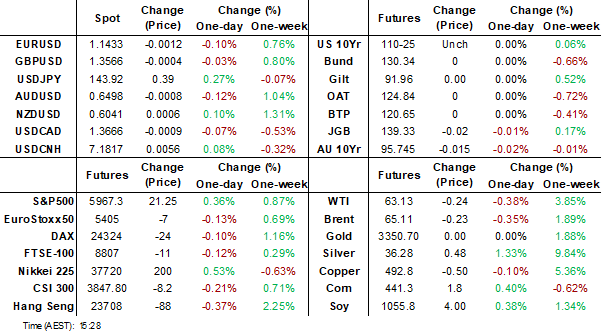

MNI EUROPEAN MARKETS ANALYSIS: RBI Surprises With 50bps Cut

- US Tsy yields are little changed as markets await the NFP print later. In the USD space, yen is down modestly, with little shifts elsewhere. Japan household spending data was softer than forecast, while US-Japan trade talks were held yesterday.

- US equity futures recovered from earlier weakness. US President Trump and Elon Musk are due to speak later Friday US time.

- The RBI surprised the market by cutting rates by 50bps but it did shift the policy stance to neutral.

MARKETS

US TSYS: Little Changed Going Into Today's US Payrolls Release

TYU5 is trading at 110-26, +0-00+ from closing levels in today's Asia-Pac session.

- Cash bonds are slightly mixed, with a steepening bias, after yesterday’s heavy session.

- The focus is on today's Non-Farm Payrolls release. US Non-Farm Payrolls are seen increasing a seasonally adjusted 126k in May in the Bloomberg survey after a stronger-than-expected 177k in April (albeit one that was more than offset by negative revisions).

- The unemployment rate is widely expected to round to 4.2% again.

- Average hourly earnings are expected to rise 0.3% M/M after a softer than expected 0.17% M/M in April, with the workweek watched after a recent recovery from January’s adverse weather lows.

- We expect greater sensitivity to a soft print in the event of a large surprise, although longer-term reaction would likely be capped by the FOMC not wanting a repeat of September’s (with hindsight) overreaction to a sharp but short-lived uplift in the unemeployment rate (See MNI US Payrolls Preview here)

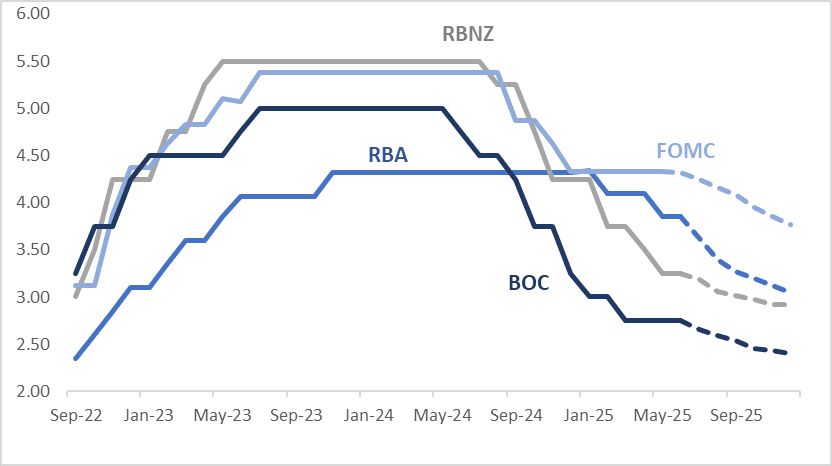

STIR: $-Bloc Sees Mixed Performance Over The Past Week

Interest rate expectations across dollar-bloc economies were mixed over the past week for December 2025. Canada stood out as the outlier, with a roughly 8bp increase in the expected year-end rate. In contrast, the US saw a 6bp decline, while Australia and New Zealand experienced more modest softening of 2–3bps.

- The Bank of Canada held its key interest rate at 2.75% for a second consecutive meeting on Wednesday. The decision to pause, rather than cut, was anticipated by a narrow majority of economists (12 out of 20), with few expecting a strong signal of easing later this year.

- While the Bank maintained language about the risks of slower growth and persistent inflation, it dropped a key line from April stating it was "prepared to act decisively" if the economic outlook became clearer, suggesting a more cautious, wait-and-see approach.

