MNI EUROPEAN MARKETS: FX Safe Havens Underperform

- Risk appetite remained on a firmer footing, particularly in the equity space. Tariff/trade deal hopes continues to be the focus point, with BBG reporting today China is considering lower tariffs on some US imports. This added positive momentum to the risk on theme.

- Safe havens have underperformed in the FX space, with USD/JPY rising to fresh highs for the week. Cash US tsys are dealing ~1bp richer in today's Asia session after reversing the slight cheapening earlier.

- On the data front, Tokyo CPI printed above expectations, but didn't impact yen sentiment.

- Later on, we get UK retail sales, Canadian retail sales also print. In the US focus will be on the final U. of Mich. sentiment reading for April.

MARKETS

US TSYS: Yields Edge Lower As Trade-Deal Optimism Sustains Risk-On Mood

TYM5 is trading at 111-07, unchanged from closing levels in today's Asia-Pac session.

- According to MNI's technicals team, the next resistance to watch for TYM5 is at 111-25, 50.0% of the Apr 7 - 11 bear leg sell-off. Clearance of this level would undermine the bearish theme.

- Cash US tsys are dealing ~1bp richer in today's Asia session after reversing the slight cheapening earlier. Yesterday, US tsys saw a solid session, led by the belly. The 5-year yield is 0.9bp lower today at 3.925%, after dropping by 9bps yesterday.

- US tsys found support on Thursday from comments by Cleveland Fed's Hammack, who noted the Fed could act as soon as June if incoming data proves "convincing." Meanwhile, Fed Governor Waller expressed concern over the potential drag of tariffs on economic growth, suggesting their inflationary impact would likely be transitory.

- Yesterday’s risk-on sentiment sparked by trade "negotiations" headlines with India and South Korea has extended into today’s Asia session. US equity futures are ~0.5% higher.

- “Any u-turn on tariffs by the Trump administration would help market sentiment, Kelvin Tay, regional CIO for UBS Global Wealth Management, says in an interview on Bloomberg TV.” (per BBG)

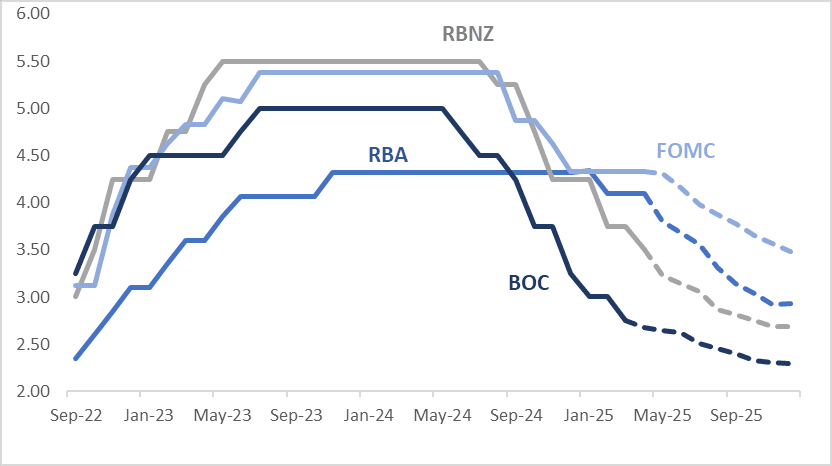

STIR: $-Bloc Markets Broadly Unchanged Over Past Two Weeks

Rate expectations across the $-bloc have remained broadly unchanged through December 2025 over the past two holiday-affected weeks.

- This stability comes despite a series of key economic releases—including CPI, employment data, central bank meetings, and meeting minutes—across most $-bloc economies.

- The muted reaction underscores how market focus remains firmly on headlines surrounding US–China trade tensions, with macroeconomic data taking a back seat.

- Looking ahead, the next major policy event in the $-bloc is the Fed's May 7 meeting, with markets currently pricing in just an 8% chance of a rate cut.

- Looking ahead to December 2025, the projected official rates and cumulative easing across the $-bloc are as follows: US (FOMC): 3.47%, -86bps; Canada (BOC): 2.29%, -46bps; Australia (RBA): 2.93%, -117bps; and New Zealand (RBNZ): 2.69%, -81bps.

Figure 1: $-Bloc STIR (%)

Source: MNI – Market News / Bloomberg

JGBS: Modest Bear-Steepener, BoJ Policy Decision Next Week

JGB futures are holding weaker, -29 compared to the settlement levels, following higher than expected Tokyo CPI for April, across all measures.

- Next week the BoJ meets, with little changed expected, but today's reading should still add to further tightening expectations for this year (particularly signs of further services related inflation).

- BoJ Governor Ueda hinted as much in earlier remarks, although tariff uncertainty continues to leave a cloud over the outlook.

- “Governor Kazuo Ueda will emphasize that the central bank will continue to raise rates as underlying inflation approaches its 2% target, which will help to strengthen the yen. The BoJ's quarterly report will likely show lower growth and inflation forecasts, but the key message that underlying inflation is approaching 2% will remain unchanged.” (per BBG Economics)

- Cash US tsys are dealing ~1bp richer in today's Asia session after reversing the slight cheapening earlier. Yesterday, US tsys saw a solid session, led by the belly. The 5-year yield is 0.9bp lower today at 3.925%, after dropping by 9bps yesterday.

