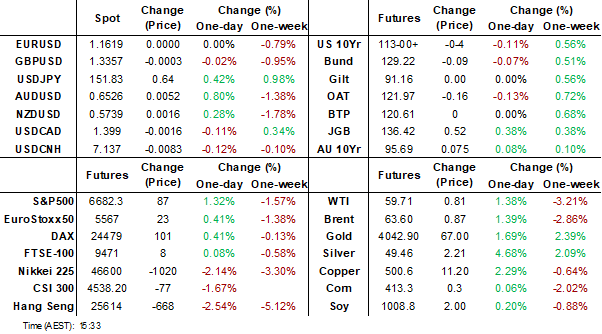

MNI EUROPEAN MARKETS ANALYSIS: Risk Sentiment Stabilizes

- Some clarification from China over the weekend on their new rare earth export controls has helped soften US rhetoric around the US-China trade/tariff outlook. Still, market sentiment remains cautious given the extent of losses seen in some markets On Friday. US equity futures are higher, but Eminis are still sub 6700, while US Tsy futures are down.

- The USD is weaker against higher beta plays, up against the yen. Gold and silver have tracked to fresh record highs.

- Regional equities are all in the red, with some Hong Kong indices starting to track under key EMAs. China exports held up in Sep, despite further weakness in US exports, suggesting China is successfully diversifying its export base.

- Later the Fed’s Paulson speaks. The US bond market is shut but equities are open. IMF/World Bank meetings are taking place. The ECB’s Buch and BoE’s Mann and Greene speak. Germany’s September WPI prints.

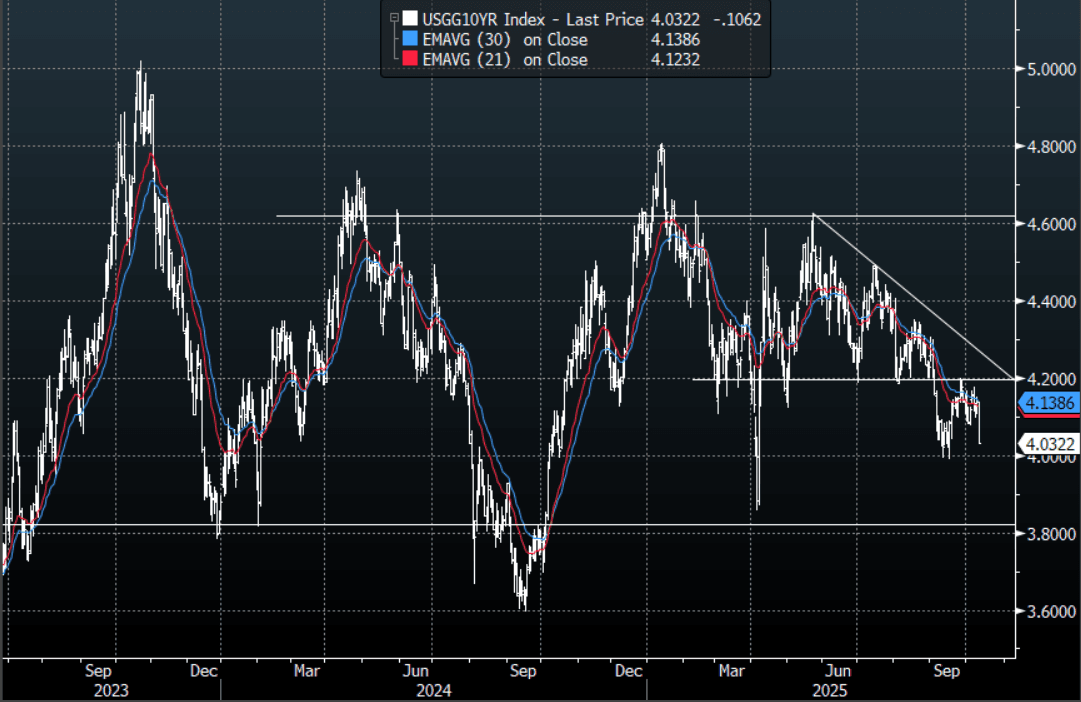

US TSYS: Futures Move Lower As Flare Up Is Trying To Be Walked Back

The TYZ5 range has been 112-30 to 113-03+ during the Asia-Pacific session. It last changed hands at 113-00, down 0-04+ from the previous close.

- 10-Year yields accelerated lower on Friday on the back of China/US Escalation. Some clarification from China over the weekend on their new rare earth export controls has seen the US walk back its aggressive stance and a more conciliatory tone is being set. I suspect a lot of Friday's moves will see some decent pullbacks on this, but how long it lasts is anybody's guess.

- The Cash Market was closed in Asia due to a Japanese Holiday.

