MNI EUROPEAN OPEN: China Stocks Down After Margin Trade Record

EXECUTIVE SUMMARY

- BESSENT EXPECTS SUPREME COURT TO UPHOLD LEGALITY OF TRUMP’S TARIFFS BUT EYES PLAN B - RTRS

- TRUMP WEIGHS DECLARING NATIONAL HOUSING EMERGENCY, BESSENT SAYS - BBG

- BOJ’S HIMINO SEES GRADUAL HIKES; UPSIDE, DOWNSIDE RISKS - MNI BRIEF

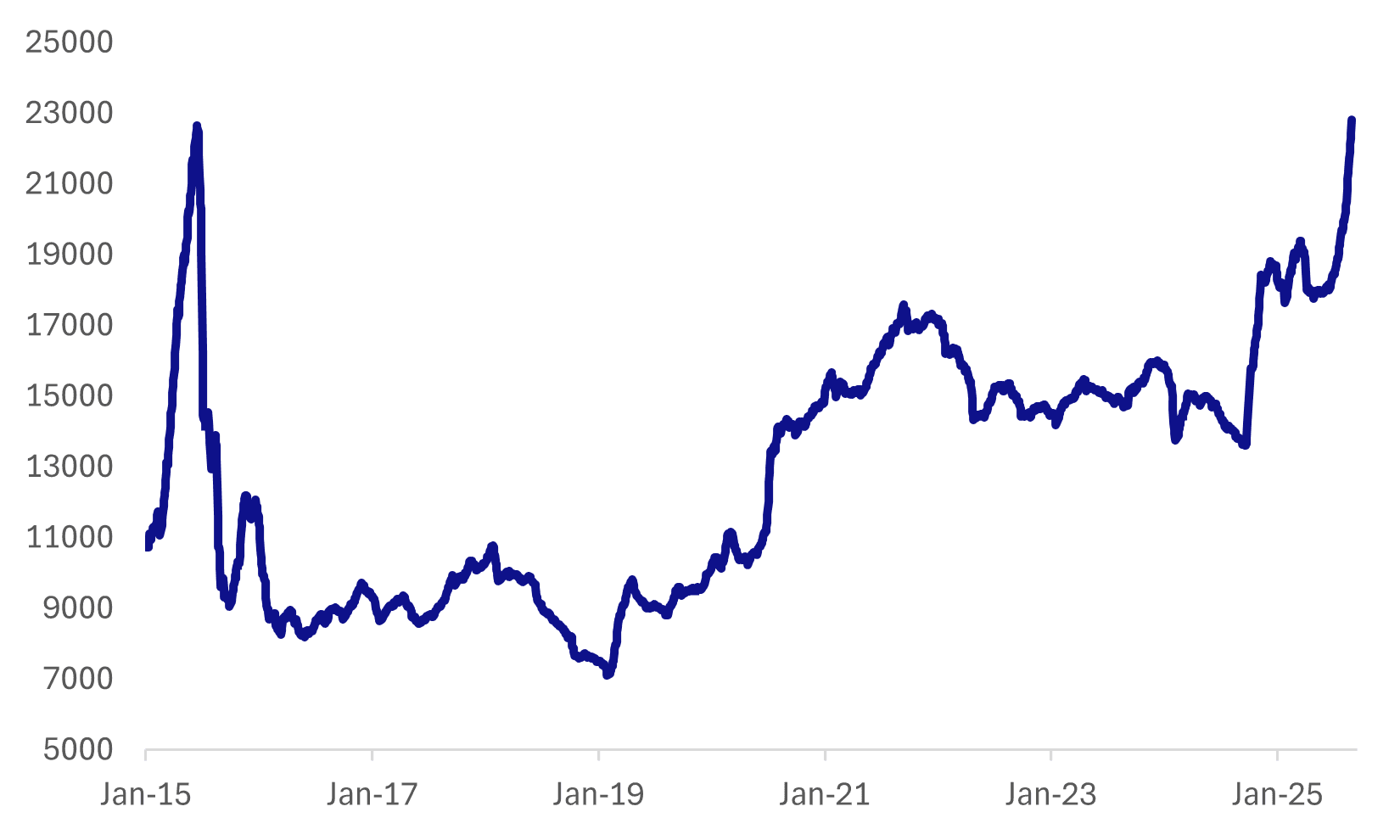

- CHINA’S MARGIN TRADES SURGE TO RECORD AS STOCK RALLY EXTENDS - BBG

- XI, PUTIN MEET IN BEIJING, HIGHLIGHT THEIR CLOSE TIES - BBG

Fig 1: China Margin Trading - Outstanding Balance of Margin Purchase and Debt Repayments

Source: Bloomberg Finance L.P./MNI

UK

POLICY (BBG): “UK Prime Minister Keir Starmer announced a raft of changes to his Downing Street team in a bid to reset his government and give him more influence over economic policy, after a stuttering first year in power saw his leadership called into question and Labour tank in the polls.”

