MNI EUROPEAN OPEN: RBA Cuts 25bps, Trims Forecasts

EXECUTIVE SUMMARY

- TRUMP SAYS RUSSIA AND UKRAINE TO START IMMEDIATE TALKS ON CEASEFIRE - RTRS

- JAPAN’S KATO PLANS BESSENT MEET TO DISCUSS TOPICS INCLUDING FX - BBG

- CHINA ACCUSSES US OF VIOLATING GENEVA DEAL WITH HUAWEI CURBS - BBG

CHINA MAY LPR DOWN 10BP - MNI BRIEF - RBA CUTS CASH RATE TO 3.85% - MNI BRIEF

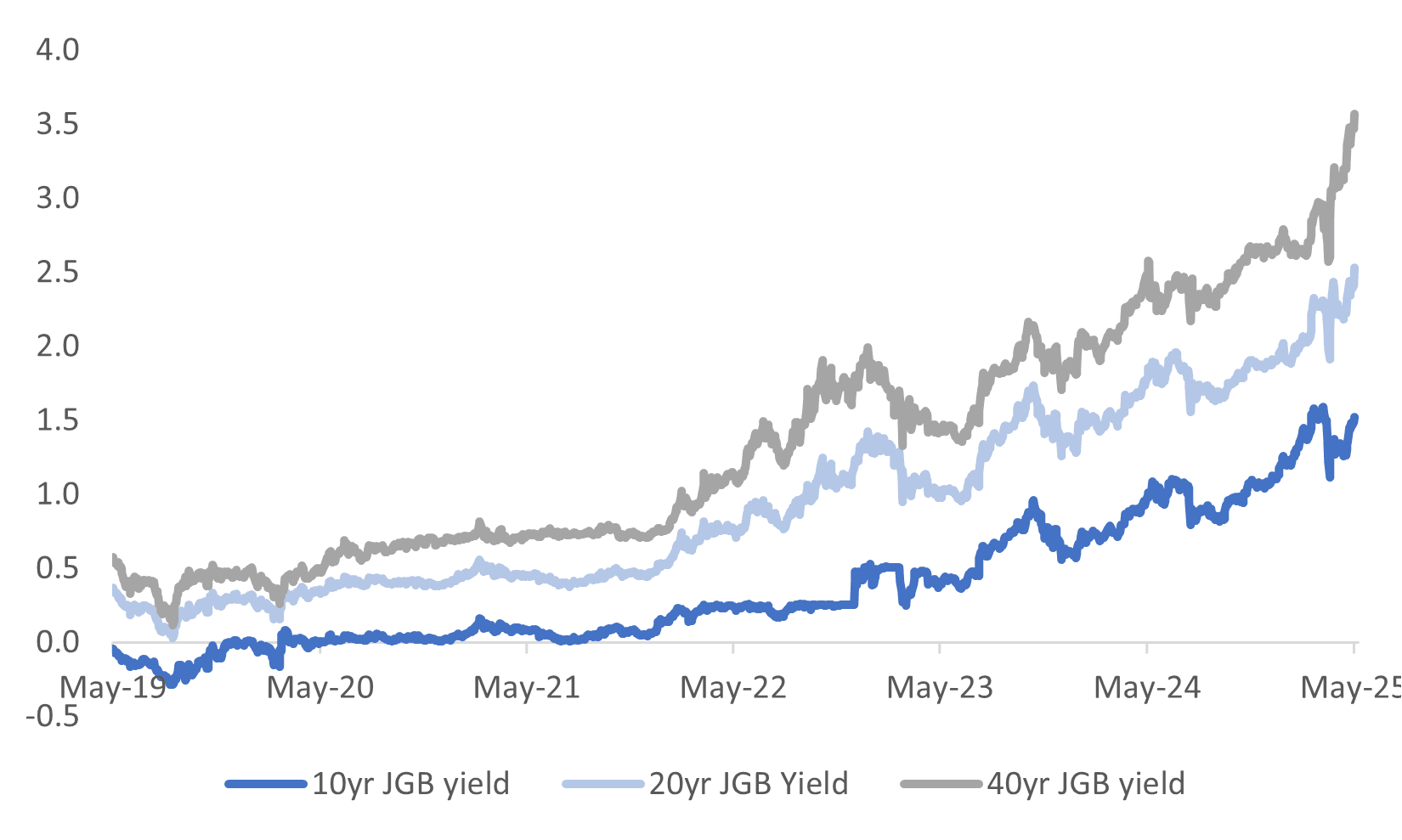

Fig 1: JGB Yields Spike Higher Following Poor 20yr Auction

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

BOE (MNI BRIEF): Bank of England Deputy Governor Clare Lombardelli has said moving away from basing its central forecast on the 'best collective judgement' of the Monetary Policy Committee to making it staff-led it was echoing the Scandinavian central banks, Norges Bank and the Riksbank and freeing up MPC members to focus on policy.

EU (BBC): “Prime Minister Sir Keir Starmer has said it is time to move on from "political fights" about Brexit, as the UK and the European Union agreed to a major reset of relations.”

IRAN (BBC): “Britain and Iran have summoned each other's envoys after three Iranians were charged with spying in the UK.”

EU

RUSSIA/UKRAINE (RTRS): “President Donald Trump spoke with President Vladimir Putin on Monday and said Russia and Ukraine will immediately start negotiations toward a ceasefire, but the Kremlin said reaching an agreement would take time and Trump indicated he was not ready to join Europe with fresh sanctions to pressure Moscow.”

EU (POLITICO): “The EU’s diplomatic branch is poised to downsize some 10 foreign delegations and cut an estimated 100 local staffers amid budget cuts and a broader reshuffle, according to a document seen by POLITICO and two officials familiar with the plans.”

US

FISCAL (BBG): “President Donald Trump plans to go to the Capitol on Tuesday to urge fractious House Republicans to overcome divisions and unite behind his signature tax-cut legislation.”