- Robin Brooks wrote a substack expanding on how he thought markets might play out if the situation escalates again: “If the China-US trade war escalates and China devalues, there'll be lots of collateral damage: (i) US Treasury market will go "yippy" like in April; (ii) high-debt countries like Japan and France will suffer; (iii) $-pegs in Argentina and Turkey will blow.” https://t.co/Sh4nlrKDWC

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

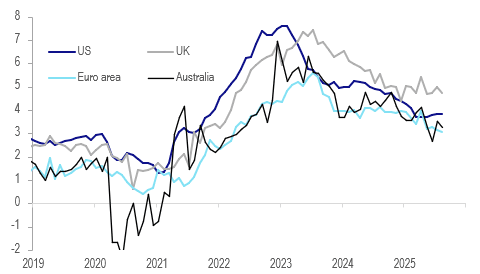

GLOBAL MACRO: Central Bankers Cautious On Stalling Services Disinflation

RBA Governor Bullock at the September 30 press conference and Kansas City Fed President Schmid (FOMC 2025 voter) last week commented on higher services inflation. Given that it reflects domestically-driven factors especially labour costs, as Bullock said, it is a key variable for central banks. They are also monitoring how it is behaving overseas and Bullock noted that it has been sticky and so the RBA needs to be careful. Q3 to date rose in the US and stabilised in the UK and Australia.

OECD services CPI y/y%

- Schmid said that services inflation has been higher than is consistent with meeting the 2% target. Bullock said in Australia that it has been a little higher than the RBA expected and that given its persistency overseas, the central bank will need to look at how far it moderates in its forecasts in the update due 4 November.

- Q3 average-to-date US services inflation is a little higher at 3.8% after 3.7% in Q2. September CPI was originally scheduled for 15 October but has been delayed to 24 October due to the government shutdown.

- Australia’s Q3 average monthly services CPI is steady at 3.4%, higher than the euro area and Canada but lower than the US, UK and Norway. The RBA focuses on quarterly data with Q3 due 29 October.

- UK Q3 average services inflation is stable at 4.9% suggesting that it has stalled at an elevated rate.

- Euro area services price pressures have moderated in Q3 to 3.1% after 3.5% in Q2 and Norway’s are also slightly lower at 3.75% compared to 3.9%.

- Canada is struggling with softer growth and higher unemployment and its services inflation moderated 0.5pp to 2.8% in Q3 to date, the lowest in our group, but even August was in line with July’s 2.8%.

AUSSIE BONDS: Key Resistance For Futures Remains Intact, RBA Mins Tomorrow

Aussie bond futures are holding higher, but away from best levels. Important key resistance points remain intact. 3yr futures were last 96.47 (+7bps), while 10yr futures were at 95.685 (+7bps). Earlier highs were at 96.505 for the 3yr and 95.7050 for the 10yr. Some cap for futures has come from the softer US Tsy futures tone and better risk appetite trends more broadly, with US official comments showing reduced recent rhetoric around US-China trade issues (albeit still with the threat of higher tariff levels come Nov 1, per remarks by US President Trump).

- Short term resistance points for futures are as follows. For 3yr: RES 1: 96.615 - High Sep 12 , while for 10yr: RES 1: 96.615 - High Sep 12.

- Cash ACGB yields are around 6-7bps lower across the curve, with the front end slightly weaker in yield terms. The 33yr benchmark last 3.50%, while the 10yr was at 4.29%, with little change in the Au3/10s curve.

- The bias is likely to be fade this yield move in Aussie, given RBA comfort around the current macro backdrop. A risk remains from higher US tariff levels on China, export controls etc, which could see negative spill over to the Australian economic outlook. For the 3yr Aussie bond, moves under 3.45% may be faded.

- At this stage, per Polymarket, 100% tariff odds by Nov 1 sit at 17%.

- Looking ahead to tomorrow, the publication of the September 30 decision minutes will be important given the Board’s more cautious tone and Bullock avoiding to state what the current stance is. She also noted that Board is concerned about certain CPI components including market services. NAB’s September business survey also prints on Tuesday.

BONDS: NZGBS: Yields Up From Lows, But Bearish Bias Intact Given Data

NZGB yields have pared losses as Monday's session has unfolded, consistent with improved risk appetite amid higher US equity futures and lower US Tsy futures. We were last 2-4.5bps weaker, led by the backend. Near term focus will remain on US-China tensions, as markets look for an off ramp to higher US tariff level and export controls. Comments from US officials up to President Trump hint at an openness to negotiate. Still, for NZGBs the risks remain for lower levels in yield terms, so long as domestic growth remains soft, something reinforced by today's data.

- The 2yr was last at 2.60% (today's low near 2.55%), the 10yr at 4.08% (today's low was under 4.04%). The 2/10s curve is around +148, flatter versus recent highs of +154bps.

- The 2yr swap rate got to lows of 2.355%, but we sit back at 2.38% in latest dealings, off close to 2bps for the session. In yield terms the 2yr swap rate is oversold, but upticks, particularly back towards 2.50% may be used as fresh entry points to express lower yield risks. Longer term trends still look for move into the 2.00-2.25% region, without a broader shift in the macro backdrop.

