MNI EUROPEAN MARKETS ANALYSIS: Nikkei Drops on UEDA Comments

- BOJ Governor UEDA said on Monday that the BOJ will consider the pros and cons of raising the policy interest rate and make decisions as appropriate at its Dec. 18-19 meeting, but that raising the policy interest rate under accommodative financial conditions should be seen as easing off the accelerator toward stable economic growth and price developments, rather than applying the brakes on economic activity.

- Rep. Don Bacon (R-Neb.) called Sunday on the Trump administration to refocus its energy on defending Ukraine’s sovereignty in peace talks with Russia (Per Politico).

- US stock futures and cryptocurrencies dropped, signaling risk aversion ahead of a slew of economic data this week even as bets for a December Federal Reserve interest-rate cut remain firm, with rate sensitive Asian bourses performing, whilst the NIKKEI was lower on the UEDA comments. The tech heavy bourses like Korea and Taiwan, followed Japan lower.

- Ahead tonight European PMIs are released, Italian and EU unemployment and US PMIs as the Fed Chair Powell speaks.

US TSYS: Bonds Weak; Long End Underperforming : 10-Yr Consolidates Above 4%

US bond futures were all lower today with the 10-Yr down -03 to 113-08. The 10-Yr retains its position above the 20-day EMA of 113-01+ as markets are set to start the trading week after the dis-jointed week last week due to holidays.

Cash was weak today with the long end underperforming.

- The 2-Yr is up +0.2bps at 3.496%

- The 5-Yr up +1.2bps at 3.61%

- The 10-Yr up +2.5bps at 4.044%

- The 30-Yr up +3.5bps at 4.701%

This week markets will look for any key messages from :

- Jerome H. Powell - Chair of the Fed - is slated to speak Monday at a panel discussion at Stanford.

- Michelle W. Bowman - Vice Chair for Supervision - is scheduled to give a speech this week (on bank supervision/regulation).

As the data flow continues, looking at the week ahead, the bond market will eye key data releases for potential further guidance on the upcoming rates decisions, specifically:

- Monday, December 1: ISM Manufacturing PMI, Construction Spending, and S&P Global Manufacturing PMI.

- Wednesday, December 3: ADP Employment Change, Industrial Production, Capacity Utilization, and ISM Services PMI.

- Thursday, December 4: Initial Jobless Claims and Continuing Jobless Claims.

- Friday, December 5: Personal Consumption Expenditures (PCE) price index, Personal Income, Personal Spending, and Michigan Consumer Sentiment.

For the issuance calendar overnight the focus for Monday will be Bill issuance with a 6-week maturity.

JGBS: Futures Testing Cycle Lows Post Ueda Speech, Dec Hike Odds Near 80%

JGB futures are holding close to session lows in latest dealings, last 134.50, -.63 versus settlement levels, as BoJ Governor Ueda said a rate hike in Dec would be considered. For 10yr futures, we are challenging the Nov 19 and cycle low of 134.56. A clean break lower points to the low 134.00 region , (with 134.04 being the 1.0% 10-day DMA envelope). Market implied BoJ rates for the Dec meeting sit around 0.675%, (roughly a 79% chance of hike in Dec). We were at 0.535% this time last week.

- Bank of Japan Governor Kazuo Ueda said on Monday that the BOJ will consider the pros and cons of raising the policy interest rate and make decisions as appropriate at its Dec. 18-19 meeting. He added that that raising the policy interest rate under accommodative financial conditions should be seen as easing off the accelerator toward stable economic growth and price developments, rather than applying the brakes on economic activity.

- Ueda also expressed confidence in the wages outlook, while noting downside risks for both the US and Japan economies have lessened.

- In the cash JGB space we are around 5-6bps higher for 5-20yr tenors. The 10yr outright yield is at 1.86%, fresh cycle highs. The 2yr is around 1.00%, while the 30 is up 4bps to 3.39%. Th 2/30s curve is little changed at +237.5bps.

- Earlier data on Capex was weaker than forecast but was largely ignored by the market.

- Note tomorrow we have a 10yr JGB auction.

