MNI EUROPEAN OPEN: Australian Business Conditions Improving

EXECUTIVE SUMMARY

- US JOB MARKET AS POTENTIAL PIVOT POINT - SHIN - MNI INTERVIEW

- WHITE HOUSE PREPARING REPORT CRITICAL OF BUREAU OF LABOR STATISTICS - WSJ

- NORWAY RULING LABOUR PARTY WINS REELECTION WHILE POPULISTS SCORE GAINS - RTRS

- JAPAN'S KONO SAYS BOJ NEEDS TO HIKE RATE TO FIX YEN, INFLATION - BBG

- AUSTRALIA'S CONSUMER PESSIMISM PERSISTS AS FIRMS MORE UPBEAT - BBG

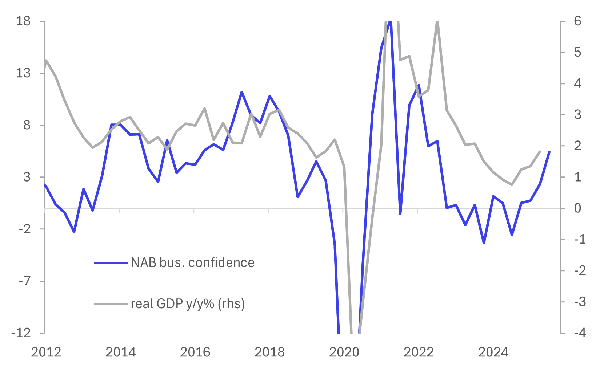

Fig 1: Australian NAB Business Conditions Pointing To Improving Growth Momentum

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

POLITICS (POLITICO): “Representatives from the CWU and ASLEF unions said they would come under pressure to disaffiliate from Labour if the government was to dilute its workers’ rights package. No. 10 has insisted dilution is not on the cards.”

RETAIL SALES (BBG): "UK's BRC like-for-like retail sales rose 2.9% y/y in August versus +1.8% in July, according to the British Retail Consortium."

EU

NORWAY (RTRS): “ Norway's minority Labour Party government won a second term in power on Monday while the populist right achieved its best-ever election result, official results showed, in a ballot dominated by concerns over rising living costs and wars in Ukraine and Gaza.”

FRANCE (BBG): “ French President Emmanuel Macron is seeking a fifth prime minister in less than two years to tackle the country’s debt problems and there are no obvious candidates with a decent chance of success.”

US

JOBS (WSJ): “ Five weeks after President Trump fired the chief of the agency that gathers the country's labor and price data, his advisers are preparing a report laying out alleged shortcomings of the Bureau of Labor Statistics' jobs data, according to people familiar with the matter.”

JOBS (MNI INTERVIEW): A raft of soft U.S. jobs data adds weight to Fed Chair Jerome Powell's view that labor market risks have increased, though central bank officials need more time to determine whether employment has hit a pivot point, Yongseok Shin, a St. Louis Fed research fellow and economist at Washington University in St. Louis, told MNI.

OTHER

JAPAN (BBG): "The Bank of Japan should raise its benchmark rate to support the yen and curb inflation, Liberal Democratic Party lawmaker and former digital transformation minister Kono Taro said, as political uncertainty clouds the outlook for economic policy."

JAPAN (BBG): "- Japan’s ruling party is set to decide when and how an upcoming leadership race will be held, after Prime Minister Shigeru Ishiba’s resignation announcement triggered a vote to choose his successor."

AUSTRALIA (BBG): "Australia’s consumer confidence declined as households worried about prospects for the economy, while business conditions improved led by gains in profitability and employment."

INDONESIA (BBG): "Indonesia’s new Finance Minister Purbaya Yudhi Sadewa will maintain fiscal discipline so that the national budget remains healthy and credible, he says during a handover ceremony in Jakarta on Tuesday."

THAILAND (BBG): "Thaksin Shinawatra, a two-time former Thai prime minister, was ordered by a court to serve one year in prison to complete a past conviction, the latest in a string of setbacks for the influential politician whose daughter was ousted as prime minister last month."

CHINA

ECONOMY (YICAI): “The Yicai Chief Economist Confidence Index rose to 50.6 in September from 50.2 in August, according to Yicai. Cheng Shi, chief economist at ICBC International, noted China's economy exhibited steady improvement, supported by recovering consumption, industrial upgrading and more diversified foreign trade.”

BOND ISSUANCE (SECURITIES DAILY): “Chinese local governments have issued new special bonds totaling 3.38 trillion yuan ($474 billion) as of Sept.8, completing 76.9% of the planned 4.4 trillion yuan ($617 billion) issuance quota this year, Securities Daily reports, citing data provided by Wind.”

