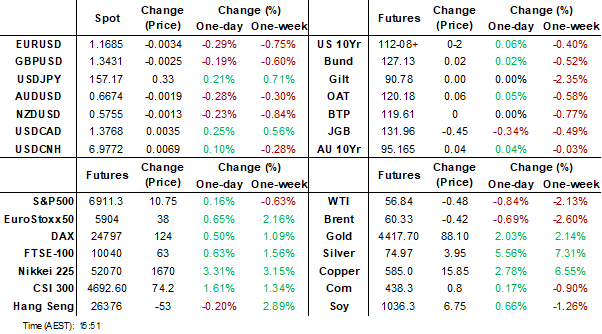

MNI EUROPEAN MARKETS ANALYSIS: USD Recovery Continues

- Oil prices fell around a percent on opening following the US’ removal of Venezuelan President Maduro, which in theory should allow for an easing of sanctions on its energy exports. Prices soon rebounded driven by significant uncertainty over Venezuela’s oil production capability, the situation in the country and stronger risk appetite in markets generally.

- The US ousting of Venezuelan dictator Maduro on the weekend has added to geopolitical uncertainty as it is unclear if the US will intervene in other countries, especially in South America, and what the outcome of current unrest in Iran could be. This appears to have driven an increase in safe haven flows in Monday’s APAC trading boosting precious metal prices. They have stabilised though in line with a stronger US dollar (BBDXY +0.3%).

- Later US December manufacturing ISM and UK November lending data are released.

MARKETS

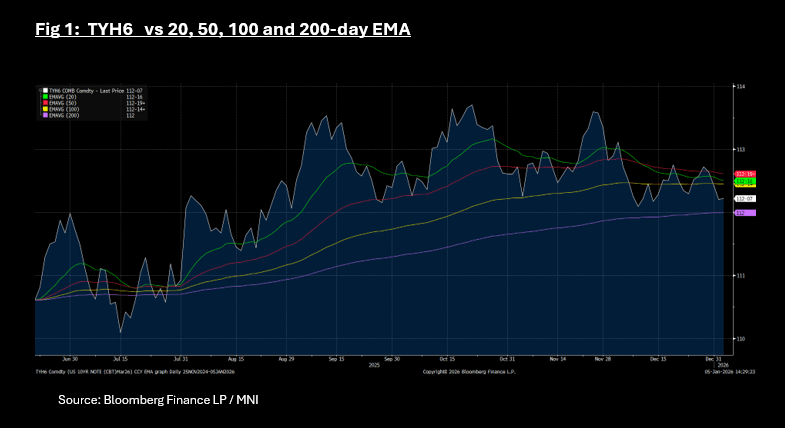

US TSYS: Cash Grinds Lower; TYH5 Wedged Between Key Tech Levels

US treasury futures have done nothing today with the 10-Yr up only marginally. At 112-07+ it remains wedged between the 100-day EMA as topside resistance and the downside resistance via the 200-day EMA of 112.

Cash is doing better with yields down -0.2bps to -0.9bps across the curve with the long end underperforming.

- The US 2-Yr is at 3.475% - flat today.

- The US 5-Yr is at 3.736%, down -0.9bps today.

- The US 10-yr is at 4.185%, down -0.6bps today.

- The US 30-Yr is at 4.869%, down -0.2bps.

Equity markets were key today but have seemingly brushed off the geopolitical risks, with strong rallies.

Whilst January is typically a busy month for issuance, Monday kicks off with just a US$86bn 13-week bill auction and a US$77bn 26-week bill auction.

Data wise ISM releases are the focus with the ISM Manufacturing forecast to remain in contraction and ISM Prices paid to remain elevated