FED (MNI BRIEF): Federal Reserve Vice Chair Philip Jefferson said Monday monetary policy is "in a good place" and policymakers need to wait to see the cumulative impact of tariffs, budget decisions and immigration policies before making a move on interest rates.

US/CHINA (BBG): "The Chinese government accused the Trump administration of undermining recent trade talks in Geneva after it warned that using Huawei Technologies Co.’s artificial-intelligence chips “anywhere in the world” would violate US export controls."

OTHER

JAPAN (BBG): “ Japan’s Finance Minister said he’s arranging a bilateral meeting with US Treasury Secretary Scott Bessent this week to discuss topics including currency matters, triggering further gains in the yen.”

AUSTRALIA (BBG): "Australia’s decades-long Liberal-National tie-up will end after the leader of the National Party, David Littleproud, said his party won’t form another coalition agreement with the Liberal Party."

AUSTRALIA (MNI BRIEF): The Reserve Bank of Australia board cut the 4.1% cash rate by 25 basis points to 3.85% on Tuesday, citing substantially lower inflation and an uncertain outlook for the domestic economy.

INDIA (BBG): "India is discussing a US trade deal structured in three tranches and expects to reach an interim agreement before July, when President Donald Trump’s reciprocal tariffs are set to kick in, according to officials in New Delhi familiar with the matter. "

CHINA

LPRS (MNI BRIEF): China's Loan Prime Rate was reduced by 10bp on Tuesday, in line with expectations following the People’s Bank of China’s recent cut to the 7-day reverse repo rate.

POLICY STIMULUS (MNI BRIEF): China will launch most of its policy measures to stabilise employment and economic growth by the end of June, Li Chao, spokesman of the National Development and Reform Commission told reporters Tuesday.

