MNI EUROPEAN MARKETS ANALYSIS: Waiting for the FED

- Most regional bourses are positive Monday ahead of a major week for financial markets. With the FED reserve decision later this week, the weak 3Q Japan GDP was seemingly overlooked as tech and AI stocks demand remains strong with Samsung and TSMC leading.

- Bonds were subdued for most markets across the region with US Treasuries starting the day strongly, only to give back earlier gains to be flat on the day.

- The USD has traded slightly softer in the Asian session with most regional currencies posting gains. The Rupiah, Rupee and Peso weakened today bucking the regional trend.

- Third quarter GDP in Japan declined -0.6% QoQ as capex and public spending lagged, whilst private consumption was revised up.

- Looking ahead there is Industrial Production from Germany, NY Fed survey of consumer expectations and BOE's Taylor & Lombardelli speak.

MARKETS

US TSYS: Bonds Give Back Early Gains

US bond futures gave back earlier gains to be near where they started in the afternoon session. The US 10-Yr is flat at 112-17+ near to the 100-day EMA of 112-15. Topside resistance is the 50-day EMA of 112-26.

Cash has trended back to relatively unchanged across the curve having been lower in yields earlier.

- The 2-Yr is at 3.563%

- The 5-Yr is at 3.713%

- The 10-Yr is at 4.137%

- The 30-Yr is at 4.793%

There are no Tier 1 data releases tonight with markets looking ahead to the JOLTs Job Openings for October

Ahead tonight is a 13 and 26 week bill auction, with the focus being the U$58bn 3-Year auction.

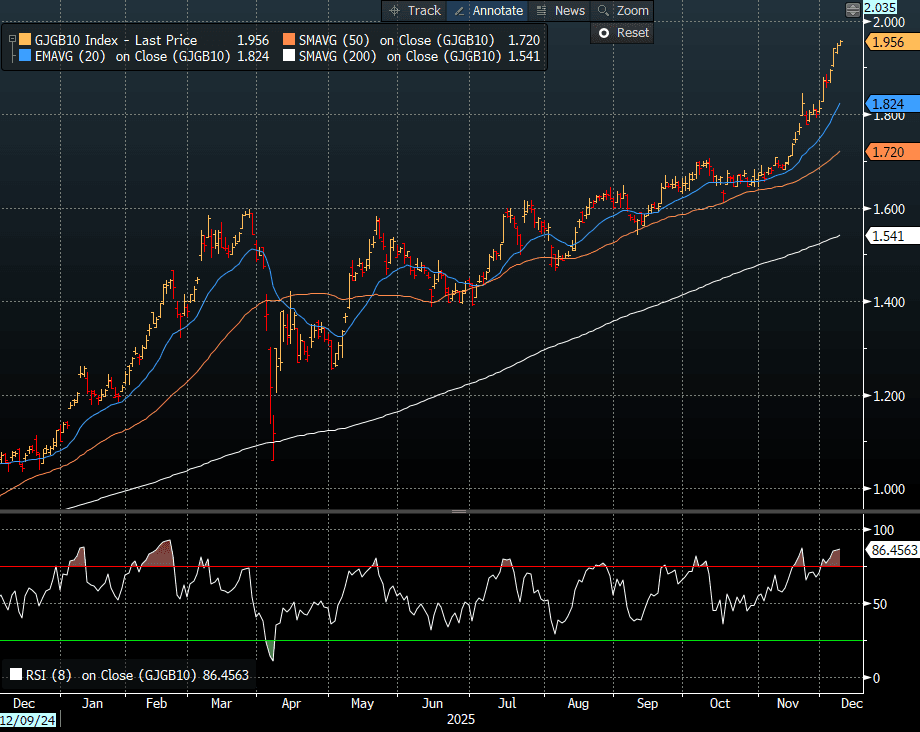

JGBS: Mostly Cheaper With 10YY A Fresh Cycle High ut A Subdued Session

JGB futures are slightly weaker, -3 compared to settlement levels, after a relatively subdued session.

- MNI Techs Team - Futures prices traded to new pullback and cycle lows again Friday, weighed by building expectations of a December BoJ rate hike and a breach of support in futures prices. This affirms the firm downtrend that's dominated prices since mid-September, and prices will need to challenge resistance before signalling any broader reversal. Key short-term resistance has been defined at 137.30, the Sep 8 high.

- MNI - Japan's Q3 GDP fell 0.6% q/q, or an annualised -2.3%, compared with the initial estimate of -0.4% q/q, or -1.8% annualised, as capital investment and public spending were revised down, although private consumption was revised slightly higher. Private consumption, which accounts for about 60% of Japan's GDP, was revised up to 0.2% from 0.1%, though its contribution remained unchanged at 0.1 pp.