- On the data front, the BNZ services and manufacturing PMIs for September were consistent with the RBNZ’s assessment in its October statement that “economic activity recovered modestly in the September quarter”. The manufacturing sector stagnated in August/September, while services continued to contract but at a slower rate with September. Continued weak activity, including employment, at the end of the quarter is consistent with further RBNZ easing with policy likely to become stimulatory.

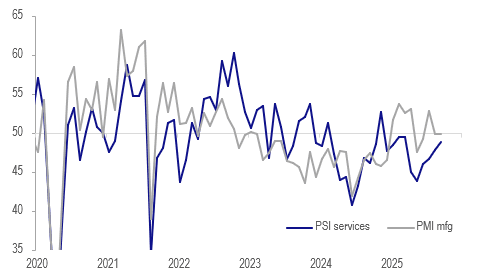

NEW ZEALAND: Services & Manufacturing Indices Signal Ongoing Weak Q3 Activity

The BNZ services and manufacturing PMIs for September were consistent with the RBNZ’s assessment in its October statement that “economic activity recovered modestly in the September quarter”. The manufacturing sector stagnated in August/September, while services continued to contract but at a slower rate with September up one point to 48.8, highest since March. Continued weak activity, including employment, at the end of the quarter is consistent with further RBNZ easing with policy likely to become stimulatory.

- The Q3 averages of the PMI and PSI show that there was some improvement in the quarter compared to Q2. Manufacturing rose 1 point to 50.9, slight growth, and services almost 3 points to 47.7, ongoing contraction.

- Forward-looking services orders rose to 51.4 from 47.8, the highest since November 2024. They continued to contract in Q3 overall at 48.6 but at a slower pace than Q2’s 45.5. Manufacturing saw an increase in orders in Q3 at 53.1 up from 49.5.

- Labour demand remained soft consistent with other data signaling a weak Q3 print on 5 November. September services employment fell to 47.8 from 48.7 with Q3 showing a further contraction in staffing at 47.6 (Q2 46.4). Manufacturing employment contracted too in the quarter.

NZ BNZ services vs manufacturing indices

Source: MNI - Market News/LSEG

FOREX: Asia-Pac: USD Drifts Lower

The BBDXY has had a range of 1211.98 - 1214.25 in the Asia-Pac session; it is currently trading around 1212, -0.10%. The USD correction higher stalled just as it began to probe its longer-term resistance. The 1215-1225 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the USD shorts. The weaker hands may be folding but I suspect we would need to do some work before the market can call a low for the USD as longer term accounts potentially look to fade this squeeze as they increase hedging ratios.

- EUR/USD - Asian range 1.1592 - 1.1628, Asia is currently trading 1.1620. Price found some decent demand towards its first support around the 1.1550 area; a break through here is needed to signal a deeper correction towards the more important 1.1200-1.1300 support. Expect sellers back towards the 1.1700 area first up.

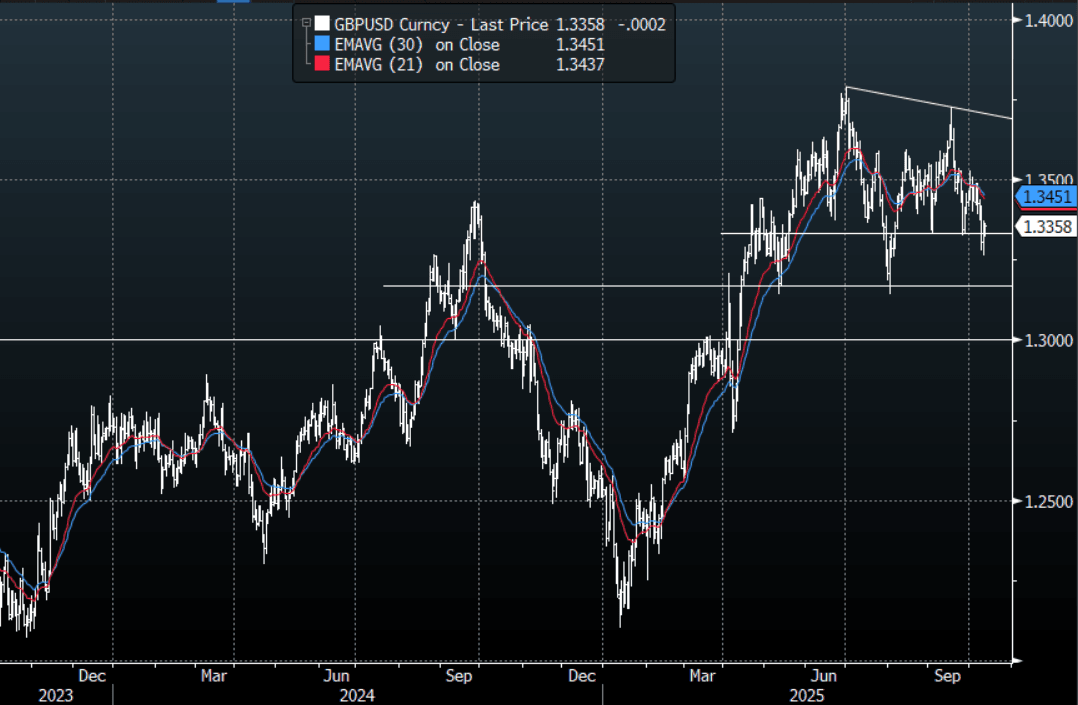

- GBP/USD - Asian range 1.3333 - 1.3363, Asia is currently dealing around 1.3360. The pair looks to have had a false break below the 1.3300 area. I suspect sellers should reemerge on any bounce back toward the 1.3450/1.3500 area.

