ASIA FX: Little Shifts Post Tuesday Moves, USD/Asia Pairs Maintaining Uptrends

In North East Asia FX, aggregate FX moves remain modest at this stage. USD/CNH is holding above 7.1800, USD/KRW has tested higher, but with little follow through. TWD is down modestly, while USD/HKD remains close to the top end of the peg range despite further HKMA intervention.

- USD/CNH was last near 7.1840, little changed for the session. Sell-side analysts are more optimistic on the full year growth outlook for China, although equity market sentiment is struggling for fresh upside. CNH has notably outperformed this recent rebound in USD sentiment, with the USD/CNY fix only marginally above recent lows. For USD/CNH a move through the 7.2000 region may see bulls get interested again.

- Spot USD/KRW got to highs of 1389.5 in earlier dealings, but now sits back near 1388. We are close to June highs of 1391. A break above this level could the 1397/1400 region targeted, where the 100 and 200-day EMA resistance points rest. The uptrend in the pair remains intact, with yield differentials moving in favor of the USD. Earlier data showed a steady unemployment rate at 2.6%, while trade prices continued to fall, imports now off over 6%y/y.

- USD/TWD is holding above its 20-day EMA (near 29.32), the pair last close to 29.35. Outside of broader USD gains, seasonal headwinds in terms of dividend outflows may be a factor. Taiwan equities and offshore inflows are positives, but they haven't been enough to turn the pair back lower.

- Hibor rates have ticked higher following HKMA intervention, which will lower the aggregate balance, but USD/HKD spot remains wedged near 7.8500.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Asia FX Wrap - USD Consolidates

The BBDXY has had a range of 1202.92 - 1204.92 in the Asia-Pac session, it is currently trading around 1204. Japan and the EU plan to step up defense-industry cooperation, with officials and private-sector representatives set to meet Monday, Nikkei reported“(BBG). CHINA Retail Sales Strong with Urban Leading: The retail sales figures for May confirm the strength of the consumer that supports an improving domestic economy. Urban retail sales grew strongly, expanding by +6.5% whilst rural increased to +5.4%.

- EUR/USD - Asian range 1.1524 - 1.1548, Asia is currently trading 1.1535. EUR has rejected the move above 1.1600 but dips should continue to find demand, first support back towards the 1.1400 area then 1.1100/1200. EUR/USD looked to have broken the pivotal 1.1500 area last week, this needs to be sustained to signal a larger move higher.