CONSUMPTION (CSJ): “Ministry of Commerce will introduce more policy measures to support service consumption this month, China Securities Journal says in front-page report.”

MNI: PBOC Net Drains CNY8.7 Bln via OMO Tuesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY247 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY8.7 billion after offsetting maturities of CNY255.7 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.4562% at 10:00 am local time from the close of 1.4523% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 48 on Monday, compared with the close of 50 on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.1008 Tues; -0.53% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1008 on Tuesday, compared with 7.1029 set on Monday. The fixing was estimated at 7.1249 by Bloomberg survey today.

MARKET DATA

UK AUG. BRC LIKE-FOR-LIKE RETAIL SALES +2.9% Y/Y; EST. +2.0%; JUL. +1.8%

NEW ZEALAND Q2 MANUFACTURING VOLUMES -2.9% Q/Q; Q1 +2.4%

NEW ZEALAND Q2 MANUFACTURING SALES -3.0% Q/Q; Q1 +4.8%

AUSTRALIA SEPT. WESTPAC CONSUMER CONFIDENCE 95.4; AUG. 98.5

AUSTRALIA SEPT. WESTPAC CONSUMER CONFIDENCE -3.1% M/M; AUG. +5.7%

AUSTRALIA AUG NAB BUSINESS CONDITIONS INDEX +7; JUL +5

AUSTRALIA AUG NAB BUSINESS CONFIDENCE INDEX +4; JUL +8

JAPAN AUG. M3 MONEY STOCK +0.8% Y/Y; JUL. +0.6%

JAPAN AUG. M2 MONEY STOCK +1.3% Y/Y; JUL. +1.0%

MARKETS

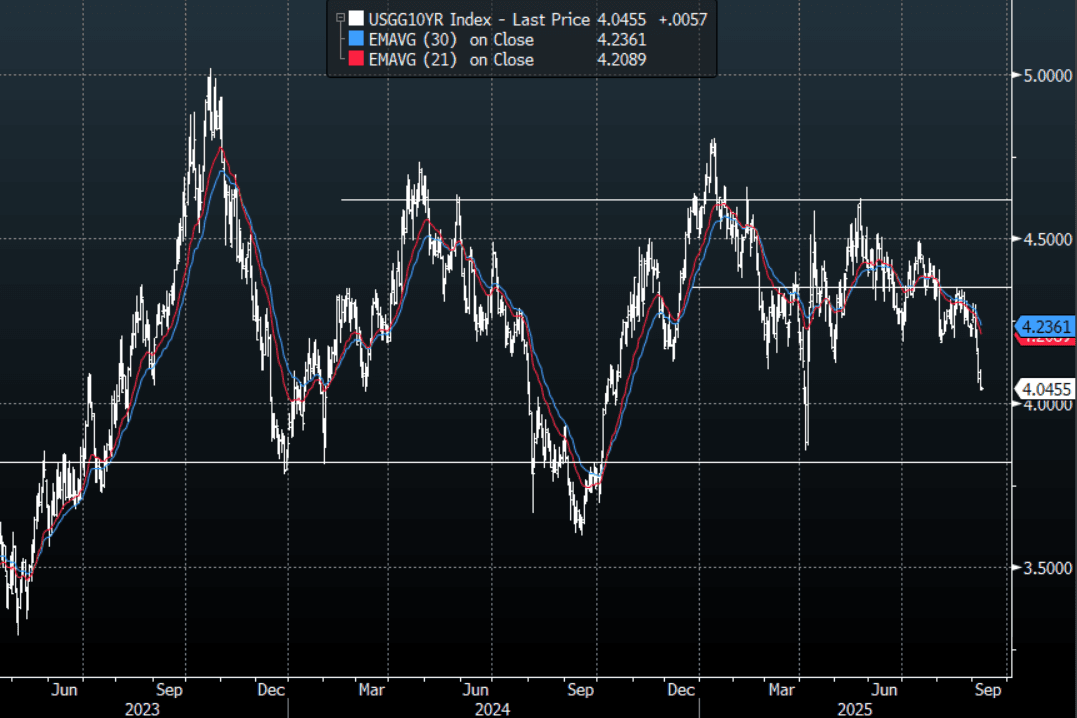

US TSYS: Asia Wrap -Yields Slightly Higher In A Quiet Session

The TYZ5 range has been 113-17+ to 113-19 during the Asia-Pacific session. It last changed hands at 113-17+, unchanged from the previous close.

- The US 2-year yield has edged higher trading around 3.493%, up 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.045%, up 0.01 from its close.

- 10-Year Yields have broken through its support as the market reacts to a labour market that is rapidly cooling. This move should now see buyers return on bounces with the first buy-zone back towards 4.20%. First target the 4.00% zone then the 3.80% area.