- USD/CNH - Asian range 7.1320 - 7.1455, the USD/CNY fix printed lower at 7.1007, Asia is currently dealing around 7.1380. The area around 7.1500/1600 has proved to be solid resistance and with the PBOC managing the fix lower, it looks likely we could consolidate 7.09-7.16 for the moment.

- Cross asset : SPX +1.25%, Gold $4055, US TYZ5 112-31+, BBDXY 1212, Crude Oil $59.74

- Data/Events : Italy Bloomberg Oct. Italy Economic Survey, Germany Wholesale Price Index/Bloomberg Oct. Germany Economic Survey/Current Account Balance, EZ Bloomberg Oct. Eurozone Economic Survey, France Bloomberg Oct. France Economic Survey, Spain Bloomberg Oct. Spain Economic Survey

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia-Pac: USD/JPY Consolidates Around 152.00

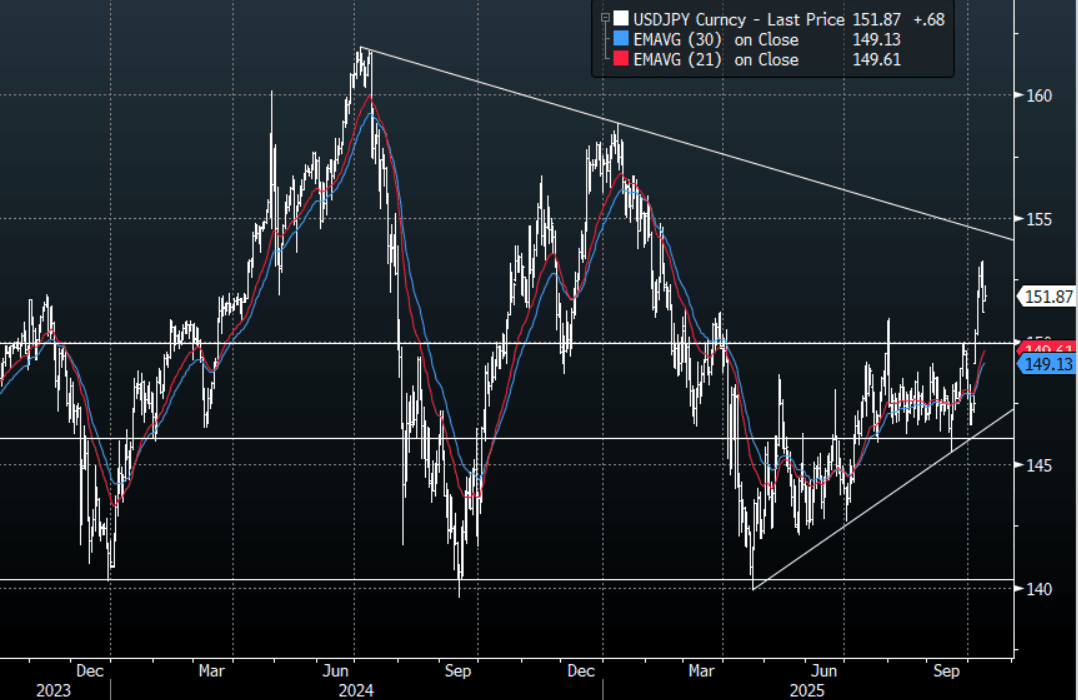

The USD/JPY range has been 151.74 - 152.28 in the Asia-Pac session, it is currently trading around 151.90, +0.45%. The pair collapsed with risk and US yields, and I am a little surprised the bounce this morning has not been bigger on the more conciliatory tone now being used. The Crypto market has led the retracement in risk higher over the weekend as the temperature was lowered, but the huge deleveraging of positions and the first crack in the markets conviction will be hard to just shake off. The JPY crosses in particular took the brunt of it on Friday and the rejections some pairs had look ugly. It will be interesting to see how the week starts and how much faith the markets have in those in charge to sort this mess out amicably. Technically dips back toward the 150/151 area should now find support first up.

- The FT is reporting the Dutch Government is taking control of the Chinese-owned chipmaker Nexperia, which could further inflame the situation. Arnaud Bertrand wrote a thread on X: “It invites retaliation from China, which is almost systematic. I wouldn't want to be a Dutch company with Chinese operations right now.”

