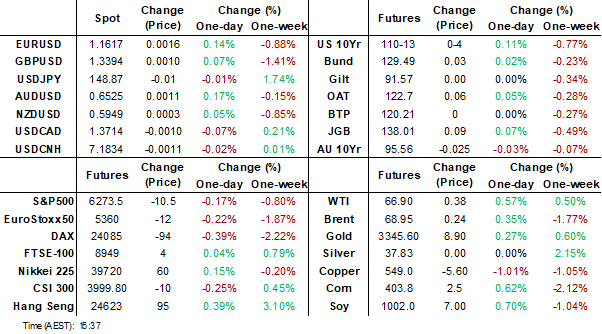

MNI EUROPEAN MARKETS ANALYSIS: USD & Tsy Yields Consolidate

- The USD and US Tsy yields have consolidated, post gains after Tuesday's CPI print. US President Trump has hinted at more tariffs in the pharmaceutical and chips space by months end and also spoken about the Fed Chair role.

- Fed speak has reiterated a patient approach to the policy outlook.

- Looking ahead, we have UK CPI, the US PPI, as well as various Fed speakers.

MARKETS

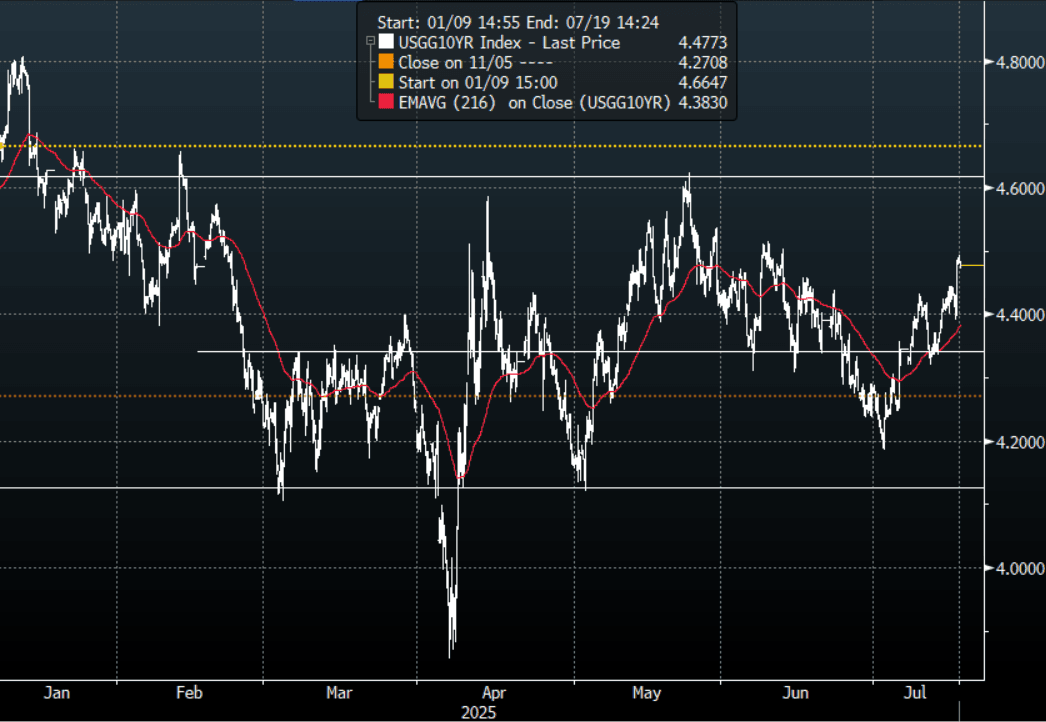

US TSYS: Asia Wrap - Quiet Session As Bonds Consolidate Overnight Move

The TYU5 range has been 110-08+ to 110-12+ during the Asia-Pacific session. It last changed hands at 110-11+, up 0-02 from the previous close.

- The US 2-year yield is trading around 3.94%.

- The US 10-year yield is trading around 4.477%.

- The 10-year yield has broken above 4.45% in response to the CPI Data, this implies price is likely to turn its focus back to 4.65% and could see further paring back of longs. Support is now back towards the 4.35/40% area which has been the pivot in the larger 4.10% - 4.65% range.

- (Bloomberg) -- “I think it sort of is,” President Donald Trump says when asked whether the renovations at the central bank were a fireable offense for Federal Reserve Chair Jerome Powell.

- “LOGAN: BASE CASE CALLS FOR CONTINUED RESTRICTIVE POLICY, HAVE BEEN DISAPPOINTED BEFORE AFTER STREAKS OF LOW INFL. ALSO POSSIBLE SOFTER LABOR MKT COULD REQUIRE CUTS SOON.” - BBG

- Bloomberg - “Term premium has been rising in several government bond markets, especially the UK, Japan and France. All three have large legacy debt loads, significant fiscal deficits and mushrooming interest payment costs. Even the US facing a mini-fiscal crisis cannot be completely ruled out, given its enormous borrowing and falling revenues relative to its deficit.”

Fig 1: 10-Year US Yield Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Cash Bond Twist-Flattener, 40Y Rallies Strongly, 40Y Auction On July 23

JGB futures are weaker but off session lows, -8 compared to the settlement levels.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session after yesterday's post-CPI sell-off.

- Cash JGBs have sharply twist-flattened across benchmarks, with yields 1bp higher to 6bps lower.