CHINA/US (MOFCOM): “Beijing has called on Washington to cease discriminatory measures and honour the Geneva consensus, according to a spokesperson for the Ministry of Commerce, following a U.S. industry warning against using Chinese semiconductors, including Huawei.”

INFRASTRUCTURE (YICAI): “China’s infrastructure investment rose by 5.8% y/y from January to April, supported by the acceleration in issuance of local government special bonds earmarked for project development, according to Wang Qing, Chief Macro Analyst at Oriental Jincheng.”

DEPOSIT RATES (BBG): “Several major Chinese banks have cut their deposit rates in the latest efforts to reduce funding costs and preserve their shrinking profitability.”

SHARES (CSJ): “Chinese listed companies in the A-share market have received a total of 120.8b yuan in loans for stock buybacks or for their key shareholders to increase stakes as of May 19, according to a report by China Securities Journal.”

EXPORTS (SECURITIES TIMES): “ Several Chinese provinces and cities have published measures this month to help exporters expand their markets and secure more orders, according to a report by Securities Times.”

CHINA MARKETS

MNI: PBOC Net Injects CNY177 Bln via OMO Tuesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY357 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY177 billion after offsetting the maturities of CNY180 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4971% at 09:33 am local time from the close of 1.6014% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 50 on Monday, compared with the close of 45 on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.1931 Tues; +0.45% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1931 on Tuesday, compared with 7.1916 set on Monday. The fixing was estimated at 7.2107 by Bloomberg survey today.

MARKET DATA

SOUTH KOREA Q1 HOUSEHOLD CREDIT RISES TO KRW1,928.7T; Q4 KRW1,925.9T

SOUTH KOREA END-MARCH HOUSEHOLD CREDIT +0.1% Q/Q; END-DEC +0.6%

SOUTH KOREA END-MARCH HOUSEHOLD CREDIT +2.5% Y/Y; END-DEC. +2.1%

MARKETS

TYM5 has traded higher within a range of 110-06+ to 110-12 during the Asia-Pacific session. It last changed hands at 110-07+, up 0-03 from the previous close.

- The US 2-year yield is dealing around 3.974%, unchanged from its close.

- The US 10-year yield has drifted higher, dealing around 4.455%, up 0.01 from its close.

- (Bloomberg) -- Switzerland’s central bank chief gave a vote of confidence to US government bonds even after the world’s biggest economy was stripped of its last top credit rating by Moody’s.

- “US Treasuries are very liquid,” Swiss National Bank President Martin Schlegel said Monday in Lucerne. “There is currently no alternative to them and it’s not foreseeable that there will be an alternative.”

- "*FREEDOM CAUCUS CHAIR HARRIS SAYS VOTES NOT THERE FOR TRUMP BILL", HARRIS PREDICTS DEAL ON TRUMP TAX BILL DELAYED UNTIL JUNE"(BBG)

- The 10-year Yield failed once again to hold above 4.5%, likewise the 30-year Yield above the pivotal 5% level. A sustained break above this level could see another round of selling targeting the 4.75% area. Support seen back towards 4.35/40%, dips back towards here should see supply emerge once more.

- Data/Events : Tuesday's schedule includes the Philly Fed nonmanufacturing survey along with another slew of Fed speakers, including Collins, Barkin, Musalem, Kugler, Hammack and Daly.

JGBS: Very Poor 20Y Auction Sparks Sharp Bear-Steepener

JGB futures are sharply weaker, -24 compared to settlement levels, but well above session cheaps seen in the aftermath of today’s very poor 20-year auction.

- The low-price underperformed dealer forecasts, according to a Bloomberg poll. Moreover, the cover ratio decreased to 2.5007x from 2.9639x in the previous auction, and the auction tail lengthened dramatically from 0.34 to 1.14 – the longest since 1987. In post-auction dealing, the 20-year JGB hascheapened 13bps.

- Cash US tsys are slightly cheaper in today’s Asia-Pac session after yesterday’s modest gains.