- Cash US tsys are little changed in today's Asia-Pac session after Friday's modest sell-off.

- Cash JGBs are 2.5bps cheaper (20-year) to 0.5bp richer (40-year) across benchmarks, with the 10-year yield 1.0bp higher at 1.958%, a fresh cycle high.

- Swap rates are 1-3bps higher, with a steeper curve.

- Tomorrow, the local calendar will see Money Stock and Machine Tool Orders data alongside 5-year supply.

Source: Bloomberg Finance LP

MNI POLICY: BOJ Unshaken By JGB Volatility

MNI EXCLUSIVE: The BoJ & JGB Yields

MNI discusses the BOJ's stance on recent JGB yield moves.

On MNI Policy MainWire now, for more details please contact sales@marketnews.com

MNI BRIEF: Japan Nov Sentiments Post 1st Drop In 7 Months

Japan’s Economy Watchers sentiment index fell for the first time in seven months in November, with the outlook index for two to three months ahead also posting its first decline in seven months, although the government kept its overall assessment unchanged, data from the Cabinet Office showed Monday.

Indexes covering households, the labour market and businesses all weakened. The current conditions index declined to a seasonally adjusted 48.7 in November from 49.1 in October, while the outlook index dropped 2.8 points to 50.3 from 53.1.

The government said the economy is recovering and, despite concerns over rising prices, the recovery is likely to continue.

A Cabinet Office official told reporters that higher material costs due to the weak yen were weighing on corporate sentiment, while households continued to face elevated living costs. He added that comments expressing concern about the future impact of the weak yen were increasing.

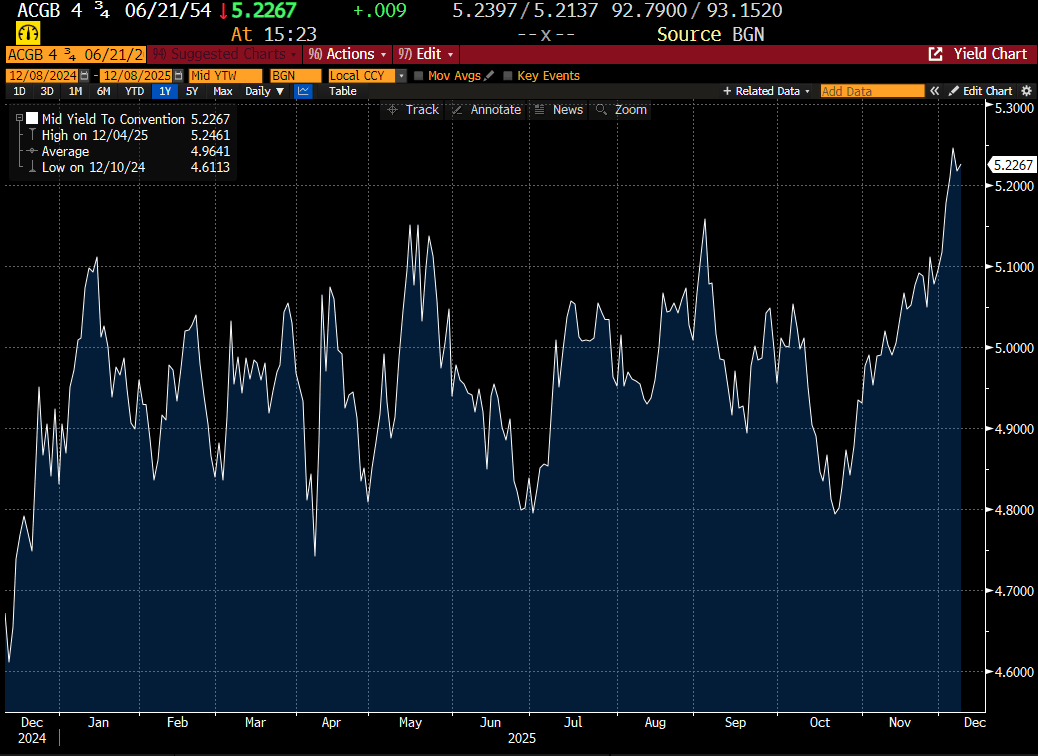

AUSSIE BONDS: Weaker But Subdued Day Ahead Of Tomorrow's RBA Policy Decision

ACGBs (YM -2.5 & XM -2.0) remain weaker after dealing in relatively narrow ranges in today’s session.

