ASIA STOCKS: Taiwan, Indonesia Firmer, Philippines Down, Modest Shifts Elsewhere

Asian equities are trading in a mixed fashion so far in Wednesday trade. There is a modestly negative bias for US and EU futures as markets digest Tuesday's US CPI data. US Tsy yields are little changed so far today though. The best performer in the region has been Taiwan, while the Philippines bourse has fallen but close to 1.8%.

- China and Hong Kong markets are mixed. The CSI 3000 is down modestly, but still above 4000 at this stage. Sell-side analysts are upgrading their full year China growth projection after yesterday's Q2 GDP beat. Still, concerns around retail spend and the property sector is likely tempering optimism.

- The Hong Kong's HSI is marginally higher, last under 24700, which marked earlier highs for the index and coincided with highs back in March. We may need to see a fresh positive catalyst from here to propel sentiment higher.

- Japan markets are little changed, while Taiwan's Taiex has risen through 23000, last up nearly 1%. Broader tech optimism is aiding sentiment. Still, the Kospi is struggling so far today, the index back under 3200.

- In SEA, the Philippines market is off by around 1.8%, having failed to hold above 6500 in recent session. The firmer US yield backdrop, coupled with uncertainty around Fed easing timing, has pushed most USD/Asia pairs higher, which could also be weighing on market sentiment in the Philippines.

- Other trends are mixed, with Indonesian stocks up around 0.60%, aided by the 19% tariff deal with the US (which is lower than tariff rates in some other parts of the region).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Bond Futures Rise

- China's bond futures are all higher today as the data suggests that any momentum in house prices and property investment may be stalling.

- The 10Yr future is up +0.03 at 109.03 and remains above all major moving averages. The nearest being the 20-day EMA at 108.88

- The 2Yr future is up +0.02 at 102.47 and is at the mid-point of the 20-day EMA at 102.43 and the 50-day EMA at 102.50

- The 10YR CGB is marginally lower in yield today at 1.69%

AUD: Asia Wrap - Drifts Lower

The AUD/USD has had a range of 0.6467 - 0.6496 in the Asia- Pac session, it is currently trading around 0.6475. The AUD has drifted a little lower for most of our session, -0.2%.

- Consensus Expects Labour Market Remained Tight In May. The highlight of the week, which doesn’t include many events, will be May jobs data. Bloomberg consensus is expecting that the status quo continued last month with Australia’s labour market remaining tight. A 20k rise in new jobs is forecast, in line with the 3-month average, with the unemployment and participation rates stable at 4.1% and 67.1% respectively.

- The AUD did well to hold above 0.6450 as risk came under pressure during the Friday session. The USD is still struggling to find any traction and as a result it still probably makes more sense to express any AUD weakness via the crosses until that changes.

- Price remains in the 0.6350 - 0.6550 range, a sustained break above 0.6550 is needed for the move higher to accelerate.

- Expect buyers to continue to be around on dips while the support in the AUD/USD holds, a close back below 0.6350 is needed to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6560(AUD549m), 0.6455(AUD476m). Upcoming Close Strikes : 0.6600(AUD 974m June 18)

