MNI EUROPEAN OPEN: ISM Chief Sees No End to Factory Slump

EXECUTIVE SUMMARY

- ISM CHIEF SEES NO END IN SIGHT TO FACTORY SLUMP - MNI

- UEDA SHARPENS DEC RATE HIKE, RISKS CREDIBILITY - MNI

- THE US COMMERCE DEPARTMENT HAS AGREED TO INVEST IN AN AI CHIP STARTUP - BBG

- THE UK WILL ADOPT A MORE PRO-BUSINESS APPROACH TO CHINA - BBG

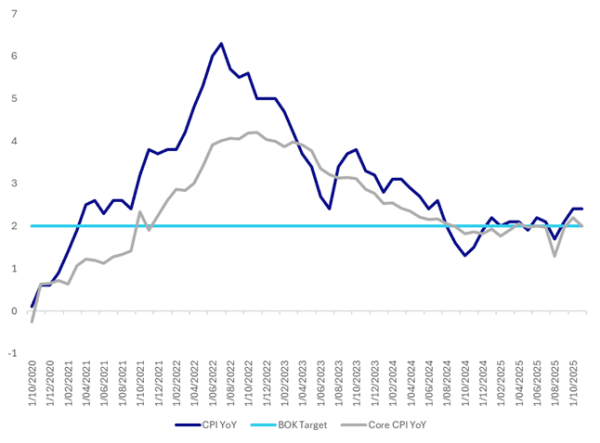

- SOUTH KOREA CPI RISE 2.4% IN NOVEMBER, SURPASSING 2% TARGET FOR 3 CONSECUTIVE MONTHS - KOREA TIMES

Fig 1: South Korea CPI YoY + Core CPY YoY vs BOK Target

Source: Bloomberg Finance L.P./MNI

UK

POLITICS/ BUDGET (MNI): The UK's Office for Budget Responsibility chairman Richard Hughes resigned on Monday, following a report into the "inadvertent" leak of the OBR's forecasts before the Nov 26 budget.

UK/EU TRADE (BBC): “The UK and the US have agreed a deal to keep tariffs on UK pharmaceutical shipments into America at zero. Under the agreement the UK will pay more for medicines through the NHS in return for a guarantee that US import taxes on pharmaceuticals made in the UK will remain at zero for three years.”

UK/CHINA RELATIONS (BBG): “The UK will adopt a more pro-business approach to China but not trade its national security for greater trade ties, Keir Starmer said as he sought to clarify his Labour administration’s approach to the Asian nation.”

ECONOMY (TIMES): “Retailers launched Black Friday deals earlier than usual this year, helping to keep shop price inflation in check. Overall shop prices were 0.6 per cent higher than a year ago in November, down from 1 per cent in October, according to the British Retail Consortium and the market researchers NIQ.”

EU

EU/UKRAINE (MNI): EU High Representative Kaja Kallas said Monday the group can address concerns Belgium has with its proposed €140 billion 'Reparations Loan' for Ukraine. "I don't diminish the worries Belgium has," she said. "We can shoulder these risks together."

EU/UKRAINE (BBC): “President Zelensky has said Kyiv's priorities in peace talks to end the war with Russia are maintaining Ukraine's sovereignty and securing strong security guarantees. Zelensky said "the territorial issue is the most difficult", as Russia continues to demand that Ukraine give up areas of the eastern Donbas region that it still holds – which Kyiv maintains it will never do.”

AUTO SECTOR (BBG): “A European Union review that could potentially soften the bloc’s looming ban on sales of new combustion-engine vehicles might be postponed by several weeks, according to EU Transport Commissioner”

UKRAINE (POLITICO): “ Despite demands from Washington to reach a peace deal ending the war in Ukraine, French President Emmanuel Macron on Monday insisted that there's still a lot of work to do before any agreement.”

BUSINESS (ECONOMIST): “On Tuesday the Court of Justice of the European Union (CJEU) will issue a preliminary ruling on a class-action suit against Apple and its Irish subsidiary, which is proceeding in a Dutch court. The ruling will determine whether the Amsterdam District Court has jurisdiction under EU law to “centralise” complaints.”

US

MANUFACTURING (MNI): U.S. manufacturing will remain in contraction as demand remains weak and for as long as trade uncertainty continues to be a drag on businesses, Institute for Supply Management manufacturing chair Susan Spence told MNI. "I do not see anything that will turn the ship," Spence said in an interview. "The [trade] uncertainty still continues to kill us."