- Cash JGBs are 1-3bps cheaper across benchmarks, with a steepening bias.

- Swap rates are 2-4bps higher, with the belly leading. Swap spreads are wider.

- On Monday, the local calendar will see Industrial Production and Capacity Utilisation data alongside 20-year supply.

JAPAN DATA: Tokyo CPI Above Forecasts, Positive Signs For Services Inflation

Tokyo April CPI came in stronger across the board relative to market expectations. Headline printed 3.5%y/y versus 3.3% forecast and 2.9% prior. The ex fresh food measure was 3.4%y/y, (3.2% was forecast and prior 2.4%), while the ex fresh food, energy measure rose to 3.1%y/y (forecasts were at 2.8%, prior 2.2%).

- Base effects looked to have played a role in terms of the y/y bounce, given April prints last year were sub 2%y/y across all of these measures. Still, it does signal further progress in terms of moving towards achieving the 2% inflation target sustainably, see the chart below

- The m/m outcomes for April were all at the same pace as March or firmer, except for goods, which rose just 0.1%. Services though rose 0.3%m/m in seasonally adjusted terms for the second straight month.

- The measure which excludes all food and energy prices rose 0.7%m/m (non-seasonally adjusted) and is back to 2% in y/y terms, from 1.1% in March.

- Looking at the break down by sub-category, food fell 0.4%m/m (led by fresh food down 5.9%), while medical care eased -0.1%m/m. All other sub-categories were positive in the month. Utilities rose 3.3%m/m, entertainment up 1.7% and education 1.4%. Household goods were +1.5% as well.

- Some of these strong m/m gains (education and utilities etc) may not be repeated, but the underlying trends still appear positive across most sub-categories.

- Next week the BoJ meets, with little changed expected, but today's reading should still add to further tightening expectations for this year (particularly signs of further services related inflation). BoJ Governor Ueda hinted as much in earlier remarks, although tariff uncertainty continues to leave a cloud over the outlook.

Fig 1: Tokyo CPI Bounces Strongly In April

Source: MNI - Market News/Bloomberg

FOREX: USD Outperforms Safe Havens, With Up Equities On Tariff/Trade Hopes

The USD BBDXY index has risen in the first part of Friday trade, up 0.30%, last near 1228. We are just of recent highs and a further extension higher could see the 1234/1235 region targeted. Safe havens are underperforming today, with yen down 0.70% and to fresh lows for the week versus the USD. The dollar is benefiting from a firmer US equity futures backdrop, amid hopes of tariff de-escalation.

- US Eminis are up close to 0.45% in latest dealings, near 5535/40, earlier we made fresh highs in the index back to early April. Positive trade talk headlines from Thursday in the US around potential deals with India and positive groundwork for US- South Korea discussions has been cited, while today BBG reported that China is considering lowering tariffs on some US imports to combat rising costs. Regional Asia Pac equities are all a sea of green, with tech related countries outperforming.

- Risk sentiment remains very sensitive to any potentially positive tariff/trade related developments. US Tsy yields are little changed so far today.

- USD/JPY got to 143.80, but sits slightly lower now, last 143.60, still off 0.70% in yen terms for the session. Note the 20-day EMA rests at 144.76, in terms of further upside targets. Earlier we had a solid beat from the Tokyo April CPI, but this didn't benefit yen.

- USD/CHF is back above 0.8300, off 0.60% in CHF terms, while EUR/USD is down to 1.1330, off 0.50%.

- AUD/USD is relatively steady, last near 0.6405/10. Liquidity may be lighter today given Australian markets are out for ANZAC day. Still, the A$ is being aided by the better equity tone. NZD/USD is down slightly, last near 0.5980/85 (NZ markets are also out).

- Later on we UK retail sales, Canadian retail sales print. In the US focus will be on the final U. of Mich. sentiment reading for April.

ASIA STOCKS: Sentiment Receives Further Support On China Tariff Headlines

Major Asia Pac indices were already tracking firmer following higher US markets, but received a further boost in latest trade on BBG headlines that China is weighing exempting some US imports from tariffs to temper rising costs (see this link).

- This followed some positive tariff related news on Thursday, albeit still without concrete details on what trade deals/new tariff levels look like - first on second hand media comments that the White House is "nearing an agreement in principle on trade with India" according to a Fox reporter, followed by Tsy Sec Bessent on a trade "understanding" with South Korea was near as well.

- The market is running with these positives, which along with the China news above, (which is under consideration and reportedly not enacted yet) continues to show market sensitivity to tariff related developments.

- Eminis were last up +0.50%, close to 5535/40, with earlier highs at 5543 best levels since early April. An earnings beat from Alphabet, late on Thursday in the US, also helped sentiment. Nasdaq futures are outperforming up around +0.60%.

- The HSI is up +1.45%, and above 22200, just shy of session highs. China mainland bourses are also up, but still with a low beta with respect to broader risk shifts.