- In the US, the May ISM services report delivered a troubling mix: prices paid rose to their highest level since late 2022, while new orders fell to their lowest since the same period. The overall index dropped to its weakest level since June 2024, marking the first sub-50 reading in nearly a year. Meanwhile, ADP employment rose by just 37k in May, following a downwardly revised 60k gain in April (initially reported as 62k). Expectations for Friday’s private payrolls report currently stand at 120k. Additionally, the June Beige Book noted that “economic activity has declined slightly since the previous report” and flagged emerging inflationary pressures tied to rising tariffs.

- The next key event for the region is the FOMC’s June 18 policy meeting, where a 25bp rate cut is currently given a ~3% probability.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.77%, -56bps; Canada (BOC): 2.41%, -34bps; Australia (RBA): 3.05%, -80bps; and New Zealand (RBNZ): 2.92%, -34bps.

Figure 1: $-Bloc STIR (%)

Source: MNI – Market News / Bloomberg

JGBS: Cash Bond Bull-Flattener Pared Ahead Of US Payrolls

JGB futures modestly weaker, -7 compared to the settlement levels, but well off session cheaps.

- (Bloomberg) -- The US Treasury called on the Bank of Japan to raise interest rates to strengthen the yen, stepping much deeper into policy recommendations for Tokyo than before in its semi-annual currency report.

- “BOJ policy tightening should continue to proceed in response to domestic economic fundamentals, including growth and inflation, supporting a normalisation of the yen’s weakness against the dollar and a much-needed structural rebalancing of bilateral trade,” the Treasury Department said in a report released Thursday in Washington.

- Headlines crossed earlier from US President Trump when asked about the feud, stating it is fine. A call will reportedly take place between Trump and Musk on Friday US time.

- Cash US tsys are slightly mixed, with a steepening bias, ahead of Non-Farm Payrolls data.

- Cash JGBs are dealing mixed, with benchmark yields 1bp higher to 1bp lower. The benchmark 30-year yield is 0.4bps higher at 2.897% after being as low as 2.857% earlier.

- The swaps curve has bull-flattened, with rates 1-3bps lower.

- Tomorrow, BOJ Deputy Governor Uchida will give a speech at Japan Society of Monetary Economics. On Monday, the local calendar will see Q1 GDP (F), May Bank Lending and April Trade Balance data.

JAPAN DATA: Real Household Spending Back Negative In April, Below Forecasts

Japan April household spending was notably weaker than forecast, printing 0.1%y/y in real terms, versus a +1.5% consensus forecast (the March outcome was +2.1%y/y). Note spending was down 1.8%m/m. This outcome continues the recent see-saw y/y pattern for real spending. as we oscillate around flat (the Dec/Jan period we saw back to back positive gains).

- This print comes after yesterday's April labor earnings data, which showed headline outcomes slightly weaker than forecast. We did see scheduled pay (on a same base period) improve further but real earnings remain entrenched in negative territory.

- The chart below plots today's real spending outcome in y/y terms, against real labor earnings. All else equal it is difficult to see a sustained rise in real spending without positive real earnings growth. This remains a key policy focus point.

- In terms of the detail, food spending was 0.3%y/y in real terms, after a -0.7% print in March. The impact of surging rice prices has been noted by officials in terms of its inflationary impact and reducing spending power elsewhere. Fuel, furniture, clothing and medical care all recorded negative y/y prints.

Fig 1: Japan Real Household Spending & Real Labor Earnings - Y/Y

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: Cheaper But Narrow Ranges Ahead Of US Payrolls

ACGBs (YM -2.0 & XM -1.5) are modestly weaker, with narrow ranges, on a typical local data-light pre-US payrolls Friday.

- Cash US tsys are slightly mixed, with a steepening bias, after yesterday's heavy session. US Non-Farm Payrolls, due later today, are seen increasing a seasonally adjusted 126k in May in the Bloomberg survey after a stronger-than-expected 177k in April. The unemployment rate is widely expected to round to 4.2% again. (See MNI US Payrolls Preview here)

- Cash ACGBs are 1-3bps cheaper with the AU-US 10-year yield differential -13bps.

- The bills strip has bear-steepened, with pricing -1 to -4.

- “CBA views the RBA's 0.7% second quarter GDP forecast as overly optimistic given global uncertainty, with household consumption seen as key to recovery. A 25 basis point rate cut is likely in August, but July remains a possibility due to weak growth data, the report added.” (MTN via BBG)

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in July is given an 84% probability, with a cumulative 78bps of easing priced by year-end.