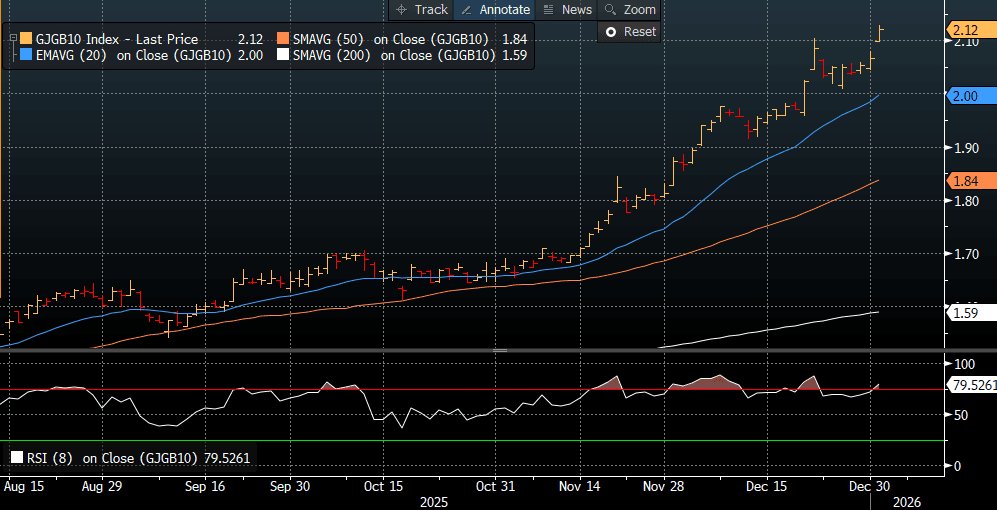

JGBS: Heavy Session, Led By 10Y, As Trading Resumes After NY Break

After the extended NY break, JGB futures are weaker and at a fresh cycle low, -44 compared to settlement levels

- Cash US tsys are ~1bp richer in today's Asia-Pac session after Friday's modest bear-steepener. Focus in the first two full weeks of the year will be on nonfarm payrolls (Friday) and CPI reports (Jan 13) for December, with those two key reports back on their original schedules having been prioritised by the BLS.

- Cash JGBs are 1-7bps cheaper across benchmarks, led by the futures-linked 7-year. The benchmark 10-year yield is 5.5bps higher at 2.121%, just shy of today's fresh cycle high.

- (Bloomberg) "Bank of Japan Governor Kazuo Ueda used his first public appearance in the new year to underscore his intention to keep raising the benchmark rate in a speech to private bankers. “We will keep raising rates in line with improvement in the economy and inflation,” Ueda said Monday in remarks at a New Year’s conference hosted by the Japanese Bankers Association. “The appropriate adjustment of monetary easing will lead to the achievement of stable inflation target and longer-term economic growth.”"

- Swap rates are 3-6bps higher, with a steepener curve.

- Tomorrow, the local calendar will see Monetary Base data along side 10-year supply.

Source: Bloomberg Finance LP

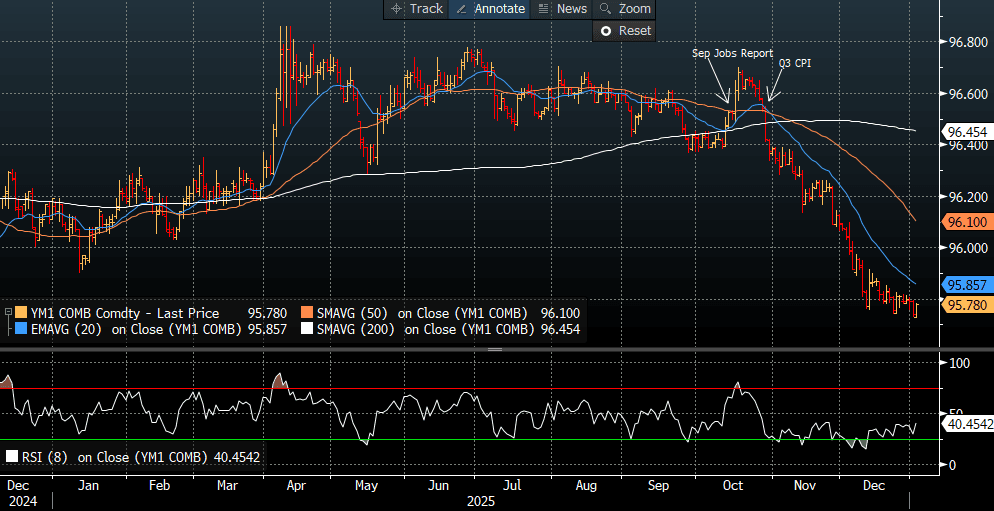

AUSSIE BONDS: Modestly Richer On A Relatively Subdued Data-Light Session

ACGBs (YM +4.0 & XM +2.5) are modestly stronger after a relatively subdued data-light session.