- Lance Roberts(RIA) - “Today we will also get the annual revisions to the BLS employment report. That adjustment will likely show that over the last 12-months somewhere between 550,000 to 800,000 fewer jobs were created than originally reported based on the QCEW report. The bond market responded as expected. Bond yields fell as investors realized the disinflationary impact of slower employment and wage growth would increase recession risk. If the revisions to employment show a substantially weaker than expected outcome, bond yields will likely fall further.”

- Bloomberg Economics - “Wall Street expects preliminary benchmark revisions to Bureau of Labor Statistics data, due out Sept. 9, to show that payrolls in the 12 months through March 2025 were overstated by 800k-1 million jobs. We expect a smaller downward revision, of about 560k. That’s still historically large - especially after the massive downward revision a year ago covering the 12 months through March 2024.”

- Data/Events: NFIB Small Business Optimism, Prelim. Benchmark Payrolls Revision

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Futures Uptick Sold, 5yr Supply Tomorrow

JGB futures sit comfortably off earlier high, last 138.00, -.04 versus settlement levels. In the first part of trade we got to 138.27, but broader positive momentum for bond futures has faded as the session progressed in Asia Pac. US 10yr futures sit unchanged, while other benchmarks have ticked down.

- Outside of broader bond future trends, focus remains on the domestic outlook, with comments today likely helping softer JGB futures at the margin.

- LDP member and former Minister Kono Taro spoke today, noting that if the BoJ delays hiking it will boost inflation (via BBG). He added that the weak yen can be fixed by hiking rates. Kono stated he was undecided on whether to run for the PM position. Kono is more hawkish (compared to other potential PM candidates) when it comes to the fiscal and monetary policy outlooks.

- Current Finance Minister Kato stated: ""JAPAN FINANCE MINISTER KATO SAYS WILL CAREFULLY CONSIDER THE POSSIBILITY WHEN ASKED ABOUT ENTERING THE LDP LEADERSHIP RACE - [RTRS]". He added that price relief is needed to protect low income households (via BBG).

- On the data front, we had Aug money stock figures earlier, while preliminary machine tool orders are out a little later (not likely to be a market mover).

- In the cash JGB space, yields sit up from earlier lows, with the front end slightly leading. The 10yr yield was last around 1.56%, the 30yr back above 3.26%. The 2/30s curve is back under +243bps, 2bps flatter.

- The data calendar is empty tomorrow, but we do have 5yr supply on tap.

AUSSIE BONDS: Yields Up From Lows, Business Sentiment Points To Improving GDP

Aussie bond futures sit off earlier highs, consistent with some softness in US Tsy futures, while locally today sentiment data outcomes were mixed. The 10yr future (XM) was last at 95.705, up 1bps, but against earlier highs of 95.74. 3yr futures sit down a touch, last near 96.555 (earlier highs were at 96.59).

- In the cash ACGB yield space we are up from earlier lows. The 3yr has ticked back up to 3.43%, while the 10yr is near 4.26%, only down 1bps for the session. Both yields were around multi week lows in the first part of trade.

- The 3/10s curve is holding flatter at +84bps.

- On the data front, Westpac consumer sentiment fell 3.1% m/m to 95.4 in September after August’s robust +5.7% m/m to 98.5. It remains in pessimistic territory but above the 2025 average helped by 75bp of monetary easing and lower inflation.

- August NAB business confidence fell to +4 from +8 but conditions improved to +7 from +5. Both have improved in Q3 to date by around 3 points signalling that GDP growth should continue to recover. The price/cost components were lower in August with purchase cost and retail price increases at multi-year lows, which should reassure the RBA.

BONDS: NZGBS: Yields Up From Earlier Lows, Q2 Data Points To Weak GDP

NZGB benchmark yields are up from earlier lows. The 2yr yield is now up close to 2bps, tracking back towards 2.95%. The 10yr NZGB yield is around 4.31%, still off 1.5bps. Both benchmarks remain close to recent lows. US Tsy yields have drifted a touch higher, led by the front end, which may have spilled over to NZ at the margins.

- The NZ 2/10s curve remains flatter last near +136.5bps. The NZ 2yr swap rate has edged up to 2.735%, against earlier lows near 2.705%, so mirroring the movement in NZGB front end yields.

- On the data front, Q2 NZ business sales values rose 2.1% q/q with profits up 4.2%. Salaries and wages rose only 1.2% q/q. Manufacturing volumes fell 2.9% q/q after rising 2.4%. Q2 GDP is released on September 18 and the RBNZ is forecasting it to fall 0.3% q/q. Data has shown weak building, goods exports and manufacturing volumes. The RBNZ is expected to cut rates at its October and November meetings.