- Monday will see the King's Birthday Holiday except for WA & QLD.

- Next week, AOFM plans to sell A$1000mn of the 1.75% 21 November 2032 bond on Wednesday.

BONDS: NZGBS: Closed Cheaper & At Worst Levels Ahead Of US Payrolls

NZGBs closed 7-9bps cheaper and at/near the session’s worst levels on a local data-light day.

- On a relative basis as well, NZGBs delivered a poor performance. With the NZ-US & NZ-AU 10-year yield differentials closing 4bps and 8bps wider, respectively.

- Cash US tsys are slightly mixed, with a steepening bias, after yesterday's heavy session.

- The focus is on today's Non-Farm Payrolls release. US Non-Farm Payrolls are seen increasing a seasonally adjusted 126k in May in the Bloomberg survey after a stronger-than-expected 177k in April (albeit one that was more than offset by negative revisions). The unemployment rate is widely expected to round to 4.2% again. Average hourly earnings are expected to rise 0.3% M/M after a softer than expected 0.17% M/M in April, with the workweek watched after a recent recovery from January's adverse weather lows. (See MNI US Payrolls Preview here)

- Swap rates closed 5-7bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed 1-2bps firmer across meetings. 6bps of easing is priced for July, with a cumulative 32bps by November 2025.

- On Monday, the local calendar will see Mfg Activity data alongside a Radio NZ interview with RBNZ Chief Economist Paul Conway.

FOREX: USD Index Steady, Equity Futures Up From Earlier Lows, US NFP Later

Aggregate FX moves have been fairly modest in Friday trade to date, as markets await the US NFP print later. The BBDXY sits unchanged in latest dealings, close to 1208.15.

- US equity futures were weaker in the first part of trade but now sit back modestly in the green. We saw cash losses in Thursday trade amid the fallout from the Trump/Musk spat. Headlines crossed earlier from US President Trump when asked about the feud, stating it is fine. A call will reportedly take place between Trump and Musk Friday US time.

- US Tsy yields are little changed as the markets await the NFP print later.

- USD/JPY has drifted a little higher, last around 143.80/85, +0.20% versus end Thursday levels in the US. We haven't breached overnight highs of 143.97. Earlier we had softer than expected April real household spending, which followed yesterday's negative wages print.

- Japan's Akazawa met the US's Lutnick yesterday US time, speaking for 110mins. Japan again pressed the US for a review of tariffs, while also discussing non-trade barriers and expanding trade. BBG notes that Japan may seek tariff concessions by pledging to make more cars in the US and cooperate on rare earths (see this link) Japan also remains on the US Tsy's FX monitoring list.

- NZD has outperformed the AUD, but local news flows has been very light. NZD/USD is above 0.6040. AUD/USD is close to 0.500. The AUD/NZD cross is back to 1.0755, still up from recent lows.

- Looking ahead, the main focus will be on the US NFP print.

ASIA STOCKS: Stocks Falter into Week's End

As news filtered through of talks between President Trump and President Xi, it failed to bolster stocks as most major bourses fell in the Asia trading day. The markets seemingly have eyes for the non-farm payrolls tonight as a guide for the next direction in interest rates. With limited major economic data out today, eyes were turned to India where the RBI surprised markets, cutting by 50bps and the cash reserve ratio by 100bps in what could be interpreted as a warning to markets of tougher times for one of the world's biggest economies.

- The Hang Seng is down -0.21% today but up +2.4% for the week. CSI 300 -0.12% and +0.37% for the week. Shanghai Comp -0.06% today and +0.56% for the week. Shenzhen -0.14% today and +0.71% for the week.

- The KOSPI is closed today and up 4% for week, with 2 days closed for holidays.

- The FTSE Malay KLCI is down -0.10% today, and down -0.16% for the week.

- The Jakarta Composite is closed today and is down -0.86% for the week.

- Singapore's FTSE Straits Times is up +0.16% and +0.75% for the week whilst the PSEi in the Philippines is flat and down -0.56% for the week.

- India's NIFTY 50 is flat and little changed for the week..

