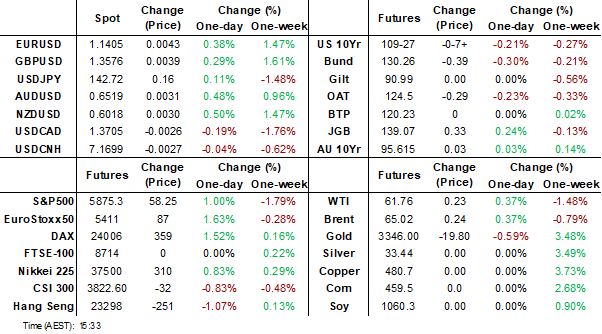

MNI EUROPEAN MARKETS ANALYSIS: USD Index Makes Fresh Lows

- Early headlines were dominated by US President Trump delaying the tariff hike for the EU. This benefited US equity futures, but the USD has remained firmly on the backfoot, making fresh lows in index terms. US Tsy futures are also down, although there is no cash trading today.

- Hong Kong and China equity markets have underperformed, with competition among EV makers a headwind.

- The US and UK are closed today for holidays. ECB President Lagarde speaks later.

MARKETS

US TSYS: Asia Wrap - Futures Trade Lower

TYM5 gapped lower on the open as President Trump agrees to an extension to July 9 for Europe. The range has been 109-24+ to 110-02+ during the Asia-Pacific session. It last changed hands at 109-28, down 0-06 from the previous close.

- No Cash trading today

- The EU is ready to advance talks and needs until July 9 to reach a good deal, Ursula von der Leyen said on X. https://x.com/vonderleyen/status/1926729529436913794

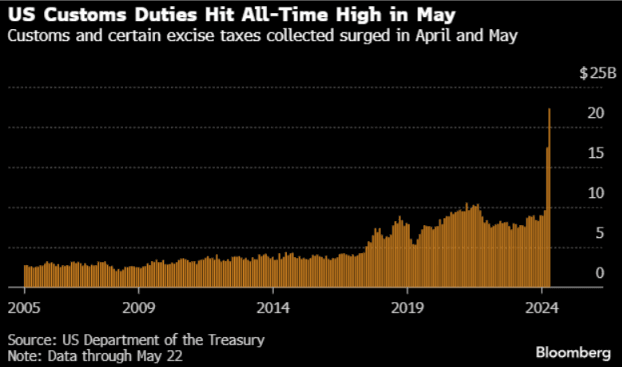

- (Bloomberg) -- “The Treasury’s latest fiscal statement is a reminder for financial markets that, despite the 90-day pause in the April 2 duties, levies have increased and they remain a risk for the economic outlook.”

- “Tariff income from excise taxes surged on May 22 to a record $22.3 billion, the first daily report to show the impact of new rates, according to the Treasury report. The one-day increase of about $16.5 billion was more than three times what was collected on the same day in May 2024 and up from $11.7 billion that was collected on April 22.” See Graph below.

The 10-year found sellers back towards 4.45% on Friday night and then moved higher to close back above 4.50%. Dips look likely to see supply in the short-term, should yields hold above 4.40% the target looks to be the 4.75% area. Watch for any announcements relating to the SLR, this could cause a knee jerk to a market that is already quite short.

Fig 1: US Customs Duties

Source: MNI - Market News/Bloomberg

GLOBAL MACRO: March Exports Jump Ahead Of US Tariffs, Especially From Asia

The March CPB global trade data showed a significant pickup in export growth as countries, especially in Asia, try to beat the imposition of US duties. Reciprocal tariffs were announced on April 2 and then delayed until July 9 to allow negotiations to take place. Exporters are likely to continue front loading shipments in case agreements are not reached, increasing inventories and thus the likelihood of a drop in trade in H2.

- Global trade rose 2.2% m/m in March to be up 6.6% y/y, fastest since December 2021, after 0.5% & 3.0% in February. Exports rose 2.3% m/m and 5.9% y/y up from 2.0% y/y with both DM and EM posting monthly increases. The Baltic Freight Index and manufacturing PMI suggest there will be a correction.

Global trade y/y% vs Baltic Freight Index

Source: MNI - Market News/LSEG

- Shipments from developed markets rose 1.2% m/m and 3.9% y/y after 1.4% y/y. This was the fifth consecutive monthly rise. Advanced Asia saw exports increase 12.1% y/y, while Japan’s rose 6.6% y/y. The euro area rose 0.5% y/y, highest since November 2022, and the US by 4.3% y/y.