- (Bloomberg) -- “House Speaker Mike Johnson said “we are almost there” on passing a sweeping US tax bill. Republicans are pushing to implement Medicaid work requirements in 2027, two years earlier than planned, Majority Leader Steve Scalise told CNBC.”

- (Bloomberg) - “Washington lawmakers are risking a "fiscal disaster" if a recession hits as they continue with their package of sweeping tax cuts, according to Guggenheim Securities Co-Chair Jim Millstein.”

- Cash JGBs have bear-steepened across benchmarks, with yields 1-13bps higher. The benchmark 20-year yield is 13bps higher at 2.543%.

- Swaps have also bear-steepened, with rates 1-11bps higher.

- Tomorrow, the local calendar will see Trade Balance data.

AUSSIE BONDS: Rallies After Cut & Dovish Tilt By RBA

ACGBs (YM +7.0 & XM +7.5) are sharply stronger on the day and richening 4-6bps after the RBA Policy Decision.

- The RBA cut the cash rate, as expected, by 25bps to 3.85% and left a dovish first impression in terms of the statement, by trimming its inflation (trimmed mean) and growth forecasts slightly.

- Last para of RBA Statement: “The Board will be attentive to the data and the evolving assessment of risks to guide its decisions. In doing so, it will pay close attention to developments in the global economy and financial markets, trends in domestic demand, and the outlook for inflation and the labour market. The Board is focused on its mandate to deliver price stability and full employment and will do what it considers necessary to achieve that outcome."

- Cash ACGBs are 7bps richer with the AU-US 10-year yield differential at flat.

- The bills strip has extended its strengthening after the RBA decision, led by late whites, with pricing +4 to +8.

- RBA-dated OIS pricing is flat to 7bps softer across meetings after the decision. A 25bp rate cut today was given a 95% probability. A cumulative 81bps of easing is now priced by year-end (-75bps before the data).

- Tomorrow, the local calendar will see the Westpac Leading Index.

- The AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond tomorrow and A$800mn of the 2.75% 21 November 2028 bond on Friday.

BONDS: Modest Bull-Flattener But NZ-US10YY Diff Wider

NZGBs closed showing a modest bull-flattener, with benchmark yields 1-3bps lower.

- Nevertheless, the NZ-US 10-year yield differential widened 3bps.

- The local market was closed at the time of the RBA decision. As a result, the post-RBA rally in ACGBs—driven by the rate cut and dovish shift—may positively influence NZGBs when trading resumes tomorrow morning.

- Cash US tsys are slightly cheaper in today's Asia-Pac session after yesterday's modest gains.

- (Bloomberg) -- Switzerland’s central bank chief gave a vote of confidence to US government bonds even after the world’s biggest economy was stripped of its last top credit rating by Moody’s.

- “US Treasuries are very liquid,” Swiss National Bank President Martin Schlegel said Monday in Lucerne. “There is currently no alternative to them and it’s not foreseeable that there will be an alternative.”

- Swap rates closed 2-5bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed little changed across meetings. 25ps of easing is priced for May, with a cumulative 63bps by November 2025.

- Tomorrow, the local calendar will see Trade Balance data ahead of the Budget on Thursday.

- On Friday, the NZ Treasury plans to sell NZ$250mn of the 3.00% Apr-29 bond, NZ$150mn of the 3.50% Apr-33 bond and NZ$50mn of the 1.75% May-41 bond.

AUD: Asia Wrap - AUD Lower As RBA Lowers Inflation & Growth Forecasts

The AUD/USD has had a range of 0.6423 - 0.6459 in the Asia- Pac session, it is trading around 0.6425. The RBA lowered rates by 25 basis points as expected to 3.85% and lowered inflation and growth forecasts.

- The AUD has come off as the RBA lowers inflation and growth forecasts: “ The Board judged that the risks to inflation have become more balanced. Inflation is in the target band and upside risks appear to have diminished as international developments are expected to weigh on the economy. With inflation expected to remain around target, the board therefore judged that an easing in monetary policy at this meeting was appropriate.”

