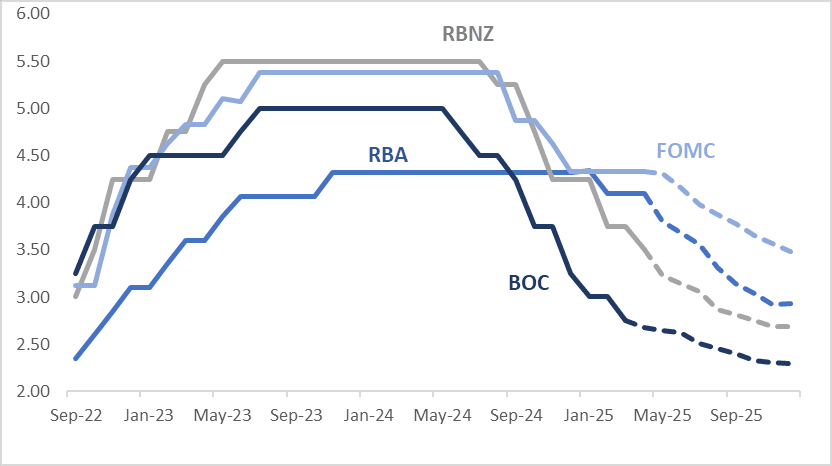

STIR: $-Bloc Markets Broadly Unchanged Over Past Two Weeks

Rate expectations across the $-bloc have remained broadly unchanged through December 2025 over the past two holiday-affected weeks.

- This stability comes despite a series of key economic releases—including CPI, employment data, central bank meetings, and meeting minutes—across most $-bloc economies.

- The muted reaction underscores how market focus remains firmly on headlines surrounding US–China trade tensions, with macroeconomic data taking a back seat.

- Looking ahead, the next major policy event in the $-bloc is the Fed's May 7 meeting, with markets currently pricing in just an 8% chance of a rate cut.

- Looking ahead to December 2025, the projected official rates and cumulative easing across the $-bloc are as follows: US (FOMC): 3.47%, -86bps; Canada (BOC): 2.29%, -46bps; Australia (RBA): 2.93%, -117bps; and New Zealand (RBNZ): 2.69%, -81bps.

Figure 1: $-Bloc STIR (%)

Source: MNI – Market News / Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: AUDUSD Bounces As Equities Rally

AUDUSD’s reaction to the lower-than-expected February CPI print was very brief and the pair has been driven by US dollar moves since. It fell to 0.6278 as the greenback rallied and then turned higher with stronger risk appetite and is now down slightly to 0.6301 today. It appears to be finding support from stronger domestic and HK equities. The USD index is slightly higher and off today’s peak.

- Given headline CPI continues to be impacted by various state and federal electricity rebates, the focus is on the underlying trimmed mean which moderated 0.1pp to 2.7% y/y in February, third straight month under 3%. February services inflation also suggests it moderated in Q1.

- AUDNZD tested 1.1000 again but couldn’t hold the move and the pair is now down 0.1% to 1.0986. Aussie is also 0.1% lower against the euro and pound at 0.5835 and 0.4867 respectively.

- AUDJPY fell to 94.26 but has bounced back to be slightly higher today at 94.54, close to the intraday high at 94.64.

- Equities are rallying with the ASX up 0.8%, Hang Seng +0.7% and S&P e-mini +0.1%. Oil prices are moderately higher again with WTI +0.5% to $69.37/bbl. Copper is up 1.7% and iron ore continues to trade around $102/t.

- Later the Fed’s Kashkari and Musalem appear and preliminary US February durable goods data print. The ECB’s Cipollone participates in a panel and UK February CPI and the government budget are released.

US: Trump Details On Reciprocal Tariff Exemptions Remain Light

US President Trump is being interviewed on Newsmax, with headlines filtering out on reciprocal tariffs.

- "“I don’t want to have too many exceptions,” for the tariffs scheduled to take effect on Apr. 2, President Donald Trump said in an interview on Newsmax. (per BBG). “I’ll probably be more lenient than reciprocal, because if I was reciprocal, that would be that would be very tough for people”

- This doesn't shed much light on exceptions/exemptions, which follows earlier comments this week from Trump around the issue. Markets were supported by Trump comments around exceptions on reciprocal tariffs.

JGBS: Little Changed After PPI Services & Gov Ueda Comments

In Tokyo morning trade, JGB futures are slightly weaker, -5 compared to settlement levels, after giving up an overnight uptick.

- The Feb Japan PPI services rose 3.0%y/y, against a 3.1% market forecast and 3.2% prior print from Jan (which was initially reported as a 3.1% rise). In m/m terms the services PPI was flat, while BBG notes the 3 month annualized paced slowed to 1.0% in Feb. This metric was at 4.8% in Dec last year.

- “Overseas trade policies and the impact on global price trends are among factors that have added to uncertainties for Japan’s economy, BoJ Governor Ueda says. The long-held belief that prices and wages won’t rise is starting to fade, Ueda says in a semi-annual report to parliament. Sees both upside and downside risks for prices, with the underlying price trend still below the bank’s 2% target.” (per BBG)

- Cash US tsys are ~2bps cheaper in today's Asia-Pac session after yesterday's modest gains. Wednesday's focus is on Durables/Cap Goods, Tsy 5Y Sale and Fed Speak from MN Fed Kashkari Fed and StL Fed Musalem.

- Cash JGBs are little changed across benchmarks. The benchmark 10-year yield is unchanged at 1.583% after reaching a fresh cycle high of 1.587%.

- Swap rates are little changed.