- EM Asia also saw strong export growth with China up 16.9% y/y and excluding China +6.4% y/y. Latin America increased 10.2% y/y. Mexico received some reprieve from US duties through USMCA-compliant goods worth around half of US imports from Mexico but still faces universal tariffs on steel and autos. Overall EM exports rose 3.7% m/m to be up 9.1% y/y following February’s 3.1% y/y.

Global exports y/y%

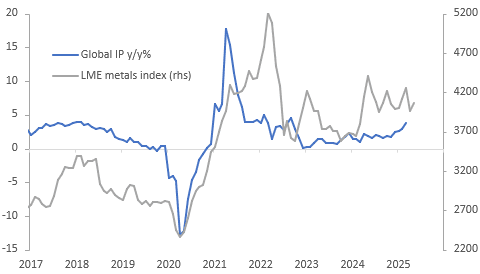

GLOBAL MACRO: IP Growth Rises In March, Outlook Uncertain

CPB data showed that global IP volumes rose 0.5% m/m to be up 3.7% y/y in March after 0.8% & 2.9% y/y respectively. This was the fastest annual growth rate since September 2022, a time when the global economy was recovering from Covid. The pickup in IP seen since December has lagged global trade growth. The global manufacturing PMI suggests that IP is likely to slow in the coming months but metal prices suggest that it could strengthen before stabilising.

- Some of the frontloading of trade to beat US tariffs may be coming out of inventories and thus IP hasn’t picked up to the same degree. Thus, IP may not slow as much in the second half of the year consistent with metal prices remaining at elevated levels.

Global IP vs LME metal prices

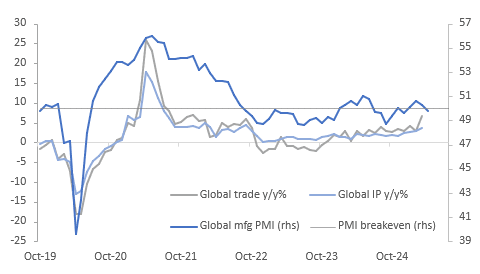

- The S&P Global manufacturing PMI signalled slightly positive growth in activity in Q1 2025 but it fell to 49.8 in April from 50.3 signalling a slight contraction. The US’ reciprocal tariffs were announced on April 2 and likely weighed on the index. There could be some unwind in the May PMI, released on June 3, due to the tariff delay.

- Central banks assume that even if trade agreements are reached by July, uncertainty in H1 2025 will weigh on demand. If deals aren’t agreed, then global growth could be significantly lower.

Global growth

JGBS: Modest Bull-Flattener, PPI Tomorrow, 40Y Supply On Wed

JGB futures are stronger, +31 compared to the settlement levels, after recovering much of the losses seen earlier in the session. Futures had closed Friday’s overnight session at +56.

- US equity-index futures have climbed in early Asian trading after President Donald Trump extended a deadline on aggressive European tariffs. Trump agreed to delay the date for a 50% tariff on goods from the European Union to July 9 from June 1.

- US tsy futures (TYM5) have weakened in today’s Asia-Pac session, with TYM5 at 109-27, -0-07+ from closing levels. Cash US tsys are closed today for Memorial Day.

- “Neel Kashkari said major shifts in US trade and immigration policy are creating uncertainty for the Fed to move on interest rates before September." (BBG)

- (Bloomberg) - "Long-term Japanese yields are set to climb further with JGB traders facing a 40-year debt auction, followed by Tokyo inflation data this week." (per BBG)

- Cash JGBs are 1-3bps richer across benchmarks with a flattening bias. The benchmark 30-year yield is 3.0bps lower at 3.023% versus the high of 3.204%. It was as low as 3.0% earlier in the session.

- Swap rates are 1-3bps higher with a flatter curve and swap spreads are wider.

- Tomorrow, the local calendar will see PPI data ahead of 40-year supply on Wednesday.

AUSSIE BONDS: Richer After A Subdued Session With Cash US Tsys Closed

ACGBs (YM +3.0 & XM +4.0) are stronger on a local-data-light Sydney session with cash US tsys closed for Memorial Day.

