US TSYS: Slightly Richer After Yesterday’s Post-PPI Sell-Off

TYU5 is dealing at 111-29, +0-03+ from closing levels in today's Asia-Pac session.

- July CPI and PPI data pulled market pricing in opposite directions this week. Softer CPI figures initially allowed markets to more than fully price in a 25bp Fed cut in September. However, that view was swiftly unwound after yesterday’s hotter-than-expected PPI report (headline +0.9% M/M vs. +0.2% expected), challenging the post-CPI narrative that tariff effects were proving less severe than feared.

- Bloomberg – “Garfield Reynolds, MLIV Team Leader, said "Treasuries will remain nervous heading into next week’s Jackson Hole event" with inflation concerns likely to see long-dated debt underperform.”

- Cash US tsys are ~1bp richer in today's Asia-Pac session after yesterday's post-PPI sell-off.

- The 4.35% area in 10-Year yields should still see demand initially, but the way the market keeps bouncing off levels just below 4.20% will be disconcerting for longs.

- Data/Events: Retail Sales, Empire Manu., Industrial Production, Business Inventories, U. of Mich. Sentiment, TIC Flows.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

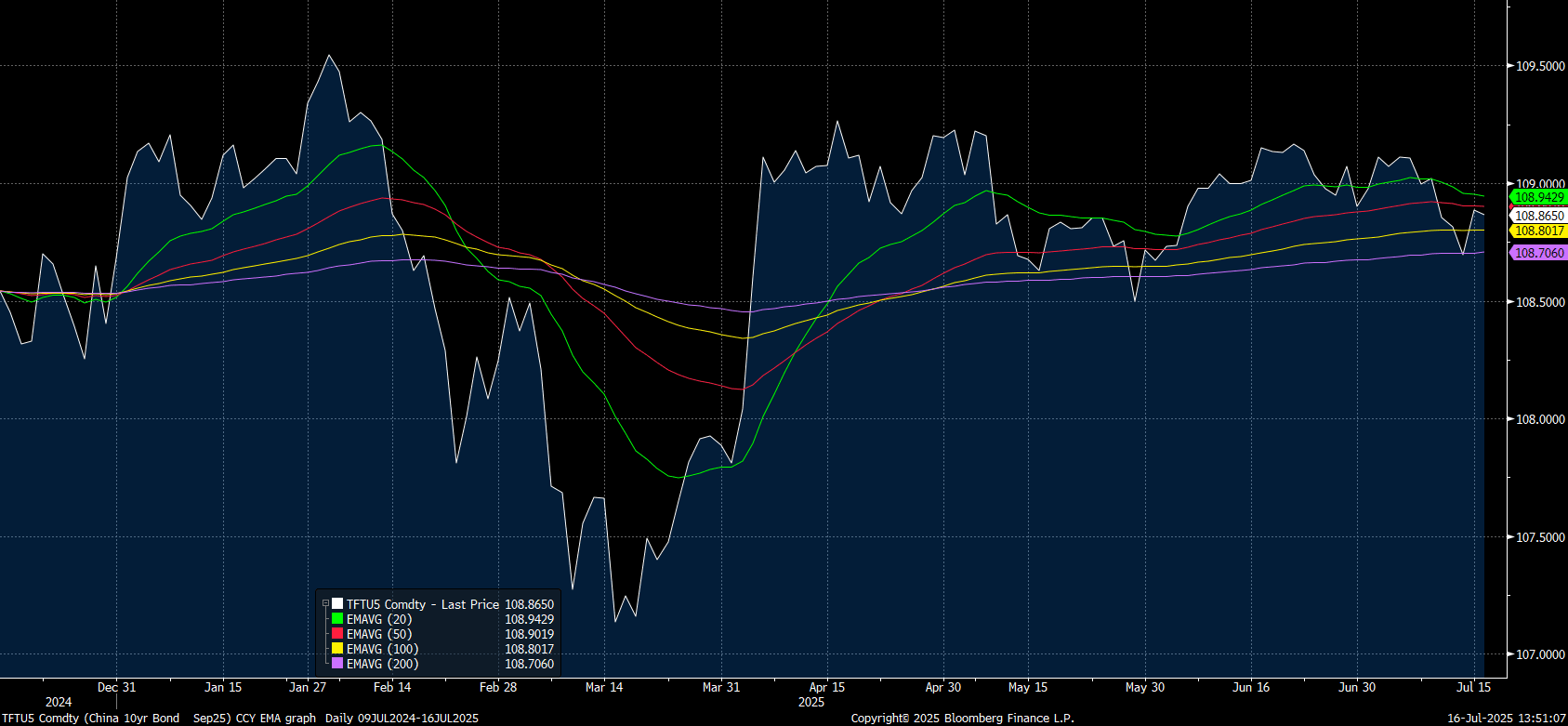

CHINA: Bond Futures Mixed in Morning Session

- China's key bond futures are moving in opposite directions in a quiet morning session.

- Having finished yesterday higher by +0.19, the 10yr future is lower by just -0.02 today at 108.865.

- The 10yr remains between the 50-day EMA of 108.90 and the 100-day EMA of 108.80

source: Bloomberg Finance LP / MNI

- The 2yr future is lower by -0.01 today at 102.42, having finished yesterday higher by +0.03.

- The 2yr future remains below all major moving averages with the 20-day above at 102.45.

- The CGB 10yr is at 1.66%

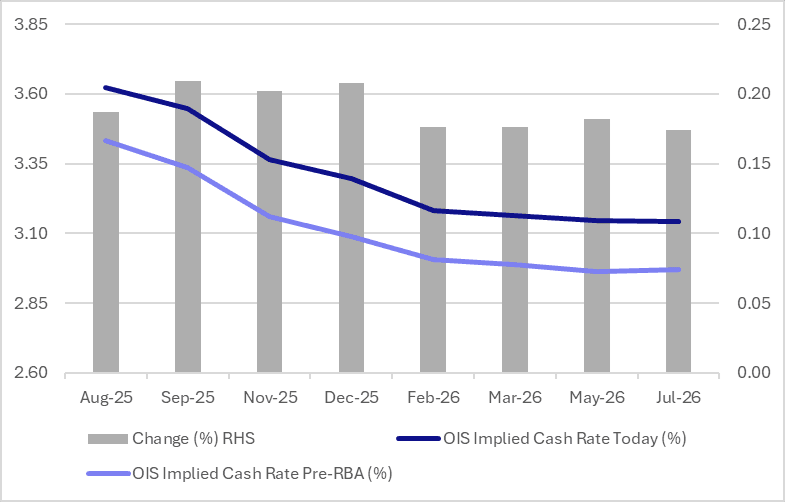

STIR: RBA Dated OIS Remains Sharply Firmer Than Pre-RBA Levels

RBA-dated OIS pricing is modestly firmer across meetings today and remains 17–21bps above levels seen prior to 8 July RBA decision.

- The RBA held the cash rate steady at 3.85%, defying market expectations that had assigned a 92% probability to a 25bp rate cut.

- Markets now assign an 87% probability to a 25bp cut in August, with a total of 54bps of easing priced in by year-end—down from 75bps ahead of the RBA decision.

