MNI EUROPEAN OPEN: China Data Disappoints, Limited Mkt Impact

EXECUTIVE SUMMARY

- TRUMPS SAYS PUTIN READY TO MAKE DEAL ON UKRAINE, US HOPES TO INCLUDE ZELENSKIY - RTRS

- JAPAN Q2 GDP RISES 0.3%Q/Q; ANNUALIZED +1.0% - MNI BRIEF

- LOCAL CHINA ECONOMISTS SHARE VIEWS ON H2 RETAIL SALES - MNI

- POLICY ADVISORS SHARE THEIR CHIAN PROPERTY OUTLOOK - MNI

- CHINA’S JULY GROWTH DRIVERS SLOW MORE THAN EXPECTED - MNI BRIEF

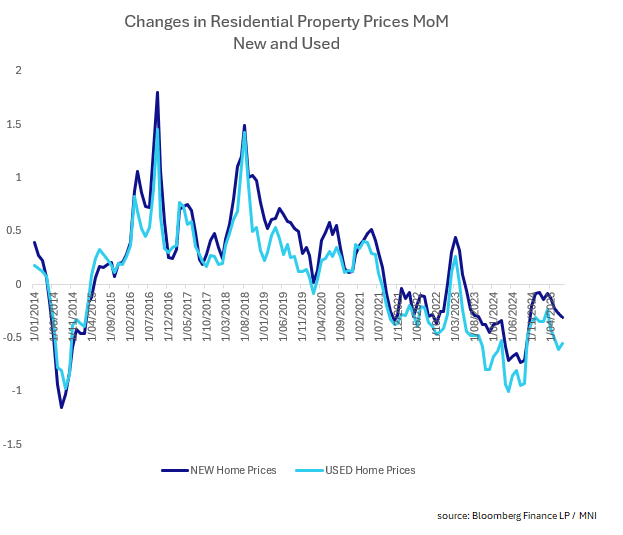

Fig 1: China Home Prices - M/M

UK

JOBS (BBG): " London is bearing the brunt of the UK’s jobs slowdown as a combination of tax rises, elevated wage costs and weak consumer spending force the city’s business to cut payrolls faster than in the rest of the country."

EU

GEOPOLITICS (RTRS): “U.S. President Donald Trump said he believes his Russian counterpart Vladimir Putin is ready to end his war in Ukraine, speaking on the eve of Friday's summit between the men, but that peace would likely require at least a second meeting involving Ukraine's leader.”

UKRAINE (BBG): “Ukrainian drones attacked Lukoil PJSC’s major refinery in Volgograd in the early hours of Thursday as Kyiv has ramped up strikes on Russian energy infrastructure this month.”

US

FED (BBG): “US Treasury Secretary Scott Bessent said he isn’t calling for a series of interest-rate cuts from the Federal Reserve, just pointing out that models suggest a “neutral” rate would be about 1.5 percentage points lower.”

CORPORATE (BBG): “The Trump administration is in talks with Intel Corp. to have the US government take a stake in the beleaguered chipmaker, according to people familiar with the plan, in the latest sign of the White House’s willingness to blur the lines between state and industry.”

OTHER

JAPAN (MNI BRIEF): Japan’s economy grew 0.3% q/q, or an annualised 1.0%, over Q2, supported by strong capital investment, solid private consumption and a positive contribution from net exports, preliminary Cabinet Office data showed Friday.

JAPAN (BBG): “ Japan’s chief trade negotiator Ryosei Akazawa said US Treasury Secretary Scott Bessent isn’t directly asking Japan to hike interest rates, a day after Bessent moved markets by describing the Bank of Japan as being behind the curve in fighting inflation.”

NEW ZEALAND (RTRS): "New Zealand citizens leaving the country have hit the highest levels in 13 years, with more than a third of those emigrating aged under 30 years as unemployment rises and economic growth remains soft."

CHINA

RETAIL SALES (MNI): Local China economists share their H2 retail sales outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

PROPERTY (MNI): Policy advisors share their China property outlook.

CONSUMPTION (MNI BRIEF): China’s domestic consumption confidence needs to be improved and enhanced, after July’s economic data showed total retail sales increased 3.7% year-on-year, lower than the 5.0% rise during H1, Fu Linghui, spokesperson for the National Bureau of Statistics, told reporters on Friday.

GROWTH (MNI BRIEF): China’s consumption and production slowed to their weakest pace this year in July, while investment growth hit a near five-year low, National Bureau of Statistics data showed Friday. Retail sales rose 3.7% y/y, down from June’s 4.8% and missing the 4.6% forecast. Industrial output grew 5.7% y/y, the lowest reading this year, compared with June’s 6.8% and below the 6.0% forecast.