POLITICS (ECONOMIST): “From Tuesday to Thursday the biggest-ever National Conservatism conference will take place in Washington, DC. Speakers include Tulsi Gabbard, America’s director of national intelligence, and Thomas Homan, Donald Trump’s “border czar”. One attendee stands out: Nigel Farage, leader of Britain’s hard-right Reform UK , the only British politician currently confirmed to speak.”

EU

EU (BBC): “The navigation system of a plane carrying Ursula von der Leyen was disrupted due to suspected Russian interference, the European Commission has said.”

UKRAINE (DW): “The leaders of Britain and France will co-chair on Thursday a summit for the so-called "Coalition of the Willing," to discuss security guarantees for Ukraine.”

UKRAINE/GERMANY (DW): “Jens Spahn, the leader of the conservative CDU/CSU in the Bundestag, and Matthias Miersch, the Bundestag leader of the center-left Social Democrats, met with President Volodymyr Zelenskyy and held talks in the Ukrainian capital. The two sought to discuss further German support and diplomatic efforts to end the Russian invasion.”

FRANCE (BBG): “French Prime Minister Francois Bayrou struck a combative tone in his effort to gain support for a Sept. 8 confidence vote, while acknowledging that talks with political parties may fail to save his government from being ousted.”

SPAIN (BBG): “Spanish Prime Minister Pedro Sanchez committed to complete his term even if his government’s allies in parliament reject his latest budget proposal.”

SPAIN (POLITICO): “Spain’s far right gains as leading parties fight over fires. Vox presents the deadly climate-linked wildfires as the result of a broken political system.”

RUSSIA (BBG): “ European Union countries are looking to ways to plug any remaining loopholes to ensure that Russian gas won’t be furtively mixed into the bloc’s supplies once a ban takes effect by the end of 2027.”

BELGIUM (POLITICO): “Belgium to recognize Palestine, sanction Israel. Foreign Minister Maxime Prévot said the move would happen only after Hamas releases all Israeli hostages and no longer manages Palestine.”

US

TARIFFS (RTRS): “U.S. Treasury Secretary Scott Bessent on Monday expressed confidence that the Supreme Court will uphold President Donald Trump's use of a 1977 emergency powers law to impose sweeping tariffs on most trading partners, but said the administration has a backup plan if it does not.”

HOUSING (BBG): “Treasury Secretary Scott Bessent said the Trump administration may declare a national housing emergency this fall as the White House looks to highlight key issues for midterm campaign voters.”

OTHER

JAPAN (MNI BRIEF): Bank of Japan Deputy Governor Ryozo Himino said Tuesday the Bank would raise its policy rate to adjust the degree of monetary accommodation if its baseline scenario for economic activity and prices materialises, though he gave no guidance on timing or pace.

JAPAN (MNI BRIEF): Japan’s economy in the April–June quarter is likely to have grown slightly faster than the initial estimate as public investment improved, though capital spending and private consumption were little changed, according to economists surveyed after a key government release.

INDIA/RUSSIA (BBC): “India's Prime Minister, Narendra Modi, says he has had an "insightful" exchange with Russian President Vladimir Putin on the sidelines of a summit in China. The two leaders spent 45 minutes inside the Russian leader's car - after which Modi posted a picture of their journey alongside the compliment to Putin.”

NEW ZEALAND (BBG): “The data inflow has improved at the margin over the past fortnight signaling better times ahead, but current economic activity is soft, the Treasury Dept. says in its Fortnightly Economic Update published Tuesday in Wellington.”

CHINA

MARGIN TRADING (BBG): “Chinese investors are borrowing a record amount of cash to buy local stocks, further fueling a liquidity-driven rally that shows few signs of stalling.”

GEOPOLITICS (RTRS): “Chinese President Xi Jinping will host his country's largest-ever military parade this week, as he seeks to recast Beijing as the custodian of a post-U.S. international order at a time of deep geopolitical uncertainty.”

CHINA/RUSSIA (BBG): "- Chinese leader Xi Jinping and Russian President Vladimir Putin met briefly in Beijing, providing a reminder of the close relationship the two have developed since Moscow’s invasion of Ukraine."

YUAN (YICAI): “The expected U.S. Federal Reserve rate cut in September and potential positive outcome in China-U.S. trade talks could drive further appreciation of the yuan this year, on top of capital inflows amid the A-share rally, Yicai.com reported citing analysts.”

LIQUIDITY (SHANGHAI SECURITIES NEWS): “Inter-bank market liquidity will likely remain stable in September amid fiscal spending and central bank support, despite a large amount of open market maturities, Shanghai Securities News reported citing analysts.”