- "AUSTRALIA NATIONAL PARTY LEADER LITTLEPROUD: ENDING COALITION WITH LIBERAL PARTY, NATIONAL PARTY WILL SIT ALONE ON A PRINCIPLE BASIS - [RTRS]"

- The AUD/USD has found demand around 0.6400 again overnight, expect buyers to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6350(AUD367m May 20), Upcoming Strikes : 0.6375(AUD483.6m May 23), 0.6550(AUD480.3m May 23)

- AUD/JPY - Today's range 93.02 - 93.84, it is trading currently around 93.05. Decent demand seen towards the 93.00 area where it holds again overnight. A sustained close back below 91.50/92.00 is needed to turn the focus back towards the lows again. If stocks continue to press higher AUD/JPY could drift back towards the 96.00 area.

FOREX: Asia FX Wrap - Risk Sees Some Reversion, The USD Holds Steady

The BBDXY has had a range of 1224.40 - 1226.87 in the Asia-Pac session, it is currently trading around 1225. China Prime Rates Lowered As Expected: The 1 and 5 year Loan Prime Rates were reduced in line with expectations. The move lower by 10bps for each sees the 1-year LPR to 3.00% and the 5-year LPR to 3.50%, the lowest they have been since inception. CATL’s huge listing on the Hong Kong exchange produced an early jump for the shares, which is lifting the Hang Seng Index as the trading debut will also encourage more IPOs to list in the city on attractive valuations.(BBG)

- EUR/USD - Asian range 1.1218 - 1.1251, Asia is currently trading 1.1245.The market is still expected to use dips as a buying opportunity with dips back towards 1.09/1.10 well supported.