CHIP MANUFACTURING (BBG): 'The US Commerce Department has agreed to invest as much as $150 million in xLight Inc., a chip technology startup tied to former Intel Corp. Chief Executive Officer Pat Gelsinger. "

CANADA

DEFENSE (BBG): “Canada has reached a deal to join the European Union’s €150 billion ($174 billion) military procurement fund, the country’s defense minister said, though the access fee has yet to be announced.”

OTHER

MARKET RISK (BBG): “Almost $1 billion of leveraged crypto positions were liquidated during another sharp drop in prices on Monday that brought fresh momentum to a wide-ranging selloff.”

SOUTH KOREA INFLATION (KOREA TIMES): "Korea's consumer prices grew over the Bank of Korea's 2 percent target for the third consecutive month in November, largely due to sharp increases in agricultural and petroleum product prices, government data showed Tuesday."

JAPAN

MONETARY POLICY (MNI): A hold at the Bank of Japan’s Dec. 18–19 meeting would be inconsistent with the bank’s recent market communications and would undermine its credibility, following Governor Kazuo Ueda’s comments on Monday that strongly indicated policymakers are set to raise the 0.5% rate this month, MNI understands.

JAPAN / CHINA RELATIONS (BBG): "The dispute between China and Japan could drag on for a year, Taiwanese Foreign Minister Lin Chia-lung said, adding Taipei hopes the two sides can find a way to ease tensions."

CHINA

MNI China Press Digest Dec 2: Vanke, REITs, 2026 Economy

PROPERTY SECTOR (BBG): " China Vanke Co., the embattled developer that rattled markets last week with an unexpected request to delay a local bond payment, has again shocked creditors with details of the plan."

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY156.3 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY145.8 billion after offsetting maturities of CNY302.1 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4174% at 09:47 am local time from the close of 1.4580% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 51 on Monday, compared with the close of 48 on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.0794 on Tuesday, compared with 7.0759 set on Monday. The fixing was estimated at 7.0745 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND TERMS OF TRADE INDEX QoQ 3Q: -2.1%; EST 0.4%; PRIOR 4.2% (REVISED UP)

AUSTRALIA NET EXPORTS OF GDP 3Q: -0.1PP; EST 0.0; PRIOR 0.1

AUSTRALIA BOP CURRENT ACCOUNT BALANCE 3Q: -A$16.6bn; EST -A$13.0bn, PRIOR -A$16.2bn (REVISED UP)

AUSTRALIA BUILDING APPROVALS MoM OCTOBER: -6.4%, EST -4.5%, PRIOR 11.1% (REVISED DOWN)

AUSTRALIA PRIVATE SECTOR HOUSES MoM -2.1%; PRIOR 3.2% (REVISED DOWN)

JAPAN NOV. MONETARY BASE -8.5% Y/Y; OCT. -7.8%

JAPAN END-NOV. MONETARY BASE OUTSTANDING Y608.47T; OCT. Y619.2T

SOUTH KOREA CPI MoM NOVEMBER -0.2%, EST -0.3%, PRIOR 0.3%

SOUTH KOREA CPI YoY NOVEMBER 2.4%, EST 2.3%, PRIOR 2.4%

SOUTH KOREA CPI ex FOOD & ENERGY YoY NOVEMBER 2.0%, EST 2.0%, PRIOR 2.2%

MARKETS

US TSYS: Yields Mixed; TYH6 Gives Back Earlier Gains

US bond futures remain higher in the Asia trading day, though gave back some of the earlier gains. The US 10-Yr (TYH6) is up +01+ to 112-27 having touched 112-29 earlier. TYH6 sits atop the 50-day EMA of 112-27+ with upside resistance above at 113 for the 20-day EMA.

Earlier in the day cash was modestly better across the curve, but the early gains faded in the afternoon, leaving yields mixed and the 10-Yr now firmly above 4%. .

- The 2-Yr is at 3.531% : -0.2bps

- The 5-Yr is at 3.667% : +0.2bps

- The 10-Yr is at 4.088% unch

- The 30-yr is at 4.735% : -0.3bps

LOOKING AHEAD to tonight at the Tuesday Data Calendar: Vehicle Sales, Fed VC Bowman Testimony

- The issuance schedule is light tonight with the focus on an auction of US$75bn 6-week bills.

JGBS: Yields Reverse After A Strong 10Y Auction

JGB futures are stronger, +20 compared to settlement levels, and hovering near session bests after today’s 10-year auction.