MNI: PBOC Net Drains CNY150.1 Bln via OMO Tuesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY255.7 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY105.7 billion after offsetting maturities of CNY405.8 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4161% at 09:34 am local time from the close of 1.4454% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 50 on Monday, compared with the close of 47 on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.1089 Tues; -0.63% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1089 on Tuesday, compared with 7.1072 set on Monday. The fixing was estimated at 7.1335 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND Q2 TERMS OF TRADE +4.1% Q/Q; EST. +1.9%; Q1 +1.9%

NEW ZEALAND Q2 EXPORT VOLUMES -3.7% Q/Q; Q1 +4.0%

NEW ZEALAND Q2 IMPORT VOLUMES +4.2% Q/Q; Q1 -2.1%

AUSTRALIA PUBLIC SECTOR DEMAND CONTRIBUTION TO Q2 GDP FLAT; Q1 FLAT

AUSTRALIA Q2 NET EXPORTS +0.1PP TO GDP; EST. 0.1%; Q1 -0.2PP

AUSTRALIA Q2 CURRENT ACCOUNT DEFICIT A$13.7B; EST. -A$16.0B; Q1 –A$14.1B

JAPAN AUG. MONETARY BASE -4.1% Y/Y; JULY -3.9%

JAPAN END-AUG. MONETARY BASE OUTSTANDING Y645.6T; END-JUL Y646.3T

SOUTH KOREA AUG. CONSUMER PRICES -0.1% M/M; EST. +0.2%; JUL. +0.2%

SOUTH KOREA AUG. CONSUMER PRICES +1.7% Y/Y; EST. +1.9%; JUL. +2.1%

SOUTH KOREA AUG. CPI EX FOOD & ENERGY +1.3% Y/Y; EST. +1.7%; JUL. +2.0%

MARKETS

US TSYS: Yields Drift Higher After US Holiday

The TYZ5 range has been 112-09+ to 112-13 during the Asia-Pacific session. It last changed hands at 112-12, down 0-04 from the previous close.

- The US 2-year yield has edged higher trading around 3.63%, up 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.246%, up 0.02 from its close.

- 10-Year Yields continue to find supply toward the 4.20% area, which signals the range might continue to dominate. A break of the recent lows around 4.18% would bring the bottom of the range towards 4.10% back into focus.

- Bloomberg - “World’s Long-Dated Bonds Face a Traditionally Terrible Month. Longer-maturity bonds may be in for a treacherous September, if history is any guide, with government bonds globally with maturities of over 10 years posting a median loss of 2% in September. The trend may worsen due to sticky inflation in Japan, political turmoil in France, and speculation that President Donald Trump may push the Federal Reserve to cut interest rates.”

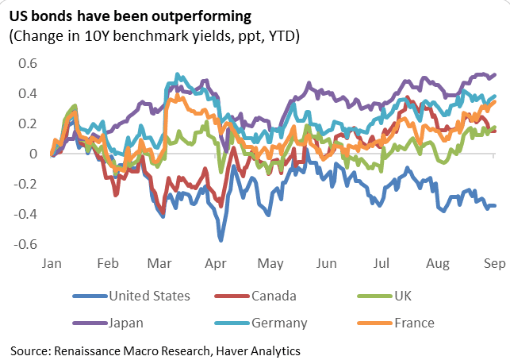

- RenMac on X: “Notable that US 10Y yields are still down year-to-date despite rising rates across G-10, concerns about US fiscal deficits, and the rising risk premium associated with Trump's alleged threatening of the Fed’s policy independence.” See Fig.1 Below.

- Data/Events: S&P Manf. PMI, ISM Manf., Construction Spending

Fig 1: US Bonds Outperforming

Source: MNI - Market News/@RenMacLLC

JGBS: Futures Bounce Post 10yr Auction, But Limited Follow Through

JGB futures have risen in the aftermath of the strong 10yr JGB auction result. We were last 137.48, +.18 versus settlement levels. Post lunchtime break highs were at 137.62, which was just short of earlier Sep highs (137.66), so recent ranges are still holding. The Sep contract opened at 137.32. JGBs are outperforming US Tsy futures, which remain weaker, but are up from session lows.

- The 10yr auction saw a bid to cover ratio of 3.92, versus 3.06 at the prior auction (note the 12-month moving average of the bid to cover ratio is 3.17, per BBG). The tail of the auction was 0.06, versus the 0.14 from the prior outcome.

- Market sentiment was somewhat bearish heading into the auction result, given last week's poor 2yr auction outcome and a slightly heavier US Tsy futures backdrop.

- Still, it may not be a turning point for futures. Earlier headlines crossed: "JAPAN PM ISHIBA MAKING ARRANGEMENT TO INSTRUCT MINISTERS AS EARLY AS THIS WEEK TO COMPILE ECONOMIC MEASURES TO ADDRESS INFLATION, TRUMP TARIFFS, SANKEI NEWSPAPER SAYS - [RTRS]"

- Hence pressure is likely to remain on the government to provide fiscal support.

- Earlier we heard from BoJ Deputy Governor Himino, who struck a balanced tone. He said Tuesday the Bank would raise its policy rate to adjust the degree of monetary accommodation if its baseline scenario for economic activity and prices materialises, though he gave no guidance on timing or pace.

- In the cash JGB yield space, the belly part of the curve is weaker in yield terms, with the 7 and 10yr yield tenors off over 2bps. This puts the 10yr back close to 1.60%. 20-40yr yield tenors are still holding higher in yield terms. The 2/30s JGB curve is 2bps steeper to +234bps.