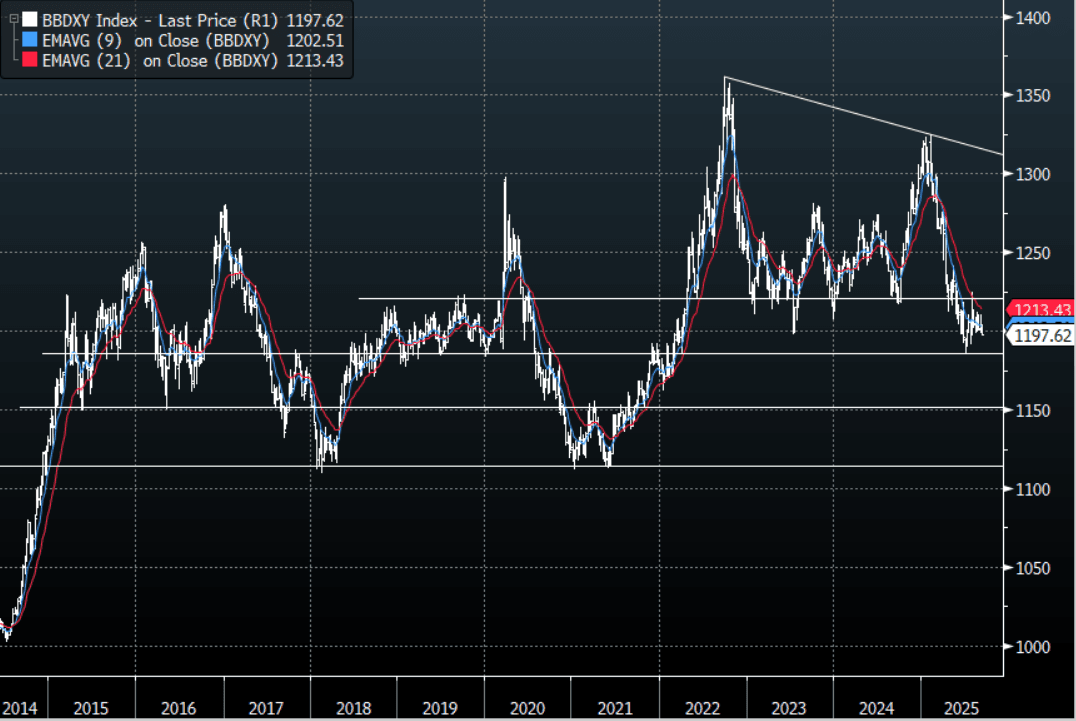

FOREX: Asia FX Wrap - BBDXY Probing Below 1200

The BBDXY has had a range of 1197.30 - 1198.68 in the Asia-Pac session, it is currently trading around 1197, -0.08%. The USD trades very heavy as the moves in US yields start to take their toll. The headwinds for the USD seem to be compounding and a look below 1195 feels almost inevitable. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows. Should the USD start another leg lower it would have big implications for FX and potentially see a lot of the recent ranges in G10 broken.

- EUR/USD - Asian range 1.1759 - 1.1778, Asia is currently trading 1.1770. The pair continues to grind higher with focus turning back towards the range highs. EUR is still within its wider 1.1350-1.1850 range with a bias to the topside.

- GBP/USD - Asian range 1.3544 - 1.3574, Asia is currently dealing around 1.3570. The pair bounced strongly off its support around 1.3350 last week. The pair is grinding higher looking towards the top end of its 1.3350-1.3650 range.

- USD/CNH - Asian range 7.1168 - 7.1238, the USD/CNY fix printed 7.1008, Asia is currently dealing around 7.1200. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.10%, Gold $3652, US 10-Year 4.05%, BBDXY 1197, Crude Oil $62.66

- Data/Events : France Industrial Production MoM

Fig 1: BBDXY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - USD/JPY Drifts Lower After Filling In The Monday Morning Gap

The Asia-Pac USD/JPY range has been 147.16-147.58, Asia is currently trading around 147.20, -0.20%. USD/JPY could not hold onto the gains it made in early Asian trading yesterday and ended up filling in the gap. The support towards 146.00 comes back into view, it has been solid for most of July and August, can it continue to hold as the USD’s own support begins to look precarious. CFTC data shows leveraged funds again added a decent clip to their short JPY position last week so the inability for the price to extend yesterday would be disconcerting, a move back below 145/146 is needed to potentially start seeing these positions being flushed out.