- US equity-index futures climbed in today's Asian session after President Donald Trump extended a deadline on aggressive European tariffs. Trump agreed to delay the date for a 50% tariff on goods from the European Union to July 9 from June 1.

- Analysis by Goldman Sachs shows short interest in the median S&P 500 stock – that is, the percentage of investors betting the stock will fall - has jumped to its highest reading since August 2019, according to Goldman’s US guru, David Kostin. (per BBG)

- US tsy futures (TYM5) have weakened in today's Asia-Pac dealings, with TYM5 at 109-27+, -0-07 from closing levels.

- Cash ACGBs are 3-4bps richer.

- The bills strip has bull-flattened, with pricing +1 to +5.

- RBA-dated OIS pricing is 2-6bps softer across meetings today, with early 2026 leading. A 25bp rate cut in July is given a 72% probability, with a cumulative 73bps of easing priced by year-end.

- Tomorrow, the local calendar will be empty ahead of April CPI data on Wednesday.

- The AOFM plans to sell A$400mn of the 4.25% 21 June 2034 bond tomorrow, with A$1200mn of the 4.25% 21 March 2036 bond on Friday.

STIR: Expected YE AU-NZ Official Rate Diff Continues To Narrow

RBNZ-dated OIS pricing was little changed across meetings today.

- Markets continue to price in 25bps of easing for Wednesday’s meeting, with a total of 64bps expected by November 2025.

- However, rates remain 2–18bps higher than levels observed prior to the Q1 CPI release on April 17.

- Amid firmer NZ rates and softer Australian rates—following last week’s dovish RBA pivot and Tuesday’s rate cut—the expected year-end policy rate differential between Australia and New Zealand has narrowed by 20–25bps over the past week, currently standing at +23bps.

Figure 1: RBA & RBNZ Official Rate Profile (%)

Source: MNI - Market News / Bloomberg

BONDS: NZGBS: Bull-Flattener, US Tsys Out Today, RBNZ Policy Decision On Wed

NZGBs closed near session bests, showing a bull-flattener, with benchmark yields 1-4bps lower.

- Total new residential mortgage lending in New Zealand fell to NZ$7.58bn in April from NZ$8.49bn in March, according to RBNZ data.

- TYM5 gapped lower on the open as President Trump agrees to an extension to July 9 for Europe. The range has been 109-24+ to 110-02+ during the Asia-Pacific session. It last changed hands at 109-28, down 0-06 from the previous close. No cash US tsys today.

- Swap rates closed 1-3bps lower.

- Tomorrow, the local calendar will be empty

- RBNZ-dated OIS pricing was little changed across meetings today. Markets continue to price in 25bps of easing for Wednesday’s meeting, with a total of 64bps expected by November 2025. However, rates remain 2–18bps higher than levels observed prior to the Q1 CPI release on April 17.

- Amid firmer NZ rates and softer Australian rates—following last week’s dovish RBA pivot and Tuesday’s rate cut—the expected year-end policy rate differential between Australia and New Zealand has narrowed by 20–25bps over the past week, currently standing at +23bps.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond and NZ$225mn of the 4.25% May-36 bond.

FOREX: Asia FX Wrap - USD Struggles Across The Board

The BBDXY has had a range of 1207.08 - 1211.08 in the Asia-Pac session, it is currently trading around 1208. President Trump agrees to an extension to July 9 for Europe. https://x.com/TrumpDailyPosts/status/1926778871442972759. The EU is ready to advance talks and needs until July 9 to reach a good deal, Ursula von der Leyen said on X. https://x.com/vonderleyen/status/1926729529436913794.

- EUR/USD - Asian range 1.1363 - 1.1419, Asia is currently trading 1.1410. EUR has traded higher and remained bid throughout the Asian session. What stood out from the price action on Friday was how well the EUR held up in the face of a potential 50% increase in tariffs, and it was again the USD that took the brunt of the impact. This clearly shows the market's current outlook and leans into the growing “sell America “ theme.

- GBP/USD - Asian range 1.3524 - 1.3593, Asia is currently dealing around 1.3580. The GBP is breaking the Pivotal Weekly Resistance in the 1.3500 area, I would be weary considering it is in thin liquidity on an Asian Monday morning, with a US and European holiday. A sustained break though would signal a potential acceleration of the trend higher.