AUSSIE BONDS: Futures Weaker, But Up From Session Lows, Q2 GDP Tomorrow

Aussie bond futures hold weaker, but are away from session lows. 3yr futures (YM) were last 96.545, off 2bps. Earlier lows were at 96.53, which was just under late August lows. 10yr futures (XM) were last around 95.62, off 3.5pbs. Session lows were at 95.61. The negative bias to US Tsys futures has likely spilled over into Aussie futures to some degree. Sentiment has been helped somewhat in the aftermath of the JGB 10yr auction, which saw solid demand.

- In the ACGB yield space, the bias if for a steeper curve, with yield gains of 2-5bps, led by the back end. The 3yr benchmark was last around 3.44% (+2bps), while the 10yr was close to 4.35% (up 3bps). This benchmark is now back to late July levels.

- On the data front, Q2 net exports contributed 0.1pp to GDP, as expected, while public demand was neutral. Q2 GDP prints on Wednesday and Bloomberg consensus is forecasting a 0.5% q/q increase bringing annual growth to 1.6% from Q1’s 1.3%, in line with the RBA’s August projection. However, almost all estimates were provided before this week’s inventory, net export and public demand data. Inventories were close to consensus and net exports were in line.

- Q2 data show only a 0.1pp contribution to growth from net exports and nothing from public demand as government consumption’s 0.2pp was offset by the 0.2pp drop in public investment. The 0.1% q/q rise in inventories is likely to mean it had a neutral effect on growth.

BONDS: NZGBS: 2/10s Curve To Steepest Level Since April

NZGB yields have seen a steeper bias through Tuesday trade. 10 to 30yr yield tenors are up a little over 4bps, while the 2yr is up less than 1bps. This leaves the 2/10s curve close to +143bps, which is highs back to April of this year. This looks to the playing some catch up with US moves, with the 2/10s Tsy curve just off late August highs.

- The outright 2yr yield remains sub 3.00%, while the 10yr yield is around 4.40%. The 2yr swap rate has risen around 2bps to be near 2.76% in latest dealings.

- US Tsy yields have re-opened, with yields pushing higher across the curve, albeit with gains in the 1-1.5bps region at this stage.

- In terms of data, NZ saw the largest improvement in the merchandise terms of trade in Q2 since Q1 2024. It rose 4.1% q/q, the sixth consecutive quarterly increase, to be up 12.2% y/y after 10.3% y/y in Q1. While domestic demand remains soft, this rise in the terms of trade will be providing some welcome support to growth.

- Via BBG: " The data inflow has improved at the margin over the past fortnight signaling better times ahead, but current economic activity is soft, the Treasury Dept. says in its Fortnightly Economic Update published Tuesday in Wellington."

- Tomorrow, the data calendar sees ANZ commodity prices for August.

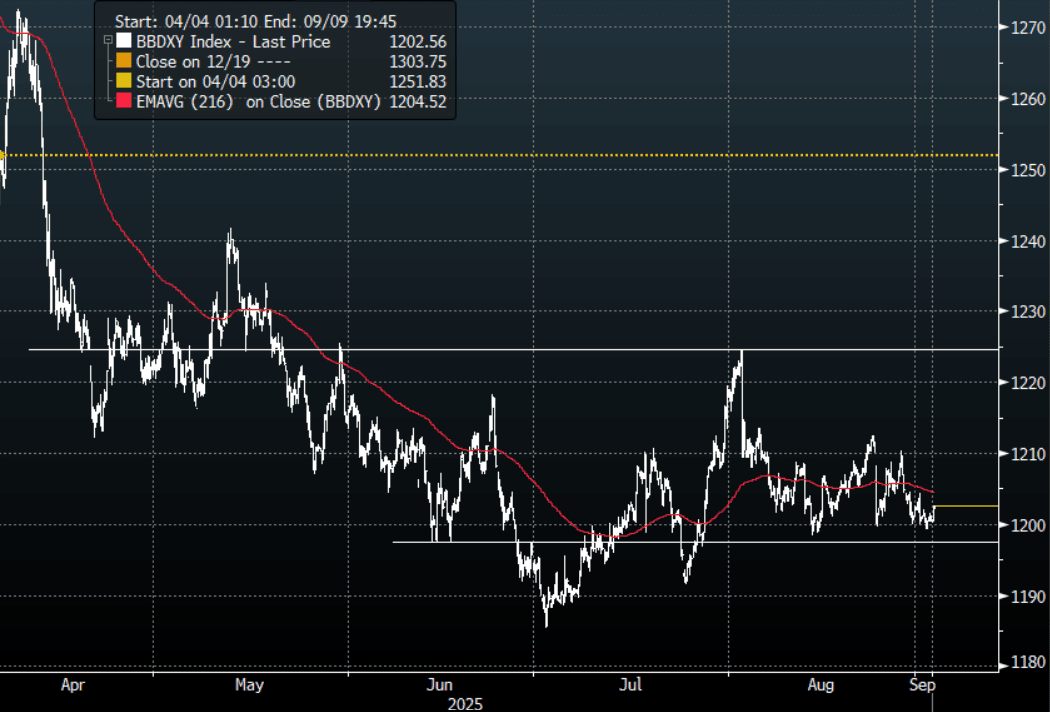

FOREX: Asia FX Wrap - USD Finds Some Demand Just Above Support

The BBDXY has had a range of 1200.18 - 1202.53 in the Asia-Pac session, it is currently trading around 1202, +0.15%. The USD continues to find demand just above its pivotal support. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows. The USD is holding just above this support but continues to trade with a heavy tone, not sure we get a clear break though until the market sees what the NFP print is, in order to allocate more risk.