- The 10-year JGB auction delivered strong results, with the low price beating expectations at 98.50, according to the Bloomberg dealer poll. Moreover, the cover ratio increased to 3.5913x from 2.9734x and the tail shortened to 0.04 from 0.13.

- This performance came with an outright yield at a fresh cycle high, around 20bps higher than the level of last month's auction.

- The 2s/10s curve was also steeper than the levels at last month's auction and sat at a new cycle high of 86bps.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday’s bear-steepener.

- Cash JGBs are slightly richer across benchmarks. The benchmark 10-year yield is 0.5bp lower at 1.868% versus today’s fresh cycle high of 1.886%. (see chart)

- Swap rates are flat to 1bp lower.

- BOJ Governor Kazuo Ueda said Monday that even if the policy rate were raised to 0.75% from 0.50%, overall financial conditions would remain accommodative.

- Market pricing has shifted sharply recently. BOJ-dated OIS now assigns an 80% probability to a 25bp hike in December, rising to 104% by March 2026.

- Tomorrow, the local calendar will see S&P Global PMIs (Composite & Services).

Source: Bloomberg Finance LP

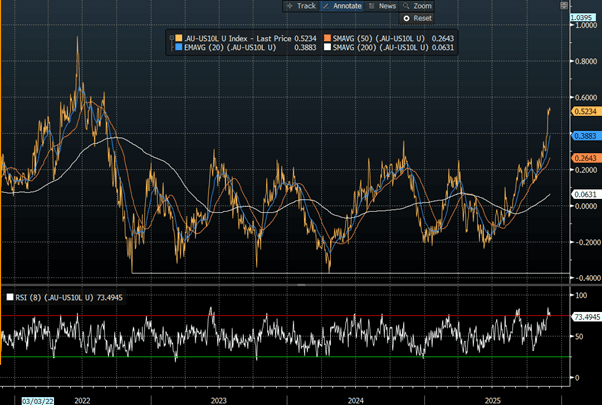

AUSSIE BONDS: Bear-Steepener Ahead Of Q3 GDP, AU-US 10Y Diff Widest Since Mid-22

ACGBs (YM -3.0 & XM -6.0) are weaker, hovering near session cheaps ahead of tomorrow’s Q3 GDP release.

- Bloomberg consensus expects Q3 GDP growth to accelerate to 0.7% q/q and 2.2% y/y, from 0.6% and 1.8% in Q2. A stronger print would give the RBA further justification to extend its pause.

- Net exports detracted 0.1pp from Q3 quarterly GDP growth, which, with the inventory print, would normally pose a downside risk to the consensus’ forecast of +0.7% q/q but public demand’s 0.4pp contribution is an upside risk.

- Cash ACGBs are 2-6bps cheaper with the AU-US 10-year yield differential at +53bps, its highest since mid-2022. (see chart)

- The bills strip has bear-steepened, with pricing -1 to -4.

- RBA-dated OIS pricing shows zero probability of a 25bp rate cut in December.

- The recent firming in rate expectations stems from the stronger-than-expected Monthly CPI released on 26 November. OIS pricing is now 5–20bps higher for meetings beyond December compared with pre-CPI levels.

- The market has also shifted to assign a 59% probability of a 25bp hike by December 2026.

- The AOFM plans to sell A$1000mn of the 4.25% 21 December 2035 bond on Wednesday and A$1000mn of the 2.75% 21 November 2028 bond on Friday