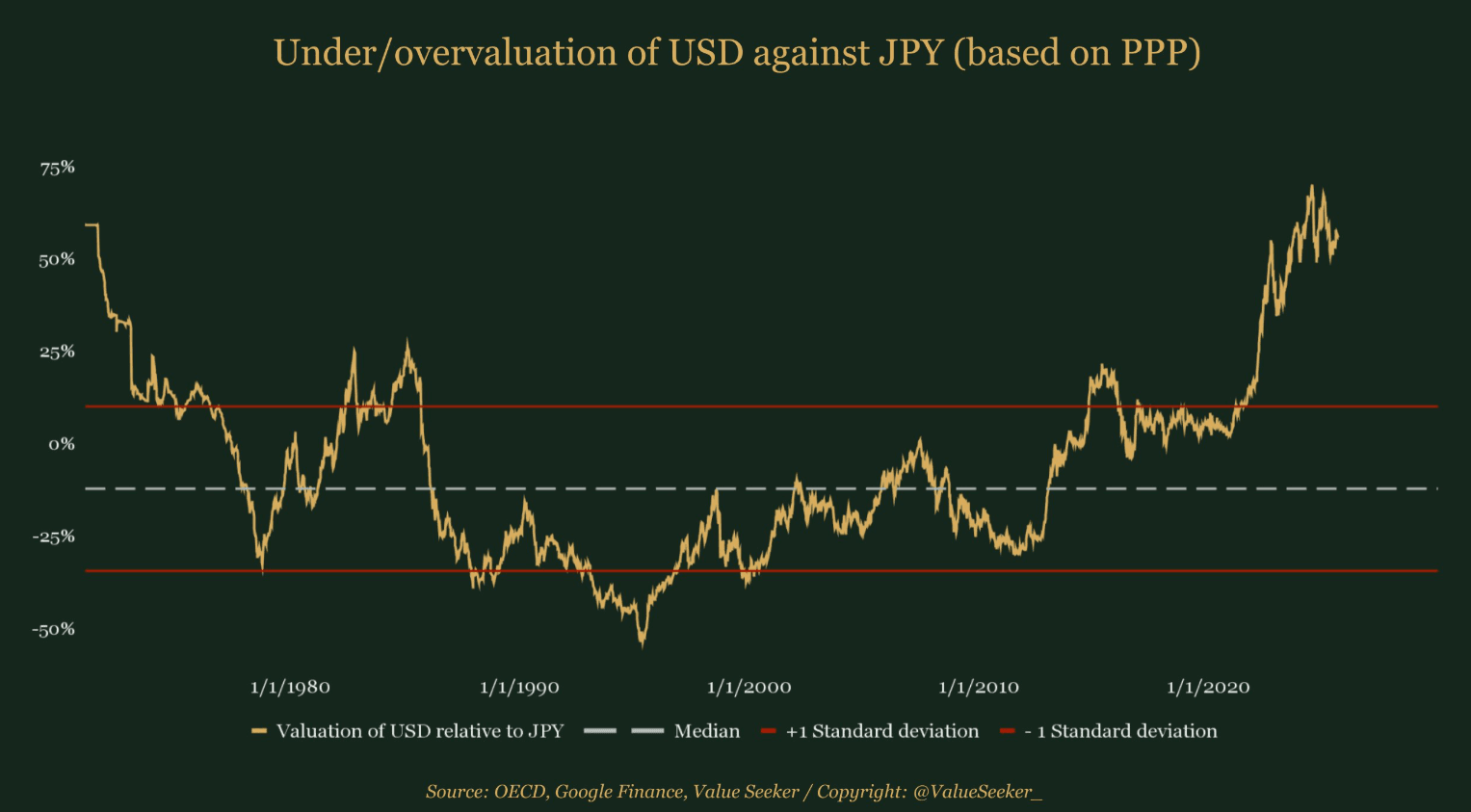

- Value Seeker on X: “The Japanese Yen remains highly undervalued relative to most currencies, including the US Dollar, which trades 50% (3 st. dev.) above its purchasing power parity against the Japanese currency.” See Graph Below.

- Bloomberg - “Japan’s Kono Says BOJ Needs to Hike Rate to Fix Yen, Inflation. The Bank of Japan should raise its benchmark rate to support the yen and curb inflation, Liberal Democratic Party lawmaker and former digital transformation minister Kono Taro said, as political uncertainty clouds the outlook for economic policy.”

- "KATO: MULL IMPACT OF TARIFFS, OPPOSITION VIEWS FOR ECO PACKAGE, PRICE RELIEF IS NEEDED TO PROTECT LOW-INCOME HOUSEHOLDS” - BBG

- "JAPAN LDP DECIDES TO HOLD 'FULL-SPEC' LEADERSHIP VOTE: NTV" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.00($931m), 147.50($521m).Upcoming Close Strikes : 145.75($1.12b Sept 11), 150.00($1.11b Sept 11) - BBG..