- "KOMEITO DOESN'T RULE OUT OPPOSITION PARTY COOPERATION: KYODO" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 150.00($340m), 151.00($856m). Upcoming Close Strikes : 150.00($986m Oct 15) - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia-Pac: AUD/USD Bounces With Risk & A Lower CNY Fix

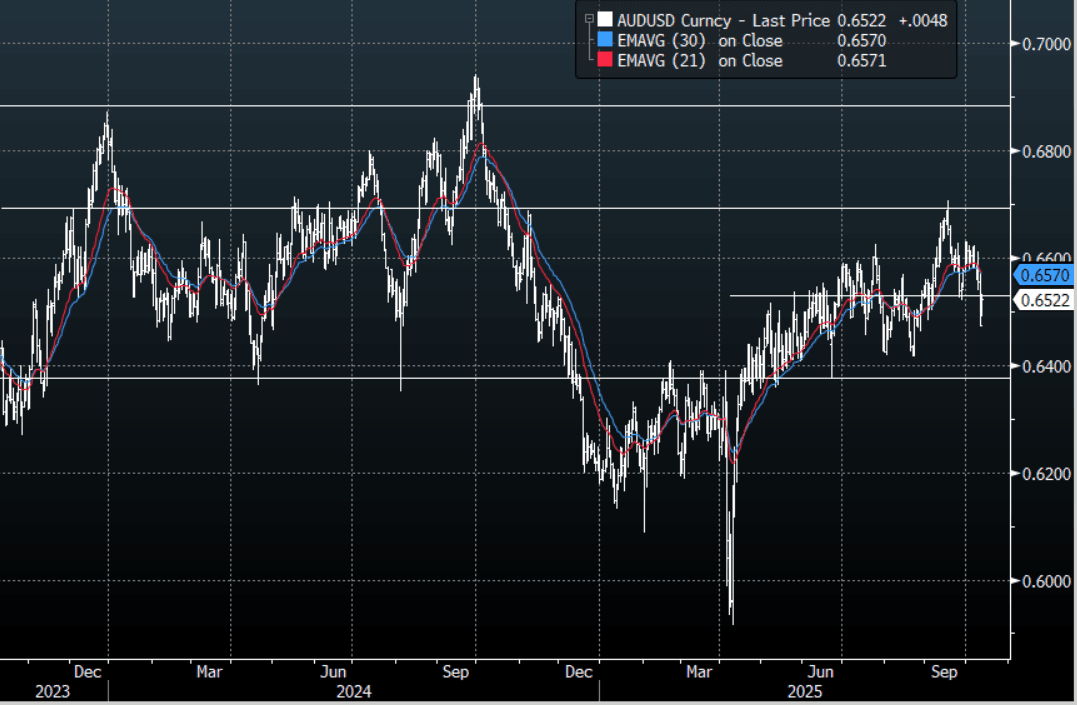

The AUD/USD has had a range of 0.6491 - 0.6533 in the Asia- Pac session, it is currently trading around 0.6520, +0.75%. Some clarification from China over the weekend on their new rare earth export controls has seen the US walk back its aggressive stance and a more conciliatory tone is being set. I suspect a lot of Friday's moves will see some decent pullbacks on this, but how long it lasts is anybody's guess. The AUD has gapped higher on the open and another very low CNY fix from the PBOC has underpinned the move for now. A lot of leverage would have been taken out last week and it's very hard for the market to just regain the conviction it previously had so I suspect the rally will stall at some point as those still overweight risk use the opportunity to pare back.

- The FT is reporting the Dutch Government is taking control of the Chinese-owned chipmaker Nexperia, which could further inflame the situation. Arnaud Bertrand wrote a thread on X: “It invites retaliation from China, which is almost systematic. I wouldn't want to be a Dutch company with Chinese operations right now.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6550(AD403m), 0.6555(AUD529m). Upcoming Close Strikes : 0.6500(AUD1.01b Oct 14), 0.6600(AUD948m Oct 14), 0.6650(AUD880m Oct 14) - BBG

- AUD/JPY - Asia-Pac range 98.57 - 99.23, Asia is trading around 99.05. The pair had an ugly rejection above 100. This morning the pair has bounced in sympathy with risk rallying, but it will need this move in risk to get back to the previous highs for it to look at breaking above 100 again.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia-Pac: NZD/USD Drifts Higher In Sympathy & Lower CNY Fix

The NZD/USD had a range of 0.5722 - 0.5745 in the Asia-Pac session, going into the London open trading around 0.5740, +0.30%. Some clarification from China over the weekend on their new rare earth export controls has seen the US walk back its aggressive stance and a more conciliatory tone is being set. I suspect a lot of Friday's moves will see some decent pullbacks on this, but how long it lasts is anybody's guess. The NZD has drifted higher from the open in sympathy to moves elsewhere and another very low CNY fix from the PBOC which has underpinned the move for now. The NZD had a poor weekly close though and technically remains a sell on rallies now for those looking for a currency to be short of in their basket. The sell zone remains back toward the 0.5800 area with the market looking for a potential move back towards the 0.5500/0.5600 area.