- Cash US tsys are slightly richer in today's Asia-Pac session after Friday's modest sell-off.

- Cash ACGBs are 2-3bps cheaper with the AU-US 10-year yield differential at +57bps.

- Today’s Jun-54 auction delivered the weighted average yield 0.81bps through prevailing mids. Moreover, demand strengthened, as reflected by a cover ratio of 3.4333x, up from 2.8500x from the previous auction. The stronger demand came with the outright yield at a fresh cycle high, 20bps higher than the previous auction (see chart).

- The bills strip has bear-flattened across contracts.

- Tomorrow, the local calendar will see NAB Business Confidence ahead of the RBA Policy Decision. Thursday’s November jobs data will also be important this week.

- The RBA is unanimously expected to leave rates at 3.6% with the market pricing in no chance of a move in either direction. Therefore, the statement will be scrutinized to gauge the Board’s thinking regarding the outlook and especially if there is a change to the balance of risks and a shift to concern about upside ones to inflation after the October trimmed mean printed at 3.3%.

- The AOFM plans to sell A$1000mn of the 1.00% 21 December 2030 bond on Wednesday.

Bloomberg Finance LP

RBA: MNI RBA Preview-Dec 2025: On Hold, Could Be A Hawkish Shift?

- Download Full Report Here

- With October trimmed mean inflation printing at 3.3%, the RBA is unanimously expected to be on hold at its December meeting.

- The strength of the data since the November meeting plus inflation rising further above the top of the band increases the chance that the RBA now sees risks skewed to the upside and as a result it may sound more hawkish and at a minimum will remain “cautious”.

- RBA-dated OIS pricing is showing the probability of a 25bp hike rising from 2% tomorrow to 105% by August and 141% by December 2026.

- With core inflation rising over H2 2025 and stronger demand increasing upside risks, future rate decisions will be even more data dependent to give clarity to the outlook. November CPI is released 7 January & Q4/December 28 January ahead of the next RBA meeting on 4 February. At this stage policy is likely to be unchanged then too.

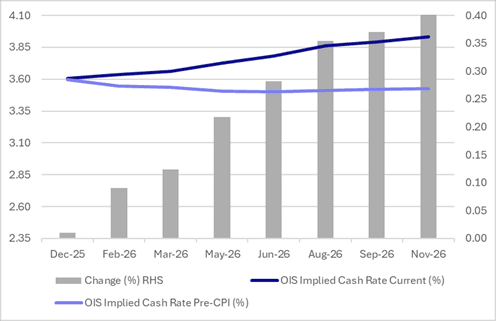

STIR: RBA-Dated OIS Pricing Fully Prices Hike By August 2026

RBA-dated OIS pricing is slightly firmer today, showing tightening across all meetings, with the probability of a 25bp hike rising from 2% tomorrow to 105% by August and 141% by December 2026.

- After today’s move, pricing is 9-40bps firmer across the curve beyond December 2025, than pre-Monthly CPI levels (26 November), led by December 2026.

Figure 1: RBA-Dated OIS – Current Vs. Pre-CPI Monthly

Source: Bloomberg Finance LP / MNI

BONDS: NZGBS: Heavy Session Outright & Relatively Vs $-Bloc

NZGBs closed 5-10bps cheaper, led by the 5-year. Accordingly, NZGBs sit amazingly 18-38bps higher than pre-RBNZ levels. (see chart)

- On a relative value basis, the 5-year swap is at its cheapest valuation since mid-2022, based on the 2-/5-/10-year butterfly spread.

- Versus the $-bloc, NZGBs also underperformed sharply, with the NZ-US and NZ-AU 10-year yield differential 5-6bps higher. At +30bps, NZ-US differential is back at April levels.

- Swap rates closed 10-13bps higher, with a steeper 2s10s curve.

- RBNZ-dated OIS pricing closed firmer across meetings. No easing is now priced for February, while November 2026 assigns 44bps of tightening.

- The local calendar was empty today and will remain so until Wednesday, when RBNZ Governor Breman hosts a media Q+A alongside Net Migration data.

- On Thursday, the NZ Treasury plans to sell NZ$175mn of the 4.50% May-30 bond, NZ$200mn of the 3.50% Apr-33 bond and NZ$75mn of the 5.00% May-54 bond.

Bloomberg Finance LP

FOREX: USD - BBDXY Testing 1210-1211 Again

The BBDXY has had a range today of 1210.91 - 1212.57 in the Asia-Pac session; it is currently trading around 1211, -0.10%. The USD has traded slightly softer in the Asian session. US yields extended their bounce last week and risk has consolidated its recent gains. The USD saw decent demand back toward the 1211 area at the back-end of last week and it looks like the range 1210-1230 could be here for the moment. On the day look for resistance again back towards the 1215-1217 area where sellers should remerge initially, support remains toward 1210/11 which needs to be worked through and then the more important 1205 area.