- CFTC data shows last week asset managers again added to their JPY longs after a consistent period of reduction +78427( Last +76761), leveraged funds though again used the dip to add a decent clip to their newly built short JPY position -66914(Last -52275). One of them is going to be wrong.

Fig 1 : JPY Undervaluation Vs USD(based on PPP)

Source: MNI - Market News/@ValueSeeker_/OECD

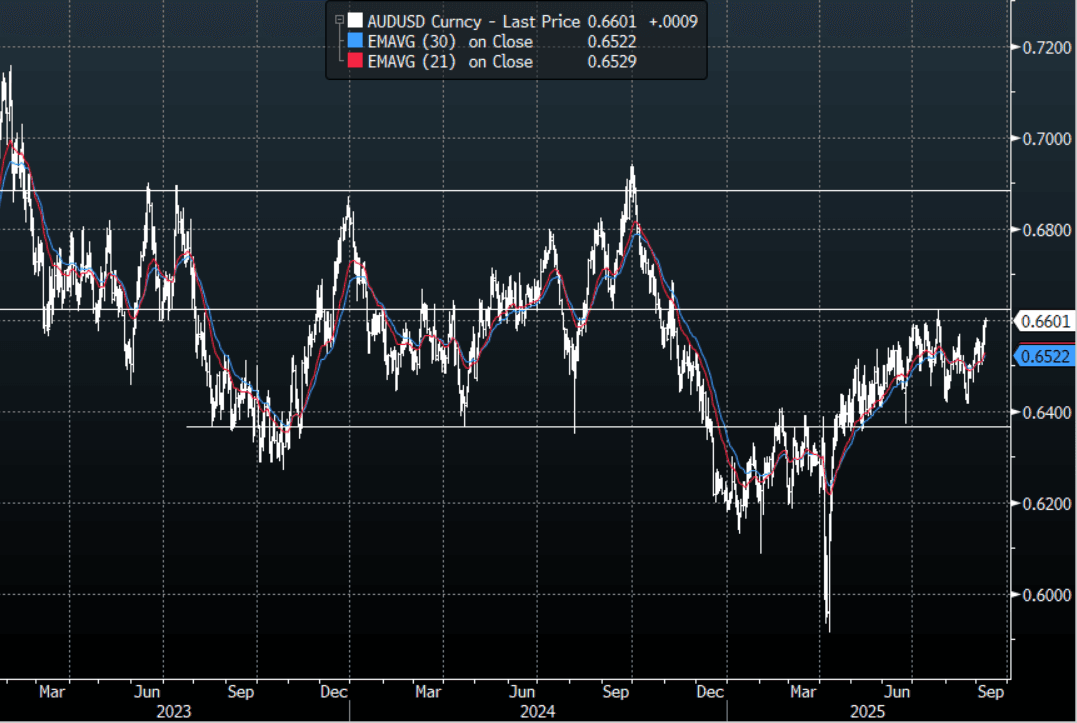

AUD: Asia Wrap - AUD/USD Probes Above 0.6600

The AUD/USD has had a range of 0.6588 - 0.6604 in the Asia- Pac session, it is currently trading around 0.6600, +0.12%. US rates extended lower again and the USD traded soft, the headwinds for the USD seem to be compounding which points to a potential look below its support. The AUD has drifted higher and is looking to test the top-end of its recent range. The AUD remains in its recent multi-month range of 0.6350-0.6650, should the USD break and extend lower we could potentially see the AUD break back above 0.6650. Should this occur it could provide the upward momentum to target levels back towards 0.6900/0.7000. Although still in the range the bias is for dips back to 0.6500 to be supported now.

- Growth Recovery Continued In Q3, August Costs/Prices Moderated. August NAB business confidence fell to +4 from +8 but conditions improved to +7 from +5. Both have improved in Q3 to date by around 3 points signaling that GDP growth should continue to recover. The price/cost components were lower in August with purchase cost and retail price increases at multi-year lows, which should reassure the RBA. However, the Q3 average of final product prices is still around where it was in H1 signaling some stabilisation in disinflation. Labour demand also appears to have steadied.

- Consumer Sentiment Weaker But Series Is Volatile: Westpac consumer sentiment fell 3.1% m/m to 95.4 in September after August’s robust +5.7% m/m to 98.5. It remains in pessimistic territory but above the 2025 average helped by 75bp of monetary easing and lower inflation.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6515(AUD429m), 0.6600(AUD420m). Upcoming Close Strikes : 0.6550(AUD777m Sept 10) - BBG

- CFTC Data last week shows Asset managers reduced their shorts for the first time in a while -66025(Last -78758), the Leveraged community though look to be rebuilding their own shorts after winding them down -11860(Last -6447).