AUSSIE BONDS: 10yr Futures Break Lower Amid Broader Moves, More GDP Partials Tue

Futures are weaker, led by the back end, with the 10yr (XM) off 4bps to 95.435, while the 3yr (YM) is down 2bps to 96.075. For the 10yr this is fresh lows since early Jan this year. The Jan 14 low was 95.30 in terms of a downside target. For the 3yr we are eyeing a test under 96.00. Broader bond futures have been softer in the US, likely seeing negative spill over to Australia, while JGB futures are also down as BoJ Governor Ueda said a Dec hike would be considered. The AU-US 10yr spread has been relatively steady today, around +51bps, just off recent highs.

- The cash ACGB 3yr yield was near 3.89%, with 4.00% an upside target if current trends persist. The 10yr is up to 4.55%, leaving the 3/10s curve at +66bps, slightly steeper for the day.

- On the data front today, Q3 Australian company profits were weaker than expected posting a flat outcome on the quarter after Q2’s sharp fall of 2.6% q/q and are now up only 1.1% y/y (strongest since Q1 2023 though). Inventory volumes fell 0.9% q/q which is likely to be a small detraction from Q3 GDP growth currently expected to rise 0.7% q/q and released on Wednesday. The net export and public demand contributions are released Tuesday.

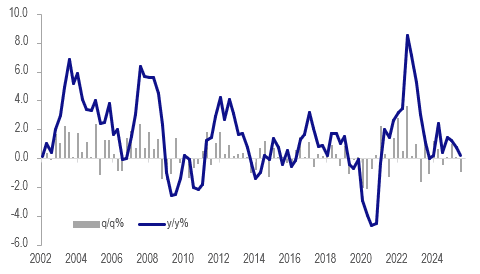

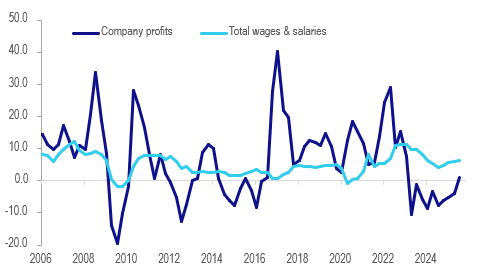

AUSTRALIA DATA: Wages Bill Continues Rising, Q3 Inventories Flat

Q3 Australian company profits were weaker than expected posting a flat outcome on the quarter after Q2’s sharp fall of 2.6% q/q and are now up only 1.1% y/y (strongest since Q1 2023 though). Inventory volumes fell 0.9% q/q which is likely to be a small detraction from Q3 GDP growth currently expected to rise 0.7% q/q and released on Wednesday. The net export and public demand contributions are released Tuesday.

Australia inventories %

Source: MNI - Market News/LSEG

- The decline in inventory volumes was mainly driven by a 4.8% q/q drop in the mining sector but retail was also 1.6% lower, which could reflect stronger-than-expected demand but also less purchasing driven by less optimistic confidence in the outlook.

- Total wages & salaries rose 1.5% q/q to be up 6.3% y/y in Q3, the highest since Q1 2024.

- Mining profits were up 0.2% q/q but wages fell 0.8%. Sales volumes rose 1.5% q/q.

Australia company profits vs wages & salaries y/y%

Source: MNI - Market News/LSEG

BONDS: NZGBS: Yield Rise Continues But 2yr Lags, NZ-US 10yr Eyeing +30bps Test

A steeper NZGB curve is the feature of Monday NZGB trading, the 2/10s last near +157bps, closing back in on recent Nov highs near +160bps. The 2yr outright yield is softer by around 2bps, last near 2.73%, while the 10yr is up a further 6bps to around 4.30%. Asia Pac fixed income markets have mostly seen higher yields today, with Japan in focus after BoJ Governor Ueda stated a Dec hike would be considered. US Tsy yields have also ticked higher, led by the back end.

- The NZ-US 10-yr spread remains biased higher, last near +28bps. Focus will be on whether we can test through +30bps, which marked recent highs. This will be a key if we continue to see divergences between the monetary policy outlooks in NZ and the US.

- For NZGB yields, the 10yr is now back to levels that prevailed in mid Sep. We are through all key EMAs, except for the 200-day (near 4.34/4.35%).