- EUR/USD - Asian range 1.1639-1.1655, Asia is currently trading 1.1655. The pair continues to consolidate around the 1.1650 area. On the day it looks like dips back toward 1.1580-1600 could be supported initially, looking to retest the 1.1680 area again eventually.

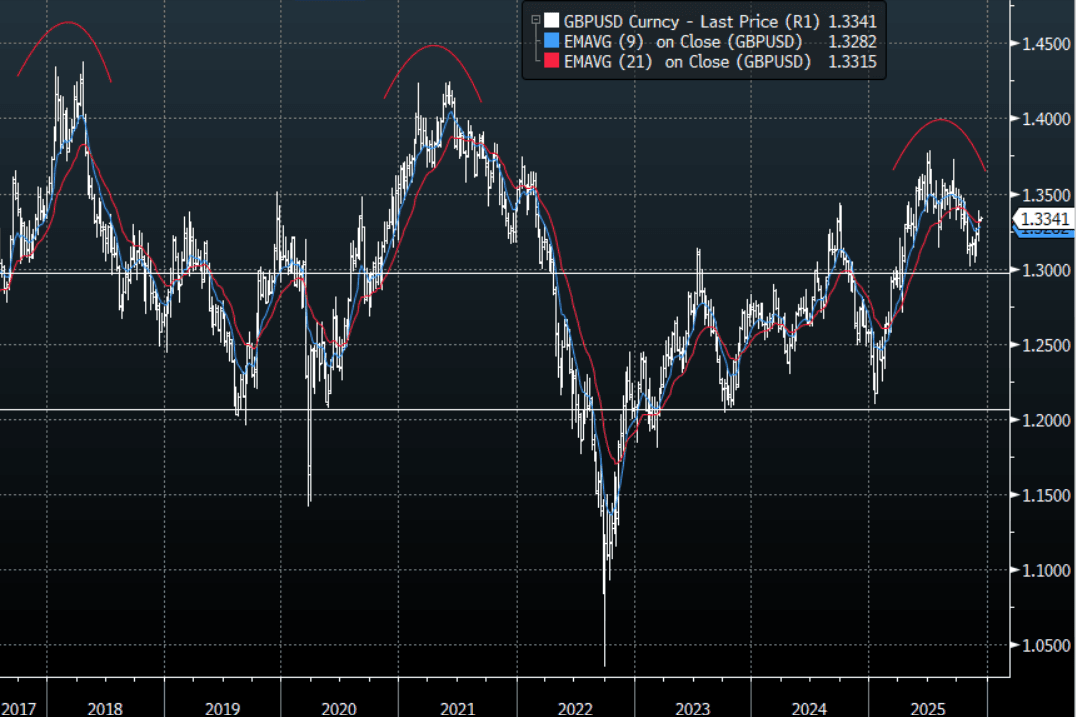

- GBP/USD - Asian range 1.3323-1.3342, Asia is currently dealing around 1.3340. The pair is consolidating on a 1.33 handle. I remain skewed toward shorts but patience is required and we are now approaching levels where I will be watching for any signs of potentially topping out. On the day GBP should see support back toward the 1.3260-1.3290 area, while above here look for the market to test the 1.3370-90 area again at some point.

- Cross asset : SPX +0.20%, Gold $4210, US 10-Year 4.133%, BBDXY 1211, Crude Oil $60.22