PBOC (ECONOMIC INFORMATION DAILY): “The People’s Bank of China is likely to sustain ample liquidity via medium-term lending facilities and outright reverse repos during the peak period of government bond issuance, Economic Information Daily reported, citing Wang Qing, analyst at Golden Credit Rating.”

PRICES (ECONOMIC DAILY): “China’s recent crackdown on excessive competition will not trigger a broad price rise, as prices remain dependent on a recovery in domestic demand, Economic Daily said in a commentary.”

MNI: PBOC Net Injects CNY116 Bln via OMO Friday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY238 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY116 billion after offsetting maturities of CNY122 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4200% at 09:30 am local time from the close of 1.4424% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 52 on Thursday, compared with the close of 48 on Wednesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.1371 Fri; -0.55% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1371 on Friday, compared with 7.1337 set on Thursday. The fixing was estimated at 7.1862 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND JULY BUSINESSNZ MANUFACTURING PMI 52.8; PRIOR 49.2

NEW ZEALAND JULY FOOD PRICES M/M 0.7%; PRIOR 1.2%

NEW ZEALAND JUNE NET MIGRATION 1670; PRIOR 1370

JAPAN Q2 GDP Q/Q 0.3%; MEDIAN 0.1%; PRIOR 0.1%

JAPAN Q2 GDP ANNUALIZED Q/Q 1.%; MEDIAN 0.4%; PRIOR 0.6%

JAPAN Q2 GDP NOMINAL Q/Q 1.3%; MEDIAN 1.4%; PRIOR 1.0%

JAPAN Q2 GDP DEFLATOR Y/Y 3.0%; MEDIAN 3.2%; PRIOR 3.3%

JAPAN Q2 GDP PRIVATE CONSUMPTION Q/Q 0.2%; MEDIAN 0.1%; PRIOR 0.2%

JAPAN Q2 GDP BUSINESS SPENDING Q/Q 1.3%; MEDIAN 0.7%; PRIOR 1.0%

JAPAN Q2 GDP NET EXPORTS CONTRIBUTION % GDP 0.3%; MEDIAN 0.1%; PRIOR -0.8%

JAPAN Q2 GDP INVENTORY CONTRIBUTION % GDP -0.3%; MEDIAN -0.3%; PRIOR 0.6%

JAPAN JUNE F INDUSTRIAL PRODUCTION Y/Y 4.4%; PRIOR 4.0%

JAPAN JUNE CAPACITY UTILIZATION M/M -1.8%; PRIOR 2.0%

CHINA JULY NEW HOME PRICES M/M -0.31%; PRIOR -0.27%

CHINA JULY USED HOME PRICES M/M -0.55%; PRIOR -0.61%

CHINA JULY RETAIL SALES Y/Y 3.7%; MEDIAN 4.6%; PRIOR 4.8%

CHINA JULY INDUSTRIAL PRODUCTION Y/Y 5.7%; MEDIAN 6.0%; PRIOR 6.8%

CHINA JULY FIXED ASSET INVESTMENT YTD Y/Y 1.6%; MEDIAN 2.7%; PRIOR 2.8%

CHINA JULY PROPERTY INVESTMENT YTD Y/Y -12.0%; MEDIAN -11.4%; PRIOR -11.2%

CHINA JULY SURVEYED JOBLESS RATE 5.2%; MEDIAN 5.1%; PRIOR 5.0%

MARKETS

US TSYS: Slightly Richer After Yesterday’s Post-PPI Sell-Off

TYU5 is dealing at 111-29, +0-03+ from closing levels in today's Asia-Pac session.

- July CPI and PPI data pulled market pricing in opposite directions this week. Softer CPI figures initially allowed markets to more than fully price in a 25bp Fed cut in September. However, that view was swiftly unwound after yesterday’s hotter-than-expected PPI report (headline +0.9% M/M vs. +0.2% expected), challenging the post-CPI narrative that tariff effects were proving less severe than feared.

- Bloomberg – “Garfield Reynolds, MLIV Team Leader, said "Treasuries will remain nervous heading into next week’s Jackson Hole event" with inflation concerns likely to see long-dated debt underperform.”

- Cash US tsys are ~1bp richer in today's Asia-Pac session after yesterday's post-PPI sell-off.

- The 4.35% area in 10-Year yields should still see demand initially, but the way the market keeps bouncing off levels just below 4.20% will be disconcerting for longs.

- Data/Events: Retail Sales, Empire Manu., Industrial Production, Business Inventories, U. of Mich. Sentiment, TIC Flows

JGBS: Cheaper After Better Than Expected

JGB futures are weaker and at session lows, -15 compared to settlement levels.