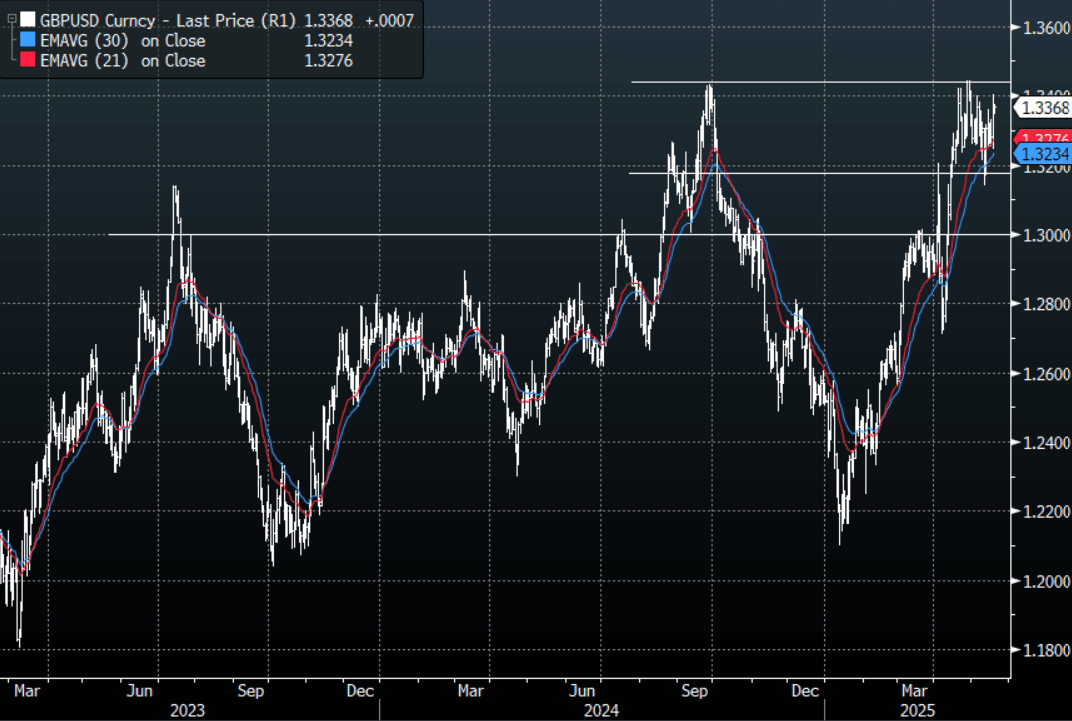

- GBP/USD - Asian range 1.3345 - 1.3376, Asia is currently dealing around 1.3370. Decent demand for GBP sub 1.3200 has seen it bounce back and it looks likely to test the upper bounds of its range above 1.3400. Like the EUR the market prefers to buy on dips.

- USD/CNH - Asian range 7.2128 - 7.2263, the USD/CNY fix printed 7.1931. Asia is currently dealing around 7.2230. Sellers should be found on a bounce back towards 7.24/25 again.

- Cross asset : SPX -0.3%, Gold $3215, US 10-Year 4.45%, BBDXY 1225, Crude oil $62.72

Data/Events : Ger PPI, EZ Current A/C, EZ Construction Output, EZ Consumer Confidence, Philly Fed nonmanufacturing survey

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

NZD: Asia Wrap - NZD Drifts Lower

The NZD/USD had a range of 0.5913 - 0.5932 in the Asia-Pac session, going into the London open around 0.5920. US Stocks have drifted lower today, paring back a little of their overnight gains.

- US President Trump has had a two hour conversation with Russian President Putin about the war in the Ukraine. Trump said that he believes that Putin wants peace. While he said that peace talks would begin "immediately", it remains unclear what the next steps will be, especially as the unconditional 30-day ceasefire was not discussed between the two leaders.

- The NZD/USD traded closely with US stocks, paring back some overnight gains before demand was seen again back towards 0.5900.

- The NZD now seems to be comfortable in a 0.5800/0.6050 range and awaits a catalyst to provide the impetus to break-out.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. The first target is the highs just above 0.6000, a break above here is needed to regain momentum.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none, Upcoming Strikes : 0.5705(NZD805.1m May 23), 0.6150(NZD356.1m May 23)

- AUD/NZD range for the session has been 1.0880 - 1.0897, currently trading 1.0885. The Cross has found some supply just above 1.0900, support is seen back towards 1.0800. A sustained break above 1.0920 would turn the focus higher.