- Data/Events : EZ Sentix Investor Confidence, Germany Industrial Production SA

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

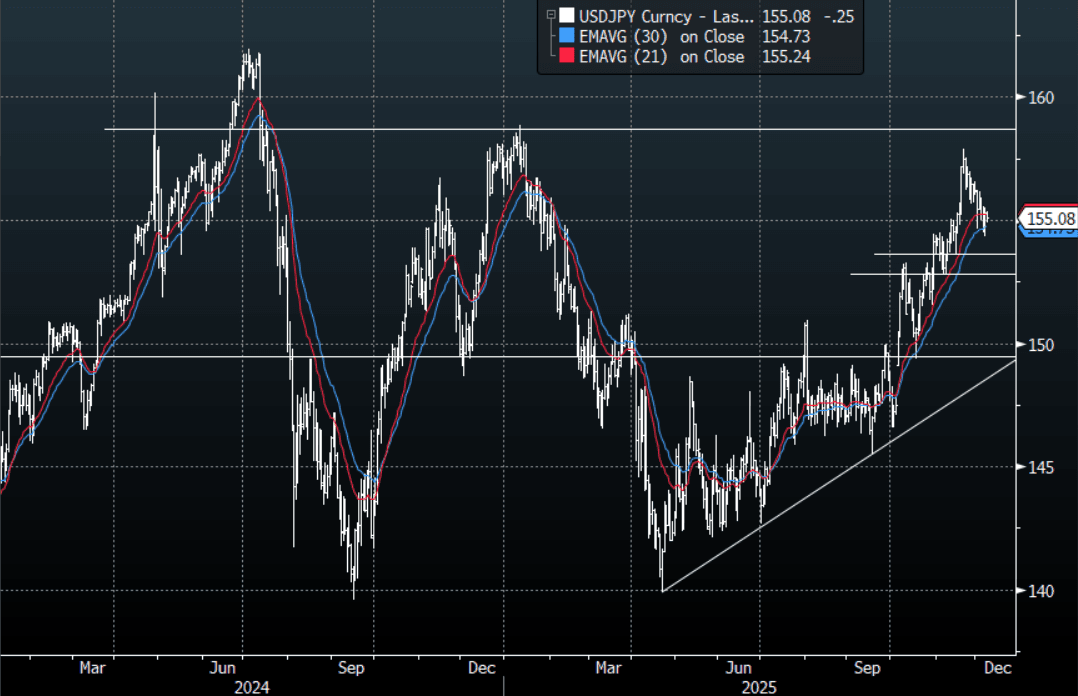

JPY: USD/JPY - Treads Water Around 154.50-155.00

The USD/JPY range today has been 154.90 - 155.38 in the Asia-Pac session, it is currently trading around 155.10, -0.15%. The pair has traded a little lower in a quiet start to the week. The market is pricing in the fact that the Yen move looks likely to force the BOJ into action in December. This has stalled the upward momentum and could keep it contained in the short-term but I suspect the market will still look for opportunities to express a long USD at the right levels. Technically USD/JPY is still in an uptrend with the first big support back toward the 153-155 area which should see buyers reemerge. In today's Asian session I suspect we will continue to consolidate within a wider 154.50-156.00 range. The FOMC later this week could be the catalyst to get this pair moving again as it could potentially be meaningful for the USD direction going into the year-end.

- MNI BRIEF: Japan's Q3 GDP Revised Down on Capex. Japan's Q3 GDP fell 0.6% q/q, or an annualised -2.3%, compared with the initial estimate of -0.4% q/q, or -1.8% annualised, as capital investment and public spending were revised down, although private consumption private consumption, which accounts for about 60% of Japan’s GDP, was revised up to 0.2% from 0.1%, though its contribution remained unchanged at 0.1 pp.

- Bloomberg - “Goldman strategists believe one BOJ rate hike won’t sustainably end yen underperformance. Investors are holding fast to the bearish wagers on the currency.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.00($1.33b), 156.00($1.49b). Upcoming Close Strikes : 155.00($877m Dec 11), 156.00($880m Dec 10), 156.00($1.24b Dec 11) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 93 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

