MNI EUROPEAN MARKTS ANALYSIS: US CPI In Focus Later

- Headlines crossed in the first part of the session that US and China will aim to implement what was agreed too at the Geneva talks from May (subject to approval from both US and China leaders). Market impact has been minimal, with US equity futures sitting modestly in the red, while US yields are little changed. China and Hong Kong equities are higher, but there has been little broader spillover.

- JGB futures are stronger and near session highs, +15 compared to settlement levels, despite MoF pushback against recent speculation of bond buybacks in July.

- Later US May CPI prints and is expected to show a 0.1pp pickup in both core and headline to 2.4% y/y and 2.9% y/y. It will be monitored for signs of any tariff impact. The US May federal budget is also released. ECB’s Lagarde, Lane, Cipollone and Buch appear today.

MARKETS

US TSYS: Asia Wrap - A Quiet Session, Focus On CPI

The TYU5 range has been 110-03+ to 110-08+ during the Asia-Pacific session. It last changed hands at 110-07+, up 0-01 from the previous close.

- The US 2-year yield is dealing around 4.012%, down 0.01 from its close.

- The US 10-year yield is trading around 4.466%, unchanged from its close.

- Bloomberg - “Treasury 10-year contracts are heading lower as today’s debt auction is unlikely to offer enough juice for it to run smoothly given there is a 30-year sale to follow and CPI data due. Indeed, investors appear to be nervous about the outcome of the longer duration offering which by default could make it more difficult for the ten-year which needs to be first.”

- Bloomberg - “Morgan Stanley strategists expect a surprise decrease in inflation data and declining oil prices to reduce the bond market's inflation expectations over the next two years.”

- The 10-year yield held its support around the 4.35% area last week. While this level holds focus will remain on potentially extending higher, CPI tonight will dictate direction.

- Data/Events: CPI, Federal Budget Balance

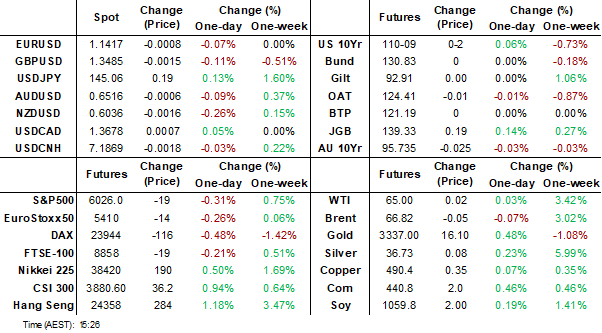

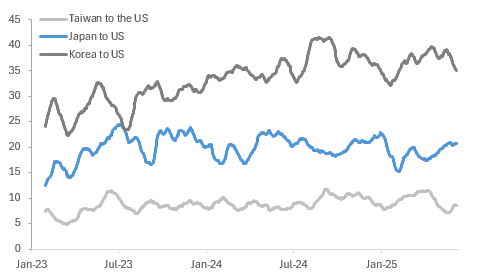

GLOBAL MACRO: Ships To US Normalising But Frontloading May Reduce H2

Container ship tracking data suggest that trade flows have picked up again following the April 2 US announcement of extensive reciprocal tariffs as traders take advantage of the 90-day delay which expires July 8. Most major routes to the US have seen the number of vessels return to around average. Trade talks are ongoing and will determine if this stays the case in Q3 but the inventory build ahead of deadlines may drive a reduction in global trade flows in H2 anyway.

- Bloomberg’s container ship count data covers the number of loaded ships leaving for the US. Looking at the 30-day average, shipments from Europe, Korea, Taiwan and Japan rose over Q1 to beat initial US deadlines, and then all ex Japan declined over April.

Bloomberg container ship count 30-day moving average

Source: MNI - Market News/Bloomberg Finance L.P.

- Interestingly cargos leaving China had been trending down from September to end-March signalling no intention to frontload exports. However, then they rose sharply to mid-April before plummeting again in line with the escalation in the US-China trade spat but at the end of April before the US-China Geneva meeting announcement on May 11 they rose sharply possibly on a willingness to absorb tariffs or expectations that they would be delayed or reduced before the ships arrived.

Bloomberg container ship count

- In June, the number of ships departing China for the US is around 5 above the average from 2023 to end-January 2025 suggesting a normalisation of trade flows or some frontloading. The number from Japan is in line with this average signalling expectations that a deal will be agreed. Taiwan is one ship above average this month and Korea is two.