- The focus of this week will be Wednesday’s November CPI, which is the new complete monthly series. The new trimmed mean CPI appears less volatile than the incomplete series but printed 0.7pp higher at 2.8% y/y in June 2025, which was the recent trough. Q2 was at 2.7% y/y overall.

- Bloomberg consensus is forecasting trimmed mean to be stable at 3.3% in November, which would be at or above the top of the RBA’s 2-3% band for the fifth consecutive month. Headline is expected to moderate 0.2pp to 3.6% but this series continues to be distorted by previous government electricity rebates.

- Cash US tsys are slightly richer in today's Asia-Pac session after Friday's modest bear-steepener.

- Cash ACGBs are 2-4bps richer, with a steeper curve and the AU-US 10-year yield differential at +64bps.

- The bills strip is stronger, with pricing +2 to +4 across contracts.

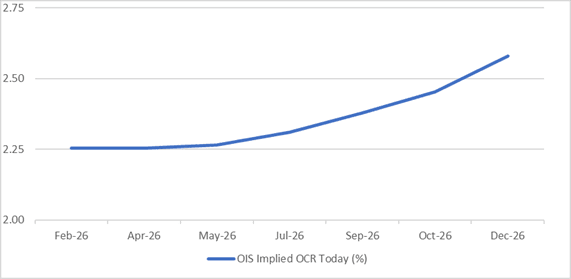

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 35% for February to 98% by June and 171% by December 2026.

- Tomorrow, the local calendar will see S&P Global PMIs: Composite & Services.

Bloomberg Finance LP

BONDS: NZGBS: Bear-Steepener On First Trading day Of Year

NZGBs closed showing a bear-steepener, with benchmark yields flat to 4bps higher, as trading resumed after the extended New Year’s break.

- The NZ-US 10-year yield differential closed at +35bps. For context, the differential was dealing around flat in mid-November.

- Cash US tsys are slightly richer in today's Asia-Pac session after Friday's modest bear-steepener. Focus in the first two full weeks of the year will be on nonfarm payrolls (Friday) and CPI reports (Jan 13) for December, with those two key reports back on their original schedules having been prioritized by the BLS. Private sector reports meanwhile are highlighted by ISM manufacturing and services reports Jan 5 and 7. No scheduled Fed speakers today.

- The local data calendar is very light this week, with just Dec Cotality home value figures out later this evening. Next week we get Nov filled jobs, along with food prices as well.

- RBNZ-dated OIS pricing closed slightly softer across meetings. No tightening is priced for February, while October 2026 assigns 20bps.

Bloomberg Finance LP / MNI

FOREX: Dollar Index Extends Recovery, Position Adjustments In Play?

The USD BBDXY index has extended its recovery, last around 1208, +0.30% versus end Friday levels. Mid to late Dec highs in the index were around 1210.4, but more important resistance is likely around the 1219 and higher region. 1219 marks the 200-day EMA resistance point, while the index couldn't sustain +1220 levels in Nov last year. Dollar gains started out against the higher beta plays in the first part of trade, as markets were risk averse after US weekend military action in Venezuela. However, modest gains for the likes of JPY and CHF proved short lived. The G10 is now down around 0.30% across the board with little differentiation for AUD, NZD versus the safe havens.

- Cross asset catalysts for today's USD bounce aren't obvious. Risk sentiment in the equity space is mostly positive with tech related plays in Asia outperforming. Precious metals, notably silver, continue to rally as well.

- US Tsy yields are little changed so far today, but the 10yr yield is holding close to 4.18%, just off Dec highs.

- One possibility is the paring of USD shorts built up late last year, with EUR and AUD leveraged longs notable in the CFTC update to Dec 23 (+40k for AUD, +.29k for EUR)

- Looking ahead US December manufacturing ISM is released.