- (Bloomberg) "JGB 40-year yields are lower today, reversing most of the climb seen on Tuesday as the longest duration bonds continue to suffer from illiquidity and tepid demand. However, yields are still higher by around 33 bps this month."

- The MOF plans to auction Y400.0 Bln of 40-Year JGBs on July 23.

- Swap rates are flat to 1bp higher. Swap spreads are tighter out to the 20-year.

- Tomorrow, the local calendar will see Trade Balance, Weekly International Investment Flow and Tokyo Condominiums for Sale data alongside 1-year supply.

AUSSIE BONDS: Modestly Cheaper, June Jobs Data Tomorrow

ACGBs (YM -3.0 & XM -3.0) are cheaper with narrow ranges.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session after yesterday's post-CPI sell-off.

- Cash ACGBs are 2-3bps cheaper with the AU-US 10-year yield differential at -7bps. At -7bps the differential is positioned near the middle of the +/- 30bps range that has held since November 2022.

- The bills strip cheaper with pricing -3 to -4 beyond the first contract (-1).

- RBA-dated OIS pricing is firmer across meetings today and remains 17–21bps above levels seen prior to the 8 July RBA decision. A 25bp rate cut in August is given an 88% probability, with a cumulative 54bps of easing priced by year-end.

- Tomorrow, the local calendar will see June Employment and Consumer Inflation Expectation data.

- (Bloomberg Economics) -- Australia’s labour market report for June is likely to show a lift in jobs and a slight increase in the unemployment rate. We expect a 20k increase in jobs, after a weaker-than-expected 2.5k decline in May.

- The AOFM plans to sell A$1100mn of the 1.00% 21 November 2031 bond on Friday.

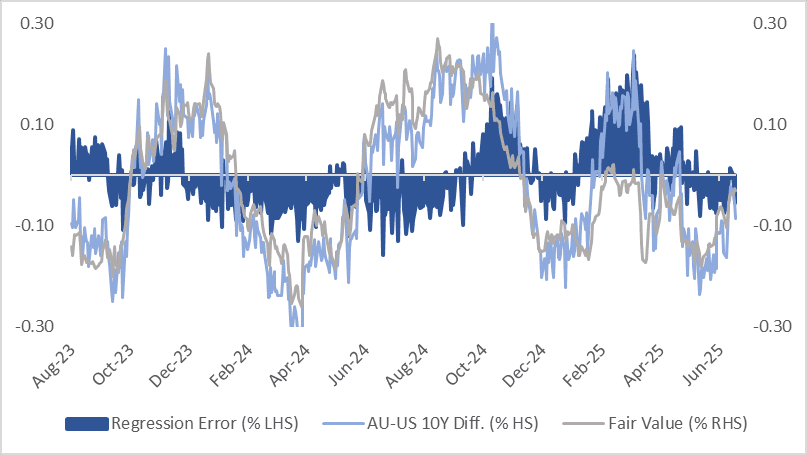

AUSSIE BONDS: AU-US 10Y Diff Is Near Middle Of Range

The AU-US 10-year cash yield differential currently stands at -7bps, positioned near the middle of the +/- 30bps range that has held since November 2022.

- A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past year suggests the current spread is slightly below fair value at -3bps.

- The 1Y3M differential, a key gauge of expected relative policy trajectories over the next 12 months, has traded within a 40bp range this year and is currently in the top half of the range at ~-5bps after last week’s surprise decision by the RBA to leave the cash rate unchanged at 3.85%.

- In early February, the 1Y3M differential had declined approximately 100bps since mid-September 2024, falling from +60bps to -40bps.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: Bloomberg Finance LP / MNI

BONDS: NZGBS: Closed Near Session Bests With A Steeper Curve

NZGBs closed slightly mixed with a steepener 2/10 curve. Benchmark yields finished 1bp lower to 1bp higher.

- NZGBs held by international investors increased to 62.7% from a month earlier in June.

- The fortnightly whole milk powder auction saw prices rise 1.7% versus the previous auction result, per GDT. This put prices back to $3928, from $3859 prior. It was the first rise since early May for the auction outcome.

- Swap rates closed little changed.

- RBNZ dated OIS pricing closed slightly firmer across meetings. 18bps of easing is priced for August, with a cumulative 32bps by November 2025.

- Tomorrow, the local calendar will see June food price data, with Q2 CPI on Monday.

- (Bloomberg Economics) -- New Zealand’s June price data are likely to show inflation holding in the Reserve Bank of New Zealand’s 1%-3% target band. In May, food prices rose 0.5% month on month, following a 0.8% gain in April. In year-on-year terms, prices climbed 4.4% after rising 3.7% in April.

- Tomorrow, the NZ Treasury plans to sell NZ$200mn of the 4.50% May-30 bond, NZ$200mn of the 4.25% May-36 bond and NZ$50mn of the 1.75% May-41 bond.