- USD/CNH - Asian range 7.1616 - 7.1824, the USD/CNY fix printed 7.1833. Asia is currently dealing around 7.1690. Sellers should be found on a bounce back towards the 7.2200 area again. Andreas Steno Larsen on x : "The elephant in the room USDCNH needs to go to 6.80 at least. https://x.com/AndreasSteno/status/1926115935200440525"

Cross asset : SPX +1.07%, Gold $3350, US TYM5 109-27 , BBDXY 1208, Crude oil $61.76

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg

JPY: Asia Wrap - Focus Turning Back To Key 140.00 Area

The Asia-Pac range has been 142.23 - 143.08, Asia is currently trading around 142.65. The brief bounce early doors this morning saw a wall of selling back above 143.00 and USD/JPY has spent the remainder of the session under pressure.

- “Neel Kashkari said major shifts in US trade and immigration policy are creating uncertainty for the Fed to move on interest rates before September.”(BBG)

- “Nvidia’s earnings this week could serve as a barometer, with the world’s most valuable chipmaker expected to post another quarter of strong growth. Revenue from its core chip business is forecast to rise over the next four quarters, and options pricing implies a post-earnings move of more than 7%, according to data curated by Bloomberg.”(BBG)

- (Bloomberg) - “Long-term Japanese yields are set to climb further with JGB traders facing a 40-year debt auction, followed by Tokyo inflation data this week.”

- USD/JPY again struggled to hold onto any gains above 143.00 this morning, fresh USD/Asia selling was seen with the USD broadly lower in our session as the tariffs on Europe are extended to July 9.

- The price action last week shows the market is still much more comfortable selling rallies, resistance is now back towards 144.00/145.00. The focus will turn once more to the pivotal 140.00 area, a break of which will open a much deeper move lower.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 144.00($1.06b), 143.00($713m) Upcoming Close Strikes : 143.00($1.71b May 28), 139.75($1.56b May 29).

CFTC data shows Asset managers maintained their already extensive JPY longs, and leveraged funds continue to build on their newly initiated shorts.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

AUD: Asia Wrap - AUD Testing Back Above 0.6500

The AUD/USD has had a range of 0.6486 - 0.6537 in the Asia- Pac session, it is currently trading around 0.6520. The USD has opened weak again in early Monday morning trading in Asia with another leg lower.

- President Trump agrees to an extension to July 9 for Europe. https://x.com/TrumpDailyPosts/status/1926778871442972759

- The AUD has been bid for most of the Asian session benefitting from the broad USD sell-off and more fresh selling in USD/ASIA.

- The AUD/USD is still in a 0.6350 - 0.6550 range but looks likely to test the top end over the course of this week if not today. If you want to express a short in the AUD the crosses look a better vehicle.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend. A break above 0.6550 and the move higher could begin to accelerate.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6510(AUD1.4b May 27), Upcoming Close Strikes : none