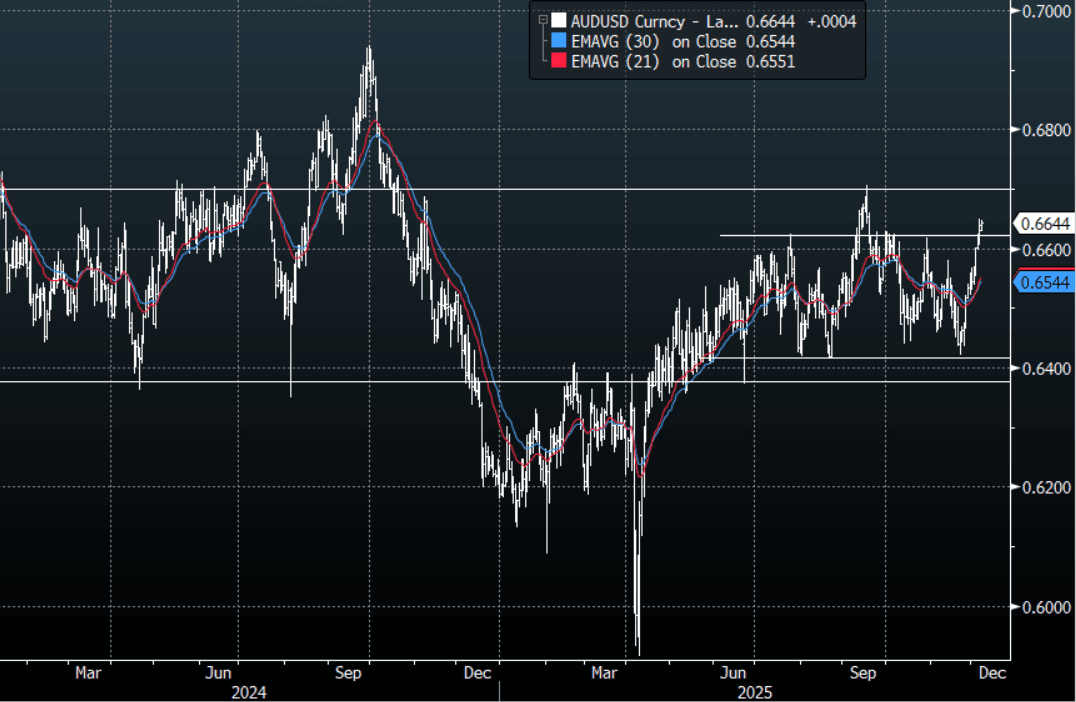

AUD/USD - Trying To Build On Break Above 0.6630

The AUD/USD has had a range today of 0.6631 - 0.6648 in the Asia- Pac session, it is currently trading around 0.6645, +0.10%. The AUD/USD is trying to build some momentum on its break above 0.6630. The AUD price action remains very constructive and indicative of a market with solid buying interest. While the AUD remains above 0.6500-0.6550 I suspect dips should continue to be supported. In the Asian session, look to see if the AUD can hold above this 0.6620/30 area. It has come a long way so if this does not hold we could see a pullback, first support below that is toward 0.6570/90 where we should see demand reappear. Ultimately the AUD is looking to rebuild momentum to have another look back toward the 0.6700 area at some point. RBA tomorrow and the FOMC later this week should dictate the upcoming price action.

- MNI AU - The focus of the week is on Tuesday’s RBA decision but Thursday’s November jobs data will also be important. The RBA is unanimously expected to leave rates at 3.6% with the market pricing in no chance of a move in either direction. Therefore, the statement will be scrutinised to gauge the Board’s thinking regarding the outlook and especially if there is a change to the balance of risks and a shift to concern about upside ones to inflation after October trimmed mean printed at 3.3%.

- “CHALMERS: TO DELIVER MID YEAR BUDGET OUTLOOK NEXT WEEK" : BBG

- MNI AU - RBA-dated OIS pricing is slightly firmer today, showing tightening across all meetings, with the probability of a 25bp hike rising from 2% tomorrow to 105% by August and 141% by December 2026.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6475(AUD814m), 0.6500(AUD342m). Upcoming Close Strikes : 0.6550(AUD1.59b Dec 11) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 35 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