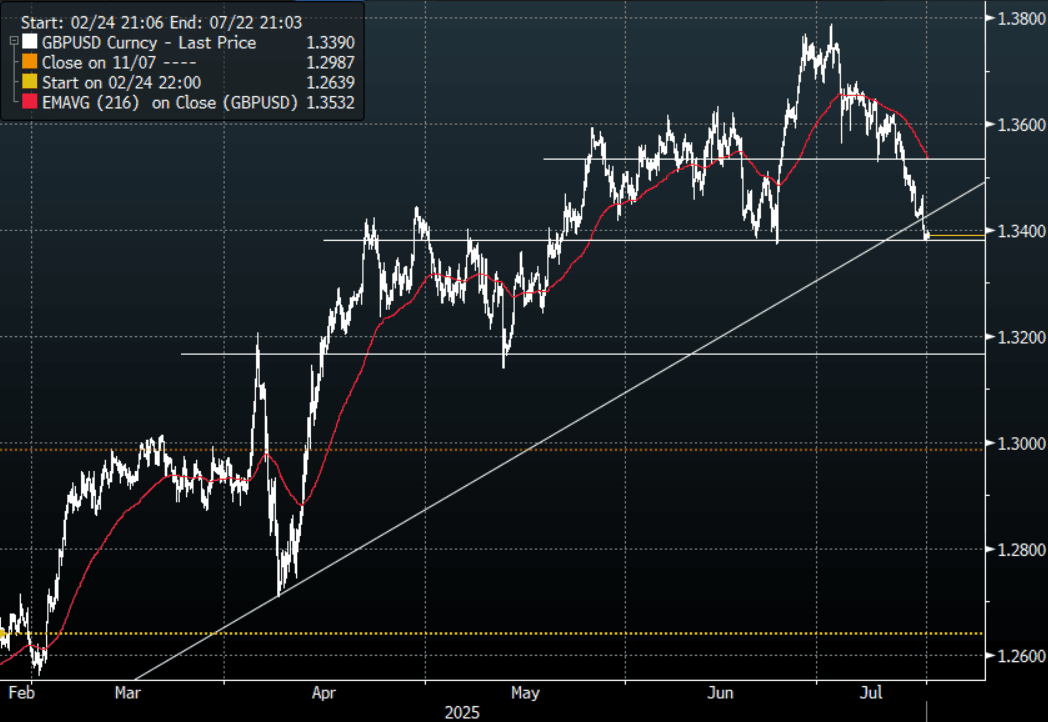

FOREX: Asia FX Wrap - BBDXY Surges Above 1200, Can It Build On This ?

The BBDXY has had a range of 1206.31 - 1208.31 in the Asia-Pac session, it is currently trading around 1207, -0.05%. The BBDXY surged higher with US yields in response to the CPI print. “Today’s inflation print showed that tariffs are having an impact on core goods and that impact is likely to get larger from here, limiting how much the Fed can cut and boosting the dollar,” said a currency strategist at Barclays” - BBG

- EUR/USD - Asian range 1.1601 - 1.1616, Asia is currently trading 1.1615. The pair is testing its first support around the 1.1600 area. The price still looks a little stretched in the short term and is vulnerable to any correction in the USD, first support around 1.1600 then more importantly the 1.1450 area.

- GBP/USD - Asian range 1.3382 - 1.3401, Asia is currently dealing around 1.3385. Price has rejected the move higher and Bailey’s hint that bigger rate cuts are on their way if the job market deteriorates further has added further headwinds. The pair has moved very quickly to test important support around 1.3350/1.3400. I would think there could be demand first up around here but a sustained break below and a deeper pullback towards 1.3000/1.3200 could be on the cards.

- USD/CNH - Asian range 7.1733 - 7.1757, the USD/CNY fix printed 7.1526, Asia is currently dealing around 7.1840. Sellers should be around on bounces while price holds below the 7.2000 area and the PBOC manages the fix lower. Above 7.2000 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.15%, Gold $3335, US 10-Year 4.475%, BBDXY 1207, Crude oil $66.76