- EUR/USD - Asian range 1.1692 - 1.1718, Asia is currently trading 1.1695. The pair is trading sideways for the moment. First support is back towards 1.1550, a break back above 1.1850 needed to regain upward momentum.

- GBP/USD - Asian range 1.3523 - 1.3549, Asia is currently dealing around 1.3525. The pair is consolidating just above the 1.3500 area. Back in the middle of its recent 1.3350-1.3650 range, the USD’s fate will have a direct impact on which side is tested.

- USD/CNH - Asian range 7.1323-7.1437, the USD/CNY fix printed 7.1089, Asia is currently dealing around 7.1420. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.10%, Gold $3495, US 10-Year 4.245%, BBDXY 1202, Crude Oil $64.92

- Data/Events : Italy PPI, EZ CPI, France Budget Balance, Spain Unemployment

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

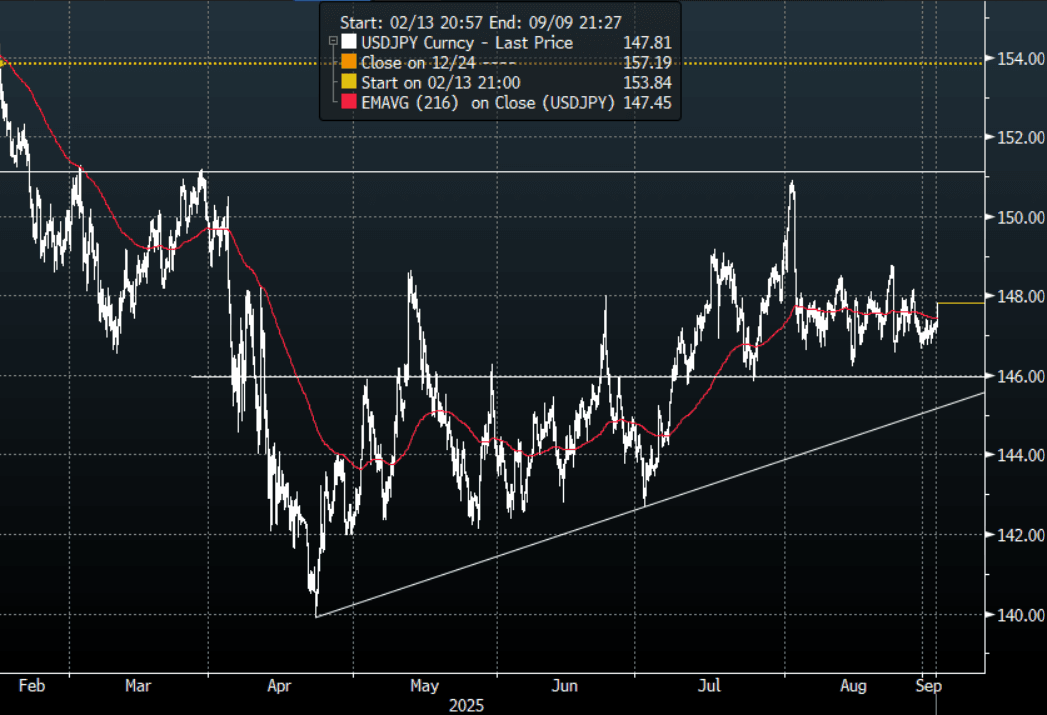

JPY: Asia Wrap - USD/JPY Demand Sees It Bounce Off 147.00 Again

The Asia-Pac USD/JPY range has been 147.05-147.82, Asia is currently trading around 147.80, +0.40%. USD/JPY saw some decent buying into the Japanese Fix, this demand then continued into the afternoon session helping the pair bounce back off its support. The demand towards 146.00 has been pretty solid all of July and August, keeping us for the most part in a 146.00-149.00 range.

- MNI: BOJ's Himino Sees Gradual Hikes; Upside, Downside Risks. Bank of Japan Deputy Governor Ryozo Himino said Tuesday the Bank would raise its policy rate to adjust the degree of monetary accommodation if its baseline scenario for economic activity and prices materialises, though he gave no guidance on timing or pace.