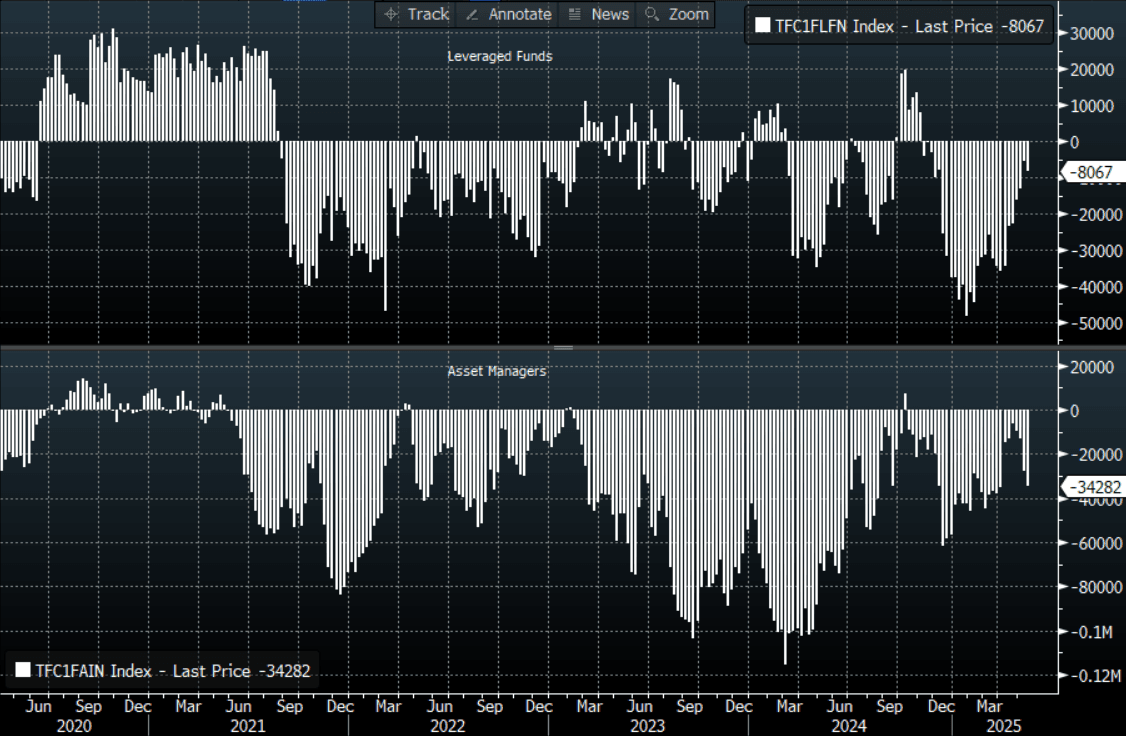

- CFTC Data shows Asset managers have continued to add to their shorts, the Leveraged community also added to shorts though still a very small position.

AUD/JPY - Today's range 92.42 - 93.07, it is trading currently around 92.95. Decent demand again seen towards the 92.00 area as it holds Friday night. A sustained close back below 91.50/92.00 is needed to turn the focus back towards the lows again.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg

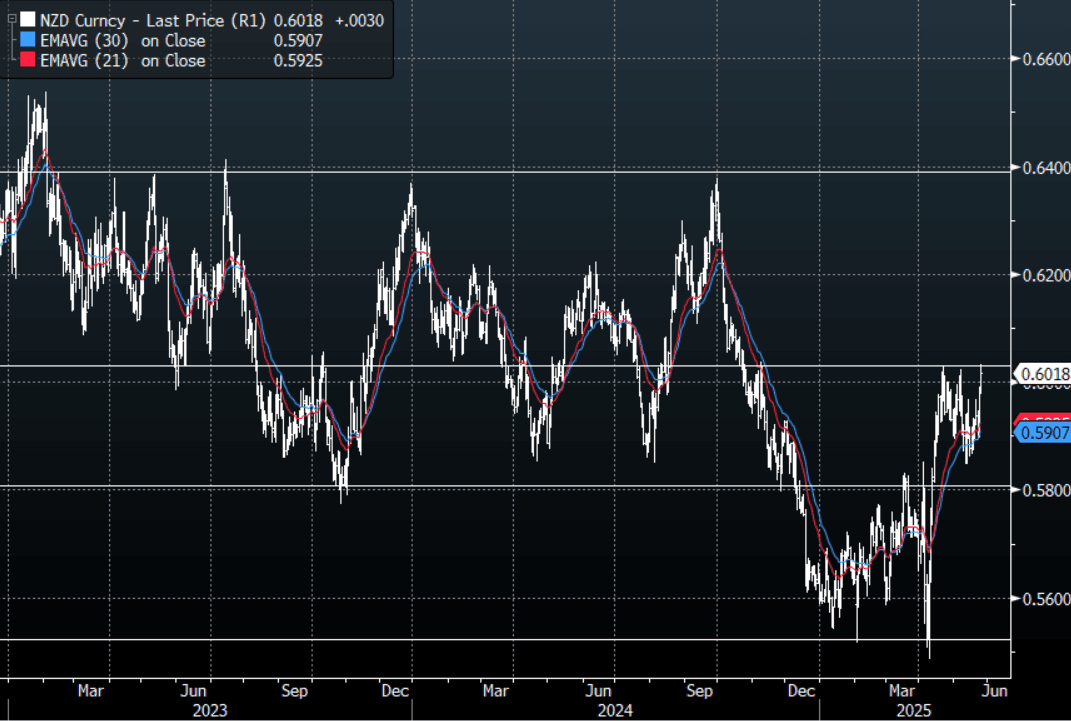

NZD: Asia Wrap - Looking To Break Higher

The NZD/USD had a range of 0.5981 - 0.6032 in the Asia-Pac session, going into the London open trading around 0.6020. The USD has opened weak again in early Monday morning trading in Asia with another leg lower.