Bloomberg Finance LP

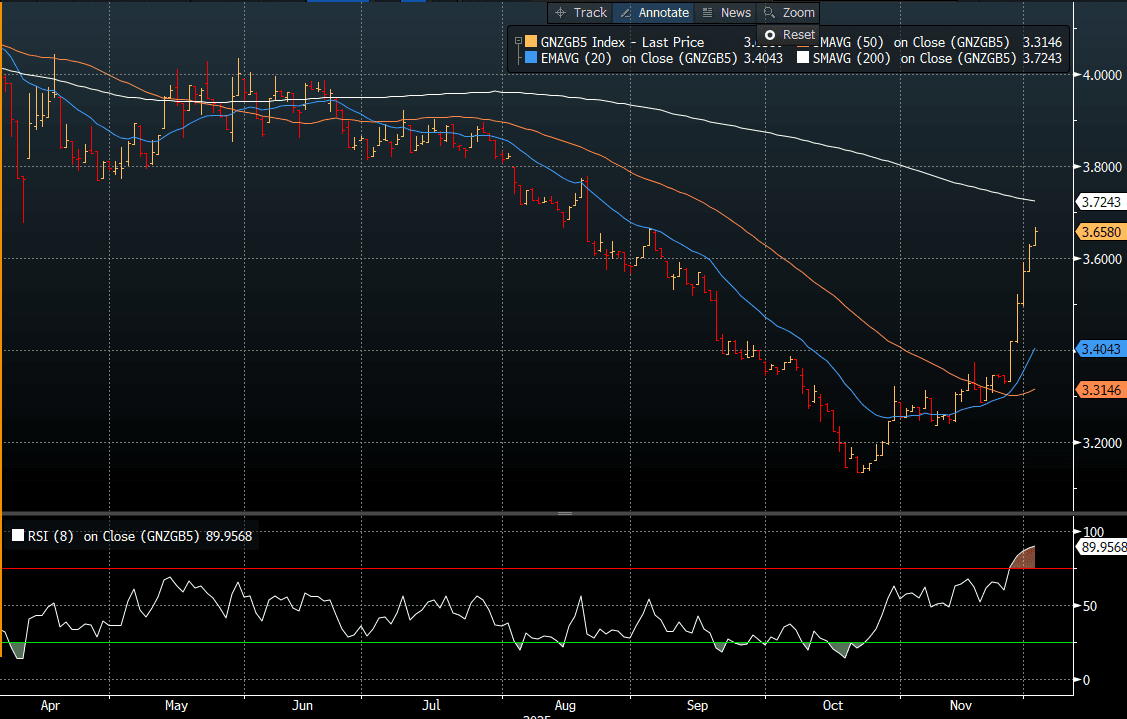

BONDS: NZGBS: Closed Showing Twist-Steepener, 5YY +30Bps Since RBNZ Decision

NZGBs closed showing a twist-steepener, with benchmark yields 1bp lower to 5bps higher.

- As it stands, yields are 16-32bps higher than pre-RBNZ levels, led by the 5-year (see chart).

- On a relative basis as well, NZGBs have underperformed recently, with the NZ-US 10-year yield differential closing at +28bps. For context, this differential sat around zero around two weeks ago.

- RBNZ-dated OIS pricing closed little changed across meetings. 2bps of easing is priced for February, while November 2026 assigns 33bps of tightening.

- Tomorrow, the local calendar will see ANZ Commodity Price data.

- On Thursday, the NZ Treasury plans to sell NZ$150mn of the 4.50% May-30 bond, NZ$225mn of the 4.50% May-35 bond and NZ$75mn of the 2.75% May-51 bond.