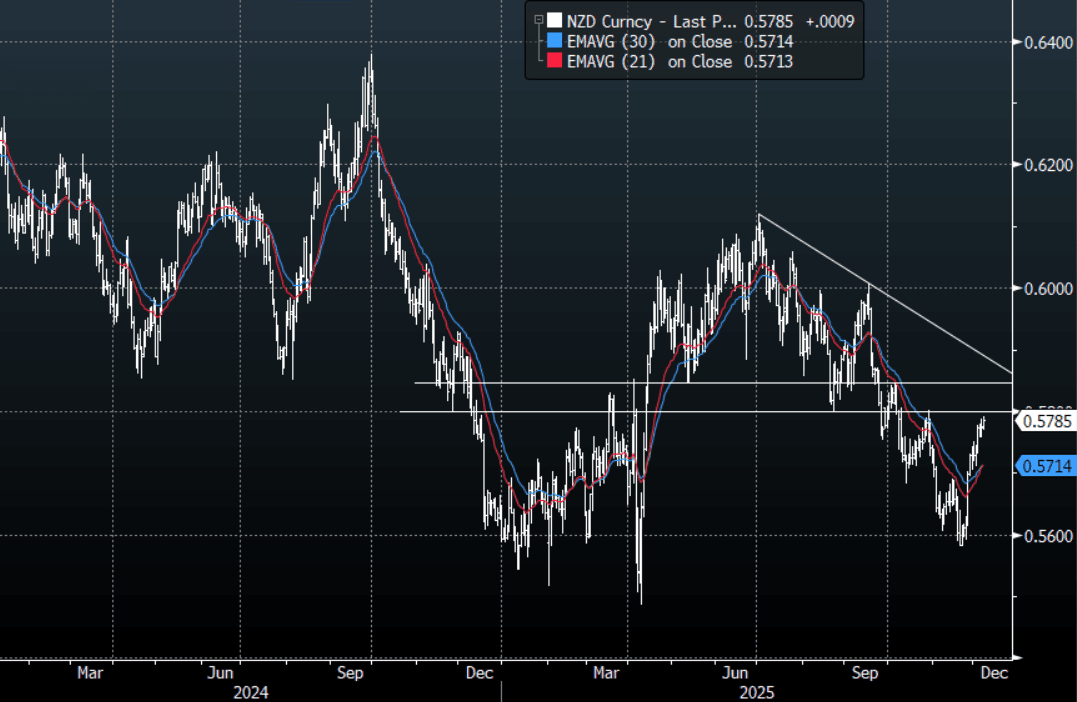

NZD/USD - Drifts Higher, Back Toward 0.5800

The NZD/USD had a range today of 0.5770-0.5791 in the Asia-Pac session, going into the London open trading around 0.5785, +0.15%. The NZD/USD has drifted higher having a look back outward the 0.5800 area in our session. On the day, look for support now back toward the 0.5735-0.5755 area as the focus turns back to the more important 0.5800-50 resistance where I suspect sellers could return initially. The FOMC this week will have important implications for the USD so the market will be gearing up for that event.

- MNI - This week is dominated by the FOMC decision, widely expected to deliver a third consecutive 25bp cut after NY Fed Williams' uncharacteristic guidance following the delayed September payrolls report. It's likely to be a contentious meeting, though, with many FOMC members preferring to pause.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5670(NZD382m), 0.5730(NZD767m). Upcoming Close Strikes : 0.5700(NZD557m Dec 10) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 34 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Markets Await FED as Japan Growth Stumbles

- Despite the worse than expected GDP, the NIKKEI has hovered around where it began the day at 50,478 above the 20-day EMA of 49,919

- The KOSPI is up again with key tech stocks like Samsung over up over +1.2% today, seeing the index up by +0.25% and the TAIEX rose +0.93% has TSMC jumped over 2% Monday.

- The onshore offshore divide was evident in China with the Hang Seng down heavily by -1.1%, whilst the CSI 300 rose by over 1%. Shenzhen is the outperformer on the day with gains of +1.3% with some tech stocks up strongly. The performance highlights a strong investor focus on technology and advanced manufacturing sectors, which have been a key growth area in the region

- The NIFTY 50 continues to moderate and is down -0.12% Monday. Since hitting new highs on NOV 27, the NIFTY has fallen five out of seven trading days though the losses have been contained. The NIFTY sits only 0.25% below the high of 26,215.

- SE Asia's bourses are led again by the Jakarta Composite which is up strongly by +0.95%, to reach overbought on the 14-day Relative Strength Index. It last reached overbought in August where it remained for several trading days. The FTSE Malay KLCI is down -0.55% and teh SE Thai -0.10%

OIL: Crude Holding Onto Gains As Watching Ukraine Developments

Oil prices are marginally higher as the market monitors Ukraine/Russia developments with negotiations ongoing, US President Trump criticizing Ukraine’s President Zelenskyy, Ukraine striking Russian refineries and Russia’s President Putin encouraging Indian oil purchases. Market expectations that there would be a peace deal faded over last week driving oil prices higher and they remain sensitive to events.

- WTI is up 0.2% to $60.21/bbl after falling to $59.97 with moves below $60 short-lived. It rose 2.7% last week. Brent is 0.2% higher at $63.88/bbl following a peak of $63.94 and a low at $63.63. It was up 2.4% last week.

- Both benchmarks have been in a very narrow range today as they wait for more information regarding geopolitical developments, including Venezuela, and monthly oil reports. Forecasts will be monitored closely for any upward revisions to 2026 surplus projections. The EIA short-term energy outlook is on Tuesday and OPEC & IEA reports on Thursday.

- Trump said that he was disappointed with how Zelenskyy has treated the latest US proposal and accused him of not reading it.

- The US and Ukraine agreed on a “framework for security arrangements” with “necessary deterrence capabilities to sustain a lasting peace”, according to the US State Department. However, Russia said that Trump’s National Security Strategy was “largely consistent” with Russia’s view.

- Ukraine struck Rosneft’s Ryazan refinery on the weekend in response to heavy attacks on its energy generation. This followed strikes late last week on Russia’s Syzran refinery and Temryuk port.

- Later US November NY Fed 1-yr inflation expectations and German October IP print. The ECB’s Cipollone and BoE’s Taylor & Lombardelli speak.