- Japan's Topix is up +1.5%, while the NKY 225 is slightly outperforming. The yen is modestly softer so far today, while government support details to combat the tariff impact are expected to be released. South Korea's Kospi is up close to 1%, with Donald Trump Jr to visit South Korea next week, along with the US Navy Secretary (which could benefit local shipbuilders depending on the outcome of the trip). The Taiex is +2.2%, the strongest performer so far today.

- Australian and New Zealand markets are closed today for ANZAC day.

- In SEA markets, Philippine stocks are up +1.8%, the Thailand index is up over +1.1%, with other markets more muted in terms of gains.

OIL: Higher, But Still Lower For The Week, Bearish Technicals Intact

Brent crude last tracked near $67/bbl, up a modest 0.60% in Friday trade so far. WTI was close to $63.15/bbl, with both benchmarks supported by the better risk tone seen so far today. The positive spill over from better equity sentiment in the region is a positive, with markets hopeful of tariff de-escalation over the coming weeks as trade negotiations continue

- Still, compared to levels at the end of last week, oil is still of around 1.5% for Brent, while WTI is still down nearly 2.4%.

- Crude was up on Thursday, after declines on Wednesday following uncertainty around Kazakhstan’s commitment to OPEC+ targets, potential June OPEC+ output increases, and ongoing US-Iran nuclear talks.

- Also note, oil prices may see further downside this year on rising production and with demand limited by China’s faltering growth, according to the IEA Executive Director Fatih Birol, cited by Bloomberg.

- A bearish theme in WTI futures remains intact and the recovery since Apr 9 is - for now - considered corrective.

- A resumption of the bear cycle would open $53.72, a Fibonacci projection. Resistance to watch is $65.84, the 50-day EMA.

- Oil prices may see further downside this year on rising production and with demand limited by China’s faltering growth, according to the IEA Executive Director Fatih Birol, cited by Bloomberg.

GOLD: Slightly Weaker After Yesterday’s Solid Rebound

Gold is 0.4% lower in today’s Asia-Pac session, after rebounding by 1.5% yesterday. This left the yellow metal broadly unchanged on the week but still more than 4.5% below Tuesday’s all-time high.

- The trend needle in gold continues to point north and this week’s fresh cycle high reinforces bullish conditions, according to MNI technicals team. Moving average studies are unchanged and remain in a bull-mode position highlighting a dominant uptrend. The next objective is $3,547.9, a Fibonacci projection. Initial firm support to watch lies at 3,207.8, the 20-day EMA.

- It has been a volatile week for bullion, with investors assessing trade tensions and the possibility of US rate cuts. Lower rates are typically positive for gold, which doesn’t pay interest.

- Yesterday, Fed Governor Christopher Waller said he’d support monetary easing if the job market deteriorated due to the trade war. In a similar vein, Fed President Beth Hammack told CNBC policy makers may cut rates as early as June.

ASIA FX: USD/Asia Pairs Mixed, PHP Outperforms

USD/Asia pairs are mixed to end the week. Focus remains on tariff/trade developments. Earlier BBG headlines that China was considering exempting some of the goods it imports from the US (due to rising costs) has aided what was already a positive risk mood. Regional equities, outside of India, are all in the green today.

- USD/CNH is lower, last near 7.2840, with some positive CNH momentum since the tariff headlines crossed earlier. The pair remains within recent ranges though, with recent lows at 7.2765. Downside focus may rest at the 200-day EMA (close to 7.2530). CNH is clearly outperforming safe havens like JPY and CHF as equity sentiment continues to improve. CNH/JPY was last back close to 19.72, up a further 0.80% today.

- Spot USD/KRW is little changed, the pair last near 1433/34, down from Thursday highs above 1440. The won hasn't seen much benefit against the USD from the turnaround in equity market sentiment, but like CNH is benefiting on crosses. JPY/KRW is back under 10.00.

- USD/INR continues see support ahead of the 85.00 level, we were last 85.35/40, slightly weaker in INR terms for the session. Indian equities are struggling in the first part of Friday trade, down around 1% for the Nifty. The +12% rally from early April lows may be driving some near term caution in sentiment. Offshore investors have been strong buyers of local equities so far this week.

- USD/IDR is down modestly but at 16820 remains within recent ranges.

- PHP is outperforming, USD/PHP was last near 56.30/35, 0.40% firmer in PHP terms. This puts the pair at fresh lows back to Oct of last year. A chunky +$5bn local bond sale may be helping the FX, while local equities are also up strongly, last +1.85%. For USD/PHP the next downside target is likely to be the 56.00 figure level.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 25/04/2025 | 0600/0700 | *** | Retail Sales | |

| 25/04/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 25/04/2025 | 1230/0830 | ** | Retail Trade | |

| 25/04/2025 | 1230/0830 | ** | Retail Trade | |

| 25/04/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 25/04/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 25/04/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 25/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 25/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 25/04/2025 | 1915/2015 | BOE's Greene on Inflation, growth and moentary policy | ||

| 25/04/2025 | 2000/1600 | Kevin Warsh |