- Japan's Q2 GDP was better than market expectations. Q/Q growth rose 0.3%, against a 0.1% forecast, while the Q1 outcome was revised up a touch to 0.1% from the original flat estimate. In terms of the detail, private consumption rose 0.2% q/q, versus 0.1% forecast, while Q1 was revised up to 0.2% (originally reported as 0.1%). Capex was up 1.3%, versus 0.7% expected (Q1 was revised down 0.1% to a 1.0% gain). Net exports contributed 0.3% to growth (0.1% was forecast), while inventories took 0.3% off growth, in line with forecasts. Nominal GDP rose 1.3%q/q, a touch below market forecasts of 1.4%.

- "JAPAN FINMIN KATO: MUST CLOSELY WATCH ECONOMIC, PRICE BACKDROP BEHIND RECENT COMMENTS BY BUSINESS SECTOR CALLING ON BOJ TO RAISE RATES, THOUGH SPECIFIC MONETARY POLICY DECISION UP TO BOJ - [RTRS]"

- Cash JGBs are 1-3bps cheaper across benchmarks. The benchmark 10-year yield is 2.7bps higher at 1.573% versus the cycle high of 1.616%.

- Swap rates are ~1bp higher, with swap spreads tighter.

- On Monday, the local calendar will see the Tertiary Industry Index.

AUSSIE BONDS: Slightly Weaker, Light Local Calendar Next Week

ACGBs (YM -1.0 & XM -2.0) are weaker but near session bests.

- Cash US tsys are ~1bp richer in today's Asia-Pac session after yesterday's post-PPI sell-off.

- US Data/Events: Retail Sales, Empire Manu., Industrial Production, Business Inventories, U. of Mich. Sentiment, TIC Flows.

- China's July industrial production expanded +5.7%, missing estimates of +6.0% and below June's result of +6.8%. This was the weakest monthly result since November 2024.

- China's retail sales for July missed forecasts and was weaker than the month prior. July retail sales expanded +3.7%, the slowest since November 2024 and a second consecutive month of moderation.

- Cash ACGBs are 1-2bps cheaper with the AU-US 10-year yield differential at -4bps.

- The bills strip is flat to -1 across contracts, with a steepening bias.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in September is given a 28% probability, with a cumulative 37bps of easing priced by year-end (based on an effective cash rate of 3.59%).

- The local calendar will be empty on Monday, ahead of Westpac Consumer Conf on Tuesday.

- Next week, the AOFM plans to sell A$1500mn of the 1.25% 21 May 2032 bond on Wednesday and A$300mn of the 4.75% 21 June 2054 bond on Friday.

BONDS: Closed Cheaper, Tracking Global Bonds

NZGBs closed 2-3bps cheaper, with the NZ-US and NZ-AU 10-year yield differentials little changed.

- (Bloomberg) - Food, electricity and gas prices increased in May from April while rents also increased, Statistics NZ said in a statement Tuesday in Wellington. Airfares and fuel prices declined.

- (Bloomberg) -- New Zealand recorded the most citizen departures in 13 years in the 12 months through June, reducing the net gain through immigration to the lowest in more than two and a half years. Some 71,851 citizens departed the country in the period, the most since June 2012, Statistics New Zealand said Friday in Wellington. There were 25,353 returning citizens, resulting in a net exodus of 46,497.

- Cash US tsys are ~1bp richer in today's Asia-Pac session after yesterday's post-PPI sell-off.

- Swap rates closed 2-3bps higher.

- RBNZ dated OIS pricing closed little changed across meetings. 23bps of easing is priced for August, with a cumulative 42bps by November 2025.

- Next week, the local calendar will see the Performance Services Index on Monday, PPI data on Tuesday and the RBNZ Policy Decision on Wednesday.