- Data/Events : Italy CPI & Trade Balance

Fig 1: GBP/USD Spot hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

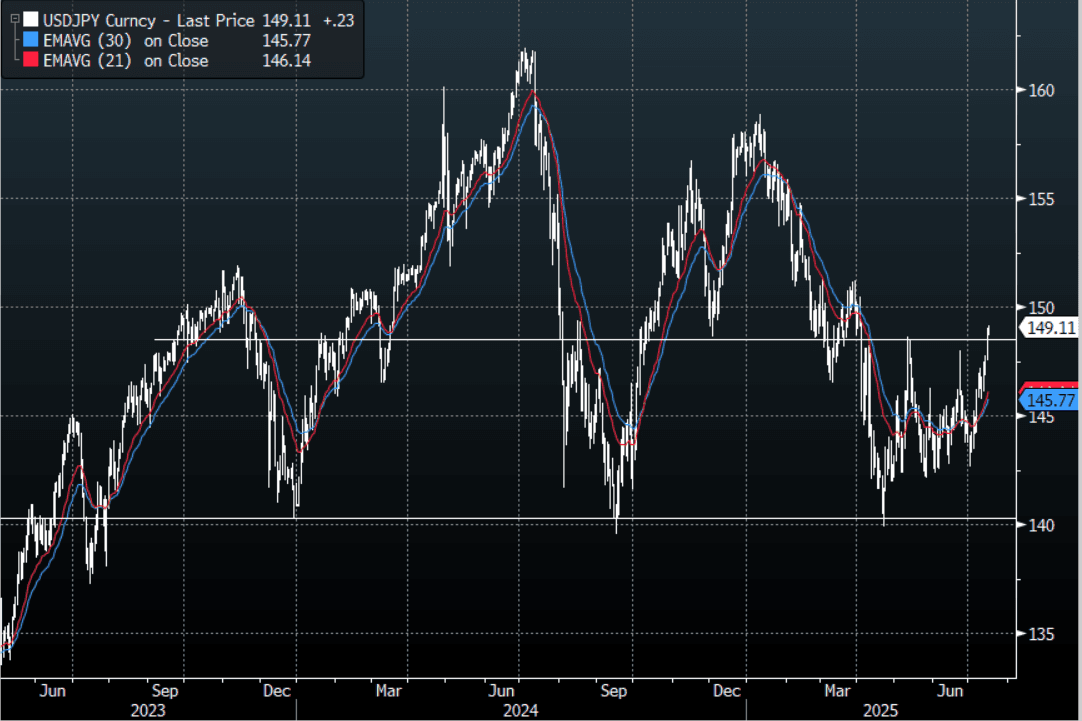

JPY: Asia Wrap - USD/JPY Is Not Backing Off, Eyes The 150.00 Area

The Asia-Pac USD/JPY range has been 148.71 - 149.18, Asia is currently trading around 149.10, +0.15%. USD/JPY surged higher overnight with US yields in response to the US CPI showing clear signs that tariffs are beginning to impact the core goods data. The USD/JPY relentless march higher has been pretty telling, challenging a market positioned the wrong way. This time USD/JPY has not given the JPY longs any respite and the powerful move back above 148.00 does not bode well. Dips should now be well supported in the short-term, will Asset Managers start paring back their extensive JPY longs now ? The first decent buy zone is now back towards the 147.00 area.

- (Bloomberg)- Short-dated options bets turned net bearish on the yen to the dollar on Tuesday for the first time since September of 2022 as the Japanese currency hit its lowest spot level since the aftermath of Liberation Day. The moves indicate the downdraft in the Japanese yen is set to extend.

- “Japan’s bond market is facing a potential Liz Truss moment as the risk of a ruling coalition defeat in Sunday’s election fuels concerns over fiscal policy. Yields on bonds with maturities of 20 years and beyond have risen at least 20 bps this month, part of a wave of selling in global bond markets as investors increasingly worry about government finances.” - BBG

- USD/JPY is now breaking above the highs of this year's range and implies the move could have more to play out. The Market is long JPY and should the USD continue to correct higher the risk is a move back above 150.00 to further challenge the conviction of the shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: 149.00($910m).Upcoming Close Strikes : 145.50($1.29b July 21).

- CFTC data shows Asset managers reduced their JPY longs slightly +89331, while leveraged funds have almost squared their newly built JPY longs +5224.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

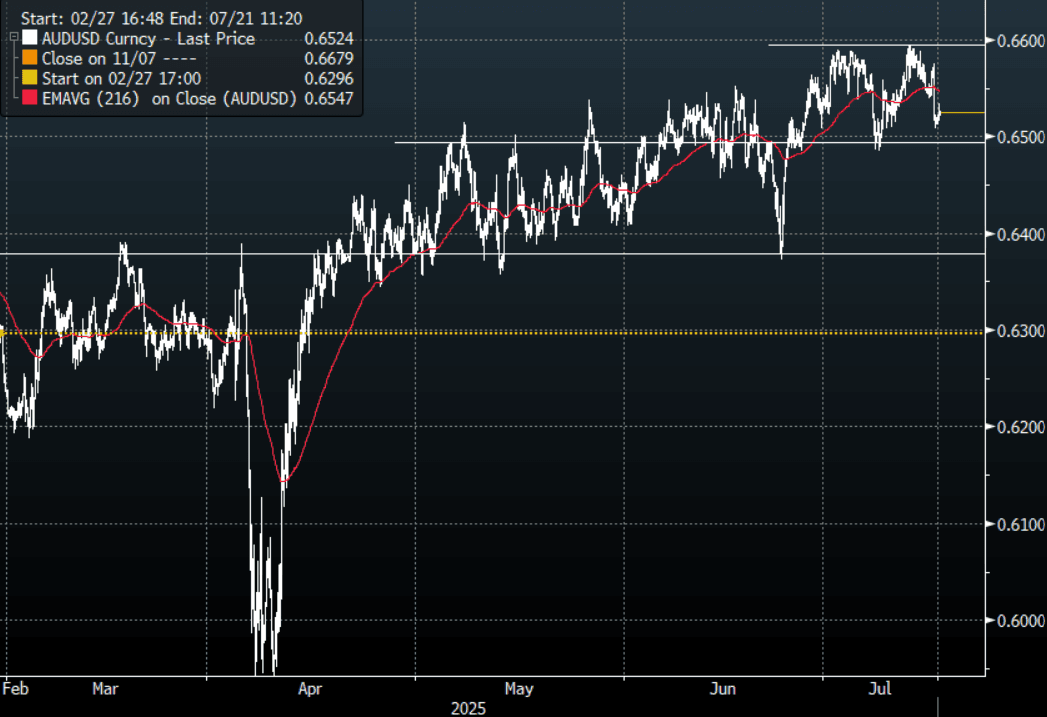

AUD: Asia Wrap - AUD/USD Finds Some Demand Towards 0.6500

The AUD/USD has had a range of 0.6512 - 0.6534 in the Asia- Pac session, it is currently trading around 0.6525, +0.18%. The USD has surged higher on the back of the US CPI showing clear signs that tariffs are beginning to impact the core goods data. US yields and the USD have both reacted as the market further reduces rate cut expectations for the year. This has seen currencies take a hit across the board, the AUD/USD has fallen quickly back to the lower end of its recent 0.6500/0.6600 range, its fortunes clearly tethered to the USD and if it can continue to pressure a short market then the AUD/USD could probe its support just below 0.6500. A Sustained break through this level opens up the potential for a further pullback towards the 0.6350 area.