- The RBNZ meets this week when the decision is announced on Wednesday with updated staff forecasts in the Monetary Policy Statement. It will be followed by a press conference which will be Hawkesby’s first as governor. The MPC is widely expected to cut rates 25bp to 3.25% bringing cumulative easing this cycle to 225bp. The OCR profile will be a focus as well as CPI given recent inflation developments.

- (Bloomberg) -- BNZ publishes new residential mortgage lending data for April, on its website. Lending to all borrowers NZ$7.58b, First-home buyers borrowed NZ$1.54b or 20.4% of total, Investors borrowed NZ$1.52b or 20% of total, There were 19,289 new mortgage commitments — down 12% m/m: RBNZ.

- The NZD has been bid for most of the Asian session benefitting from the broad USD sell-off and more fresh selling in USD/ASIA.

- The NZD continues to trade in a 0.5850/0.6050 range, could this latest round of USD selling provide it with the momentum to break this week ? As the “sell America” trade gathers pace.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. The first target is the highs just above 0.6000, a break here could provide the spark for the next leg higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5980(NZD513m May 26), Upcoming Close Strikes : 0.5725(NZD1.09b May 28)

- CFTC Data showed Asset managers maintaining their shorts, while the leveraged community added a decent clip back to their own short.

AUD/NZD range for the session has been 1.0819 - 1.0857, currently trading 1.0830. A sustained break above 1.0930 is needed to turn the focus higher, until then expect supply on bounces.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

FOREX: Mixed CFTC Trends, CAD Shorts Dominate, JPY Longs Added Too

In terms of leveraged investors in the FX space, CFTC data showed mixed trends. Yen longs were added too, bringing the outright long to over 30k, see the table below. This is the highest net longs since 2019 for this segment. Elsewhere though the bias was in favor of the USD. EUR net shorts were built by close to 8k, while shorts against the AUD and NZD were added to, same applied to CAD. CAD outright shorts of just over -40k are the largest for the leveraged investor base.

- In the asset manager or real money segment, it was similar trend. CAD shorts were added too, with over -14k in fresh shorts. AUD shorts were also added too by over 6k.

- For the majors, there was little net change in weekly positioning. EUR and JPY longs continue to dominate.

Table 1: CTCF Positioning By Currency & Investor Type

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | 6029 | 30770 | 728 | 111647 |

| EUR | -7790 | -13104 | -681 | 335187 |

| GBP | 139 | 37110 | -899 | -6809 |

| AUD | -2514 | -8067 | -6383 | -34282 |

| NZD | -4335 | -7867 | 269 | -19888 |

| CAD | -3895 | -40091 | -14381 | -82468 |

| CHF | 2035 | 1137 | -1943 | -26953 |

| MXN | -3814 | -5497 | 3080 | 30189 |

Source: MNI - Market News/Bloomberg

ASIA STOCKS: EV Shares Lead Stocks Lower in HK

Chinese electric vehicle stocks fall in Hong Kong on investors concern over intensifying sector competition after leader BYD announced price cuts for some mass-market models. BYD drops over 7% in Hong Kong; Geely Auto -7%, Great Wall -5%, Li Auto -4.8%, Xiaomi -2%, Nio -2%, Xpeng -2%. This comes as Citigroup expects Xiaomi’s new YU7 SUV to be priced in the 250,000 yuan-320,000 yuan range with monthly sales at about 30,000 units, and “significantly erode” Tesla model-Y’s China market share.

- The declines in Hong Kong led broader moves in China. The Hang Seng fell -1.00%, the CSI 300 0.75%, Shanghai Comp -0.30% and Shenzhen -0.37%

- The KOSPI is the region's outperformer as politicians vying for the leadership tout further stimulus and the BOK meets this week and is expected to cut. The KOSPI has jumped +1.30% today.

- In what continues to be a challenging period, the FTSE Malaysia KLCI shrugged off Friday's gains to return to the recent downward trend, falling -0.20% today.

- The Jakarta Composite fell today by -0.93% yet remains in a bullish period with only seven down days since the begging of April and strong foreign inflows.