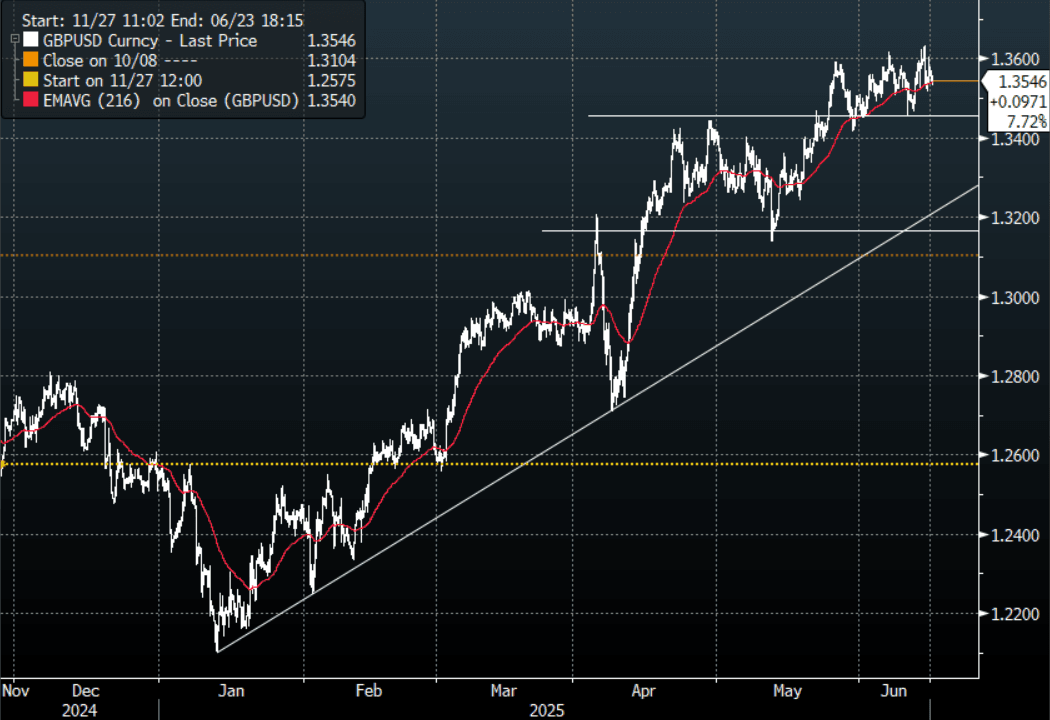

- GBP/USD - Asian range 1.3535 - 1.3567, Asia is currently dealing around 1.3545. The GBP looks to have failed to hold onto its upward momentum as it attempts to sustain a break above its pivotal Weekly resistance. First support seen back towards 1.3400/50.

- USD/CNH - Asian range 7.1843 - 7.1904, the USD/CNY fix printed 7.1789. Asia is currently dealing around 7.1850. Sellers should be around on bounces while price holds below the 7.2500 area.

- Cross asset : SPX +0.15%, Gold $3430, US 10-Year 4.425%, BBDXY 1204, Crude oil $73.80

Data/Events : Italy CPI, EZ Labour Costs

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGBS: Bear-Steepens, Global Bond Yields Push Higher, Q1 GDP On Thu

NZGBs closed at the session’s worst levels, showing a solid bear-steepening of the 2/10 curve. Benchmark yields rose by 3-8bps higher.

- BNZ’s manufacturing and services PMIs both deteriorated in May and are below the breakeven-50 level. Senior economist Steel warned that they are consistent with a return to a recession. With rates now in the “neutral zone” and the RBNZ Governor Hawkesby saying the MPC doesn’t have a bias, it looks like the RBNZ will be on hold on July 9.

- The focus of the week will be on Thursday’s Q1 GDP release. Bloomberg consensus is forecasting another 0.7% q/q increase in production-based GDP. Expenditure-based GDP should see a significant contribution from agricultural and services (tourism) exports.

- Swap rates closed 3-8bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed 1-5bps firmer across meetings. 4bps of easing is priced for July, with a cumulative 28bps by November 2025.

- Tomorrow, the local calendar will see Food Prices.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 2.75% Apr-37 bond and NZ$50mn of the 2.75% May-51 bond.

JPY: Asia Wrap - Tries Higher Finds Offers Back Towards 145.00 Again

The Asia-Pac USD/JPY range has been 143.97 - 144.75, Asia is currently trading around 144.35. USD/JPY has been better bid for most of our session as US yields extend their move higher and US Equity futures turn positive again after initially trying lower.

- “Japan and the EU plan to step up defense-industry cooperation, with officials and private-sector representatives set to meet Monday, Nikkei reported.”(BBG)

- The BoJ is expected to keep its policy rate unchanged at 0.50% at its June 16-17 meeting. The key area of interest will be Governor Kazuo Ueda's post-meeting press conference. Investors will closely examine his comments for any signals on the timing and likelihood of future rate hikes. If the BoJ begins to hint at stronger underlying inflationary trends or shows greater optimism about the economy, it could stoke expectations of a rate hike in the autumn.

- "JAPAN, US LEADERS ARRANGING TO MEET ON 17TH: KYODO" - BBG

- USD/JPY held its support back towards the 142.00 area once more, with oil surging again and US yields bouncing this pair has drifted back to the middle of its recent range.

- Price is back in its recent 142.00 - 147.00 range and will need a break either side of that to get a clearer direction. The larger interest around 145.00 looks to be rolling off tonight.

- The market still seems very confident of a move lower in USD/JPY but with positioning quite large now we have seen the risk of pullbacks increase. A break above 147.00 would be needed to challenge the conviction of any shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($4.87b). Upcoming Close Strikes : 143.00($692m June 18).