- “The Australian dollar was bought by exporters ahead of Thursday’s local jobs report, according to Asia-based FX traders.” - BBG

- (Bloomberg Economics) -- Australia’s labor market report for June is likely to show a lift in jobs and a slight increase in the unemployment rate. We expect a 20k increase in jobs, after a weaker-than-expected 2.5k decline in May.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6550(AUD452m), 0.6575(AUD670m). Upcoming Close Strikes : 0.6480(AUD786m July18), 0.6500(AUD639m July 21), 0.6600(AUD725m July 21)

- CFTC Data shows Asset managers added to their shorts slightly -38252, the Leveraged community pared back their shorts to -19061..

- AUD/JPY - Today's range 96.94 - 97.24, it is trading currently around 97.20, +0.25%. The pair has had a good move above 96.00 and looks to be building momentum to extend higher. The market has been caught wrong-footed in both legs of this pair and price action suggests a potential move back to 99.00/100.00. With the risk backdrop souring it is unusual to still see this pair so well bid, this continues to point to a market that is paring back positioning. A Deeper correction in risk though would start to provide headwinds to further gains.

Fig 1: AUD/USD spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

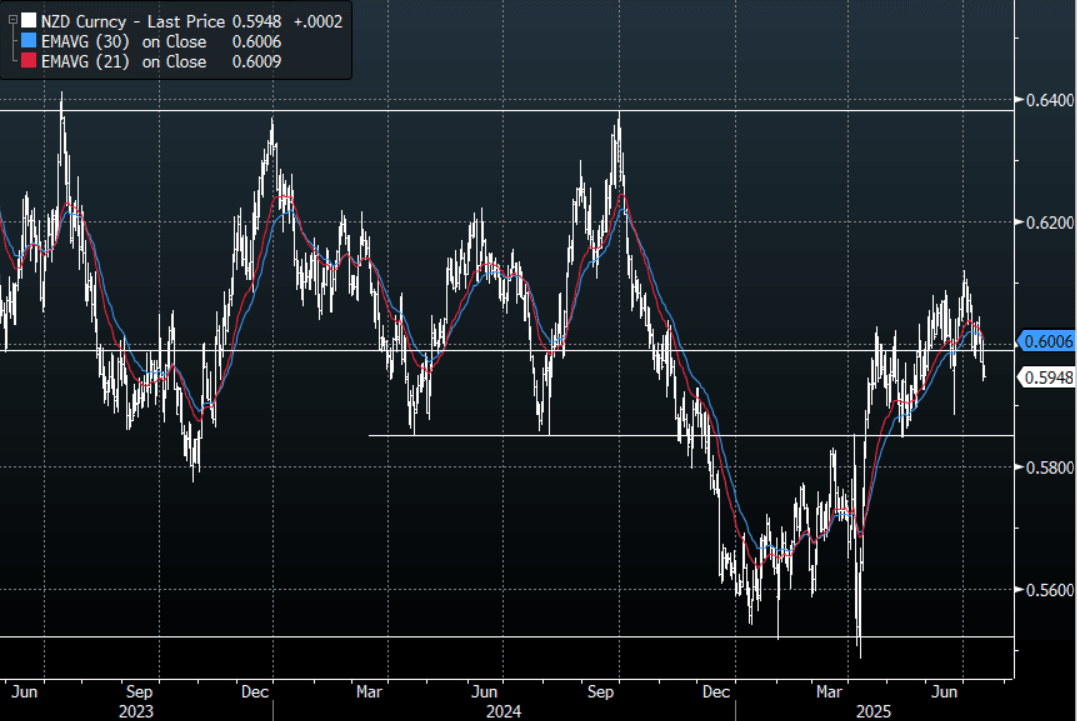

NZD: Asia Wrap - NZD/USD Has Broken Support, Risk Is A Move Back To 0.5850

The NZD/USD had a range of 0.5944 - 0.5966 in the Asia-Pac session, going into the London open trading around 0.5945, +0.01%. The USD has surged higher on the back of the US CPI showing clear signs that tariffs are beginning to impact the core goods data. US yields and the USD have both reacted as the market further reduces its rate cut expectations for the year. NZD/USD has broken below its recent support just below 0.6000 and the price action now suggests we could have a look back towards the important 0.5850 support area. Look for supply now on bounces back towards 0.6000 to cap initially.

- (Bloomberg Economics) -- New Zealand’s June price data are likely to show inflation holding in the Reserve Bank of New Zealand’s 1%-3% target band. In May, food prices rose 0.5% month on month, following a 0.8% gain

- "NZ JUNE GOVT. BONDS HELD BY FOREIGNERS RISE TO 62.7%" : BBF

- NZ Milk Prices Rise At Auction For The First Time Since May : Overnight the fortnightly whole milk powder auction saw prices rise 1.7% versus the previous auction result, per GDT. This put prices back to $3928, from $3859 prior.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6000(NZD382m). Upcoming Close Strikes : 0.5932(NZD317m July18). - BBG

- CFTC Data shows Asset Managers added slightly to their newly built longs in NZD +9229, the Leveraged community added slightly to their shorts last week -8654.