- The FTSE Straits Times is down -0.45% and the PSEi in the Philippines down -0.38%.

- The NIFTY 50 is up +0.78% and is building on what was modest but positive week last week for returns.

OIL: Crude Moderately Higher As Trade Fears Abate

Oil prices are slightly higher during APAC trading helped by news that the US and EU would continue trade talks and that reciprocal tariffs would be delayed until July 9, the original timeframe. The USD index is down 0.3%, which is also providing support to dollar-denominated crude.

- WTI is up 0.4% to $61.76/bbl off the intraday low of $61.51. It rose to $62.14 early in the session following the US-EU trade news, approaching initial resistance at $62.75, 50-day EMA. Gains continue to be seen as corrective but a clear break of the 50-day EMA would signal a stronger reversal.

- Brent is 0.4% higher at $65.06, off the intraday low of $64.77. It reached $65.40 earlier. Technicals suggest a short-term bullish theme but in the medium-term it is bearish. The bear trigger is at $58, while initial resistance is $66.24, 50-day EMA.

- Through geopolitical and trade headlines, crude continues to watch OPEC closely. It meets on Sunday to decide output plans from July. It has decided to increase production substantially this year as it focuses on gaining market share rather than on prices and thus penalising overproducing members. Another rise is generally expected increasing excess supply for 2025 and likely 2026 further.

- The US and UK are closed today for holidays. ECB President Lagarde speaks later.

GOLD: Bullion Slightly Lower On Better Risk Tone Following Tariff Delay For EU

Gold prices are moderately lower during today’s APAC session after rising close to 2% on Friday. They are down 0.2% to $3350.20/oz but off the intraday low of $3331.62 which followed some pullback in safe-have flows after news that the US and EU would continue to work towards a trade deal and the threat of a 50% US tariff on June 1 was postponed until July 9. The USD index is down 0.2%.

- Despite today’s lower gold price due to the better risk tone following more positive trade talk, it is likely to continue to find support from the US given ongoing trade negotiations are likely to be bumpy. There are also concerns over the fiscal position after the House passed the tax bill which now faces the Senate. Global relations remain fraught especially in the Middle East and Russia/Ukraine.

- Regional equities are mixed with the Hang Seng down 1.0% but KOSPI up 1.3% and S&P e-mini +1.0%. Oil prices are slightly higher with WTI +0.4% to $61.76/bbl. Copper is up 0.8% but iron ore is down to around $97/t. Silver has been range trading and is little changed.

- The US and UK are closed today for holidays. ECB President Lagarde speaks later.

CHINA: Country Wrap: Could China Lower its Growth Target

- The blowout in Chinese steel exports has likely peaked, as trade barriers mount and domestic production falls, according to Goldman Sachs Group Inc. Exports climbed last year to a nine-year high of 111 million tons, but are forecast to moderate by 3% in 2025 before dropping more sharply by a third in 2026, the bank said in a note on Friday. The biggest headwind to sales is the substantial number of ongoing anti-dumping investigations around the world, the bank said. (source BBG)

- If job creation is robust and debt is contained, annual economic growth of around 4 per cent is feasible for the 2026-30 period, former economic official Xu Lin says. A former senior economic planner has called for China's annual growth target to be lowered for the next five years, factoring in the likelihood of a protracted rivalry with the United States and the need to solve deep-rooted structural problems in China. Xu Lin, who helped draft Beijing's five-year plan for decades while an official at the National Development and Reform Commission, made the comments as the world's second-largest economy is increasingly relying on economic planning for continued growth. Compared with some market estimates of around 4.5 per cent annual growth from 2026-30, he said the potential growth rate and growth target figure should be around 4 per cent in the next five to 10 years, owing to China's shrinking population, its falling savings and production rate, and other headwinds. (source SCMP via BBG)

- Yuan Reference Rate at 7.1833 Per USD; Estimate 7.1766

- Bonds remain in a tight range with CGB10YR 1.68% (-1bps) today

INDIA: Country Wrap: Growth Gaining Momentum

- The Reserve Bank of India (RBI) is preparing for the possibility of directly lending to non-banking financial companies and mutual funds during periods of extreme liquidity constraints, ensuring survival for those that get shut out of the lending markets during the episodic crises, said a person familiar with the matter. (source Economic Times)