- On the data front earlier we had softer Oct building permits but this was after a strong Sep. Tomorrow Q3 NZ terms of trade prints.

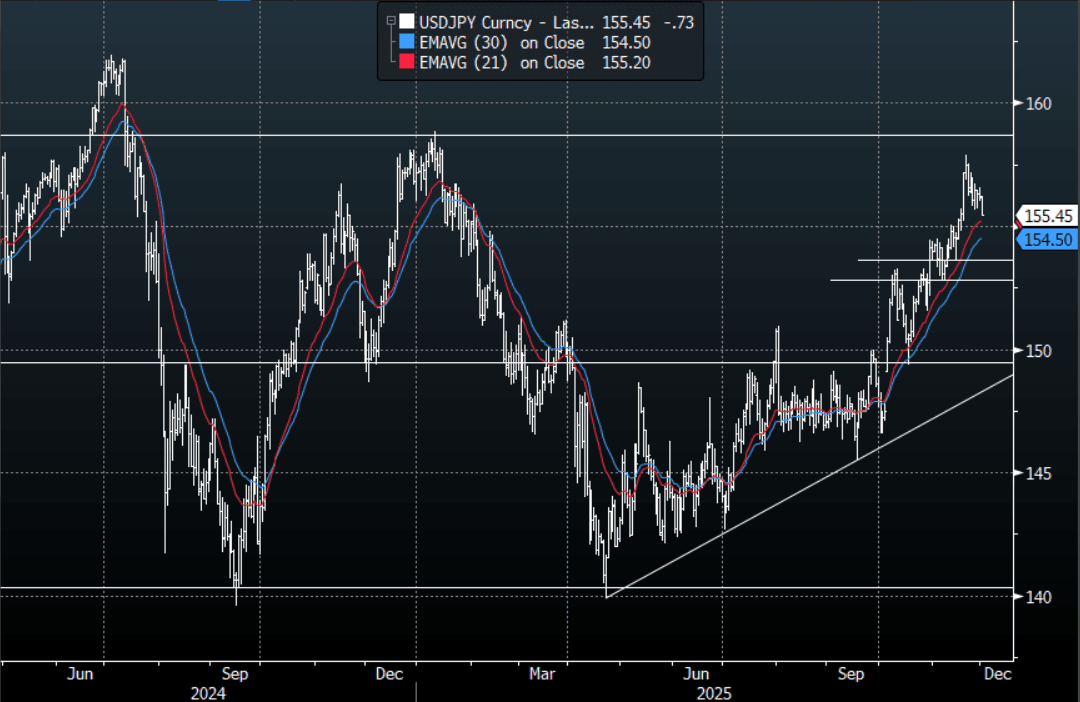

JPY: USD/JPY - Breaks Back Below 156.00 As Ueda Signals Dec Hike Possible

The USD/JPY range today has been 155.43 - 156.20 in the Asia-Pac session, it is currently trading around 155.50, -0.45%. The pair has fallen away as Ueda puts a rate hike in December on the table, Japanese yields are extending higher and have put a real dampener on risk across the board. The move in the Yen looks like it might force the BOJ into action in December and with Hassett now the leading front-runner to replace Powell so is the market's confidence for US cuts. This is having an impact or at least slow what looked like a situation that was about to get out hand. Technically this pullback looks like it could have more to go, especially if the risk-off start to the week grows. The first big support is back toward the 153.00-155.00 area where I suspect buyers will remerge. On the day I suspect rallies will remain heavy in the short term while below the 156.20-156.50 area.

- MNI: BOJ's Ueda Says Raising Rate Will Not Slow Economy. He said on Monday that raising the policy interest rate under accommodative financial conditions should be seen as easing off the accelerator toward stable economic growth and price developments, rather than applying the brakes on economic activity. Ueda also expressed confidence in continued wage growth, saying that corporate profits, the source of wage hikes, are expected to remain high overall even after taking into account the impact of tariff policies

- (Bloomberg) -- Japan’s Ministry of Finance will auction about ¥2,600 billion of 2035 bonds on Tuesday and then ¥700 billion maturing 205

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.00($744m),156.00($794m). Upcoming Close Strikes : 153.00($1.2b Dec 4), 155.00($2.25b Dec 2) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 94 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

