ECB: Is EURUSD Getting “Complicated” For the ECB? Not In Isolation

Jan-27 15:58

EURUSD’s push to fresh multi-year highs of 1.1955 may reignite concerns around exchange rate-driven downside inflation risks. This could have contributed to this afternoon’s light uptick in Euribor futures. However, we do not think recent FX moves are enough to motivate a wholesale ECB pivot at next Thursday’s decision/press conference. Domestic data should remain the primary focus, with Q4 flash GDP due on Friday alongside initial country-level January flash inflation readings.

- A reminder that in July 2025, ECB Vice President de Guindos suggested that a EURUSD rate above 1.20 could be “complicated”, owing to less competitive regional exports and weaker imported inflation trends. However, ECB speakers were careful to play down this signal in subsequent comments, stressing that the exchange rate is a factor that is monitored - but not targeted.

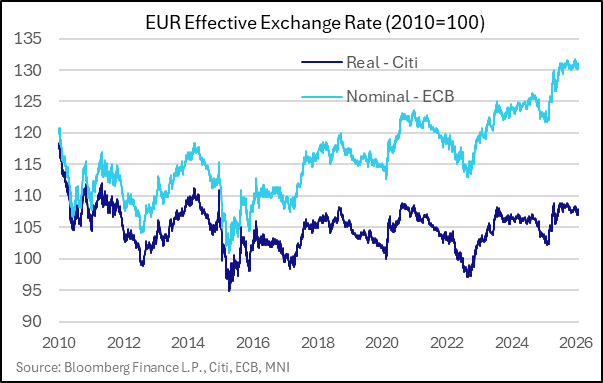

- Indeed, nominal and real EUR effective exchange rate indices have been relatively steady for several months now. We would likely need to see a renewed push higher (i.e. broad-based EUR strength) in these benchmarks before action is taken from the ECB.

- A reminder that risks stemming from Chinese trade remain a concern for the Governing Council, making EURCNY another important cross to monitor. The December meeting accounts noted that "The "second China shock" - referring to the country's increased global presence in more advanced products and technologies – was widely highlighted as a major challenge for the euro area economy”.

- EURCNY is currently close to – but importantly below – multi-year highs. From President Lagarde’s December press conference: “It's something we look at carefully, how currencies are positioned around the world. We pay attention to the position against the RMB as one of those.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Curves Twist Steeper, Quiet Return from Christmas Holiday

Dec-26 20:17

- Treasuries look to finish mixed Friday, curves twisting steeper with 2s-10s holding modestly higher vs. weaker Bonds after the bell.

- Currently, the TYH6 contract trades +2.5 at 112-19 vs. 112-23 early session high, on light post Christmas holiday volume of just over 650,000. 10Y yld near steady at 4.1336%. Key short-term resistance into 112-31, the Dec 18 high.

- Projected rate cut pricing gained vs. late Wednesday levels (*): Jan'26 at -5bp (-3.3bp), Mar'26 at -15.2bp (-12.3bp), Apr'26 at -21bp (-18.1bp), Jun'26 at -35.2bp (-31.1bp).

- US$ index near midrange after bouncing off midmorning lows, Bbg index BBDXY +0.21 at 1200.86

- Mining shares continued to buoy the Materials sector after Gold climbing to new record highs early Friday (4,549.92), trading desks citing an uptick in geopolitical tensions after Pres Trump launched attacks on Isis elements in Nigeria.

- Look Ahead: Monday data sees Pending Home Sales MoM (1000ET), Dallas Fed Mfg Activity (1030). COMC minutes for the December meeting to be released at 1400ET Tuesday.

US STOCKS: Late Equities Roundup: Miners Outperform as Gold Hits Record High

Dec-26 19:58

- Stocks hold near steady (SPX Eminis & Nasdaq) to weaker for the DJIA late Friday. Currently, the DJIA trades down 81.36 points (-0.17%) at 48652.31, S&P E-Mini Futures down 4.5 points (-0.06%) at 6978.5, Nasdaq up 16.4 points (0.1%) at 23629.91.

- Materials, Information Technology and Health Care sector shares led advances in late trade. Miners continued to buoy the Materials sector after Gold climbing to new record highs early Friday (4,549.92), trading desks citing an uptick in geopolitical tensions after Pres Trump launched attacks on Isis elements in Nigeria.

- Freeport-McMoRan +1.77%, Smurfit WestRock +1.14%, Newmont +0.78% and LyondellBasell Industries +0.72%.

- NVIDIA +1.88%, Crowdstrike Holdings +0.97%, Lam Research +0.94% and Dell Technologies +0.85%.

- Elevance Health +1.21%, Viatris +0.78%, UnitedHealth Group +0.71% and Baxter International +0.65%.

- Conversely, Energy sector and Utilities/Industrials shares led declines in the second half:

- Devon Energy -2.04%, APA Corp -1.64%, Diamondback Energy -1.23% and Occidental Petroleum -1.20%.

- Edison International -1.31%, Constellation Energy -1.29%, American Water Works -0.69% and Alliant Energy -0.61%.

- Huntington Ingalls Industries -1.18%, General Dynamics -1.08%, Axon Enterprise -1.07% and Northrop Grumman -1.06%.

US TSY OPTIONS: Apr'26 10Y Vol Sale

Dec-26 19:26

- -4,500 TYJ6 112/113 strangles, 134

Related bullets

Related by topic

EUR/USD

Bunds

Germany

Euribor

European Central Bank