STIR: $-Bloc Sees Mixed Performance Over The Past Week

Jun-06 03:38

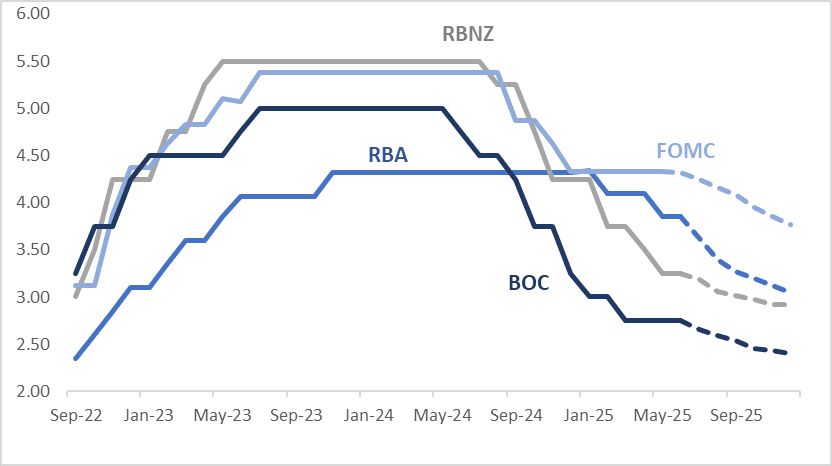

Interest rate expectations across dollar-bloc economies were mixed over the past week for December 2025. Canada stood out as the outlier, with a roughly 8bp increase in the expected year-end rate. In contrast, the US saw a 6bp decline, while Australia and New Zealand experienced more modest softening of 2–3bps.

- The Bank of Canada held its key interest rate at 2.75% for a second consecutive meeting on Wednesday. The decision to pause, rather than cut, was anticipated by a narrow majority of economists (12 out of 20), with few expecting a strong signal of easing later this year.

- While the Bank maintained language about the risks of slower growth and persistent inflation, it dropped a key line from April stating it was "prepared to act decisively" if the economic outlook became clearer, suggesting a more cautious, wait-and-see approach.

- In the US, the May ISM services report delivered a troubling mix: prices paid rose to their highest level since late 2022, while new orders fell to their lowest since the same period. The overall index dropped to its weakest level since June 2024, marking the first sub-50 reading in nearly a year. Meanwhile, ADP employment rose by just 37k in May, following a downwardly revised 60k gain in April (initially reported as 62k). Expectations for Friday’s private payrolls report currently stand at 120k. Additionally, the June Beige Book noted that “economic activity has declined slightly since the previous report” and flagged emerging inflationary pressures tied to rising tariffs.

- The next key event for the region is the FOMC’s June 18 policy meeting, where a 25bp rate cut is currently given a ~3% probability.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.77%, -56bps; Canada (BOC): 2.41%, -34bps; Australia (RBA): 3.05%, -80bps; and New Zealand (RBNZ): 2.92%, -34bps.

Figure 1: $-Bloc STIR (%)

Source: MNI – Market News / Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Bond Market Reaction to PBOC Announcement

May-07 03:25

- the various measures announced by the PBOC will have longer term implications for the bond market as financial institutions will likely be selling bonds held as reserves.

- This is a longer run story but could not doubt put upwards pressure on yields going forward.

- Bond futures have reacted to the announcement with the 10YR lower by -0.19 at 108.86. The move lower puts the 10YR in touching distance with the 20-day EMA of 108.80 which it hasn't trade through since early April.

- The 2YR bond future by contrast is unchanged at 102.322 and remains below all major moving averages. The nearest being the 20-day EMA at 102.40.

- The cash market is seeing yields higher with the CGB10YR up by +1bp at 1.64%.

- The next major test for the bond market will be Friday when the central government issues CNY71bn of 2055 and CNY170bn of 2026 bonds

CHINA: Measures Announced to Support Stocks

May-07 03:09

- In September the concept of the “national team” was created which effectively is key asset management companies through which support for equity markets will occur. Today sees the addition of two more entities being China Chengtong Holdings, China Reform Holdings and Central Huijin Investment Ltd.

- The PBOC also announced two new funding schemes of up to CNY800bn to support the stock market.

- These announcements aim to stabilize markets and expected to lower borrowing costs for those looking to invest in the stock market.

- The funding schemes will have lower interest rates than those on offer previously.

- The PBOC noted of their intention to support insurance companies in their investing in stock markets also

- The PBOC announced further support for Central Huijin Investment Ltd (a state owned investment company) to allow it to increase its index holdings in the stock market.

AUSSIE BONDS: Richer Despite Risk-On, PBoC Eases, US-CH Trade Talks

May-07 02:51

ACGBs (YM +7.0 & XM +6.5) are stronger on a local data-light session.

- The PBoC announced today a cut to the seven-day reverse repurchase rate to 1.4% from 1.5%. The change will come into effect from tomorrow.

- Markets have agonised for some time as to when there would be new measures announced by authorities to support the Chinese economy in a bid to ensure the 5% GDP growth target is achievable in the face of 145% tariffs from the US.

- Cash US tsys have twist-flattened, pivoting at the 20-year, with benchmark yields 2bps higher to 1bp lower.

- After the US close, risk appetite is firmer post-headlines of US-China officials to meet this week to discuss trade issues.

- The FOMC today will be watched closely, MNI Economist - "The FOMC will extend its series of rate holds to a third meeting in May, keeping the Fed funds target rate at 4.25-4.50% while maintaining its forward guidance in the Statement."

- Cash ACGBs are 6-7bps richer with the AU-US 10-year yield differential at -4bps.

- The bills strip has bull-flattened, with pricing flat to +8.

- RBA-dated OIS pricing is flat to 7bps softer across meetings today. A 50bp rate cut in May is given a 4% probability, with a cumulative 107bps of easing priced by year-end.