- Growth in the Indian economy likely gained momentum to touch at least a four quarter high in Q4 (January - March) of FY 25 after witnessing moderate growth rates in the preceding three quarters, owing to strong showing in agricultural output that likely lifted rural consumption demand, trade, hotels and transport segment and construction sector, according to analysts. (source Business Standard)

- The NIFTY 50 is up +0.78% and is building on what was modest but positive week last week for returns

- The Rupee is up +0.45% today at 84.84 and up +.65% over the last 5 trading days

- Bonds have edged weaker Monday with the IGB 10YR at 6.25% (+0.5bps)

INDONESIA: Country Wrap: SWF Fund Agrees Ties with China

- China and Indonesia agreed to step up ties between their economies during Premier Li Qiang’s visit to Jakarta, including one on investment involving their sovereign wealth funds. Both their central banks signed a MOU on a framework for bilateral transactions in local currencies during a ceremony witnessed by Li and President Prabowo Subianto on Sunday. The two countries will boost cooperation on tourism and agricultural exports, while wealth funds China Investment Corporation and Danantara Indonesia entered an investment agreement. No details were provided. (source BBG)

- Indonesia will cut transport and power costs and deliver other stimulus in June and July in an effort to boost household spending and rekindle economic growth. The government will provide discounts on train, plane and ferry tickets during the school holiday period, as well as toll road fee reductions targeting about 110 million drivers, the Coordinating Economic Affairs Ministry said in a statement Saturday. It will also slash electricity bills by 50% for 79.3 million households and increase the allocation of staple food assistance for 18.3 million families. There will be salary top-ups for workers earning less than 3.5 million rupiah ($215) per month as well as for contract teachers. (source BBG)

- The Jakarta Composite fell today by -0.93% yet remains in a bullish period with only seven down days since the begging of April and strong foreign inflows.

- The rupiah has done very little today broadly unchanged at 16,213 yet remains over 1% better over the last week.

- Bonds have rallied in most maturities today with the 5YR and 10YR the best performers. INDOGB 10YR 6.80% (-2bps today)

ASIA FX: USD Weaker, USD/TWD Breaks Sub 30.00

In North East Asia FX markets, the bias has been for a weaker USD, consistent with recent themes. CNH moves so far today have been modest, but USD/CNH has still hit fresh year to date lows. USD/KRW has edged down, while USD/TWD has broken under 30.00. TWD Is up 0.50%, the best performer in this space.

- After gapping lower through Friday trade as Trump's EU tariff threat rattled US asset sentiment, the early morning announcement of a delay to July for the tariff hike hasn't provided any meaningful USD relief. USD/CNH was last near 7.1700 and tracking towards a test of the 7.1400 handle, which we last saw in Nov 2024. The USD/CNY fix was set above market expectations, but the actual fix was still lowered noticeably compared to Friday's outcome.

- Spot USD/KRW found support ahead of 1360, but the recent downtrend in the pair remains intact. We were last near 1365, little changed for the session. Again, downside interest is likely to rest near 1350 for this pair. The pair looks too low relative to US-SK 1y1y rate differentials, but other drivers around the sell American theme are more dominant at the moment.

- Spot USD/TWD has broken down through 30.00, for the first time since early May (we were last near 29.85, up around 0.50% in TWD terms). Downside focus is likely to be on 29.60/65 region, which marked lows in the pair back on May 5. The RSI (14) remains in significantly oversold territory, near 16, but with broader USD sentiment so weak, it isn't deterring downside momentum in the pair.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 26/05/2025 | 0600/0800 | ** | PPI | |

| 26/05/2025 | 0700/0900 | ** | PPI | |

| 26/05/2025 | 1320/1520 | ECB's Lagarde On Europe's Role In A Fragmented World | ||

| 27/05/2025 | 2301/0001 | * | BRC Monthly Shop Price Index | |

| 27/05/2025 | 0600/0800 | * | GFK Consumer Climate | |

| 27/05/2025 | 0645/0845 | *** | HICP (p) | |

| 27/05/2025 | 0800/0400 | Minneapolis Fed's Neel Kashkari | ||

| 27/05/2025 | 0900/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 27/05/2025 | 1000/1100 | ** | CBI Distributive Trades | |

| 27/05/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/05/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/05/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Quarterly Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Quarterly Price Index |