- While European ships to the US are off the May 23 low, in June they were still 10 vessels below average. There was significant European frontloading in Q1, as seen by Irish pharmaceutical exports to the US, and this below-par recovery may reflect that.

GLOBAL MACRO: Sharply Higher June Shipping Rates Suggest Stronger Trade Growth

Container rates are consistent with a trade recovery over Q2 following the delay of US tariffs to early July, as also signalled by Bloomberg ship tracking data. Rates are significantly higher over May/June. Increased sailings since end-May have increased vessel demand and thus costs. Trade talks with the US are ongoing and will determine if rates rise further but inventory build ahead of tariff deadlines may drive a reduction in global trade in H2 anyway.

- The recent rise in bulk and container rates suggests that global trade growth (CPB) could trend higher towards mid-year after picking up to 6.6% y/y in March from 3.0% y/y in December.

Global trade growth vs Baltic Freight Index

- The FBX global container index was up almost 60% on June 10 from 31 May with China/East Asia to North American east coast up 78%, to the Mediterranean +43% and Baltic Freight Index (BFI) +18.5%.

FBX container rates USD/points

- The month average FBX global rate fell sharply in the three months to April but then rose 4.7% m/m in May and is +69% m/m in June to date reaching its highest level since January. This increase is likely to reflect both optimism of a trade deals being reached plus further frontloading of exports in case they fail. But the FBX index is still down 15.2% y/y in June after -32% y/y.

- The China/East Asia to North American east coast route began to rise in April and the June average is up 85% m/m but still down 11.4% y/y but has reached its highest since September 2024.

- Bulk commodities have also seen an increase in shipping prices but less than containers. The BFI June average is up 22% m/m after falling in April and May and is still down 14.6% y/y but after 28.8% y/y.

JGBS: MoF: Buyback Unrealistic, RTRS Poll: BoJ On Hold This Year

JGB futures are stronger and near session highs, +15 compared to settlement levels

- BBG notes: " Buying back of super-long government bonds from July is unrealistic and not envisioned, an official from Japan's Ministry of Finance said in an email to Bloomberg News."

- Reuters Poll Summary – Bank of Japan Outlook: 52% of economists expect the BOJ to hold its key interest rate at 0.50% through year-end, up from 48% in May; 55% expect the BOJ to slow bond purchases starting April 2026, while 45% see no change;78% forecast a rate hike to at least 0.75% by end-Q1 2026; and 75% expect a reduction in super-long JGB issuance, while 25% see it unchanged.

- Cash US tsys are little changed in today's Asia-Pac session ahead of today's CPI data.

- Earlier US-China trade talk headlines from London had little impact on the markets.

- Cash JGBs are slightly mixed across benchmarks, with a mild steepening bias. The benchmark 10-year yield is 1.2bps lower at 1.466%.

- Swap rates are flat to 2bps lower. Swap spreads are tighter.

- Tomorrow, the local calendar will see BSI Industry Survey, Weekly International Investment Flows and Tokyo Avg Office Vacancies data alongside an auction for Enhanced-Liquidity of 15.5 - 39-year JGBs.

JAPAN DATA: PPI Weaker Than Forecast, Off Cycle Highs, Imports Down -10.3%Y/Y

Japan's May PPI was below market expectations, we fell 0.2% m/m (against a +0.2% forecast). April's rise was revised to +0.3% (from 0.2%). In y/y terms we printed 3.2%, against a 3.5% forecast (prior was 4.1%).

- The chart below plots the headline PPI y/y, against Japan CPI y/y. At face value it is suggesting less upside pressure on headline CPI pressures.

- In terms of the detail, manufacturing PPI was down 0.4%m/m. Weakness was evident in commodities, particularly petroleum, coal (-4.8%m/m). Iron ore and steel was also down in m/m terms.

- Import prices for commodities were down 1.1%m/m, continuing a negative trend, now off 10.3% in y/y terms.

Fig 1: Japan PPI Y/Y & Nationwide CPI Y/Y

Source: Bloomberg Finance L.P./ MNI

JAPAN DATA: Firmer Yen Y/Y Backdrop May Keep Import Prices Negative Near Term

Japan import prices in May fell to -10.3%y/y, the weakest read since Oct 2023. The chart below plots USD/JPY y/y changes against Japan import prices y/y. Note the y/y line for USD/JPY is extended to end Q3 of this year by assuming that current USD/JPY levels hold until then. If such conditions hold it suggests that the negative impulse to import prices from a stronger yen will fade by the end of Q3.