FOREX: Asia FX Wrap - PPI Gives The USD A Reprieve

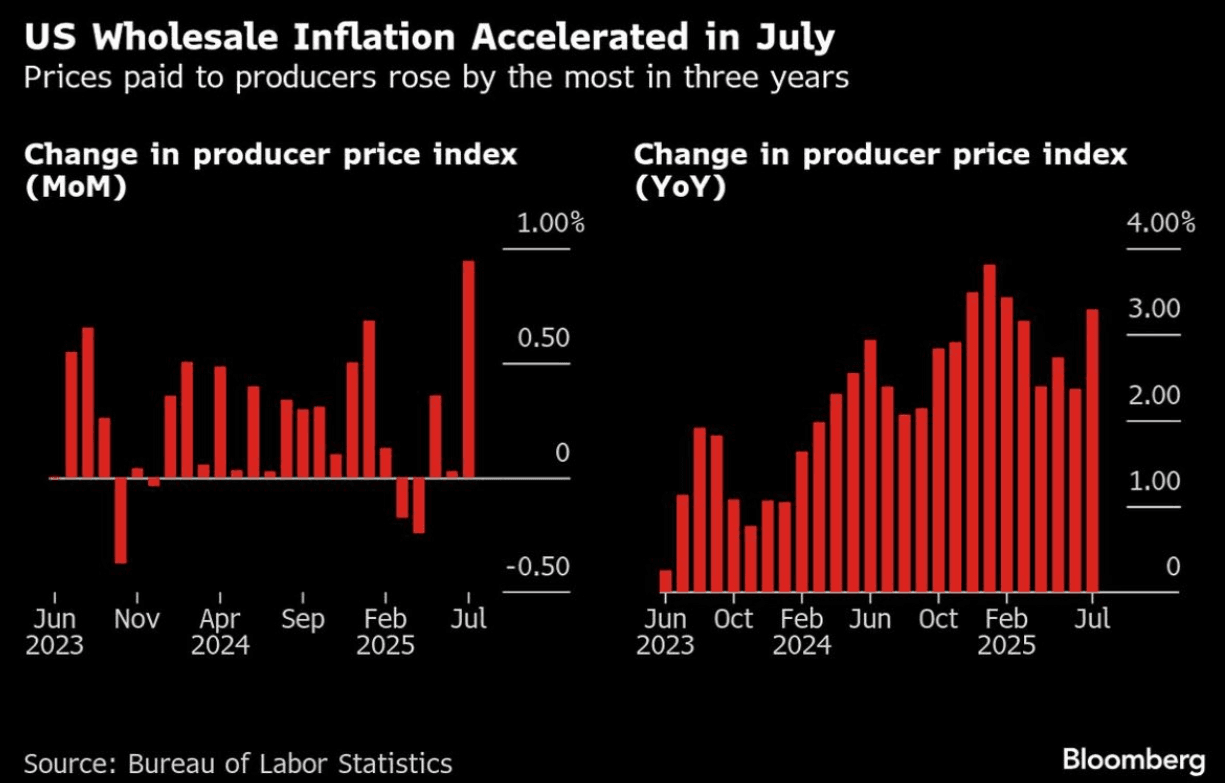

The BBDXY has had a range of 1204.29 - 1205.94 in the Asia-Pac session, it is currently trading around 1204, -0.15%. The USD again found some solid demand just below 1200 and the PPI print then gave it a lift off the lows. Is this just a stay of execution for the USD or can it gain some traction as it makes yet another higher low. The market is clearly more comfortable selling the USD but the longer it fails to extend below 1200 the higher the chances of a pullback. Alexander Stahel on X: "Say after me: stagflation. US wholesale inflation (PPI demand) up 0.9% mom & 3.3% yoy in July -> big -> Same ex energy & food -> companies pass on higher import costs related to tariffs. Sucks for Fed. If they do 25bps in Sept it’s on hold thereafter unless the jobs report blows up.” See Fig.1 Below.

- EUR/USD - Asian range 1.1646 - 1.1665, Asia is currently trading 1.1665. The market moved very quickly back to 1.1700 where it stalled on its first attempt to challenge this area. The pair's momentum higher was extinguished by the data overnight, look for some consolidation while the market looks for some direction.

- GBP/USD - Asian range 1.3526 - 1.3551, Asia is currently dealing around 1.3550. GBP stalled back towards 1.3600 overnight, first support seen now back towards 1.3400/1.3500.

- USD/CNH - Asian range 7.1786-7.1865, the USD/CNY fix printed 7.1371, Asia is currently dealing around 7.1840. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.20%, Gold $3345, US 10-Year 4.27%, BBDXY 1204, Crude Oil $63.87