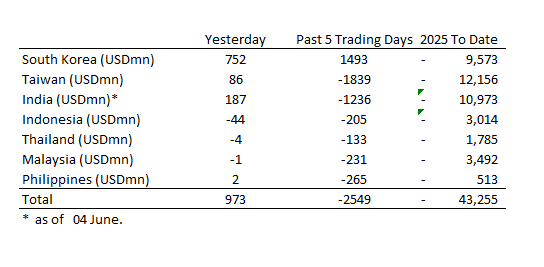

ASIA STOCKS: Large Outflows for the Week, Korea Bucking that Trend

Despite a relatively positive end to the week for flows, the damage was done early on with outflows topping US$2.5bn to Thursday.

- South Korea: Recorded inflows of +$752m yesterday, bringing the 5-day total to +$1,493m. 2025 to date flows are -$9,573. The 5-day average is +$299m, the 20-day average is +$124m and the 100-day average of -$96m.

- Taiwan: Had inflows of +$86m as yesterday, with total outflows of -$1,839 m over the past 5 days. YTD flows are negative at -$12,156. The 5-day average is -$368m, the 20-day average of +$160m and the 100-day average of -$127m.

- India: Had inflows of +$187m as of the 4th, with total outflows of -$1,236m over the past 5 days. YTD flows are negative -$10,973m. The 5-day average is -$247m, the 20-day average of +$14m and the 100-day average of -$109m.

- Indonesia: Had outflows of -$44m as of yesterday, with total outflows of -$205m over the prior five days. YTD flows are negative -$3,014m. The 5-day average is -$41m, the 20-day average +$2m and the 100-day average -$30m.

- Thailand: Recorded outflows of -$4m as of yesterday, outflows totaling -$133m over the past 5 days. YTD flows are negative at -$1,785m. The 5-day average is -$27m, the 20-day average of -$9m and the 100-day average of -$17m.

- Malaysia: Recorded outflows of -$1m as of yesterday, totaling -$231m over the past 5 days. YTD flows are negative at -$3,492m. The 5-day average is -$44m, the 20-day average of +$1m and the 100-day average of -$25m.

- Philippines: Saw inflows of +$2m yesterday, with net outflows of -$265m over the past 5 days. YTD flows are negative at -$513m. The 5-day average is -$53m, the 20-day average of -$14m the 100-day average of -$5m.

- China's official news agency Xinhua reported that US President Donald Trump and Chinese President Xi Jinping spoke Thursday with no conversation details provided. The conversation was a 90-minute discussion with Trump acknowledging that the trade relationship had 'gotten off track'. The call drove optimism with oil markets up on ideas that discussions could provide an pathway forward to resolution.

- WTI opened at US$63.26 bbl in Asia trading and is down -0.08% to $63.20. WTI is currently up for the week just under 4%

- Brent opened at US$65.26 bbl and is down -0.11% to $65.19. Brent is currently up just over 2% for the week.

- Saudi Arabia wants OPEC+ to continue with accelerated oil supply hikes in the coming months to regain lost market share. The kingdom wants the group to add at least 411,000 barrels a day in August and potentially September to take advantage of peak demand during the northern hemisphere summer. This comes as Russia's crude oil production for May was below its OPEC+ target.

- Global oil investments are expected to drop 6% in 2025, driven by economic uncertainties, lower demand expectations, and lower prices according to an IEA report.

- Oil markets will wait for Non-Farm payrolls tonight for a guide on the US economy and the direction of interest rates.

Gold Up as Equities Falter Friday

- As equities retreated into Friday, gold got a boost and is set to finish the week strongly.

- Gold rose +0.53% in the Asia trading day to US$3,370.42.

- Gold is currently up +2.51%, recovering all of the losses from the week prior.

- Yet another Central Bank reported an increase in reserves with the Bank of Ghana reporting that gold reserves increased to 32.16 tons in May.

- Gold remains above all major moving averages, the nearest being the 20-day EMA of $3,318.71.

- All major moving averages remain upward sloping, a sign that the bullish momentum remains for gold.

INDIA: Country Wrap: RBI Cuts Rates by 50bps

- The RBI surprised markets with a 50bps cuts on the back of ongoing softness in inflation, describing the fall as 'significant'. Given the outlook for monsoon season the RBI described the outlook for Core inflation as 'benign' and projects FY 2026 inflation at 3.7% (April CPI 3.16%). The RBI governor suggested that the growth / inflation dynamic called for front loading of cuts and puts monetary policy stance to neutral, suggesting that future cuts should not be expected. The RBI Governor described the global backdrop as fragile and highly fluid and that this last period of downward pressure on prices (CPI) being protracted. The Governor reminded that the starting point for India is good given the strength of balance sheets across sectors and that rural demand is steady urban demand is improving and investment spending is reviving. (source MNI Market News)

- RBI has surprised the market by cutting repo rate by 50 bps to 5.50% and CRR by 100 bps supporting the growth. In fact they have advanced the rate reduction and changed the outlook to neutral. Big booster to get growth back on fast track and positive for equity market outlook going forward.” (source BBG)

- India's NIFTY 50 is flat and little changed for the week.