- If USD/JPY falls to say 140.00 and holds there, then the negative y/y import pulse may persist beyond end Q3. The rough sell-side consensus is for USD/JPY to track lower, not higher as we progress through 2025.

- At the margin, the firmer yen backdrop compared to 2024 may have given the BoJ some comfort around holding steady from a policy standpoint in the near term, even with real policy rates remaining negative.

- Import price shifts have a strong correlation with PPI y/y shifts: +87% for the past decade. The earlier headline PPI print suggested we may see headline CPI lose some y/y momentum as we progress through Q2.

- The PPI and CPI correlation has also been reasonable at +58%, but is much lower in terms of import prices and CPI at just 25%.

Fig 1: USD/JPY Y/Y & Japan Import Prices Y/Y

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Cheaper Ahead of US CPI, AU-US 10Y Diff Near Bottom Of Range

ACGBs (YM -5.0 & XM -2.0) are weaker after trading in narrow ranges on a local-data-light session.

- Cash US tsys are little changed in today's Asia-Pac session ahead of today's CPI data. Analyst unrounded estimates see core CPI inflation accelerating mildly to 0.27% M/M (median, 0.28% average) in May after 0.24% M/M in April. (See link)

- Focus has also been on US-China trade talks, with headlines from London crossing earlier. The market reaction has been fairly muted, with the main outcome being agreement to move forward with what was agreed at the Geneva talks in May (although both US and Chinese leaders need to sign off on implementation).

- Cash ACGBs are 2-4bps cheaper with a flatter curve and the AU-US 10-year yield differential at -20bps.

- The bills strip has cheapened, with pricing -2 to -3.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in July is given a 79% probability, with a cumulative 72bps of easing priced by year-end.

- Tomorrow, the local calendar will be empty apart from a speech from RBA Jacobs, Head of Domestic Markets Department – Australia’s Bond Market in a Volatile World – at the Australian Government Fixed Income Forum, Tokyo.

AUSSIE BONDS: AU-US 10Y Diff Sits Near Bottom Of Range

The AU-US 10-year cash yield differential currently stands at -20bps, positioned near the bottom of the +/- 30bps range that has largely held since November 2022.

- A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past year suggests the current spread is slightly below fair value at -18bps.

- The 1Y3M differential, a key gauge of expected relative policy trajectories over the next 12 months, has traded within a 40bp range this year and is currently near the bottom of the range at ~-35bps.

- In early February, the 1Y3M differential had declined approximately 100bps since mid-September 2024, falling from +60bps to -40bps.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: MNI - Market News / Bloomberg

BONDS: NZGBS: Closed With A Twist-Flattener Ahead Of US CPI

NZGBs closed showing a twist-flattener, with yields 2bps higher to 1bp lower.

- Bloomberg - "New Zealand's annual net immigration fell to 21,317 in April, a two-and-a-half-year low, which could slow the country's economic recovery and lead to more interest-rate cuts."

- "The decline in net immigration is partly driven by New Zealand citizens leaving the country to seek better incomes, which could dampen demand and prompt the Reserve Bank to provide policy stimulus."

- Cash US tsys are little changed in today's Asia-Pac session ahead of today's CPI data.

- Focus has also been firmly on US-China trade talks, with headlines from London crossing earlier. The market reaction has been fairly muted, with the main outcome being agreement to move forward with what was agreed at the Geneva talks in May (although both US and Chinese leaders need to sign off on implementation).

- Swap rates closed showing a flatter curve, with yields 2bps higher to 2bps lower.

- RBNZ dated OIS pricing closed firmer across meetings. 4bps of easing is priced for July, with a cumulative 27bps by November 2025.

- Tomorrow, the local calendar will see Card Spending data, ahead of BusinessNZ Manufacturing PMI on Friday.

FOREX: Asia FX Wrap - Quiet Session Ahead Of US CPI

The BBDXY has had a range of 1209.44 - 1212.04 in the Asia-Pac session, it is currently trading around 1211.”With weaker data eroding the UK’s relative yield advantage and the Federal Reserve clinging to its higher-for-longer script, GBP/USD now faces a more challenging landscape. The pound has rallied nearly 8% year-to-date against the dollar, but the backdrop may be shifting”(BBG). PPG Macro on X: “UK (un)employment. HMRC PAYE employees total for May fell 109k. Even allowing for revisions, payrolled employment has fallen for 7 months in a row. 6-month average fall of 41.7k. The equivalent of nonfarm payrolls falling at over 200k a month.”