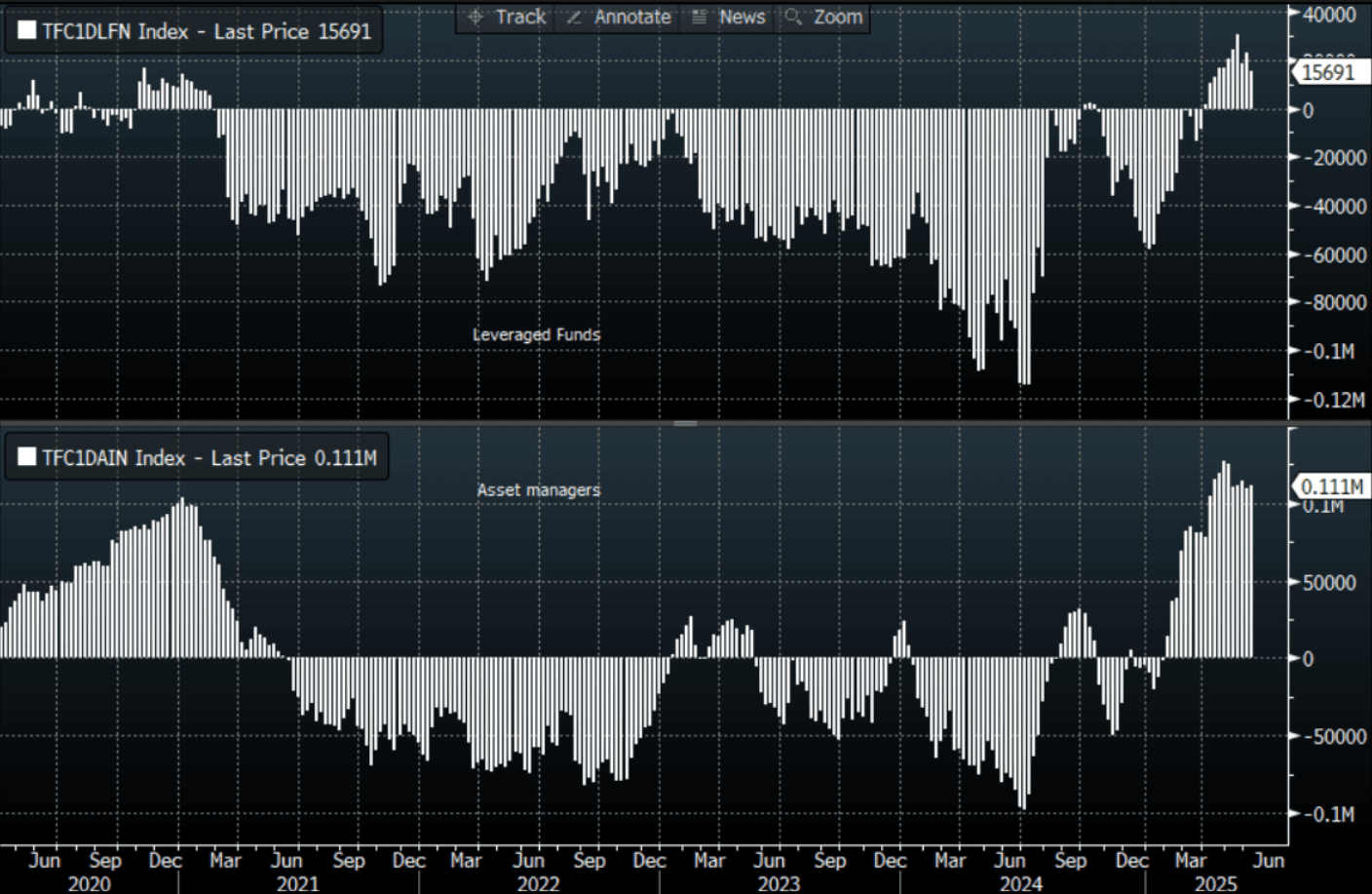

CFTC data shows Asset managers maintained their already extensive JPY longs, leveraged funds looked to have pared back their own longs once more.

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P