- MNI - Services & Manufacturing Indices Signal Ongoing Weak Q3 Activity. The BNZ services and manufacturing PMIs for September were consistent with the RBNZ’s assessment in its October statement that “economic activity recovered modestly in the September quarter”. Continued weak activity, including employment, at the end of the quarter is consistent with further RBNZ easing with policy likely to become stimulatory.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5850(NZD300m Oct 14), 0.5950(NZD312m Oct 16) - BBG

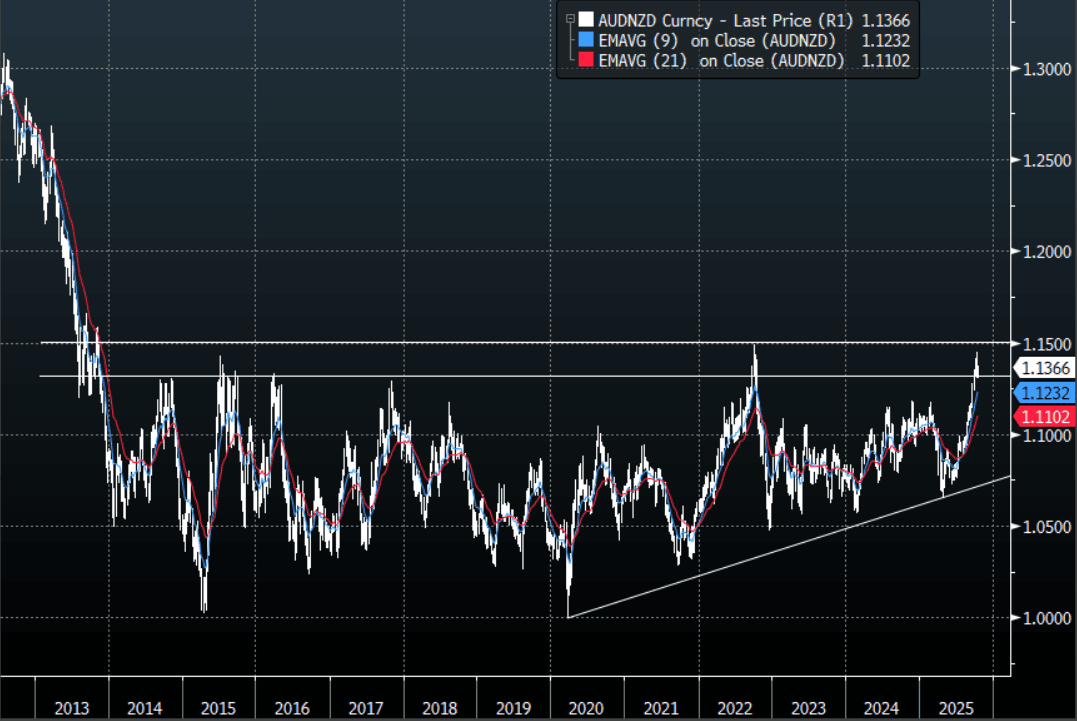

- AUD/NZD range for the session has been 1.1321 - 1.1373, currently trading around 1.1365. The Cross failed again above the 1.1400 area where I suspect initial paring back of longs. A clear sustained break above 1.15/1.16 resistance and the market will begin to think about levels back towards 1.2000 and above. Dips back toward 1.1200 should be a good place to start buying again if seen.

Fig 1: AUD/NZD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: As Trade War Intensifies, Equities Suffer (amended)

- With Japan out today, it was left to China's major bourses to guide sentiment as the trade war rhetoric ramps up. Having declined over -1.9% Friday, the CSI 300 started the week on the back foot, dragging the other key bourses with it. Down -1.7% today, it was the biggest two days of consecutive falls since April when the trade war began first ratcheted up. The Hang Seng fell sharply, down -3.3% as it traded through the key 20-day and 50-day EMA's and now is approaching the 100-day EMA which it last traded below in April. There was little positives to find as Shanghai Comp fell -1.30% and Shenzhen down -2.2%. The retail expansion of equity accounts over recent months has been a key contributor to the performance of stocks and comes on the back of a multi year decline in housing. The authorities will be loathe to see significant stock losses for investors and news agencies over the weekend were keen to spell out that the outlook for the CSI 300 should be little impact by the threats coming from Washington.

- Unsurprisingly the KOSPI followed China's lead and is down -1.6%. As always with market, context is key and the KPSPI hit new all time highs recently and any move lower is as much driven by the locking in of profits by investors, rather than a sea change in sentiment at this stage.

- With the JCI doing very little, South East Asia's other major bourse the FTSE Malay KLCI is down just over -0.50%. It has consistently underperformed the run up in equities in the recent period of strength and naturally its downside seems less pronounced.