- EUR/USD - Asian range 1.1406 - 1.1439, Asia is currently trading 1.1415. EUR has drifted down during the Asian session in response to the move lower in US stocks. Dips should continue to find demand, first support around 1.1350 then the 1.1100/1200 area.

- GBP/USD - Asian range 1.3475 - 1.3510, Asia is currently dealing around 1.3485. The GBP looks to be failing in its attempt to gain any momentum above the pivotal 1.3500 weekly pivot. Poor data yesterday capped the move, support seen back towards 1.3400 and then 1.3200.

- USD/CNH - Asian range 7.1823 - 7.1897, the USD/CNY fix printed 7.1815. Asia is currently dealing around 7.1865. Sellers should be around on bounces while price holds below the 7.2500 area.

- Cross asset : SPX -0.29%, Gold $3340, US 10-Year 4.47%, BBDXY 1211, Crude oil $64.95

Data/Events : US CPI

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - USD/JPY Doing Work Around The 145.00 Interest

The Asia-Pac USD/JPY range has been 144.66 - 145.16, Asia is currently trading around 145.00. USD/JPY has had a muted session trading around some decent Option interest in the 145.00 area.

- Japan's May PPI was below market expectations, falling 0.2% m/m (against a +0.2% forecast). April's rise was revised to +0.3% (from 0.2%). In y/y terms, we printed 3.2%, against a 3.5% forecast (prior was 4.1%). In terms of the detail, manufacturing PPI was down 0.4%m/m. Weakness was evident in commodities, particularly petroleum, coal (-4.8%m/m). Iron ore and steel were also down in m/m terms. Import prices for commodities were down 1.1%m/m, continuing a negative trend, now off 10.3% in y/y terms.

- (Dow Jones) - “October may be the last chance for the Bank of Japan to raise interest rates, says Norinchukin Research Institute economist Takeshi Minami. Consumer inflation is expected to slow in the summer and slip below 2% after the start of 2026, he says.”

- Some large option interest around these levels has seen it do some work around 145.00.

- The market still seems very confident of a move lower in USD/JPY but with positioning quite large now we have seen the risk of pullbacks increase.

- With the failure to break below 142.00 last week, price is back in its recent 142.00 - 147.00 range and will need a break either side of that to get a clearer direction. US CPI tonight will dictate price action. Expiries below show a lot of interest around the 145.00 area.

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($1.14bm). Upcoming Close Strikes : 143.00($1.28b June 12), 140.00($1.22b June 12), 145.00($4.54b June 16).

CFTC data shows Asset managers maintained their already extensive JPY longs, and leveraged funds try again to build their own longs.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