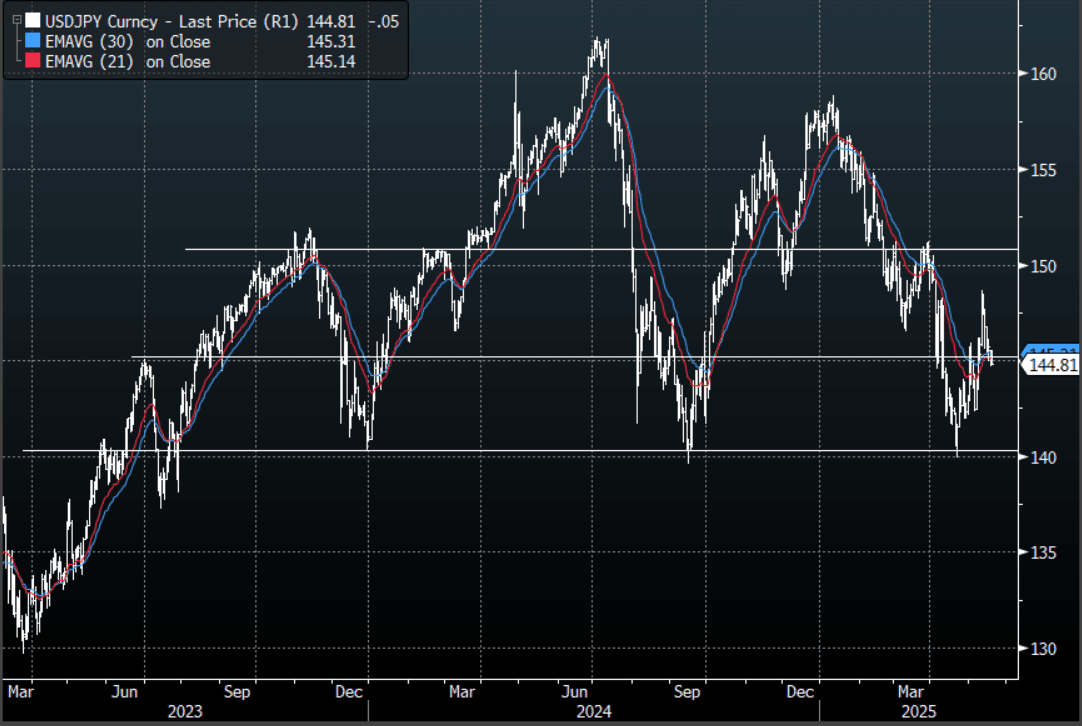

JPY: Asia Wrap - Kato Remarks Test Overnight Lows

The Asia-Pac range has been 144.73 - 145.51, Asia is currently trading around 144.80. Early demand for USD’s going into the Japanese Fix was met by fresh selling reacting to comments from the Japanese Finance minister Kato, this saw a quick move to revisit the overnight lows where some demand again returned.

- "*KATO: ARRANGING BESSENT MEETING TO DISCUSS TOPICS INCLUDING FX, TALKS W BESSENT ON FX WILL SEEK TO FOLLOW EXISTING STANCE" - BBG

- Akazawa made comments this morning reiterating his commitment to seek a removal of “All US Tariffs”.

- Very poor demand seen in the 20-year JGB auction today, tail the longest since 1987.

- Nippon Steel pledged to invest more in US Steel — including building a new mill and preserving jobs — if the US approves their merger, people familiar said.(BBG)

- USD/JPY continues to test its support and the price action is interesting considering the bounce in stocks.

- The support around 144/145 looks important now and a break would once again bring the focus back to the pivotal 140.00 area. The price action though does not look great and the market is still more comfortable selling rallies.

Options : Closest significant option expiries for NY cut, based on DTCC data: 145.50($1.03b May 20), 145.00($789.7m May 20) , Upcoming Strikes : 145.00($2b May 23),144.00($1.37b May 23), 140.00(1.67b May 23)

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Key Bourses Positive Today

One of the key IPO's in Asia this year is EV battery marker CATL. Making its trading debut this week in Hong Kong CATL's shares jumped 14% even after its initial pricing was at the top end of expectations.

This gave a boost to the Hang Seng which had fallen for three days straight prior to CATL's first day of trading, as it delivered a strong rally.

- China's Hang Seng is up +1.29% today taking back the losses incurred over recent days. The CSI 300 was up +0.62%, the Shanghai Comp up +0.38% and the Shenzhen Composite is up +0.86%.

- The KOSPI barely moved today as it lacked direction and rose just +0.03% after yesterday's fall of -0.89%.

- The FTSE Bursa Malaysia KLCI index is lower by -0.42% as the index falls for a fourth straight day despite stronger than expected trade data today.

- Indonesia's Jakarta Composite has rallied 18 out of the last 20 trading days and is up again today by +0.36%.

- Singapore's FTSE Straits Times is up +0.19% and the PSEi in the Philippines is lower by -1.5%.

- India's NIFTY 50 continued to fall for a third straight day, down -0.20%.

OIL: Crude Range Trading, Not Finding Support From Better Risk Appetite

Oil prices are close to flat in today’s APAC trading as the market continues to watch closely progress on trade, Iran and Ukraine. It hasn’t benefited from today’s better risk tone. WTI is around $62.16/bbl after a high of $62.33 followed by a low of $62.02. Brent is flat at around $65.54/bbl following a peak of $65.72 early in the session but off the trough of $65.39. The USD index is also little changed.