- AUD/JPY - Asia-Pac range 97.12 - 97.28, Asia is trading around 97.20. The pair topped out towards 97.50 but has held onto most of its gains on the gap higher yesterday unlike USD/JPY. A sustained break above 97.50/98.00 is needed to reignite the upward trend.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

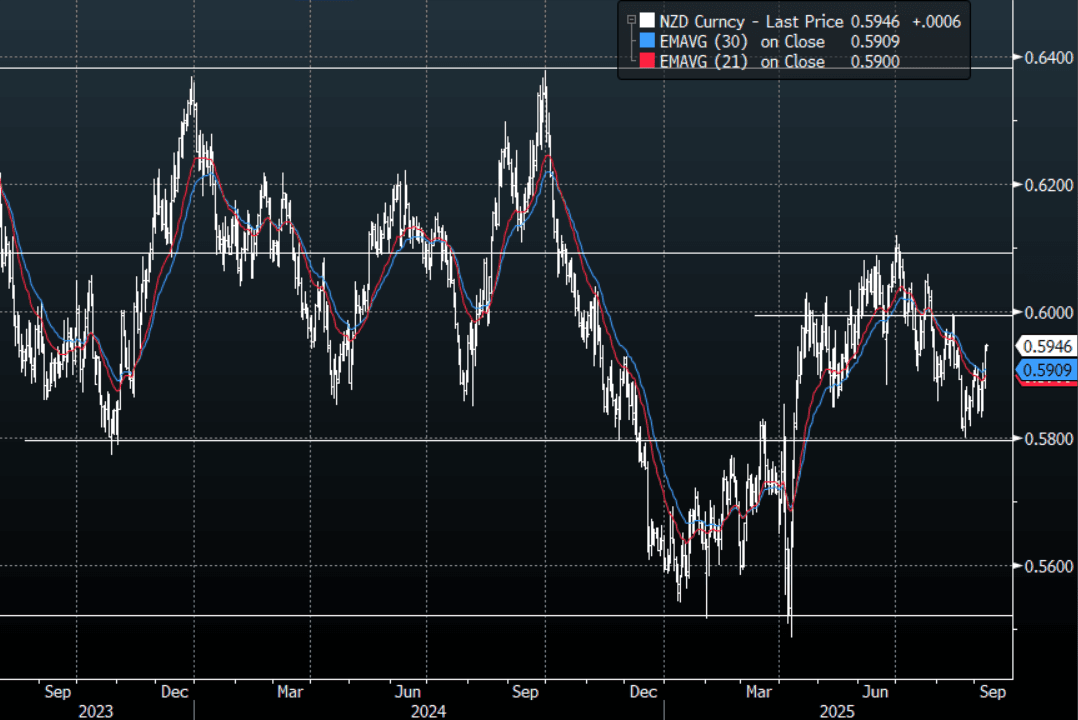

NZD: Asia Wrap - NZD/USD In The Sell Zone, The USD Is A Concern Though

The NZD/USD had a range of 0.5937 - 0.5949 in the Asia-Pac session, going into the London open trading around 0.5845, +0.10%. US rates extended lower again and the USD traded soft, the headwinds for the USD seem to be compounding which points to a potential look below its support. The NZD has bounced into what should be the perfect zone to fade for bears, the price action for the USD though gives me pause. CFTC Data shows light positioning in a market that is struggling for a strong trend as we move back into the middle of the recent 0.5800-0.6100 range.

- (Bloomberg) -- “New Zealand’s main opposition Labour Party is open to having a discussion about the RBNZ’s 1-3% inflation target, the NZ Herald reports.”

- Q2 Data Suggesting Weak GDP Outcome: Q2 NZ business sales values rose 2.1% q/q with profits up 4.2%. Salaries and wages rose only 1.2% q/q. Manufacturing volumes fell 2.9% q/q after rising 2.4%. Q2 GDP is released on September 18 and the RBNZ is forecasting it to fall 0.3% q/q. Data has shown weak building, goods exports and manufacturing volumes. The RBNZ is expected to cut rates at its October and November meetings.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5800(NZD515m Sept 10), 0.5870(NZD320m Sept 10) - BBG

- CFTC Data of last week shows Asset Managers added slightly to their new short position in the NZD -5127(Last -4743), the Leveraged community have completely exited their short and have turned a fraction long +285(Last -225).