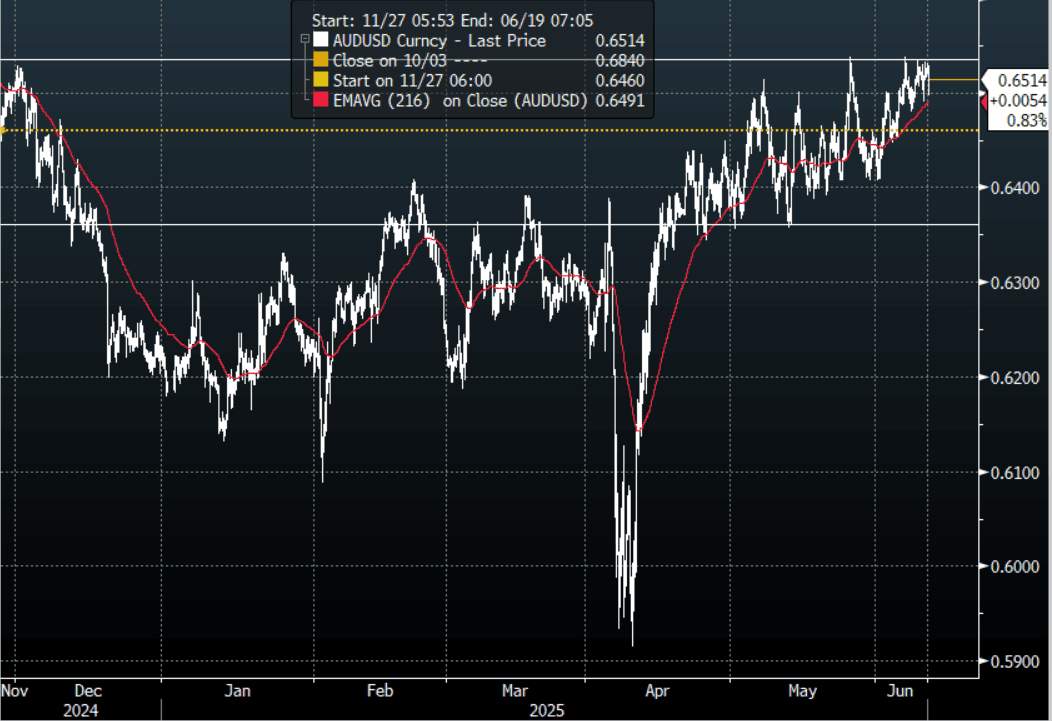

AUD: Asia Wrap - AUD/USD Drifts Lower Into US CPI

The AUD/USD has had a range of 0.6497 - 0.6532 in the Asia- Pac session, it is currently trading around 0.6515. The AUD has drifted lower for most of our session as US stocks fail to push on after positive headlines on the conclusion of the US-China talks. Another failure to get back above 0.6550, CPI tonight will determine if it gets tested again.

- AUS Bond Auction: ACGB Nov-32 Auction Goes Smoothly But With Less Demand: Today's auction reflected solid pricing for ACGBs, with the weighted average yield coming in 0.65bps below prevailing mid-yields, according to Yieldbroker.

- The AUD continues to see demand back towards the 0.6500 area, but the inability to break above 0.6550 on multiple occasions will have any bulls a little concerned.

- Price remains in the 0.6350 - 0.6550 range, a sustained break above 0.6550 is needed for the move higher to accelerate. Price looks like it wants to test the top end of the range, tonight's US CPI print will have a say in that.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6350 is needed to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6495(AUD400m), 0.6365(AUD550m). Upcoming Close Strikes : 0.6350(AUD 711m June 12), 0.6600(AUD643m June 12)

- CFTC Data shows Asset managers maintaining their shorts, the Leveraged community though continued to add to their shorts again.

AUD/JPY - Today's range 94.20 - 94.75, it is trading currently around 94.35. Price broke the multiple tops around the 94.00 area over NFP’s. It has since managed to hold these gains, while this continues focus will turn to the high towards 96.00. Support should now be back towards the 93.00/50 area.