FOREX: Early Risk Off Gives Way To Broader USD Gains, MXN Underperforms

USD gains have been fairly uniform against the G10 as Monday's Asia Pac session unfolded. Initial risk off drove AUD and NZD underperformance but this wasn't sustained. USD/JPY got to lows of 156.66, but now sits close to session highs, last 157.25/30, up around 0.30%. This keeps the recent uptrend intact, with upside focus likely to rest near the 158.00 (where we got to late last year post the Dec BoJ rate hike and where FX intervention rhetoric picked up from Japan officials).

- Despite the firmer US equity futures, and regional equity tone (albeit mainly focused in the tech/AI space), along with higher metal prices, the A$ has struggled to recovery ground. The pair was last around 0.6670/75. This is back close to the 20-day EMA support point, near 0.6660, which also coincides with recent lows. The 50-day EMA is further south near 0.6610.

- NZD/USD is off by a similar amount, last near 0.5750. This is close to recent lows in the pair around 0.5740, with a clean break lower potentially bringing 0.5700 back into focus.

- EUR/USD is softer as well, last 1.1680/85, levels last seen in the first half of Dec 2025. We are right around the 50-day EMA currently. GBP/USD is down 0.20% to 1.1325/30 right on the 20-day EMA support point.

- USD/MXN has risen close to 0.70%, up to 18.02/03. This keeps us close to highs from the second half of the Dec. Broader USD trends have aided the move, while remarks from US President Trump around needing to do something to curb drug flows from Mexico has likely weighed on sentiment as well. The weekend military action in Venezuela may leave the market not ruling out the possibility of US military action in Mexico to curb drug related activity.

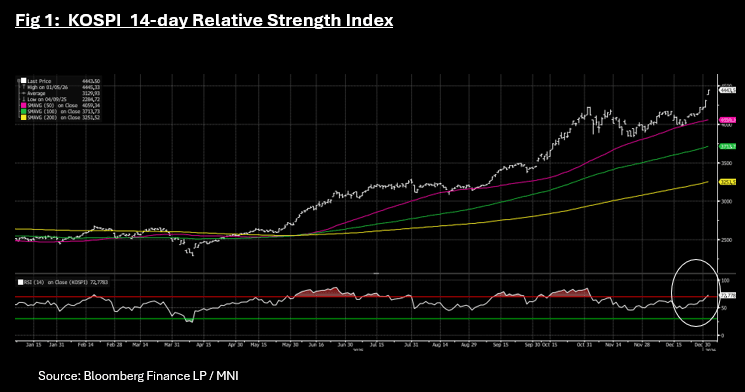

ASIA STOCKS: KOSPI Reaches Overbought as AI/Tech Rallies Again

The AI / tech rally continued today with key stocks like Samsung in Korea up +5.6%, TSMC in Taiwan +6.3% and Softbank in Tokyo +4% to help their respective bourses post strong gains. However the theme of China's key AI / tech stocks underperforming regional peers continues with Tencent in Hong Kong up just +0.15% today. Whilst the US ousting of Venezuela's president initially caused oil price volatility, Asian markets largely brushed off these tensions, maintaining their positivity throughout the day.

- The NIKKEI is gaining 3% today to 51,849 to be within 1% of the October high whilst the KOSPI jumped 3.10% to 4,442 and trend above the overbought line on the 14-day relative strength index. Joining in the AI / tech led party was the TAIEX which jumped +2.7% to a new high of 30,153 as it too reached overbought. There are growing calls from market observers as to the heated valuations from AI / tech stocks. SK Hynix in Korea for example is now up over 300% since its lows of April 2025.

- China's bourses were more subdued with the Hang Seng down -0.08% whilst the CSI 300 rose +1.5%, Shanghai +1.07% and Shenzhen +1.66%. For the Shanghai Comp, the rise above 4,000 to 4,011 brings the November high of 4,029 into its sights.

- SE Asia's major bourses all posted gains with the SE Thai outperforming following a much stronger than expected December PMI manufacturing. The SE Thai is up +1.7%, whilst the Jakarta Composite is up +0.65% and the FTSE Malay +0.34%

- India's NIFTY 50 continues to exhibit lower volatility relative to regional peers as it resets new highs. At 26,360 it remains up almost 20% from the March lows with gains of +0.15% Monday . The NIFTY 50 finished 2025 marginally below the 5-Year high of 23.50x, but is above the full year 2026 forecast. This suggests that from a valuation perspective, any near-term pressures on equities may not come from valuations though with the equity dividend yield at 1.26%, equity valuations relative to bonds look expensive.