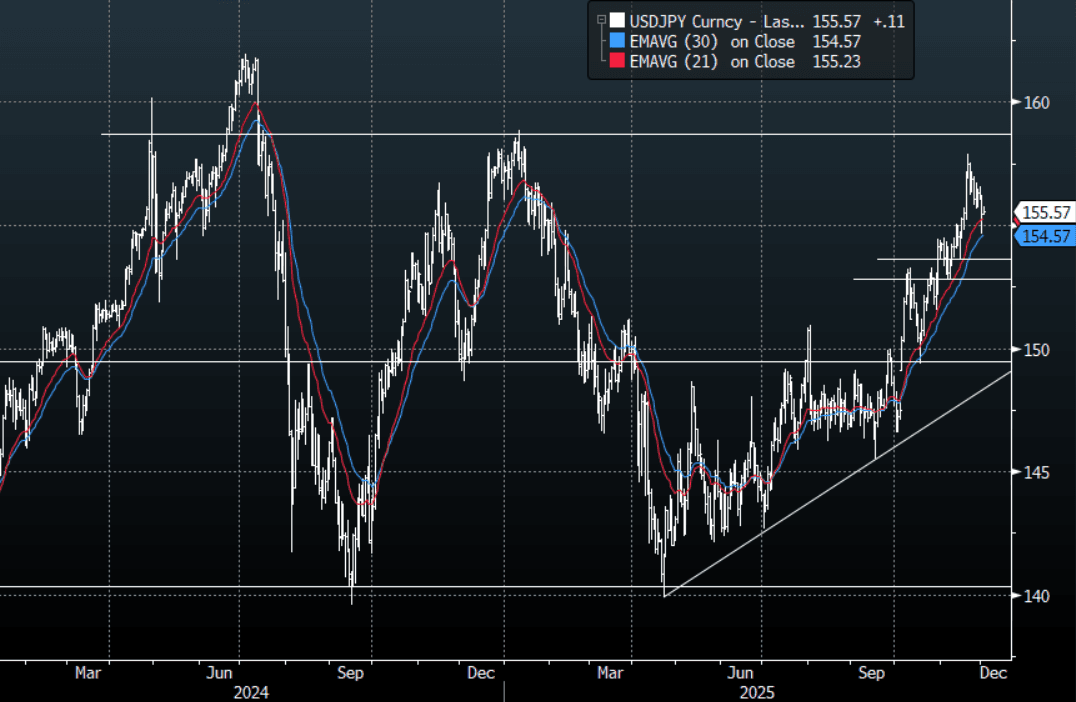

JPY: USD/JPY - Drifts Higher In A Quiet Session

The USD/JPY range today has been 155.43 - 155.77 in the Asia-Pac session, it is currently trading around 155.60, +0.10%. The pair has tried to move higher after its strong bounce from the lows seen in New York. The market is pricing in the fact that the Yen move looks like it could force the BOJ into action in December. This should keep the move that looked about to go parabolic a little more contained. Technically USD/JPY continues to look like it wants to test higher with the first big support back toward the 154-155 area seeing lots of demand on the first attempt. On the day I suspect we will consolidate, looking for sellers to reemerge back toward the 156.00-30 initially. First strong support remains in the 153.00-155.00 area.

- OMFIF printed a commentary on Japanese Foreign Exchange Policy: “The MoF feels it has to do something. Rather than Japan confronting its policy mix, the finance minister jawbones about the weak yen, threatens intervention and decries that markets are one-sided, disorderly and not reflecting underlying fundamentals. But while significant short positions may occasionally build up, trading in yen is not disorderly – business is getting done, liquidity is good and bid/offer spreads are narrow. Rather, markets are reflecting fundamentals and voting on Japanese economic policy. Ultimately, the weak yen in significant part reflects Japanese policy incoherence.” https://www.omfif.org/2025/12/japanese-foreign-exchange-policy-riddled-in-contradictions/

- MNI AU - A BoJ Hike Fully Priced By March With Two Hikes By October 2026:

- BOJ Governor Kazuo Ueda said Monday that even if the policy rate were raised to 0.75% from 0.50%, overall financial conditions would remain accommodative.

- "JAPAN’S 30-YEAR YIELD HITS FRESH RECORD HIGH SINCE 1999 DEBUT" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.00($2.59b),156.00($885m), 156.50($951m). Upcoming Close Strikes : 153.00($1.2b Dec 4), 155.00($1.4b Dec 5), 155.50($1.11b Dec 3) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 94 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