Fig 1: AUD/USD spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

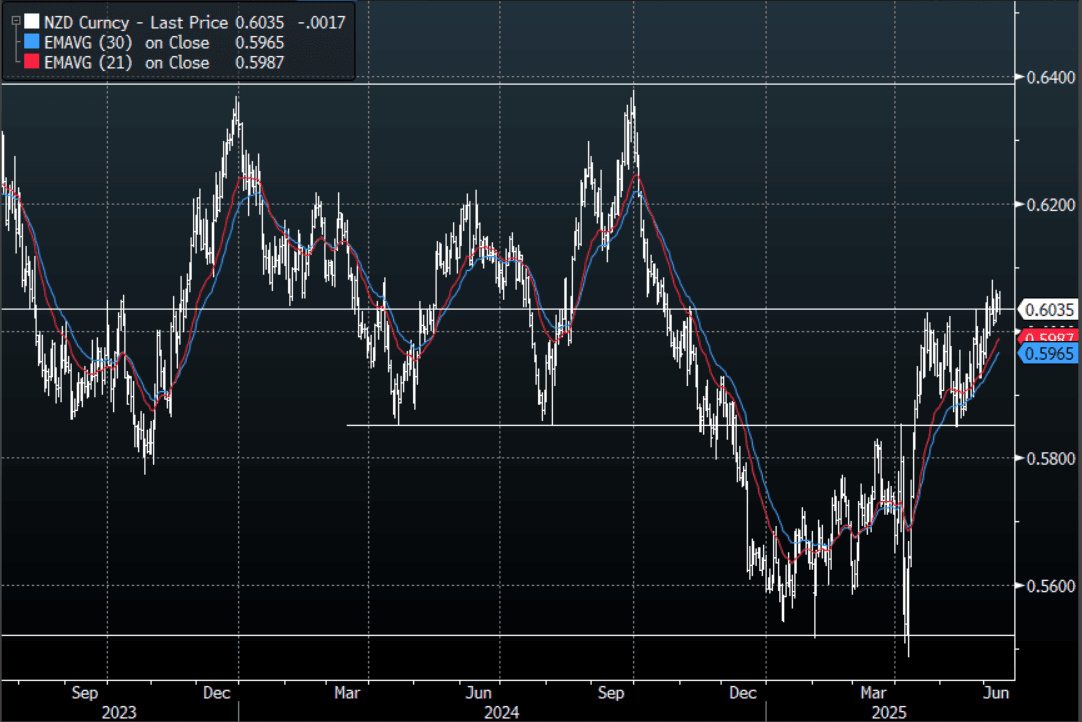

NZD: Asia Wrap - Drifts Lower, Holds Above 0.6000

The NZD/USD had a range of 0.6025 - 0.6062 in the Asia-Pac session, going into the London open trading around 0.6035. The NZD has drifted lower for most of our session as US stocks fail to push on after positive headlines on the conclusion of the US-China talks. The NZD has looked to be building for an extension higher, CPI tonight will determine if this can come to pass.

- Bloomberg - “New Zealand's annual net immigration fell to 21,317 in April, a two-and-a-half year low, which could slow the country's economic recovery and lead to more interest-rate cuts.”

- “The decline in net immigration is partly driven by New Zealand citizens leaving the country to seek better incomes, which could dampen demand and prompt the Reserve Bank to provide policy stimulus.”

- The NZD continues to find demand back towards the 0.6000 area as dips remain well supported, bulls will be hoping this holds to have another crack at extending higher.

- The support back towards 0.5850 has held very well, and while this continues to hold expect buyers to be around on dips. A clear break above 0.6050/0.6100 could provide the spark for the next leg higher. The market remains short and above here they could be forced to pare back.

- CFTC Data showed Asset managers maintaining their shorts, while the leverage actually added to their shorts last week.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6100(NZD353m), 0.6145(NZD348m). Upcoming Close Strikes : none

AUD/NZD range for the session has been 1.0769 - 1.0793, currently trading 1.0790. A top looks in place now just above 1.0900, the cross topped out on Monday towards the 1.0800/25 sell area, the first target looks to be around 1.0650.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Regional Gains Amid Trade War Hope

China's major bourses were among the regional leaders today as news filtered in on positive steps from the US China discussions. The KOSPI followed suit hitting highest since the end of 2021 led by chip makers hopeful of a trade resolution. Hong Kong listed China Rare Earth surged over 12% on the hope that trade tensions could ease.

- The Hang Seng led the way for the major Chinese bourses, erasing yesterday's losses to be up +0.95%. The CSI 300 followed suit rising +0.82%, the Shanghai Comp +0.54% and the Shenzhen Comp +0.72%.

- The KOSPI is in fast approaching the 3,000 mark at 2,898 and rose +0.94% today, following yesterday's gains of +0.56%

- The FTSE Malay KLCI is up +0.49% more than erasing yesterday's losses.

- The Jakarta Composite's gains of +1.65% yesterday were forgotten today as it fell -0.40%.

- The FTSE Straits Times fell -0.54% whilst the PSEi in the Philippines rose +0.45%

- The NIFTY 50 has eked out modest gains this morning of +0.20% and is on its sixth consecutive day of positive results.

ASIA STOCKS: Large Inflows for Taiwan as TAIEX Surges

Large inflows across major markets as the TAIEX gained over 2% yesterday.

- South Korea: Recorded inflows of +$466m yesterday, bringing the 5-day total to +$3,104m. 2025 to date flows are -$8,273. The 5-day average is +$621m, the 20-day average is +$189m and the 100-day average of -$86m.

- Taiwan: Had inflows of +$1,490m as yesterday, with total inflows of +$2007 m over the past 5 days. YTD flows are negative at -$11,121. The 5-day average is +$401m, the 20-day average of +$137m and the 100-day average of -$105m.

- India: Had inflows of +$282m as of the 9th, with total inflows of +$237m over the past 5 days. YTD flows are negative -$10,538m. The 5-day average is +$47m, the 20-day average of +$17m and the 100-day average of -$100m.