- The focus on China arguably gives India a short respite having been in the sights of the US recently. The NIFTY 50 delivered a positive though modest week of gains last week, yet is giving some of those gains back in Monday morning trade.

OIL: Partial Recovery On Hopes Of US-China Trade De-escalation

Oil prices are 1.3% higher on Monday with some payback for Friday’s fall of around 5% plus also some relief from US/China comments on the weekend that the current trade issues can be resolved. Since President Trump’s announcement of tariffs at the start of the year, oil markets have been concerned about the impact of increased protectionism on energy demand at a time of excess supply.

- WTI is up 1.3% to $59.65/bbl off the intraday high of $60.01. Brent is 1.3% higher at $63.56 after reaching $63.84. The USD index is slightly lower also helping dollar-denominated crude.

- Trump sounded confident before flying to the Middle East that the trade issues with China can be resolved when he speaks with President Xi at the end of October. Xi stated that China will retaliate if the US imposes 100% tariffs on November 1.

- Risks remain around Ukraine-Russia with strikes continuing and Ukraine hitting a major Russian refinery on the weekend. President Zelenskyy also discussed longer-range Tomahawk missiles with Trump, which Russia sees as an escalation.

- Later the Fed’s Paulson speaks. The US bond market is shut but equities are open. IMF/World Bank meetings are taking place. The ECB’s Buch and BoE’s Mann and Greene speak. Germany’s September WPI prints.

GOLD: Trade Jitters Drive Safe-Haven Flows, New Highs For Gold & Silver

Gold fell early in the APAC session to $4006.48/oz on comments from US President Trump suggesting that the US-China trade situation may not be as severe as implied on Friday. However, it didn’t last and concerns that the trade war could be reignited as well as a lower US dollar drove gold just above last Wednesday’s record to $4060.01, opening resistance at $4074.5, a Fibonacci projection. It is currently 1.0% higher at $4057.4.

- Silver has rallied strongly with prices up 2.3% to $51.47, close to the intraday high and above resistance and all-time high at $51.235. It is also above a Fibonacci projection at $51.405 opening round number resistance at $52.00. It has been boosted not just by trade-related safe-haven flows but also by constrained liquidity in London. In addition, it remains unclear if it will be excluded from US import duties.

- Regional equities have sold off with the Hang Seng down 3.5% and ASX -1.0% but S&P e-mini up 1.2%. Oil prices are higher with WTI +1.4% to $59.73/bbl. Copper is up 2.0%.

- Later the Fed’s Paulson speaks. The US bond market is shut but equities are open. IMF/World Bank meetings are taking place. The ECB’s Buch and BoE’s Mann and Greene speak. Germany’s September WPI prints.

CHINA: September Exports Surge (Ex US) as Trade War Intensifies

- The moderation of exports in August was short-lived as September's numbers jumped +8.3% YoY, beating expectations and much stronger than the month prior.

- According to BBG estimates, the decline in exports to the US was significant, down -27% YoY. This points to the growth of demand from non US markets, arguably weakening the US's position in a trade war. Exports to Africa, India and other Asian nations are soaring with the latter back to pre-COVID levels.

- US President Donald Trump had threatened to raise tariffs on China and withdraw from a high-profile upcoming meeting with Chinese President Xi Jinping, in a lengthy statement on Truth Social, citing a letter from Beijing which he claims lays out new rare earth export control measures.

- The new Chinese rare earth export control measures are scheduled to take effect on December 1. Starting November 8, Beijing will also restrict exports of equipment needed to manufacture batteries for electric cars in a bid to protect the competitiveness of Chinese autos, per The New York Times.

- Imports climbed +7.4% in September for it's largest monthly expansion since April 2024. Despite being a crude indicator for domestic demand, the result nevertheless comes a an invaluable time as the US rhetoric ramps up.

- Along with the decline in exports to the US, imports from the US declined -16.1%, widening the trade surplus with the US to $22.bn.

- Whilst this data captures a period before the weekend's escalation it may slightly strengthen Beijing's position in negotiations, given the ever growing decline in the US's importance to China's trade outcome.

ASIA FX: Fresh Trade Tensions Being Expressed Through KRW, TWD, Not CNH

In North East Asia FX the bias has been for weaker KRW and TWD spot trends, but CNH has been resilient. US authorities (including US President Trump) still left the door ajar for talks/trade deal ahead of the Nov 1 tariff deadline (announced late last Friday), which has supported broader risk appetite. However, this hasn't done much for spot KRW and TWD, while USD/CNH sits under 7.1400. Local equities for these markets are off sharply today. The 1 month USD/KRW and USD/TWD NDFS sit sub end Friday levels though.

- The USD/CNY fix, a fresh low back to Nov last year, helped cap USD/CNH. We also had stronger than expected Sep export data, despite a sharp fall in exports to the US. This, along with other anecdotes suggests that China is quite comfortable with its current trade/external backdrop, particularly in terms of the US. Spot USD/CNY is around 7.1310/15, which is quite resilient, in light of higher USD levels in recent weeks and Trump's tariff threat.