- "BOJ DEPUTY GOV HIMINO: THERE IS BOTH CHANCE TRADE POLICY IMPACT COULD BE SMALLER OR BIGGER THAN EXPECTED, MUST FOCUS ON POSSIBILITY IT COULD BE BIGGER THAN EXPECTED - [RTRS]"

- On the balance sheet: "BOJ DEPUTY GOV HIMINO: BOJ'S PLAN TO REDUCE JGB BUYING SHOULD BE BASED ON PRINCIPLE THAT LONG-TERM RATES ARE TO BE FORMED IN MARKETS, BOJ SHOULD PROVIDE PREDICTABILITY WHILE ALLOWING ENOUGH FLEXIBILITY TO SUPPORT MARKET STABILITY" RTRS

- “JGB Futures Jumping With Relief After Solid 10-year Auction. JGBs are enjoying a leap higher after the bid-to-cover ratio printed at 3.92 for today’s auction, the best since 2023; there’s also a tighter tail than the previous sale. The list of buyers was led by MUFJ-MS, which typically signals long-term buyers participated.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 148.30($334m).Upcoming Close Strikes : 146.50($1.39b Sept 3), 146.00($2.16b Sept 5) - BBG.

- CFTC data for last week shows leveraged accounts have maintained their recent JPY shorts and will be hoping this support continues to be solid. A sustained break below 145.50/146.00 is needed to to turn the focus back to the year's lows towards 140.00.

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

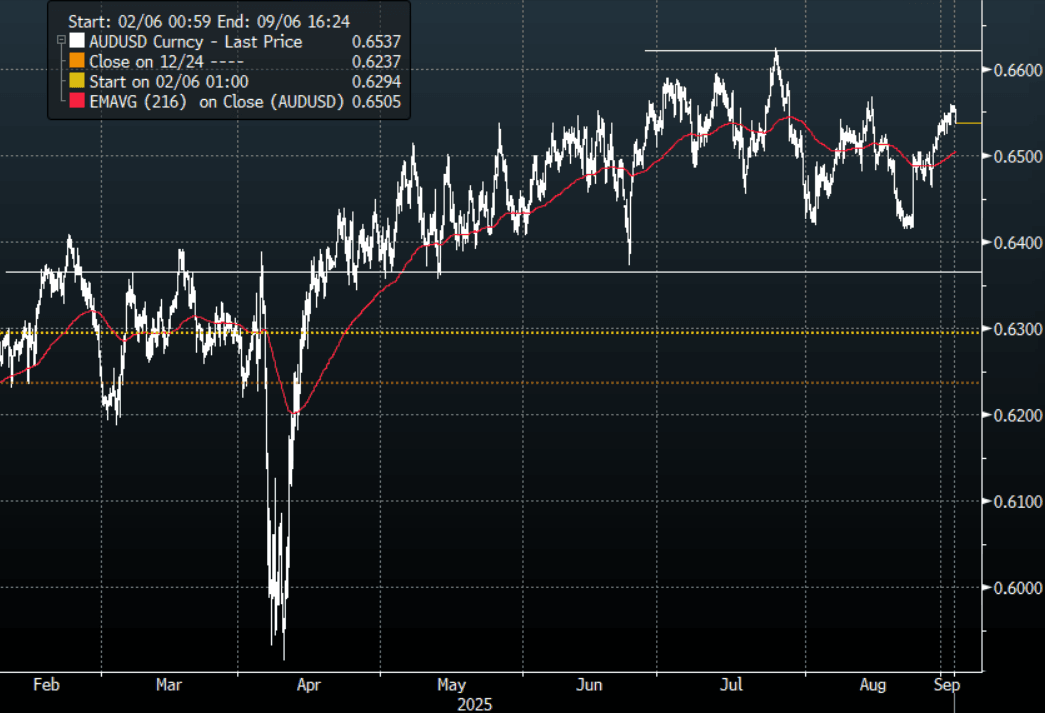

AUD: Asia Wrap - AUD/USD Drifts Lower, Within Range

The AUD/USD has had a range of 0.6537 - 0.6559 in the Asia- Pac session, it is currently trading around 0.6540, -0.20%. The AUD has drifted lower for most of our day. The AUD finds itself firmly back in the middle of its recent multi-month range of 0.6350-0.6650 with little clear long-term direction. The market will be looking towards NFP at the end of the week to hopefully be a catalyst.

- Current Account Deficits Continue, Net Exports Added 0.1pp. While Q2 recorded its ninth consecutive quarterly current account deficit, it narrowed from Q1 driven by the primary income deficit. Q2 printed at -$13.7bn after $14.1bn with primary income at -$16.8bn down from Q1’s -$18bn but the goods and services surplus was down $1.2bn at $3.1bn, the lowest in 7 years. Net exports contributed 0.1pp to Q2 growth, as expected.

- MNI: RBA November Cut Eyed, Lower Productivity To Pull Down R*. The Reserve Bank of Australia is likely to hold at its September meeting before delivering another 25-basis-point cut to the 3.6% cash rate in November, former staffers and leading economists told MNI, with the Bank’s downgraded productivity outlook expected to weigh on neutral rate estimates over the longer term.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6400(AUD770m). Upcoming Close Strikes : 0.6400(AUD1.12b Sept 5), 0.6500(AUD974m Sept 5), 0.6600(AUD1b Sept 5) - BBG

- CFTC Data last week shows Asset managers continue to add to their shorts -78758(Last -72904), the Leveraged community though again reduced their own shorts -6447(Last -7818).