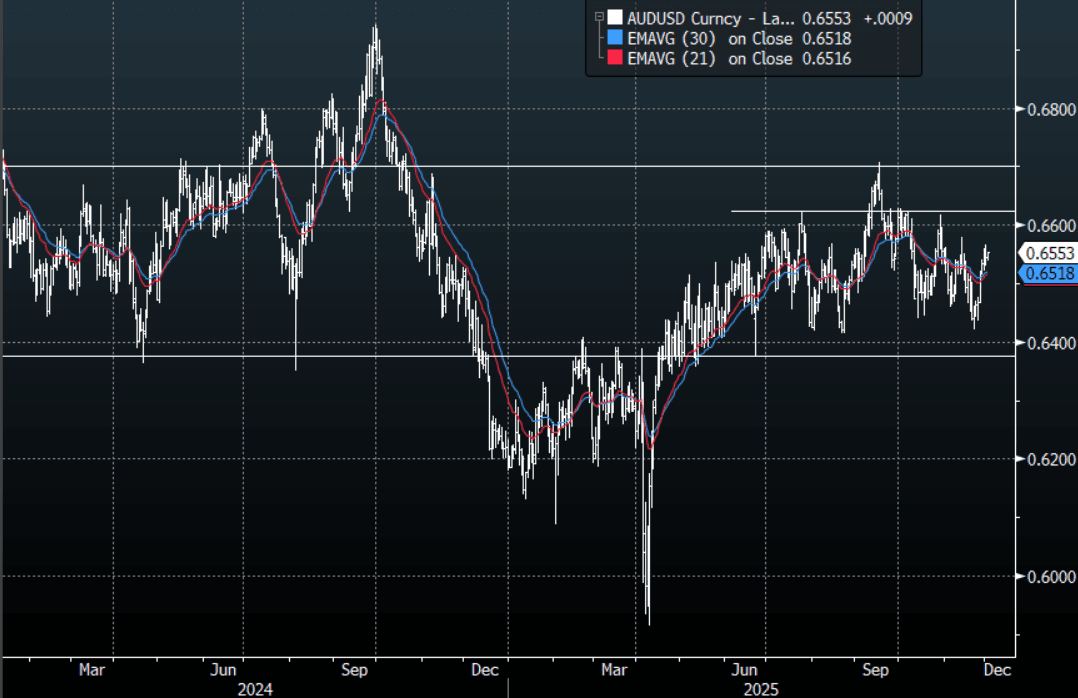

AUD/USD - Consolidates Around 0.6550, Shrugs Off Risk-Off Worries

The AUD/USD has had a range today of 0.6538 - 0.6552 in the Asia- Pac session, it is currently trading around 0.6545, -0.10%. The AUD/USD has had a subdued session again as risk attempts to stabilize after its fragile start to the week. The AUD is consolidating around the pivot toward 0.6560-80 within its wider 0.6350-0.6700 range. On the day, I still think risk-reward probably favours a slight short skew but back above 0.6580 and the focus will turn to the highs of the range. On the day support should be seen back toward the 0.6500-20 area initially.

- MNI AU - Slight Q3 Net Export Detraction As Trade Surplus Narrows: Net exports detracted 0.1pp from Q3 quarterly GDP growth, which with the inventory print would normally pose a downside risk to consensus’ forecast of +0.7% q/q but public demand’s 0.4pp contribution is an upside risk. Q3 balance of payments was also released and not only did the current account deficit widen, when a narrowing was forecast, but it was revised substantially higher in Q2 to $16.2bn. Q3 was $0.4bn higher at $16.6bn, the highest since Q4 2024, as the trade surplus narrowed.

- MNI AU - Sideways Dwelling Approvals To Add To Housing Inflation: The number of building approvals fell 6.4% m/m in October, weaker than expected, after rising 11.1% m/m to be down 1.8% y/y. Multi-dwelling approvals have been driving the volatility in the headline number but annual growth in both it and private houses is soft and likely to add to already strong house price growth. Approvals have moved sideways this year.

- "ANZ NO LONGER SEES ONE FINAL RBA RATE CUT IN 1H 2026" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6800(AUD532m). Upcoming Close Strikes : 0.6490(AUD710m Dec 4), 0.6500(AUD1.13b Dec 5) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 36 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