- AUD/NZD range for the session has been 1.0942 - 1.0970, currently trading 1.0970. The cross has broken out of its recent range and is now trying to push through the more pivotal 1.0950 area. Dips back to 1.0850/1.0900 should now be supported as the pair tries to build momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Taiwan, Indonesia Firmer, Philippines Down, Modest Shifts Elsewhere

Asian equities are trading in a mixed fashion so far in Wednesday trade. There is a modestly negative bias for US and EU futures as markets digest Tuesday's US CPI data. US Tsy yields are little changed so far today though. The best performer in the region has been Taiwan, while the Philippines bourse has fallen but close to 1.8%.

- China and Hong Kong markets are mixed. The CSI 3000 is down modestly, but still above 4000 at this stage. Sell-side analysts are upgrading their full year China growth projection after yesterday's Q2 GDP beat. Still, concerns around retail spend and the property sector is likely tempering optimism.

- The Hong Kong's HSI is marginally higher, last under 24700, which marked earlier highs for the index and coincided with highs back in March. We may need to see a fresh positive catalyst from here to propel sentiment higher.

- Japan markets are little changed, while Taiwan's Taiex has risen through 23000, last up nearly 1%. Broader tech optimism is aiding sentiment. Still, the Kospi is struggling so far today, the index back under 3200.

- In SEA, the Philippines market is off by around 1.8%, having failed to hold above 6500 in recent session. The firmer US yield backdrop, coupled with uncertainty around Fed easing timing, has pushed most USD/Asia pairs higher, which could also be weighing on market sentiment in the Philippines.

- Other trends are mixed, with Indonesian stocks up around 0.60%, aided by the 19% tariff deal with the US (which is lower than tariff rates in some other parts of the region).

ASIA STOCKS: Taiwan Inflows Buoyant Amid Tech Optimism, Outflows In India & SEA

Positive inflow momentum was a standout for Taiwan and South Korean markets yesterday. Sentiment around the AI/tech space was boosted by Nvidia resuming sales of a key chip to China (which was part of the broader US/China trade truce). Taiwan remains the best performer, with just under $1.8bn in net inflows in the past 5 trading days. Month to date, Taiwan has seen over $4.5bn in inflows. Tech equity bourses outperformed globally in Tuesday trade, although the firmer US yield backdrop (post the CPI outcome, which showed tariff effects emerging), has tempered sentiment in this space.

- Elsewhere, trends were mostly softer, with India unable to sustain a positive bounce from the end of last week.

- Recent positive momentum into Thailand cooled.

- Indonesian markets also continued to see outflow pressures, now at over $350mn in July to date. The overnight news of a 19% tariff deal with the US may help stabilize sentiment, at least on a relative value basis with tariff rates elsewhere in the region mostly higher.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 203 | 840 | -8137 |

| Taiwan (USDmn) | 710 | 1796 | -1395 |

| India (USDmn)* | -92 | -406 | -8420 |

| Indonesia (USDmn) | -20 | -108 | -3591 |

| Thailand (USDmn) | -18 | 97 | -2341 |

| Malaysia (USDmn) | -21 | -76 | -2813 |

| Philippines (USDmn) | -6 | -8 | -556 |

| Total (USDmn) | 756 | 2136 | -27254 |

| * Data Up To July 14 |

Source: Bloomberg Finance L.P./MNI

OIL: Modest Gain for Oil in Asia Today as Equities Mixed

- After two days of falls, oil ticked marginally higher in the Asia trading day today.

- WTI is up +0.39% at US$66.78 bbl

- Brent is up +0.22% at US$68.86 bbl.

- The price for brent futures is in backwardation at present, with some 90c of difference and points to the potential to pay a premium to ensure supply. Whilst this technical remains in place, oil could remain supported over the coming days.

- For the month WTI is up +2.7% and WTI up +1.7% as signs emerge that major economies are beginning to re-establish their oil reserves at lower prices.