Fig 1: US Wholesale Inflation

Source: MNI - Market News/Bloomberg Finance L.P/@BurggrabenH

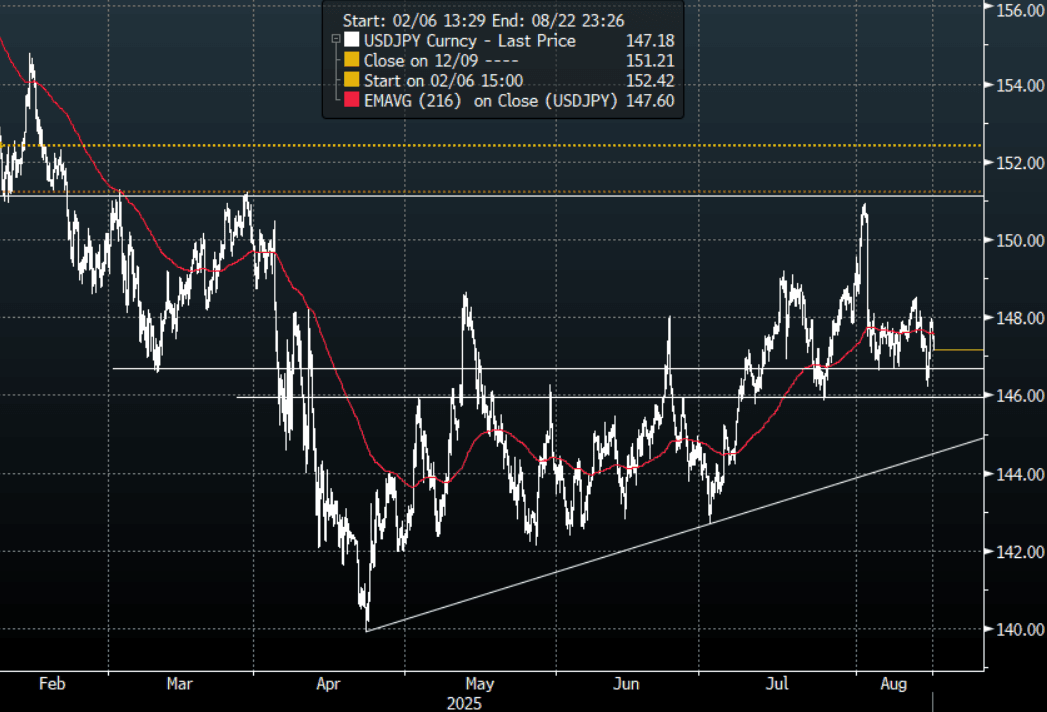

JPY: Asia Wrap - USD/JPY Tops Out Toward 148.00, Trades Offered In Asia

The Asia-Pac USD/JPY range has been 147.20-147.87, Asia is currently trading around 147.25, -0.35%. USD/JPY found good demand towards 146.00 and then reacted higher to the move in US yields by reversing the whole move lower. Price continues to hold above the support area between 146.00/147.00, a sustained move below this support is needed to turn the momentum potentially lower again. While this plays out it looks to be more range trading within the wider 146.00-151.00 range. The pair has traded heavily all throughout the Asian session after stalling towards 148.00.

- Japan Q2 GDP Beats, Aided By Strong Capex, Consumption Slightly Firmer: Japan Q2 GDP was better than market expectations. Q/Q growth rose 0.3%, against a 0.1% forecast, while the Q1 outcome was revised up a touch to 0.1% from the original flat estimate. In terms of the detail, private consumption rose 0.2% q/q, versus 0.1% forecast, while Q1 was revised up to 0.2% (originally reported as 0.1%). Capex was up 1.3%, versus 0.7% expected (Q1 was revised down 0.1% to a 1.0% gain). Net exports contributed 0.3% to growth (0.1% was forecast), while inventories took 0.3% off growth, in line with forecasts. Nominal GDP rose 1.3%q/q, a touch below market forecasts of 1.4%.

- "JAPAN FINMIN KATO: MUST CLOSELY WATCH ECONOMIC, PRICE BACKDROP BEHIND RECENT COMMENTS BY BUSINESS SECTOR CALLING ON BOJ TO RAISE RATES, THOUGH SPECIFIC MONETARY POLICY DECISION UP TO BOJ - [RTRS]"

- "JAPAN ECONOMY MINISTER AKAZAWA: U.S. TARIFF LIKELY TO PUSH DOWN JAPAN'S REAL GDP BY 0.3-0.4%, WON'T URGE BOJ TO SET RATES AT PARTICULAR LEVEL - [RTRS]"

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($977m), 150.00($685m).Upcoming Close Strikes : 150.00($846m Aug 19), 148.00($809m Aug 20) - BBG.