OIL: Uncertainty Drives Minimal Change In Oil Prices

Oil prices fell around a percent on opening following the US’ removal of Venezuelan President Maduro, which in theory should allow for an easing of sanctions on its energy exports. Prices soon rebounded driven by significant uncertainty over Venezuela’s oil production capability, the situation in the country and stronger risk appetite in markets generally. At this stage markets don’t seem concerned that the action has set a destabilising precedent.

- WTI fell to $56.56/bbl on today’s open but soon began trending higher reaching $57.73. It is currently around $57.10 to be 0.4% down on the day. Brent declined to $60.00 before rising to $61.24 and is currently -0.2% at $60.61.

- With a record surplus widely projected for 2026, any extra Venezuelan supplies on global markets could add to current downward pressure on oil prices. OPEC’s decision on Sunday to stick with its plan of unchanged Q1 quotas should provide a short-term floor though.

- Venezuela’s oil producing region appears to have seen minimal impact from the weekend’s events. The US blockade had already caused a pause in production, which was not a major concern, as storage facilities filled.

- The industry needs significant investment after an extended period of neglect which will be a long process and so there is unlikely to be an increase in Venezuelan oil exacerbating the 2026 market surplus.

- Morgan Stanley expects global oil supply to peak in mid-2026 and so has cut its Brent forecasts for Q1, Q2 and Q3 with the trough at $55 in Q2, according to Bloomberg.

- Later US December manufacturing ISM and UK November lending data are released.

OIL: Venezuelan Oil Unlikely To Have Material Impact On Global Market

Venezuela is not a major player in the oil market despite having the largest known reserves, as years of sanctions and dictatorship have resulted in its crude production trending lower. The industry has been neglected and significant private investment will be needed to increase output as well as the lifting of sanctions. Low oil prices could discourage the needed capex. President Trump has said that the US needs full access to Venezuelan oil to rebuild the country.

- In the 1990s, Venezuela produced over 3mbd and OPEC reported that recently it was 1mbd which is above its 2020 trough. According to the IEA it was the 17th largest oil exporter globally and second in South America in 2023 as sanctions and a related-lack of investment in the sector drove output down 73% since 2000.

- Venezuela sells at a discount to benchmarks and most of its oil exports go to China.

- Even if it can return to producing 3mbd, Venezuela would still only be the 10th largest oil exporter and 15th largest producer, assuming other countries are unchanged.

PRECIOUS METALS: Venezuela Drives Safe Haven Flows Into Gold & Silver

The US ousting of Venezuelan dictator Maduro on the weekend has added to geopolitical uncertainty as it is unclear if the US will intervene in other countries, especially in South America, and what the outcome of current unrest in Iran could be. This appears to have driven an increase in safe haven flows in Monday’s APAC trading boosting precious metal prices. They have stabilised though in line with a stronger US dollar (BBDXY +0.3%).

- Gold is up 1.7% to $4405.7/oz after an intraday high of $4420.99. Silver is 3.6% higher at $75.44 after reaching $76.344.

- Currently Venezuela is being run by Rodriguez, a Maduro ally, and she has said that the country is ready to cooperate with the US. President Trump warned her against being obstructive and said that the US needs full access to Venezuela’s oil. Secretary of State Rubio said that it will take time to hold elections and that the US doesn’t have troops on the ground.

- Risks at this stage don’t appear to stem from Venezuela itself but what type of precedent the US action has set.

- Equities are generally stronger with the S&P e-mini up 0.1% and CSI 300 +1.6% but Hang Seng down 0.1%. Oil prices are lower with WTI -0.4% to $57.08/bbl. Copper is 2.9% higher.

- Later US December manufacturing ISM and UK November lending data are released.

INDONESIA: Headline Up But Core Stable, IDR May Continue To Keep BI On Hold

Headline inflation rose more than expected in December printing at 2.9% y/y up from 2.7% but in line with the October outcome. There was a pickup in both fresh food and administered price inflation. Core was stable at 2.4% y/y for the third straight month and below 2025’s high of 2.5%. Both measures remain well with Bank Indonesia’s 1.5-3.5% corridor but with USDIDR higher than the last meeting and BI’s focus returning to FX stability, it could again be on hold at its next decision on 21 January.