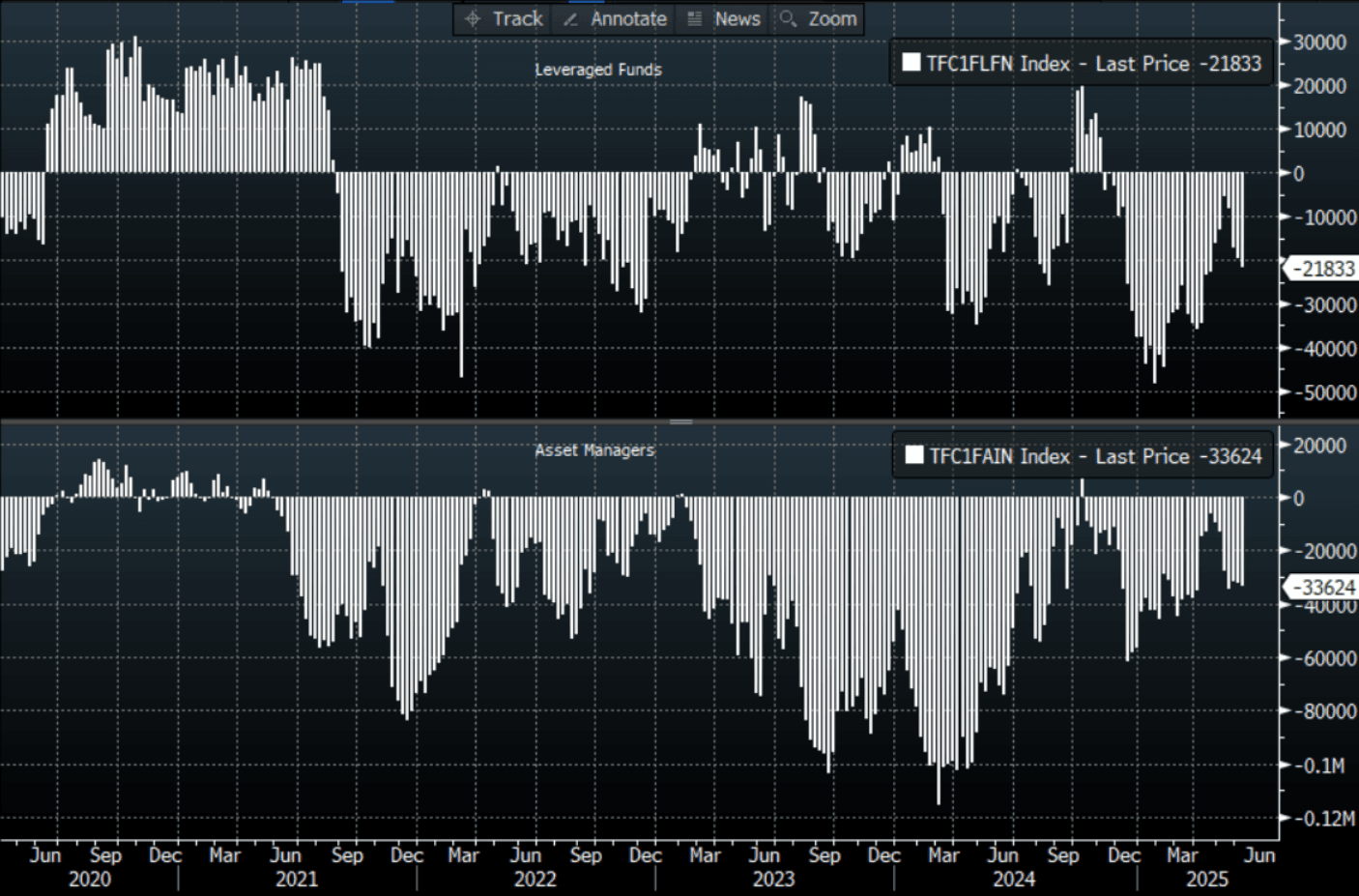

- CFTC Data shows Asset managers maintaining their shorts, the Leveraged community though continued to build up their shorts again.

AUD/JPY - Today's range 93.34 - 93.89, it is trading currently around 93.45. The price has topped out again towards 94.00 this morning after a big bounce off 92.50 overnight. A break back below 91.50/92.00 is needed to see the move lower regain momentum and the focus turn back to the year's lows again.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

STIR: BoJ Market Pricing: Wait-And-See Approach Still Priced

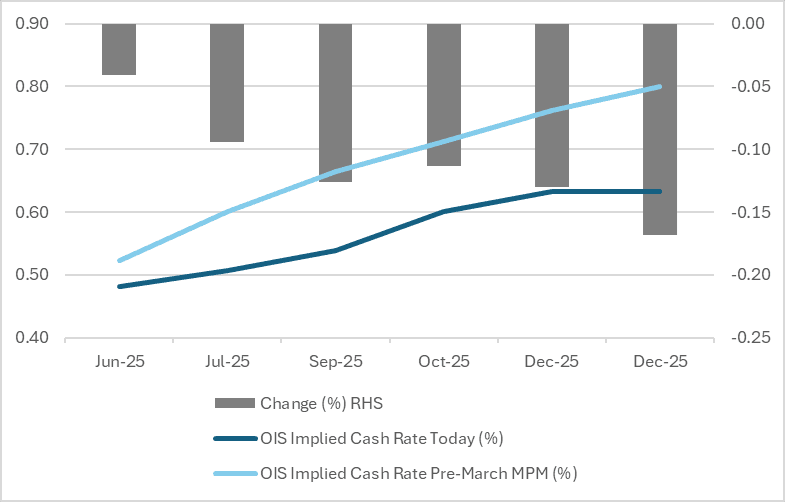

At the time of writing, BoJ-dated OIS pricing was 4–17bps softer across meetings compared to pre-March MPM levels, reflecting growing concerns over economic growth, driven largely by recent external shocks, particularly changes in US tariff policy.

- The BoJ is expected to keep its policy rate unchanged at 0.50% at its June 16-17 meeting. The key area of interest will be Governor Kazuo Ueda’s post-meeting press conference. Investors will closely examine his comments for any signals on the timing and likelihood of future rate hikes. The second area of market focus is on the BoJ’s JGB purchase program.

- Markets are positioned for a cautious, wait-and-see approach from the BoJ at this meeting.

- Current OIS pricing implies just a 2% probability of a 25bp hike this week, rising to 25% by September and 67% by December — a notable shift from mid-February, when a hike by September was fully priced in.

- For comparison, the market had been assigning a 47% chance of a September hike and a 62% probability by October going into the May 1 MPM decision.

Figure 1: BoJ-Dated OIS – Today Vs. Pre-March MPM

Source: Bloomberg Finance LP / MNI