Figure 1: RBA-Dated OIS – Current Vs. Pre-RBA

Source: Bloomberg Finance LP / MNI

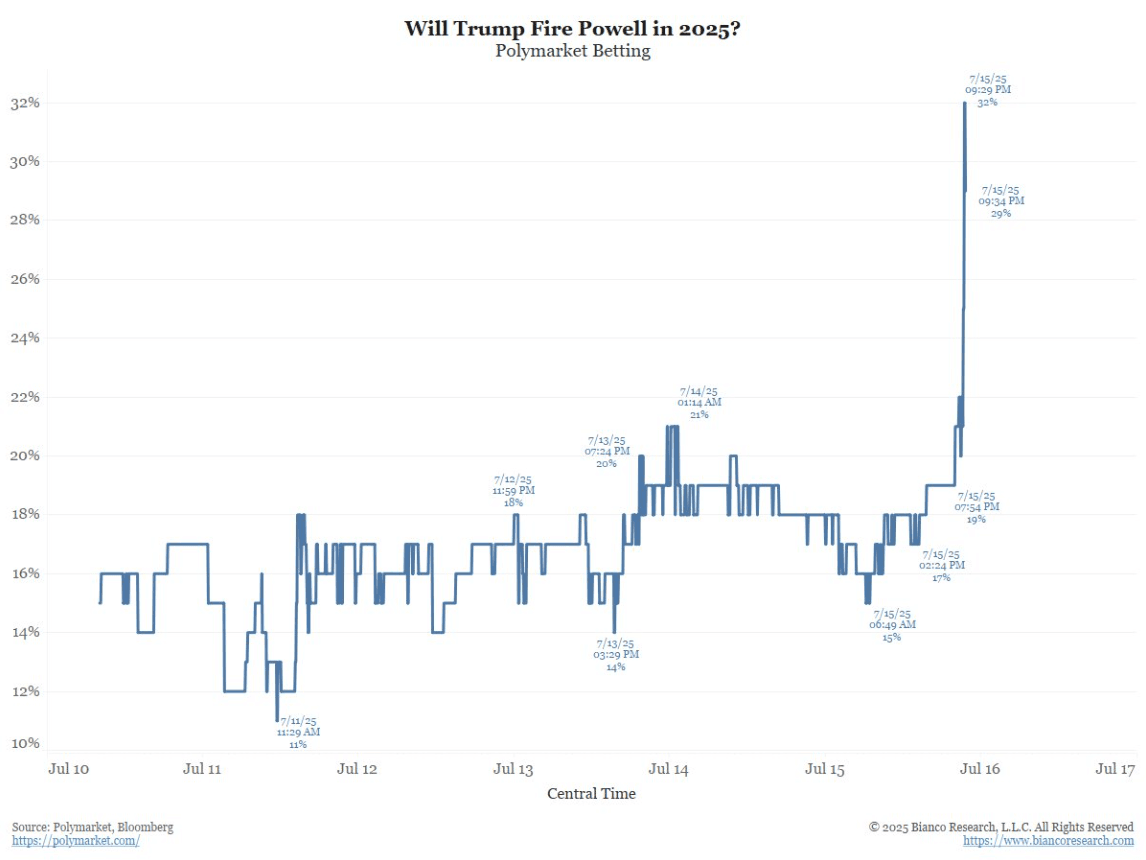

US: Is The Fed Chair Being Sacked Underpriced ?

A post on X from Congresswoman Anna Paulina Luna alluding to the imminent firing of Jerome Powell is adding fire to the situation. For the moment the market seems to be brushing this off and should it materialise is massively underpriced. What if the only way Trump can actually get yields lower is to replace the Fed Chair with someone who is willing to cut, and cut a lot. Should this happen it would further erode trust in US Assets and the USD would freefall once more. You would think the knee-jerk reaction would be higher in the Long-End but should an Uber Dove be appointed this could drive yields lower albeit with the front-end leading the charge and the curve steepening further.

- Rep. Anna Paulina Luna on X: “Jerome Powell is going to be fired. Firing is imminent.”

- (Bloomberg) -- “I think it sort of is,” President Donald Trump says when asked whether the renovations at the central bank were a fireable offense for Federal Reserve Chair Jerome Powell.

- Jim Bianco - “The betting market of “Will Trump fire Powell in 2025” has responded and the uptrend continues. See Graph Below.

Fig 1: Polymarket Betting - Will Trump Fire Powell In 2025

Source - @biancoresearch/Polymarket/Bloomberg