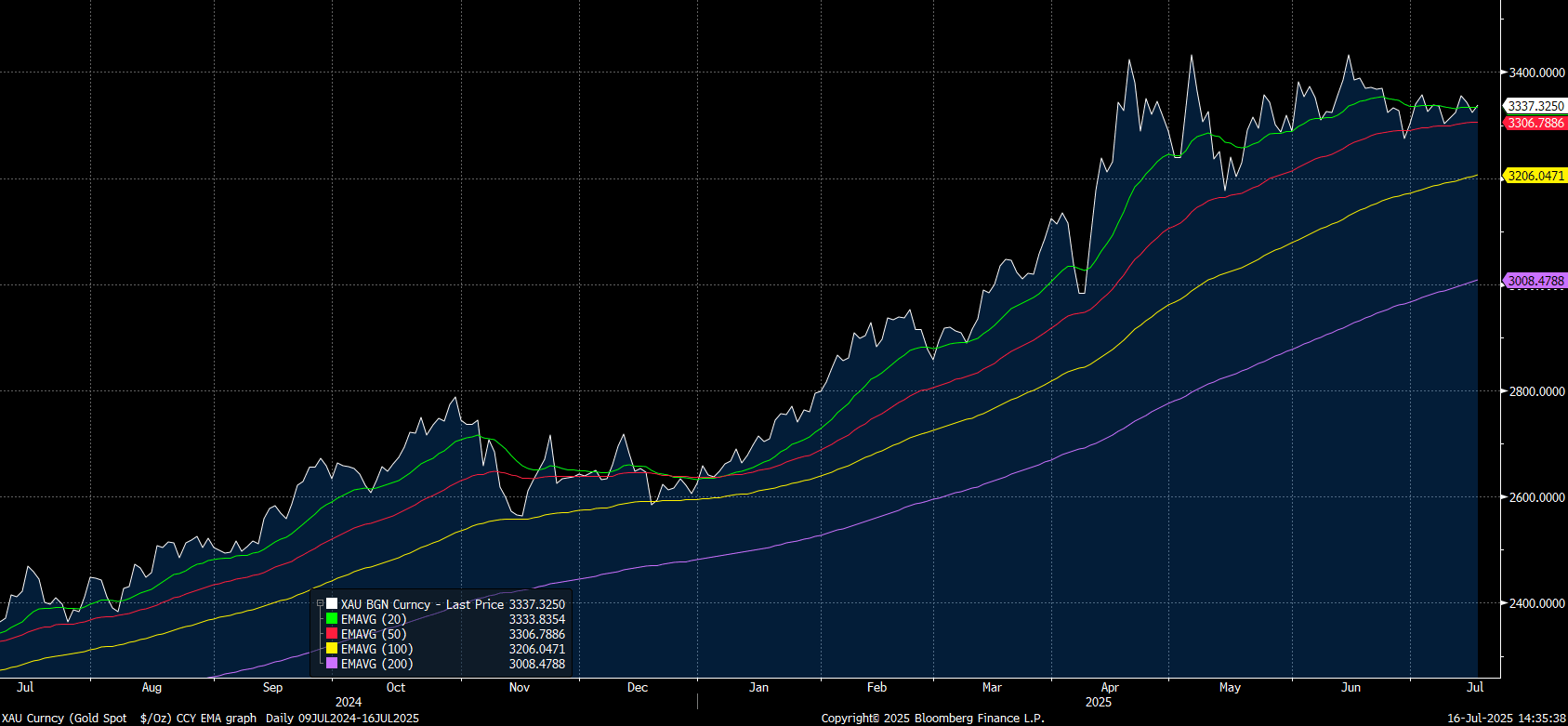

Gold Posts Modest Gains in Asia Trading Day

- Gold edged higher by +0.36% in the Asia trading day after two consecutive days of losses.

- At US$3,336.40 gold remains close to the June high of $3,3432.34.

- With the two day sell off, gold briefly dipped below the 20-day EMA of $3,333.78 but with today's gains trade back above all major moving averages.

Source: Bloomberg Finance LP / MNI

- Gold is up over 28% year to date with underlying options in exchange-traded SPDR gold shares indicating that bullish positioning relative to bearish ones has picked up considerably after reaching a low in early May. The improved sentiment suggests that some investors may be preparing for the next leg higher in the commodity with some forecasters saying that $4,000 is possible this year.

INDIA: Country Wrap: RBI Would Consider Further Cuts

- RBI governor Sanjay Malhotra said the central bank may consider cutting rates again if both inflation and growth slow, indicating that inflation could fall below the bank's forecast of 3.7% (source: Times of India)

- India's goods exports to the US rose by 23.53 per cent to USD 8.3 billion in June while imports dipped by 10.61 per cent to about USD 4 billion during the month, according to the commerce ministry data. During April-June, the country's exports to the US increased by 22.18 per cent to USD 25.51 billion, while imports rose 11.68 per cent to USD 12.86 billion, the data showed. (source Economic Times)

- After four consecutive days of losses, the NIFTY 50 finished ahead yesterday by +0.45% but unfortunately has turned down again in morning trade to be lower by -0.20%.

- The Rupee is flat at 85.82

- Bonds are doing very little with the 10yr at 6.31%

SOUTH KOREA: Country Wrap: Unemployment Rate Marginally Better

- Koo Yun-cheol, the nominee for deputy prime minister and minister of economy and finance, emphasized the need to capitalize on artificial intelligence (AI)-driven transformation to foster new industries, Tuesday, saying the “fate of Korea is at stake over AI and other advanced technologies.” “AI is not only essential to the competitiveness of individual industries, but also a critical foundation for enhancing productivity across the economy in the long term,” Koo said in a written answer submitted to the National Assembly for his confirmation hearing scheduled Thursday. (source Korea Times)

- Korea's unemployment rate for June saw a marginal improvement to +2.6% SA, from +2.7% in May. The economy added more than 180,000 jobs for the month, the sixth consecutive month of strong growth with the last month where net losses were recorded was December. Since then jobs increases has been 135k January, 136k February, 193k March, 194k April and 245k May to give a six month average of 158k. Employment in the manufacturing and construction sectors declined as the trade war impacts manufacturing and government policy aimed at slowing the housing boom comes into affect. (source MNI)

- The KOSPI finished yesterday strongly with gains of +0.41% but has given those gains and more back today to be lower by -0.86%.