- AUD/JPY - Asia-Pac range 96.37 - 96.65, Asia is trading around 96.60. The pair is probing above the 96.50 area this morning. A sustained move back above 96.50 would turn the trend higher again but until then sellers should be around looking for this move to top out.

Fig 1: AUD/USD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

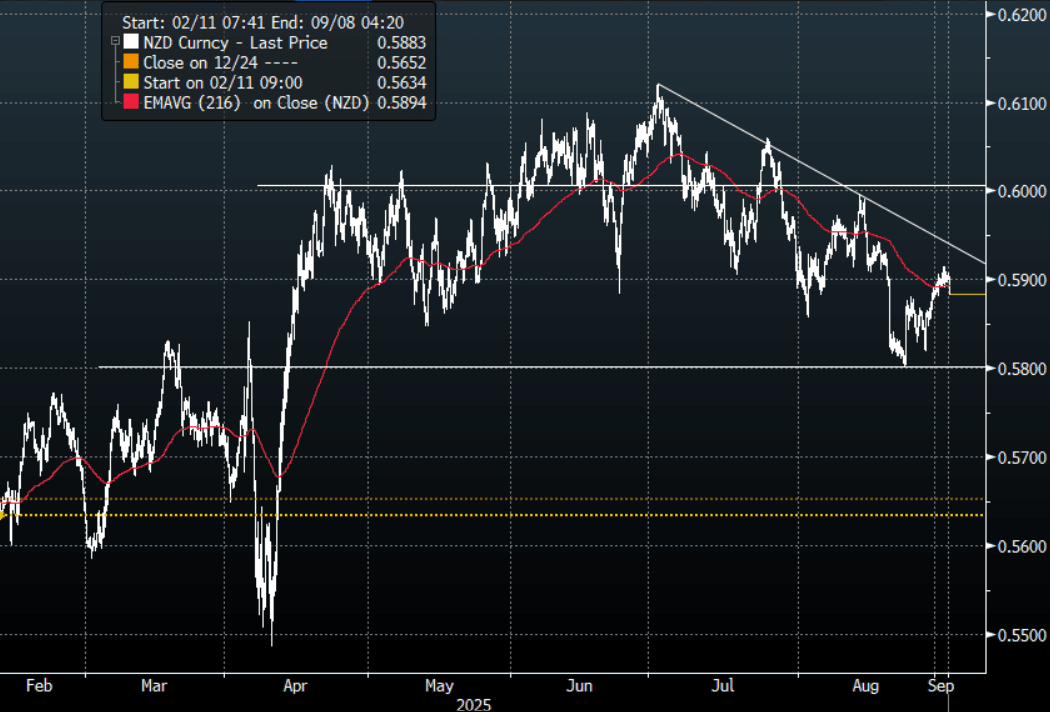

NZD: Asia Wrap - NZD/USD Sellers Return Above 0.5900

The NZD/USD had a range of 0.5883 - 0.5908 in the Asia-Pac session, going into the London open trading around 0.5885, -0.30%. The NZD has topped out above 0.5900 for now as the USD finally sees some demand return. The NZD has bounced off its support toward 0.5800, sellers should continue to be around looking to fade the move back towards the 0.5950/0.6000 area initially. Should the USD break lower and gain momentum this would complicate this trade and then it would be prudent to rotate the NZD shorts into the crosses.

- Goods Terms Of Trade Continues Moving Higher: NZ saw the largest improvement in the merchandise terms of trade in Q2 since Q1 2024. It rose 4.1% q/q, the sixth consecutive quarterly increase, to be up 12.2% y/y after 10.3% y/y in Q1. While domestic demand remains soft, this rise in the terms of trade will be providing some welcome support to growth. The services terms of trade fell 0.4% q/q but rose 1.0% y/y after falling 7.3% y/y.

- "New Zealand Treasury Says Domestic Economic Conditions Are Soft. The data inflow has improved at the margin over the past fortnight signaling better times ahead, but current economic activity is soft, the Treasury Dept. says in its Fortnightly Economic Update published Tuesday in Wellington." - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5700(NZD500m). Upcoming Close Strikes : 0.5700(NZD384m Sept 3) - BBG

- CFTC Data of last week shows Asset Managers added slightly to their new short position in the NZD -4743(Last -3198), the Leveraged community have almost completely exited their short -225(Last -4004).

- AUD/NZD range for the session has been 1.1095 - 1.1112, currently trading 1.1110. Momentum higher looks to have stalled above 1.1100 for now, look for demand to return on a dip back towards the 1.1000 area.