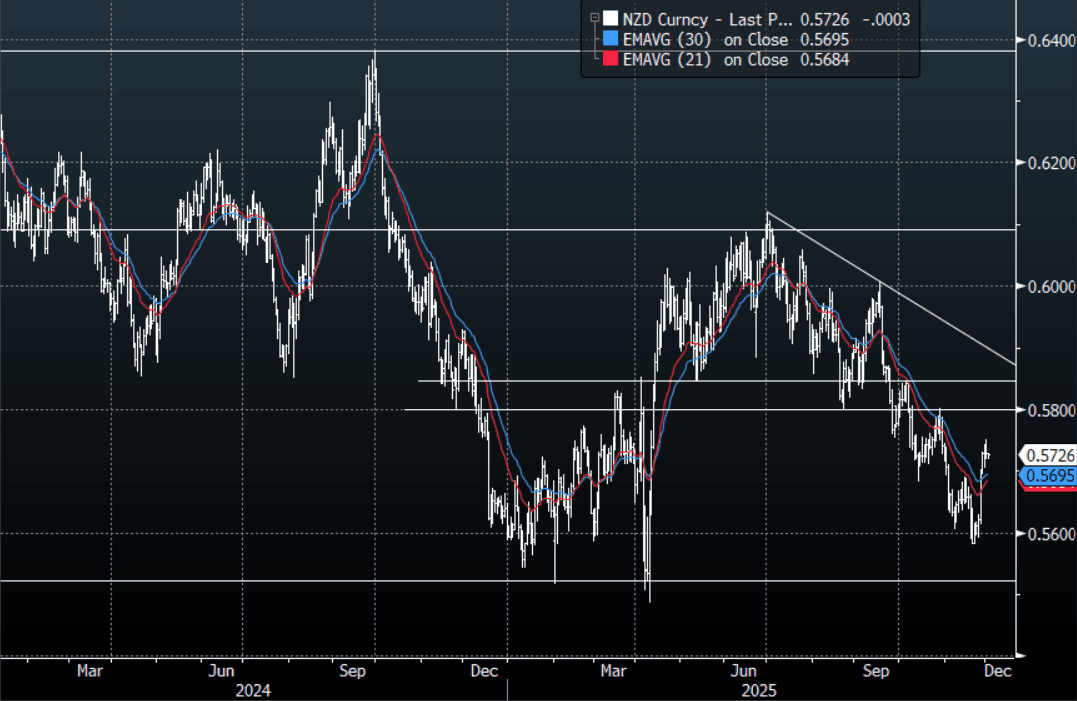

NZD/USD - Consolidates Gains Above 0.5700

The NZD/USD had a range today of 0.5719 - 0.5729 in the Asia-Pac session, going into the London open trading around 0.5725, -0.05%. The NZD/USD has had a subdued session again as risk attempts to stabilise after its fragile start to the week. Focus will be on the ability of the market to turn the poor start of the week around. On the day I still remain wary but the NZD remains well supported on dips, a sustained push back above 0.5760 should see the focus turn back toward the more important 0.5800-50 resistance. On the day support looks to be back toward the 0.5670-0.5690 area

- MNI AU - Dairy Weighs On ToT, Q3 Consumer Imports Rise: NZ’s terms of trade fell 2.1% q/q in Q3 driven by a 1.6% q/q drop in export prices as the dairy component was down 1.6% q/q. Import prices rose 0.5% q/q to be up 1.8% y/y. Q3 was the first quarterly fall in the terms of trade since Q3 2023 but it is still up 7.2% y/y after 12.2% y/y in Q2.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5700(NZD356m). Upcoming Close Strikes : 0.5575(NZD547m Dec 3), 0.5700(NZD332m Dec 5), 0.5730(NZD564m Dec 3) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 38 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: China's Focus on Crypto; Ueda's Signal to Markets

Markets were mixed across the region with Japan and Korea up modestly whilst China's major onshore bourses were all lower. In China authorities are focusing on crypto with the PBOC signaling that tougher enforcement are intended, spooking crypto markets which fell today. The BOJ"s Ueda continues to impact markets with further speculation of a December rate hike and key Japanese ministers making it clear that monetary policy is for the BOJ to decide. Japan's FANUC saw it's share rise over 6% on news it is partnering with Nvidia to include Nvidia's open-source robotic simulation in factory lines. The markets will look ahead to the US for signs of confirmation of a December rate hike, a move seen as stabilizing some markets in Asia. Korea saw the US announce a reduction in Auto tariffs and expectations for the approval of the 2026 budget plan, which will included changes on dividend income driving sentiment today.

- The NIKKEI is up +0.20% with FANUC the biggest gainer today, spurring gains for other robotic and heavy machinery stocks.

- The major onshore bourses in China are all down, with CSI 300 down -0.6% and Shenzhen down -0.7% whilst the Hang Seng bucked that trend to be modestly up +0.11%.

- The KOSPI was up also, by +1.85% today with the tariff reduction specifically fueling gains in carmakers like Hyundai Motor, which jumped over 4.5%, and Kia Corp, which rose just over 4%. Additionally major chip stocks including Samsung Electronics and SK Hynix, also performed strongly, which contributed to the overall market sentiment.

- India's NIFTY 50 continues to moderate from last weeks high, declining -0.38% Tuesday with Rupee weakness attributed to the decline as markets await the RBI decision.

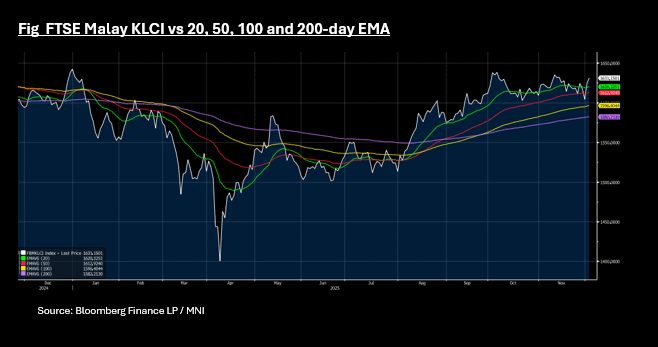

- Malaysia and Indonesia's major bourses are strong Tuesday, with the JCI up +0.65% and the FTSE Malay up +0.4%. Recent gains for the FTSE Malay KLCI has seen it trend above all major moving averages and at 1,630 sits above the nearest - the 20-day EMA of 1,620.

source: Bloomberg Finance LP/ MNI

OIL: Crude Holds Gains As Watching Geopolitical Developments

Crude has held onto Monday’s gains supported by geopolitical risks related to Ukraine/Russia and Venezuela. Benchmarks rose around 1.5% and are off their intraday lows to be slightly higher in Tuesday’s APAC session. WTI is up 0.2% to $59.42/bbl after falling to $59.33 off a high of $59.67. Brent is 0.1% higher at $63.21/bbl off the session low of $63.14. The US dollar is little changed.