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

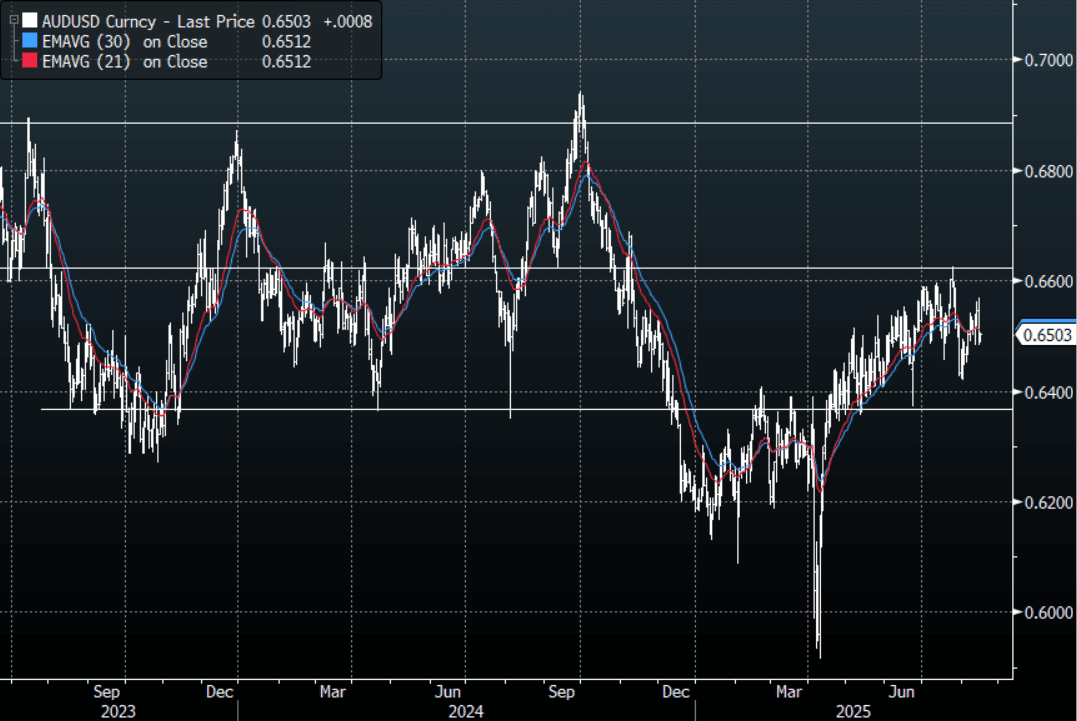

AUD: Asia Wrap - AUD/USD Drifts Higher

The AUD/USD has had a range of 0.6488 - 0.6505 in the Asia- Pac session, it is currently trading around 0.6505, +0.15%. US yields bounced hard in reaction to the PPI print, reigning in its expectations for larger rate cuts. This saw the USD get a reprieve and bounce off its support area. This has unfortunately really muddied the water for the AUD/USD just as it looked to be trying to build some upward momentum. AUD has drifted back to 0.6500 as a result, firmly in the middle of its 0.6350-0.6650 range with no clear direction. Softer China data was unable to get any follow through below 0.6500 in our session.

- China Property Investment & Sales Decline Further in July: There appears no end in sight for the property sector with Property Investment and Residential Property Sales declining further in July. Property investment Yet to date declined -12%, its worst result since late 2019 as COVID was erupting. Residential Property sales declined -6.2%, down from -5.2% in June. The data shows few bright spots with domestic loans for property and funds for property development down as new construction contracts -19.4%. Properties under construction were down -9.2%.

- China Industrial Production Expansion Weakest Since November: July's industrial production expanded +5.7%, missing estimates of +6.0% and below June's result of +6.8%. This was the weakest monthly result since November 2024.

- China Retail Sales Moderate Further in July: China's retail sales for July missed forecasts and was weaker than the month prior. July retail sales expanded +3.7%, the slowest since November 2024 and a second consecutive month of moderation.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6523(AUD562m), 0.6700(AUD498m). Upcoming Close Strikes : 0.6475(AUD428m Aug 18 ), 0.6515(AUD673m Aug 19), 0.6270(AUD435m Aug 19) - BBG

- CFTC Data shows Asset managers added to their shorts -60729(Last -49183), the Leveraged community added very slightly to their own shorts -13997(Last -13823).

- AUD/JPY - Asia-Pac range 95.59 - 96.07, Asia is trading around 95.75. The pair has bounced and tested its first resistance around the 96.50/97.00 area where momentum stalled. The sellers have capped the move for now, price is firmly back into the 94.50-97.50 range.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