- Indonesia: Had inflows of +$63m yesterday, with total outflows of -$225m over the prior five days. YTD flows are negative -$2,951m. The 5-day average is -$45m, the 20-day average +$5m and the 100-day average -$29m.

- Thailand: Recorded inflows of +$44m as of yesterday, outflows totaling -$35m over the past 5 days. YTD flows are negative at -$2,128m. The 5-day average is -$7m, the 20-day average of -$28m and the 100-day average of -$22m.

- Malaysia: Recorded outflows of -$19m as of yesterday, totaling -$90m over the past 5 days. YTD flows are negative at -$3,542m. The 5-day average is -$13m, the 20-day average of -$13m and the 100-day average of -$24m.

- Philippines: Saw outflows of -$9m yesterday, with net outflows of -$11m over the past 5 days. YTD flows are negative at -$526m. The 5-day average is -$2m, the 20-day average of -$15m the 100-day average of -$5m.

OIL: Crude Little Changed As Waits For Upcoming US CPI Data

Oil prices are moderately lower during today’s APAC trading having already priced in some optimism on the outcome of US-China trade talks this week. Commerce Secretary Lutnick said that the Geneva Consensus was agreed to but it is now up to both presidents to agree to its implementation which could also allow further talks to occur. The focus had been on easing export controls.

- Oil prices fell slightly on Tuesday as the market became impatient waiting for a US-China announcement. They are slightly down again today ahead of US CPI data but off their intraday lows with WTI -0.1% to $64.93/bbl after a trough of $64.60, while Brent is -0.1% to $66.78/bbl following a fall to $66.47. The USD index is up 0.1%.

- The EU is putting together a new package of sanctions including a sharp reduction in the G7 price cap for Russia’s oil exports as its drone attacks on Ukrainian cities have escalated. There had been hope that a ceasefire may have enabled sanctions to be eased.

- Bloomberg reported that US oil inventories fell around 400k barrels last week, according to people familiar with the API data. Product stocks were higher with gasoline up 3mn and distillate 3.7mn. The official EIA data is out Wednesday including gasoline demand.

- Later US May CPI prints and is expected to show a 0.1pp pickup in both core and headline to 2.4% y/y and 2.9% y/y. It will be monitored for signs of any tariff impact. The US May federal budget is also released. ECB’s Lagarde, Lane, Cipollone and Buch appear today.

GOLD: Firmer, But Tracking Within Recent Ranges

Gold has ticked higher in the first part of Wednesday trade, last near $3341-42/oz, up around 0.50% versus end Tuesday levels in the US. This comes despite an uptick in the USD, with the BBDXY index around 0.1% stronger so far today. Focus has been firmly on US-China trade talks, with headlines from London crossing earlier. The market reaction has been fairly muted, with the main outcome being agreement to move forward with what was agreed at the Geneva talks in May (although both US and China leaders need to sign off on implementation).

- US equity futures have edged down, with the market perhaps looking for something more around broader tariff relief. This may be helping gold at the margins, although most regional equity markets in Asia Pac are firmer in Tuesday trade.

- For gold techs, the bullish theme remains intact with moving-average studies staying in a bull mode. Initial resistance is at $3403.5, 5 June high with the bull trigger at $3500.1. Initial support is at $3242.4, 50-day EMA.

SOUTH KOREA: Market Update Post Election

- The newly elected Lee Jae-myung named economic growth as his top priority, immediately boosting stock market sentiment. The strong market rebound leading up to the election reflects investors' hope after a six-month leadership vacuum.

- The markets since election day however have been mixed as much driven by the positivity built in leading up to the election and eyes on discussions between China and the US, yet positivity still remains

- The KOSPI has gained +4.36% in the time since the election result to be at 2,889.76 today.

- The Won has done little from 1,363 on election day to 1,370 today.

- The 3yr government bond is +1bp in yield whereas the 10yr is lower by -6bps.

- Lee promised a 5,000 target for the KOSPI and the market awaits sign of 'market friendly' policies

- Lee will need to prioritize the Corporate Value UP program. The South Korean Corporate Value-up Program, launched by the Financial Services Commission (FSC) in February 2024, aims to improve corporate governance and market practices to boost shareholder value. It focuses on enhancing transparency, aligning the interests of controlling and minority shareholders, and incentivizing companies to adopt higher governance standards. The program encourages voluntary disclosure and communication of value enhancement plans by listed companies.