- The rupee is flat today at 85.80 and for the week has lost ground by -0.25%

- Bonds have rallied on the RBI decision with the IGB10YR at 6.24% and down -4.5bps for the week.

CHINA: Country Wrap: XI and Trump Hold Talks

- Chinese President Xi Jinping said on Thursday that dialogue and cooperation are the only correct choice for China and the United States. In the phone talks initiated by U.S. President Donald Trump, Xi said that recalibrating the direction of the giant ship of China-U.S. relations requires the two sides to take the helm and set the right course, adding that it is particularly important to steer clear of the various disturbances and disruptions. (source XINHUA)

- n the first formal assessment of US trading partners’ foreign-exchange practices since President Donald Trump returned to office, the Treasury Department declined to name any country a currency manipulator while singling China out for “its lack of transparency.” The Treasury also said, in a semiannual foreign-exchange report released Thursday, it would strengthen its analysis of trading partners’ exchange-rate policies going forward. And it issued a stark warning against attempting to engage in “unfair” currency practices. (source BBG)

- The Hang Seng is down -0.21% today but up +2.4% for the week. CSI 300 -0.12% and +0.37% for the week. Shanghai Comp -0.06% today and +0.56% for the week. Shenzhen -0.14% today and +0.71% for the week.

- Yuan Reference Rate at 7.1845 Per USD; Estimate 7.1755

- China's 10YR government bond is ending the week where it started at 1.70% as the PBOC maintains a grip on liquidity.

MALAYSIA: Country Wrap: Local Banks See BNM Cutting Rates

- Petronas, Malaysia’s state-owned oil and gas company, will cut about 10% of its workforce in a firm-wide restructuring as it looks to reduce costs due to falling crude prices. The company will reduce headcount by more than 5,000 people, and all those affected will be informed in stages through next year, Chief Executive Officer said in a briefing and it will also freeze hiring until December 2026, he said. (source BBG)

- Local banks are positioning for a potential overnight policy rate (OPR) cut in the second half of the year by paring back deposit rates and recalibrating fixed deposit (FD) strategies. In April, total deposits grew 3.8% year-on-year (y-o-y) and 0.2% month-on-month (m-o-m), supported by current account savings account (CASA) growth of 4.5% and FD growth of 2.5%. The CASA ratio held relatively stable at 28.5%, slightly lower than 28.6% in March 2025 but up from 28.4% a year ago. (source The Star)

- The FTSE Malay KLCI is down -0.10% today, and down -0.16% for the week.

- The Malaysia Ringgit is weaker by -0.05% but better by +0.65% for the week at 4.2292

- Bonds have had a good end to the week with the MSG10YR down in yield to 3.54%, -5bps for the week.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 06/06/2025 | 0600/0800 | ** | Trade Balance | |

| 06/06/2025 | 0600/0800 | ** | Industrial Production | |

| 06/06/2025 | 0645/0845 | * | Industrial Production | |

| 06/06/2025 | 0645/0845 | * | Foreign Trade | |

| 06/06/2025 | 0830/1030 | ECB Lagarde Video Message For CIBP Anniv | ||

| 06/06/2025 | 0900/1100 | ** | Retail Sales | |

| 06/06/2025 | 0900/1100 | *** | GDP (final) | |

| 06/06/2025 | 0900/1100 | * | Employment | |

| 06/06/2025 | 1230/0830 | *** | Labour Force Survey | |

| 06/06/2025 | 1230/0830 | *** | Employment Report | |

| 06/06/2025 | 1230/0830 | *** | Labour Force Survey | |

| 06/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/06/2025 | 1900/1500 | * | Consumer Credit | |

| 07/06/2025 | 0730/0930 | ECB's Lagarde Speech In Monaco | ||

| 07/06/2025 | 0940/1140 | ECB's Schnabel in Dubrovnik panel discussion | ||

| 07/06/2025 | 0940/1040 | BOE Greene On Central Bank Decoupling Panel |