- Trade deals are important for the energy demand outlook, while agreements on Iran and Ukraine could increase oil supply if sanctions are eased.

- Following his discussion with Russian President Putin, US President Trump said that he believes that Putin wants peace. While he said that peace talks would begin “immediately”, it remains unclear what the next steps will be. Like with negotiations on Iran’s nuclear programme, progress is uncertain and success or failure will have some impact on global oil supplies.

- With the IEA continuing to forecast excess supply in both 2025 and 2026 and the market looking for signs of uncertainty impacting the US economy, industry-based US crude inventory data out later today will be monitored for indications of softening demand.

- Later the Fed’s Bostic, Barkin, Collins, Musalem, Kugler and Hammack appear and the Atlanta Fed’s conference continues. The ECB’s Lagarde and Cipollone attend the G7 meeting, while Buch, Cipollone and Donnery speak. In terms of data, US May Philly Fed non-manufacturing and Canadian April CPIs are released.

GOLD: Correction Continues As Risk Sentiment Improves

Gold prices are down 0.5% to $3212.15/oz so far today as better risk appetite weighs. They rose 0.8% to $3229.61 on Monday supported by safe-haven buying following Moody’s US sovereign downgrade. US Treasury yields are little changed in APAC trading, while the USD index is range trading and flat.

- Bullion reached $3232.72 earlier today but then trended down to $3204.71. It continues to trade between initial resistance at $3259.5, 20-day EMA, and initial support at $3121.0, 15 May low. It is almost 2% lower this month as more conciliatory trade developments have helped improve the global growth outlook, but with US tariffs only delayed and not scrapped uncertainty remains high.

- Asian equities are rallying with the Hang Seng up 1.4% but the S&P e-mini down 0.3%. Oil prices are little changed with WTI around $62.19/bbl. Copper is 0.4% lower and iron ore approaching $100/t. Silver is 0.5% lower at $32.19.

- Later the Fed’s Bostic, Barkin, Collins, Musalem, Kugler and Hammack appear and the Atlanta Fed’s conference continues. The ECB’s Lagarde and Cipollone attend the G7 meeting, while Buch, Cipollone and Donnery speak. In terms of data, US May Philly Fed non-manufacturing and Canadian April CPIs are released.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 20/05/2025 | 0430/1430 | *** | RBA Rate Decision | |

| 20/05/2025 | 0600/0800 | ** | PPI | |

| 20/05/2025 | 0800/1000 | ** | EZ Current Account | |

| 20/05/2025 | 0800/0900 | BOE's Pill At Barclays Briefing | ||

| 20/05/2025 | 0900/1100 | ** | Construction Production | |

| 20/05/2025 | 1000/1200 | ECB's Cipollone pre-rec video at Sustainability Festival | ||

| 20/05/2025 | - | ECB's Lagarde and Cipollone at G7 Meeting | ||

| 20/05/2025 | 1230/0830 | *** | CPI | |

| 20/05/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 20/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 20/05/2025 | 1300/0900 | Richmond Fed's Tom Barkin | ||

| 20/05/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 20/05/2025 | 1700/1300 | St. Louis Fed's Alberto Musalem | ||

| 20/05/2025 | 2100/1700 | Fed Governor Adriana Kugler | ||

| 20/05/2025 | 2300/1900 | San Francisco Fed's Mary Daly | ||

| 20/05/2025 | 2300/1900 | Atlanta Fed's Raphael Bostic | ||

| 20/05/2025 | 2300/1900 | Cleveland Fed's Beth Hammack | ||

| 21/05/2025 | 2301/0001 | * | Brightmine pay deals for whole economy | |

| 21/05/2025 | 0600/0700 | *** | Consumer inflation report | |

| 21/05/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 21/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index |