- Foreign investors have held long concerns as to corporate governance in Korea. The revision of the Commercial Act 382 is a priority. Article 382 of the South Korean Commercial Act primarily deals with the duty of care and fiduciary duty of corporate directors. Focusing on the duty of loyalty, stating that directors must perform their duties in good faith and for the benefit of the company. Recent discussions and proposed amendments aim to expand this duty to include protecting the interests of shareholders a move that would be welcomed by foreign investors.

ASIA FX: CNH Steady Despite Trade Headlines, USD/KRW Supported On Dips

In North East Asia FX markets, CNH is little changed, despite seemingly positive US-China trade headlines. USD/KRW has been supported on dips, while TWD has outperformed. USD/HKD remains close to the top end of the peg band.

- USD/CNH spot hasn't spent too much time out of the 7.1850/7.1900 range so far in Wednesday trade. We had earlier US-China trade headlines, where the main take away was an agreement to implement the consensus from the Geneva talks (in May), subject to approval to leaders in both the US and China. China equities have recouped Tuesday losses, but are sub May highs.

- Spot USD/KRW sunk to the low 1360 region not long after the onshore, as local equities rallied over 1%. President Lee visiting the Korea Exchange today raised optimism around positive corporate governance news. Equities sit just off highs, but USD/KRW has rebounded back above 1370, threatening a downtrend channel, which has been in play since April this year. NPS reportedly no longer selling USD to hedge offshore investments has impact sentiment in the won space over the past 24 hours.

- Spot USD/TWD is holding at 29.90 in latest dealings, down marginally for the session. Taiwan equities have been buoyed by continuing strong momentum for tech bellwether TSMC, which is also aiding fresh inflows from offshore investors. For USD/TWD, earlier June lows rest close to 29.85.

- Spot USD/HKD remains supported, last near 7.8490.

MALAYSIA: Country Wrap: Industrial Production Up +2.6% in April

- Malaysia's Industrial Production in April expanded +2.7% YoY missing estimates yet remains above the 3-year average. The market had expected an improvement on March's +3.2% result. Mining was the biggest drag on the performance, contracting over the month by -6.3%. Manufacturing however was very strong up +5.6% versus +4.0% in March. The BNM next meets on July 09 with some domestic investors suggesting that the probability of a rate cut is growing. (source MNI Market News)

- Trade between Malaysia and Taiwan is up 38% YoY making it Malaysia's fourth largest trading partner. (source BERNAMA)

- The FTSE Malay KLCI is up +0.49% more than erasing yesterday's losses.

- The ringgit was modestly down at 4.2413 in a quiet day of trading.

- Bonds were steady with the MGS 10YR at 3.55%

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 11/06/2025 | 0630/0730 | BOE Saporta Speech At Bank of Finland and SUERF Conference | ||

| 11/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 11/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 11/06/2025 | 0930/1130 | ECB Lane At 2025 Government Borrowers Forum | ||

| 11/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 11/06/2025 | 1130/1230 | Chancellor Reeves presents Spending Review to Parliament | ||

| 11/06/2025 | - | *** | Money Supply | |

| 11/06/2025 | - | *** | New Loans | |

| 11/06/2025 | - | *** | Social Financing | |

| 11/06/2025 | 1200/1400 | ECB Cipollone On Digital Payments Panel | ||

| 11/06/2025 | 1230/0830 | * | Building Permits | |

| 11/06/2025 | 1230/0830 | *** | CPI | |

| 11/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 11/06/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/06/2025 | 1800/1400 | ** | Treasury Budget | |

| 12/06/2025 | 0600/0700 | ** | UK Monthly GDP | |

| 12/06/2025 | 0600/0700 | ** | Trade Balance | |

| 12/06/2025 | 0600/0700 | ** | Index of Services | |

| 12/06/2025 | 0600/0700 | *** | Index of Production | |

| 12/06/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 12/06/2025 | 0900/1100 | ECB Schnabel Visits "House of the Euro" | ||

| 12/06/2025 | 1200/1400 | ECB de Guindos At Financial Integration Conference | ||

| 12/06/2025 | 1220/1420 | ECB Schnabel At Financial Integration Conference | ||

| 12/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 12/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 12/06/2025 | 1230/0830 | * | Household debt-to-income | |

| 12/06/2025 | 1230/0830 | *** | PPI |