- AUD/NZD range for the session has been 1.1093 - 1.1105, currently trading 1.1100. The Cross is consolidating around 1.1100, dips back towards 1.1000/1.1050 should be supported now.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: A Mixed Day as Jakarta Down

Indonesia stocks slid again today following yesterday's shock announcement of the removal of the popular Finance Minister. Concerns are rising as to whether the Prabowo government will maintain fiscal discipline and damage the long term outlook for the economy. Japanese stocks were weaker today after yesterday's gains, in what local traders are describing as profit taking. China's homebuilder index is up by around 5% as after Shenzhen announced home buying curbs will be eased yesterday, with the positive momentum carried into today.

- China's major onshore bourses were all lower today with the CSI 300 down -0.46%, Shanghai Comp -0.29% and Shenzhen down -0.80% whilst the Hang Seng in Hong Kong went the other way, up +0.80%.

- The NIKKEI is down moderately by -0.13%

- The TAIEX in Taiwan is one of the strongest regional performers today as portfolio inflows turn strongly positive; up +1.05% today.

- The KOSPI is up again, today by +1.10%, and has now gained for six successive trading days.

- The FTSE Malay KLCI is lower by -0.12%.

- The Jakarta Composite is down heavily by -1.75% following yesterday's falls of -1.28%hp

- India's NIFTY 50 has had five days of very modest gains and is up today by a mere +0.27%

OIL: Crude Continues Rally, EIA Report & US Inventory Data Out Later

Oil prices have continued to rise during today’s APAC trading after rallying around a percent on Monday. WTI is 0.7% higher at $62.70/bbl, close to the intraday day high, and Brent is up 0.7% to $66.46/bbl. The USD index is 0.1% lower today, which is likely supportive of dollar-denominated crude.

- The IEA forecast a record market surplus for 2026, which has pressured oil prices. The EIA short-term energy outlook is published Tuesday with the IEA and OPEC monthly reports on Thursday. After OPEC’s weekend decision to increase its production target 137kbd, the projections in these reports will be watched closely.

- Saudi Arabia cut prices for October across grades for its Asian buyers after OPEC hiked output 2.2mbd over the last five months. This is another sign that the group is now focussed on regaining market share rather than managing prices. US shale producers have grown their share in recent years.

- Industry-based US inventory data is also out today.

- US benchmark revisions to payrolls are released later. US August NFIB small business optimism prints. The ECB’s Montagner & Machado and the BoE’s Breeden appear.

GOLD: Another New Record High, US Payroll Revisions Later

Gold prices reached a new record high of $3654.57/oz during today’s APAC session but are currently around $3652.8 to be up 0.5% on the day. Friday’s disappointing US payroll data has bolstered Fed cut expectations with over 25bp now priced in for September 17 and almost 75bp by year end. The market is also waiting for the ruling on whether Fed Governor Cook can be removed. The US dollar is 0.1% lower today while yields are little changed.

- Gold held below resistance at $3674.8. Today’s US payroll revisions, Wednesday’s August PPI and Thursday’s CPI will be important for the rate outlook and thus for non-yield bearing bullion.

- ETF flows into gold have also pushed prices higher with Bloomberg reporting Monday’s inflows were the highest in close to 3 months.

- Silver is off its intraday low of $41.209 to be little changed around $41.35. It reached $41.419 earlier holding below resistance $41.467.

- Equities are mixed with the S&P e-mini is up 0.1% and Hang Seng +0.8% but CSI 300 down 0.5% and Jakarta Comp -1.6%. Oil prices are higher again with WTI +0.6% to $62.66/bbl. Copper is up 0.3%.

- US benchmark revisions to payrolls are released later. US August NFIB small business optimism prints. The ECB’s Montagner & Machado and the BoE’s Breeden appear.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 09/09/2025 | 0645/0845 | * | Industrial Production | |

| 09/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 09/09/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 09/09/2025 | 1150/1350 | SNB's Schlegel at BIS fireside chat | ||

| 09/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 09/09/2025 | 1400/1000 | *** | Preliminary Benchmark Revision | |

| 09/09/2025 | 1515/1615 | BOE Breeden Moderates BIS Fireside Chat | ||

| 09/09/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 10/09/2025 | 0130/0930 | *** | CPI | |

| 10/09/2025 | 0130/0930 | *** | Producer Price Index | |

| 10/09/2025 | 0600/0800 | *** | CPI Norway | |

| 10/09/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/09/2025 | 0700/0900 | ** | Industrial Production | |

| 10/09/2025 | 0800/1000 | * | Industrial Production | |

| 10/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 10/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 10/09/2025 | 1145/1345 | SNB's Schlegel on Central Bank Communication in Vezia | ||

| 10/09/2025 | - | *** | Money Supply | |

| 10/09/2025 | - | *** | New Loans | |

| 10/09/2025 | - | *** | Social Financing | |

| 10/09/2025 | 1230/0830 | *** | PPI | |

| 10/09/2025 | 1230/0830 | *** | PPI |