- The Won is flat at 1,387.35

- Bonds are mixed across the curve with intermediate maturities rallying and 10yr + losing ground. The KTB10yr is at 2.88%

INDONESIA: Country Wrap: US Trade Deal Struck

- Indonesia’s labor-intensive industries such as textiles, footwear, and furniture risk losing global competitiveness due to the United States’ reciprocal tariff policies, according to the Indonesian Employers Association (Apindo). Apindo chairwoman Shinta Kamdani said Tuesday that the sectors most vulnerable to the US tariffs are those reliant on large labor forces, as these industries contribute significantly to Indonesia’s export market. (source Jakarta Globe)

- President Donald Trump said Tuesday that he had struck a trade pact with Indonesia resulting in significant purchase commitments from the Southeast Asian country, following negotiations to avoid steeper US tariffs. Indonesian goods entering the United States would face a 19 percent tariff, Trump said in a post on his Truth Social platform. This is significantly below a 32 percent level the president earlier threatened. (source Jakarta Post)

- The Jakarta Composite is up for the eight day straight, rising by +0.53% today. For the month it is over 3.6% better.

- The Rupiah is lower by -0.12% today at 16,287 but remains in a tight trading range.

- Bonds were marginallly weaker ahead of the Central Bank's decision later. Yields were marginally higher across the curve. The 10yr is 6.57%

ASIA FX: Little Shifts Post Tuesday Moves, USD/Asia Pairs Maintaining Uptrends

In North East Asia FX, aggregate FX moves remain modest at this stage. USD/CNH is holding above 7.1800, USD/KRW has tested higher, but with little follow through. TWD is down modestly, while USD/HKD remains close to the top end of the peg range despite further HKMA intervention.

- USD/CNH was last near 7.1840, little changed for the session. Sell-side analysts are more optimistic on the full year growth outlook for China, although equity market sentiment is struggling for fresh upside. CNH has notably outperformed this recent rebound in USD sentiment, with the USD/CNY fix only marginally above recent lows. For USD/CNH a move through the 7.2000 region may see bulls get interested again.

- Spot USD/KRW got to highs of 1389.5 in earlier dealings, but now sits back near 1388. We are close to June highs of 1391. A break above this level could the 1397/1400 region targeted, where the 100 and 200-day EMA resistance points rest. The uptrend in the pair remains intact, with yield differentials moving in favor of the USD. Earlier data showed a steady unemployment rate at 2.6%, while trade prices continued to fall, imports now off over 6%y/y.

- USD/TWD is holding above its 20-day EMA (near 29.32), the pair last close to 29.35. Outside of broader USD gains, seasonal headwinds in terms of dividend outflows may be a factor. Taiwan equities and offshore inflows are positives, but they haven't been enough to turn the pair back lower.

- Hibor rates have ticked higher following HKMA intervention, which will lower the aggregate balance, but USD/HKD spot remains wedged near 7.8500.

ASIA FX: USD/PHP Tests 200-day EMA Resistance, IDR Lower Despite US Trade Deal

In South East Asia FX, the bias has been for catch up to USD gains from Tuesday in spot markets. USD/PHP rose close to 57.00, before edging lower. IDR is off as well, despite getting a 19% tariff deal with the US. MYR and THB are down modestly versus the USD.

- USD/PHP probed above 57.00 in the first part of trade, which was testing 200-day EMA resistance in the pair. There didn't appear to be a fresh catalyst for today's move, outside of broader USD gains recently and the pick up in US yields. Philippines equities are also down sharply (off around 2%), adding to the USD support for the pair. We were last near 56.95.

- USD/IDR has climbed towards 16290, up around 0.20%. This comes despite securing a 19% tariff deal with the US, which is lower than a lot of other countries reciprocal tariff levels. Sell-side analysts see this as a positive for Indonesian assets. Local equities are up over 0.50% and focus will be on whether we see selling outflow pressures ease in this space. So far in July we have only seen one day of positive net inflows. The higher US yield backdrop is also likely curbing IDR gains.

- USD/THB is up around 0.20%, last in the 32.45/50 region. Fallout from delaying the decision on the new BoT Governor has been limited at this stage.

- USD/MYR was last around 4.2500. Recent highs in the pair have been around 4.2600, which is acting as a near term resistance point.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 16/07/2025 | 0600/0700 | *** | Consumer inflation report | |

| 16/07/2025 | 0800/1000 | *** | HICP (f) | |

| 16/07/2025 | 0900/1100 | * | Trade Balance | |

| 16/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 16/07/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/07/2025 | 1230/0830 | *** | PPI | |

| 16/07/2025 | 1230/0830 | *** | PPI | |

| 16/07/2025 | 1315/0915 | *** | Industrial Production | |

| 16/07/2025 | 1315/0915 | Cleveland Fed's Beth Hammack | ||

| 16/07/2025 | 1400/1000 | Fed Governor Michael Barr | ||

| 16/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 16/07/2025 | 1800/1400 | Fed Beige Book | ||

| 16/07/2025 | 2230/1830 | New York Fed's John Williams | ||

| 17/07/2025 | 0130/1130 | *** | Labor Force Survey | |

| 17/07/2025 | 0600/0700 | *** | Labour Market Survey | |

| 17/07/2025 | 0900/1100 | *** | HICP (f) | |

| 17/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/07/2025 | - | ECB Cipollone At G20 Meeting | ||

| 17/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 17/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 17/07/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/07/2025 | 1230/0830 | *** | Retail Sales | |

| 17/07/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/07/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 17/07/2025 | 1230/0830 | *** | Retail Sales |