- Spot USD/KRW got to fresh highs 1432.45, but sits back at 1428 in latest dealings. Proximity to China coupled with export control concerns in the tech space (from both the US and China sides) has weighed on local equities, down 1.5%. Spot USD/KRW has been capped though, with the authorities noting they are on the watch for herd like behavior in FX markets, which can sometimes signal a stronger intervention stance. We are still some distance from potential support though (with late Sep highs around the 1413/14 region potentially eyed). The 1month NDF is lower, last near

- Spot USD/TWD is up to 30.65, around 0.40% weaker in TWD terms versus end Friday levels. This brings early Sep highs around 30.75 into view. The 1 month NDF is off 0.15% last at 30.63. So today's spot move is largely catch up to Friday's USD gain in the NDF space.

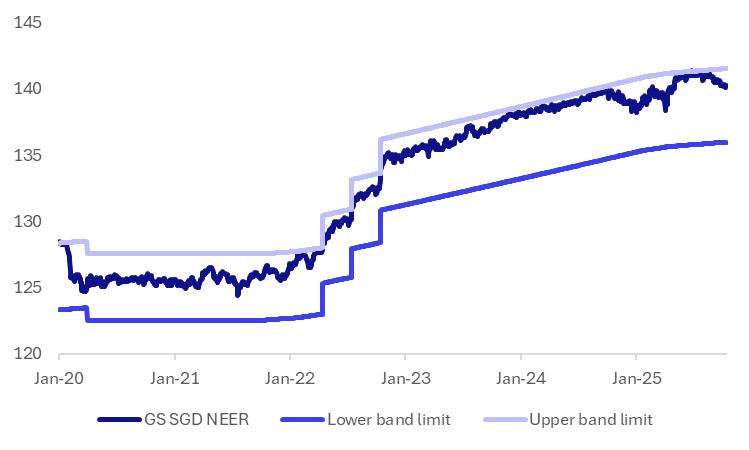

SINGAPORE: MAS Seen On Hold, But SGD NEER Away From Top End Of Policy Band

Tomorrow the MAS delivers its Oct policy meeting outcome. The broader market consensus is for no change, although some forecasters are calling for further easing. A Rtrs poll had 10 out of 14 analysts surveyed forecasting no change, while for BBG 16 out of 20 forecast no change. The resilient domestic growth backdrop is cited as a factor to stay on hold, along with easings already undertaken by the MAS (Jan and Apr of this year). It maintained a modestly positive SGD NEER slope. The bias in 2026 is for further easing though. Our bias is with no change, but it is likely to be a close call between the status quo and easing further.

- In terms of market pricing, we have seen some softness in the SGD NEER. The chart below plots the SGD against the upper and lower policy bands (per Goldman Sachs estimates). We are now around -0.90% from the top end of the band, which is still above cycle lows but we were around -0.60% from the top end of the band this time last month.

- We also get Q3 advanced GDP estimates tomorrow. The market expects 0.6%q/q growth after 1.4% in Q2. Measures of domestic activity have been holding up, but uncertainty rests with the external side. Our sense is the central bank is likely to wait until further evidence of weaker economic momentum before deciding to ease more. It does meet again in Jan 2026.

- From an inflation standpoint, pressures are quite modest and could provide further justification for easing (Core y/y at 0.3%, while headline is 0.5%). There doesn't appear to be a large disconnect though between SGD NEER y/y change and inflation trends.

- For USD/SGD, recent highs rest just short of the 200-day EMA (1.3015), which could be targeted on any dovish MAS surprise tomorrow. The 100-day EMA support point is back at 1.2910/15 (current spot is 1.2970).

Fig 1: Goldman Sachs SGD NEER Versus Upper & Lower Policy Bands

Source: Goldman Sachs/Bloomberg Finance L.P./MNI

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 13/10/2025 | 1105/1205 | BOE Greene at Society of Professional Economists Conference | ||

| 13/10/2025 | - | *** | Money Supply | |

| 13/10/2025 | - | *** | New Loans | |

| 13/10/2025 | - | *** | Social Financing | |

| 13/10/2025 | - | ECB Lagarde and Cipollone at IMF/World Bank Meetings | ||

| 13/10/2025 | 1655/1255 | Philly Fed's Anna Paulson | ||

| 13/10/2025 | 1910/2010 | BOE Mann in MonPol Panel, National Association of Business Economists | ||

| 14/10/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 14/10/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 14/10/2025 | 0750/0950 | ECB Cipollone Speech on Digital Euro | ||

| 14/10/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 14/10/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 14/10/2025 | - | ECB Lagarde and Cipollone at G20 Meeting | ||

| 14/10/2025 | 1200/1300 | BOE Taylor Remarks and Fireside Chat at University of Cambridge | ||

| 14/10/2025 | 1230/0830 | * | Building Permits | |

| 14/10/2025 | 1245/0845 | Fed Governor Michelle Bowman | ||

| 14/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index |