- US special envoy Witkoff is in Russia to discuss changes to the original peace plan. Secretary of State Rubio met with Ukrainian officials in Florida on the weekend. President Zelenskyy has noted that an agreement on territory is going to be very difficult, as Ukraine is not prepared to cede unoccupied areas to Russia.

- Ukraine struck two Russian tankers and apparently also a wharf used to load Kazakh crude in the Black Sea, which has now stopped. It also continues to target Russian refineries. Diesel prices trended lower through the last 10 days of November but have stabilised this week.

- There are reports that there was a meeting at the White House on Venezuela later on Monday. President Trump has suggested closing Venezuelan airspace and may have offered safe passage for Venezuelan President Maduro and his family if they leave. Venezuela was the 17th largest exporter of oil in 2023 (IEA).

- Later the Fed’s Bowman testifies before the House Committee but given that the FOMC blackout has begun ahead of the 10 December decision, she is not expected to say anything on monetary policy or the economy. There is little data in the US with November Wards vehicle sales the only release.

- November euro area CPI and October unemployment rate are released and the ECB’s Buch speaks. The BoE publishes its Financial Stability Report. CFTC market positions data are scheduled to print.

PRECIOUS METALS: Silver Down As Indicators Suggest Overbought

There appears to have been some profit taking in silver on Tuesday after it rose 8.6% since last Thursday and started to look overbought. The metal is down 1.3% to $57.21/oz off the intraday low at $56.595 and back below resistance at $57.864. Gold continues to range trade with the US dollar, yields and Fed pricing little changed. Bullion is down 0.3% to $4219.0/oz off the intraday low of $4200.08.

- Silver reached a record high on Monday at $58.843. Bloomberg estimates that its 14-day RSI is above 70 signalling that it is overbought and also the gold/silver ratio is its lowest in over a year, which can signal a turning point. The metal has benefited from increased Fed rate cut expectations but market tightness has encouraged speculators.

- With little information out of the US on Tuesday, gold is likely to remain range bound. Of note on Wednesday are ADP November employment and November services ISM/PMI.

- Later the Fed’s Bowman testifies before the House Committee but given that the FOMC blackout has begun ahead of the 10 December decision, she is not expected to say anything on monetary policy or the economy. There is little data in the US with November Wards vehicle sales the only release.

- November euro area CPI and October unemployment rate are released and the ECB’s Buch speaks. The BoE publishes its Financial Stability Report. CFTC market positions data are scheduled to print.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 02/12/2025 | 0700/0700 | BOE Financial Stability Report | ||

| 02/12/2025 | 0745/0845 | Budget Balance | ||

| 02/12/2025 | 0900/1000 | Unemployment | ||

| 02/12/2025 | 1000/1100 | ** | EZ Unemployment | |

| 02/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 02/12/2025 | 1000/1000 | * | Index Linked Gilt Outright Auction Result | |

| 02/12/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 02/12/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 02/12/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 02/12/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 02/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 02/12/2025 | 1500/1000 | Fed Vice Chair Michelle Bowman | ||

| 03/12/2025 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 03/12/2025 | 2200/0900 | ** | S&P Global Final Australia Composite PMI | |

| 03/12/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 03/12/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 03/12/2025 | 0030/1130 | *** | Quarterly GDP | |

| 03/12/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 03/12/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 03/12/2025 | 0700/0200 | * | Turkey CPI | |

| 03/12/2025 | 0730/0830 | *** | CPI | |

| 03/12/2025 | 0815/0915 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0815/0915 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0845/0945 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0845/0945 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0850/0950 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0850/0950 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0855/0955 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0855/0955 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0900/1000 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0900/1000 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0930/0930 | ** | S&P Global Services PMI (Final) | |

| 03/12/2025 | 0930/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/12/2025 | 1000/1100 | ** | EZ PPI | |

| 03/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 03/12/2025 | 1030/1130 | ECB Lane Keynote at Banca d'Italia Workshop on Exchange Rates | ||

| 03/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index |