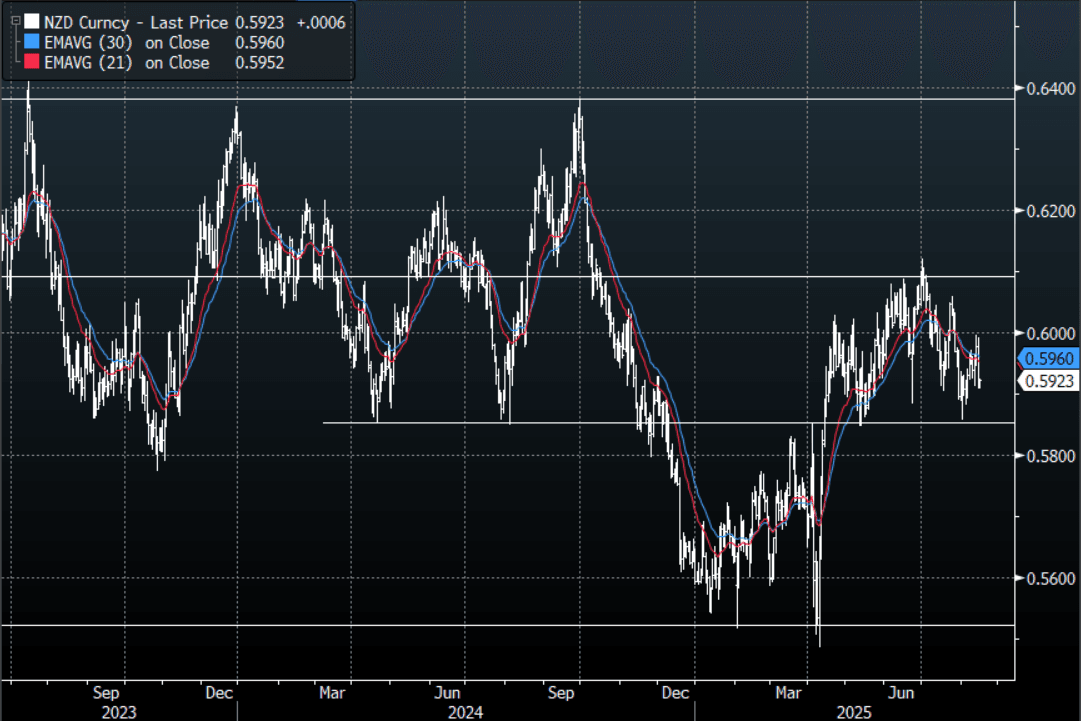

NZD: Asia Wrap - NZD/USD Consolidates Towards 0.5900

The NZD/USD had a range of 0.5908 - 0.5925 in the Asia-Pac session, going into the London open trading around 0.5920, +0.10%. US yields bounced hard in reaction to the PPI print, reigning in its expectations for larger rate cuts. This saw the USD get a reprieve and bounce off its support area. The NZD/USD has moved lower overnight in reaction to this but while still firmly in the 0.5850-0.6150 range it's tough to discern any real direction. Risk has traded a little stronger this morning, E-minis +0.20%, NQU5 +0.05%. NZD has had a quiet session treading water above 0.5900 in our session.

- NZ PMI Bounces Strongly In July, Back In Expansion Territory : The July BNZ manufacturing PMI rose to 52.8, from a revised 49.2 outcome in June (originally reported as 48.8). This puts the index back to March levels, with Feb's read of 54.0 the recent cycle high for the index. We did get as low as 47.4 in May, so at face value this is a decent recovery in the index.

- NZ Food Prices Up 5%y/y In July, Fuel, Travel & Accommodation Up M/M : For July, New Zealand food prices rose 0.7%m/m, after June's +1.2% gain. Food prices are now up 5.0% y/y. Stats NZ noted: "Higher prices for the grocery food group, up 5.1 percent, contributed the most to the annual increase in food prices. The price increase for the grocery food group was due to higher prices for milk, butter, and cheese."

- “NEW ZEALAND ANNUAL NET IMMIGRATION SLOWED TO 13,701 IN JUNE" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5925(NZD400m Aug 20). - BBG

- AUD/NZD range for the session has been 1.0969 - 1.0983, currently trading 1.0975. The Cross continues to trade sideways after stalling towards the 1.1000 area once more. The range looks to be 1.0850-1.1000 for now.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Japan Rebounds, HK Down, China Shrugs Off Weaker July Data

Stock trends are mixed in Asia Pac markets for the first part of Friday trade, although more markets are up than down at this stage. US equity futures sit little changed, while EU futures are painting a positive tone, up around 0.35% at this stage.

- China and Hong Kong markets are mixed. The HSI is off over 1%, while the CSI 300 and Shanghai Composite are up close to 0.50%. Disappointment on earnings appears to be weighing on Hong Kong markets, while July China data activity outcomes were all below market expectations. July home prices also fell again in m/m terms.

- This hasn't impacted onshore China equity market sentiment though. The authorities noted flood and higher temperatures impacted July activity. The outcomes may also encourage fresh stimulus. Focus this week has been on subsidy plans on loan interest for individuals and businesses aimed at improving consumption. Another proposal considered would see state owned enterprises purchasing unsold homes. The CSI 300 real estate sub index is up around 1.6% so far today.