- USDIDR strengthened to around 16700 on 31 December but is trending higher again and today is at 16755.

- Base effects from 2025’s energy discounts will drop out of the year-on-year comparison in Q1 and will temporarily boost headline inflation at the start of this year.

- Volatile food inflation rose to 6.2% y/y in December up from 5.5% due to chilis, chickens, shallots and fresh fish.

- Personal items rose 13.3% y/y up from 12.5% driven by jewellery as global gold prices rose 5.6% m/m on average in December to be up 63.4% y/y. Higher petrol prices boosted the transport component to 1.2% y/y from 0.7%.

Indonesia CPI y/y%

CHINA: Weekly Preview: PPI and CPI Key, Equity Valuations Looking Stretched

Download Weekly Preview Here:

- The key data releases are the PPI and CPI which have been mired in or near to deflation for some time. Whilst PPI has remained in deflation since 2022, CPI has inched back positive in November and will be keenly watched this week.

- The CSI 300 ended the week with modest gains and in early January is at 5-Year highs for Price to Earnings. At 17.52x, it remains significantly above the 2026 forecast of 14.40x, suggesting downside risks could build. The dividend yield finished 2025 at 2.36% to remain a supportive factor from a valuation perspective, relative to bond yields.

- Despite this, investor sentiment remains in a weakening trend with the property sector woes continuing to weigh heavy.

- USD/CNH consolidated its late 2025 break under 7.00, tracking near 6.9700 in latest dealings. The pair saw little upside through the tail end of last year, despite broader USD indices recovering some ground.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 04/01/2026 | 1730/1230 | Minneapolis Fed's Neel Kashkari | ||

| 05/01/2026 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 05/01/2026 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 05/01/2026 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 05/01/2026 | 0700/0200 | * | Turkey CPI | |

| 05/01/2026 | 0730/0830 | ** | Retail Sales | |

| 05/01/2026 | 0930/0930 | ** | BOE M4 | |

| 05/01/2026 | 0930/0930 | ** | BOE Lending to Individuals | |

| 05/01/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 05/01/2026 | 1500/1000 | *** | ISM Manufacturing Index | |

| 05/01/2026 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 05/01/2026 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 06/01/2026 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 06/01/2026 | 2200/0900 | ** | S&P Global Final Australia Composite PMI | |

| 06/01/2026 | 0001/0001 | * | BRC Monthly Shop Price Index | |

| 06/01/2026 | 0745/0845 | *** | HICP (p) | |

| 06/01/2026 | 0815/0915 | ** | S&P Global Services PMI (f) | |

| 06/01/2026 | 0815/0915 | ** | S&P Global Composite PMI (final) | |

| 06/01/2026 | 0815/0915 | ECB Cipollone Chairs Intl Monetary System Panel | ||

| 06/01/2026 | 0845/0945 | ** | S&P Global Services PMI (f) | |

| 06/01/2026 | 0845/0945 | ** | S&P Global Composite PMI (final) | |

| 06/01/2026 | 0850/0950 | ** | S&P Global Services PMI (f) | |

| 06/01/2026 | 0850/0950 | ** | S&P Global Composite PMI (final) | |

| 06/01/2026 | 0855/0955 | ** | S&P Global Services PMI (f) | |

| 06/01/2026 | 0855/0955 | ** | S&P Global Composite PMI (final) | |

| 06/01/2026 | 0900/1000 | *** | North Rhine Westphalia CPI | |

| 06/01/2026 | 0900/1000 | ** | S&P Global Services PMI (f) | |

| 06/01/2026 | 0900/1000 | ** | S&P Global Composite PMI (final) | |

| 06/01/2026 | 0930/0930 | ** | S&P Global Services PMI (Final) | |

| 06/01/2026 | 0930/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 06/01/2026 | 1300/1400 | *** | Germany CPI (p) | |

| 06/01/2026 | 1300/1400 | *** | Germany CPI (p) | |

| 06/01/2026 | 1300/0800 | Richmond Fed's Tom Barkin | ||

| 06/01/2026 | 1355/0855 | ** | Redbook Retail Sales Index |