Fig 1: NZD/USD Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: China's Bourses Falls as Regional Markets Strong

In what seems like a rarity of late, the major bourses across China all trended lower today following yesterday's strong gains. This comes as data shows Chinese investors are borrowing a record amount of cash to buy local stocks, further fueling a liquidity-driven rally that shows few signs of stalling. The outstanding amount of margin trades in China’s onshore equities market climbed to 2.28 trillion yuan ($320 billion) Monday, surpassing the previous record of 2.27 trillion yuan in 2015. An interesting perspective to note though is despite the latest expansion of margin trades, the size of China’s stock market also has nearly doubled in the past decade. The amount of leveraged purchases as a proportion of total market capitalization was 2.2% as of Monday, slightly above the 10-year average but far below 2015’s peak of 4.6%. (via BBG)

- The Hang Seng is down -0.61% today, having finished yesterday up +2.15%. The CSI 300 has lost ground by -0.91% after closing at new highs yesterday. The Shanghai Comp is down -0.70% and Shenzhen down heavily by -2.3%.

- The NIKKEI has posted modest gains of +0.27%

- The TAIEX in Taiwan is flat today after finishing Monday lower.

- Following the weaker than expected CPI, the KOSPI is up +0.89% as investors begin to extrapolate a rate cut. This following falls of -1.35% yesterday.

- The Jakarta Composite bounced back today as the Finance Minister re-assured markets and is up +1.05%.

- The FTSE Malay KLCI is lower by -0.20% despite better than expected PMIs.

- The NIFTY 50 has had two days of gains; up +0.45% Tuesday morning following +0.81% gains yesterday.

OIL: Crude Continues Higher As Upcoming OPEC Meeting & US Payrolls In Focus

Oil prices have continued the rally started on Monday. WTI is up 1.4% to $64.90/bbl after reaching $65.10. Brent is 0.4% higher at $68.42/bbl after a peak of $68.58, remaining below resistance at $69.06. The prospect of a near-term easing in sanctions on Russia has faded with the US and EU now looking at extending them after attacks on Ukrainian cities have intensified. The USD index is up 0.1%.

- With the oil market expected to post a substantial surplus in 2026, supply developments are being watched closely.

- OPEC meets on September 7 to decide its October production target. There are still 1.65mbd of previous voluntary output cuts that could be unwound but analysts believe the group will hold production stable.

- Demand also remains in focus with concerns regarding the impact from increased US tariffs but the prospect of Fed easing is calming concerns. Friday’s August US payroll data will be key.

- Later the ECB’s Elderson and Machado appear. US August manufacturing PMI/ISM, July construction, euro area August CPI and July French budget data print.

Gold Back Below $3500 After Reaches New Record High

Gold prices spiked to a new record high of $3508.73/oz earlier in today’s APAC session on increased expectations of a September Fed easing. It is also benefiting from concerns regarding Fed independence. It rose above the bull trigger at $3500.1, 22 April record, but has been unable to hold the break. Bullion is now up 0.6% to $3497.0 despite a stronger US dollar (BBDXY +0.2%) and slightly higher yields.

- UBS believes that gold will continue trending higher driven by softening growth, rate cuts and geopolitical/economic uncertainty, according to Bloomberg.

- After rising 2.5% on Monday, silver is up another 0.3% to $40.82 today, holding just above initial resistance at $40.798. It reached a high of $40.850 after a low of $40.558. Bloomberg reported that in August ETF buying of silver rose for the 7th straight month.

- Silver has also been added to the US list of critical minerals. It is a key component of solar panels. The Silver Institute is expecting 2025 to be the fifth year the metal is in deficit, Bloomberg reported.

- Equities are mixed with the S&P e-mini slightly lower, Hang Seng down 0.6% but KOSPI up 0.8%. Oil prices are stronger again with WTI +1.4% to $64.92/bbl. Copper is little changed.

- Later the ECB’s Elderson and Machado appear. US August manufacturing PMI/ISM, July construction, euro area August CPI and July French budget data print.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 02/09/2025 | 0900/1100 | ** | PPI | |

| 02/09/2025 | 0900/1100 | *** | EZ HICP Flash | |

| 02/09/2025 | 1130/1330 | ECB Elderson and Machado Panel at ECB Legal Conference | ||

| 02/09/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 02/09/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 02/09/2025 | 1400/1000 | * | Construction Spending | |

| 02/09/2025 | 1400/1000 | * | Construction Spending | |

| 02/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 02/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/09/2025 | 1700/1300 | ** | US Treasury Auction Result for 52 Week Bill | |

| 03/09/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 03/09/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 03/09/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 03/09/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 03/09/2025 | 0130/1130 | *** | Quarterly GDP | |

| 03/09/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 03/09/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 03/09/2025 | 0700/0300 | * | Turkey CPI | |

| 03/09/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0730/0930 | ECB Lagarde Speaks at ESRB Conference | ||

| 03/09/2025 | 0730/0830 | BOE Mann at Signum's London Westminster Day roundtable | ||

| 03/09/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0815/0915 | BOE Breeden at Innovation in Money and Payments Conference | ||

| 03/09/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 03/09/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/09/2025 | 0900/1100 | ** | EZ PPI | |

| 03/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 03/09/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 03/09/2025 | 1300/0900 | St. Louis Fed's Alberto Musalem | ||

| 03/09/2025 | 1315/1415 | BOE testify at TSC: Bailey, Greene, Lombardelli, Taylor |