uncertainty, according to a blog published Monday by the president of the Federal Reserve Bank of New York, John Williams, and two other Fed system economists.

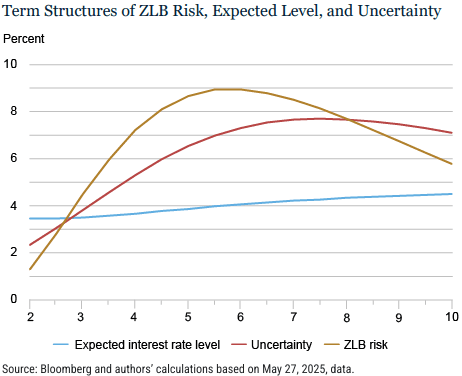

"Currently, seven-year-ahead ZLB risk is comparable to that observed in 2018, even though the expected interest rate level is higher. This reflects that uncertainty is higher today than it was in 2018," John Williams, Sophia Cho, and Thomas Mertens wrote.

The post examines to what extent markets are concerned that Fed policy might return to being constrained by the zero lower bound at some future date, using forward-looking financial market prices. The authors use price data for derivatives from January 2, 2007, to May 27, 2025, to construct a daily time series of ZLB risk for a range of forecast horizons.

The expected level of interest rates is a key driver of variation in ZLB risk over time, the authors find, but the term structure of uncertainty is upward-sloping, meaning that longer-horizon interest rate forecasts are less precise than shorter-horizon forecasts.

"While the expected level of interest rates at the seven-year horizon is about a full percentage point higher than in 2018, the current considerably elevated uncertainty offsets it and results in a comparable likelihood of reaching the ZLB," Williams and coauthors say.

"With an expected level of interest rates around 3–4%, the perceived risk of returning to the ZLB over the next two years is about 1%. This risk increases to about 9% at the seven-year horizon and remains at similar levels over longer horizons," they said. "To put the current term structure into context, medium- to long-term ZLB risk is currently at the lower end of the range observed over the past fifteen years. The last time seven-year-ahead ZLB risk reached a similar level was in 2018."