- Elsewhere, Japan markets are rebounding from yesterday's losses. Both the Topix and NKY 225 are up around 1.15%. Earlier data showed Q2 GDP growth better than expected led by capex. USD/JPY is lower but still around 100pips above Thursday's lows.

- South Korean markets are closed today, while Taiwan's Taiex is up around 0.30%.

- In South East Asia, Indonesia's JCI hit record highs above 8000 earlier, but is away from best levels now. Focus is on President Prabowo's annual address, while the 2026 fiscal outlook will also be discussed later. Aiming for better growth, but along with fiscal responsibility, will market watch points.

- Singapore, Malaysia and the Philippines are weaker elsewhere in South East Asia.

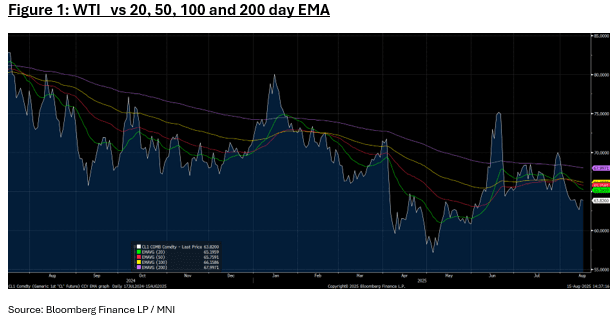

OIL: Slow End to the Week for Oil

- If oil maintains current level, it will end the week largely where it began.

- After finishing yesterday +2.09%, WTI is lower today by a mere -0.14% and -0.09% for the week.

- The strong gains overnight did little to change the technical picture as WTI remains below all major moving averages.

- Brent is down -0.15% in the Asia trading session, but remains up +0.24% for the week.

- OPEC+ crude oil production moderated in June for the first monthly decline for the year after reaching a 24-month-high in June. Saudi Arabia led the fall in production, easing its output after a surge in June.

- Chinese state-owned and mega-sized private refiners are snapping up Western Russian crude cargoes for Oct. and Nov. arrival as India eases off, according to Kpler (a global trade analytics company provider).

- The risks remain that a less than constructive discussion between US and Russia in Alaska could see a knee-jerk reaction from Trump resulting in increased sanctions against Russia that impact its flow of oil.

- US President Donald Trump warned he would impose "very severe consequences" if Vladimir Putin didn't agree to a ceasefire agreement later this week.

- Despite the imminent threats from the summit, global oil markets could record surplus next year as demand growth slows and supplies swell, the International Energy Agency said, with oil inventories forecast to grow at their fastest pace in 5-years.

- Oil inventories will accumulate at a rate of 2.96 million barrels a day, surpassing even the average buildup during the pandemic year of 2020, data from the IEA's monthly report showed. World oil demand this year and next is growing at less than half the pace seen in 2023.

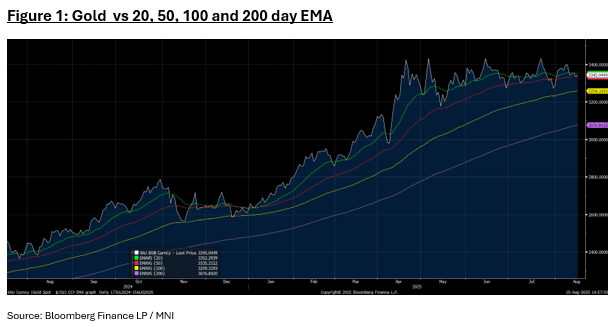

Gold Holds Modest Gains But Down for the Week

- Gold has delivered modest gains today of +0.29% taking bullion to US$3,345.19 yet remains down -1.54% for the week.

- Overnight US data saw strong producer price data cast doubt on Fed easing prospects, with a September Fed rate cut now no longer fully priced. US wholesale inflation accelerated in July by the most in three years, suggesting companies are passing along higher import costs related to tariffs. US wholesale inflation accelerated in July, suggesting companies are passing along higher import costs related to tariffs. The producer price index increased 0.9% from a month earlier, with services costs increasing 1.1% and goods prices excluding food and energy rising 0.4%. Certain policy-related price increases, such as a 1.2% rise in financial services and insurance costs, will contribute to core PCE inflation.

- Gold remains in tight ranges between the 20-day EMA $3,352.28 and the 50-day $3,335.20.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 15/08/2025 | 0700/0900 | * | CH Flash GDP | |

| 15/08/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/08/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/08/2025 | 1230/0830 | *** | Retail Sales | |

| 15/08/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 15/08/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/08/2025 | 1230/0830 | *** | Retail Sales | |

| 15/08/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/08/2025 | 1315/0915 | *** | Industrial Production |