GOLD: Range Trading As Wait For Wednesday’s Fed Decision

Gold prices are slightly higher in Monday’s APAC trading supported by a lower US dollar (BBDXY -0.1%) but have moved in a very narrow range of $4195.60/4213.17. They are currently up 0.3% to $4211.8/oz. Bullion, like other assets, will probably remain in a narrow range ahead of the Fed decision on Wednesday. The market has 23bp of easing priced in but it could be a hawkish cut, which may weigh on gold.

- Silver is down 0.6% to $58.02 oz today, driven by profit taking, after rising 2.1% on Friday. It finished last week up 3.3% and has been hovering around overbought on a 14-day RSI basis, according to Bloomberg. It started today at a high of $58.789, just below initial resistance at $58.979. The metal remains in an uptrend supported by a resumption of ETF inflows.

- Gold continues to trade between initial resistance at $4264.7 and initial support at $4139.7, 20-day EMA. The bull trigger is at $4381.5.

- PBoC data for November showed a 30k troy oz rise in gold reserves, the thirteenth consecutive monthly increase.

- Equities are mixed with the S&P e-mini up 0.2% and CSI 300 +1.0% but Hang Seng down 1.1% and ASX -0.2%. Oil prices are little changed with WTI +0.2% to $60.23/bbl. Copper is down 0.3%.

- Later US November NY Fed 1-yr inflation expectations and German October IP print. The ECB’s Cipollone and BoE’s Taylor & Lombardelli speak.

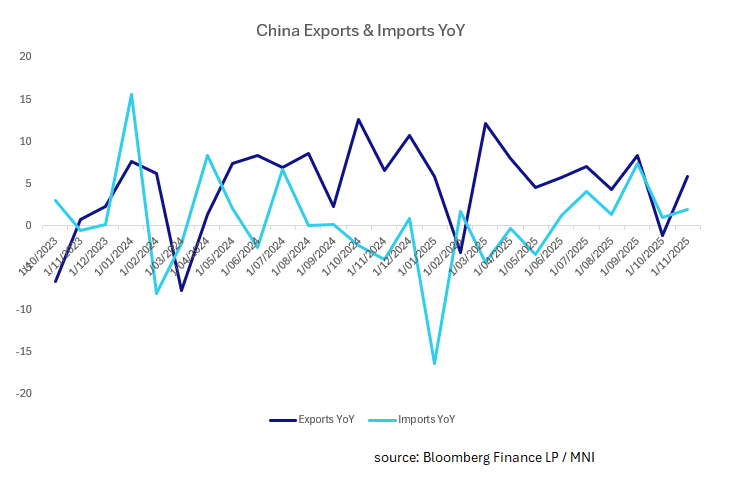

CHINA: November Exports Rebound, Trade Surplus $111bn

- After the sudden contraction in October, November exports rebounded strongly topping expectations.

- November exports expanded +5.9%, above estimates of +4.0% and beating October's result of -1.1%

- The decline in October is attributed to shipments being brought forward ahead of the Trump Xi meeting, shipments being front loaded ahead of the holiday period and base effect.

- Imports missed estimates with a rise of +1.9%, versus estimates of 3.0% and prior of 1.0%

- This left China with a trade balance ahead of estimates at US$111.6bn at a time when French President Emmanuel Macron warned that the European Union may be forced to take “strong measures” against China, including potential tariffs, if Beijing fails to address its widening trade imbalance with the bloc.

- Despite some signs of a softening in economic data, the strength in exports will remain highly supportive of China achieving it's stated 5% GDP growth for 2025 and likely dampen calls for further monetary policy stimulus in the near term.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 08/12/2025 | 0500/1400 | Economy Watchers Survey | ||

| 08/12/2025 | 0700/0800 | ** | Industrial Production | |

| 08/12/2025 | - | *** | Trade | |

| 08/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 08/12/2025 | 1500/1600 | ECB Cipollone Lecture at Frankfurt School of Finance & Management | ||

| 08/12/2025 | 1600/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 08/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 08/12/2025 | 1700/1700 | BOE Taylor Panel on Growth/Wealth/Debt | ||

| 08/12/2025 | 1800/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 08/12/2025 | 1830/1830 | BOE Lombardelli Panel on Women in Economics | ||

| 09/12/2025 | 0001/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 09/12/2025 | 0330/1430 | *** | RBA Rate Decision | |

| 09/12/2025 | 0700/0800 | ** | Trade Balance | |

| 09/12/2025 | 1000/1000 | * | Index Linked Gilt Outright Auction Result | |

| 09/12/2025 | 1100/0600 | ** | NFIB Small Business Optimism Index |