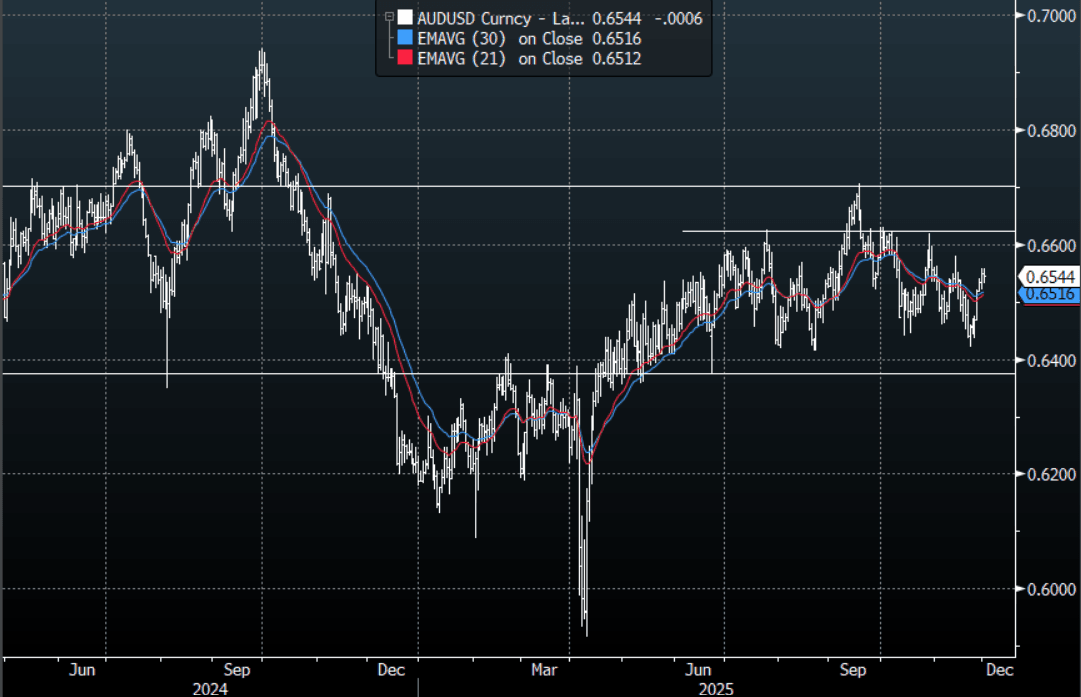

AUD/USD - Treads Water Around 0.6550, Ignores Risk-Off For Now

The AUD/USD has had a range today of 0.6531 - 0.6557 in the Asia- Pac session, it is currently trading around 0.6545, -0.10%. The AUD/USD has had a subdued session considering the risk-off start to the week. Asia has broadly sold the USD as USD/JPY trades lower, but if this risk-off start to the week turns into something more I would look for the USD to potentially bounce against risk currencies. The AUD is consolidating around 0.6550 just below the pivot toward 0.6550-60 within its wider 0.6350-0.6700 range. On the day, I would not be surprised to see the AUD/USD drift back toward the 0.6490-0.6510 area on the back of this shaky start to the week.

- MNI POLICY: RBA Sees Balanced Risk, Despite Monthly CPI Shock. The Reserve Bank of Australia continues to view the 3.6% cash rate as somewhat restrictive, despite recent strong inflation data, including October’s monthly print, which policymakers will largely look through, MNI understands.

- MNI AU - Wages Bill Continues Rising, Q3 Inventories Flat: Q3 Australian company profits were weaker than expected posting a flat outcome on the quarter after Q2’s sharp fall of 2.6% q/q and are now up only 1.1% y/y (strongest since Q1 2023 though). Inventory volumes fell 0.9% q/q which is likely to be a small detraction from Q3 GDP growth currently expected to rise 0.7% q/q and released on Wednesday. The net export and public demand contributions are released Tuesday.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6400(AUD445m), 0.6425(AUD444m), 0.6550(AUD521m). Upcoming Close Strikes : 0.6490(AUD710m Dec 4) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 39 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

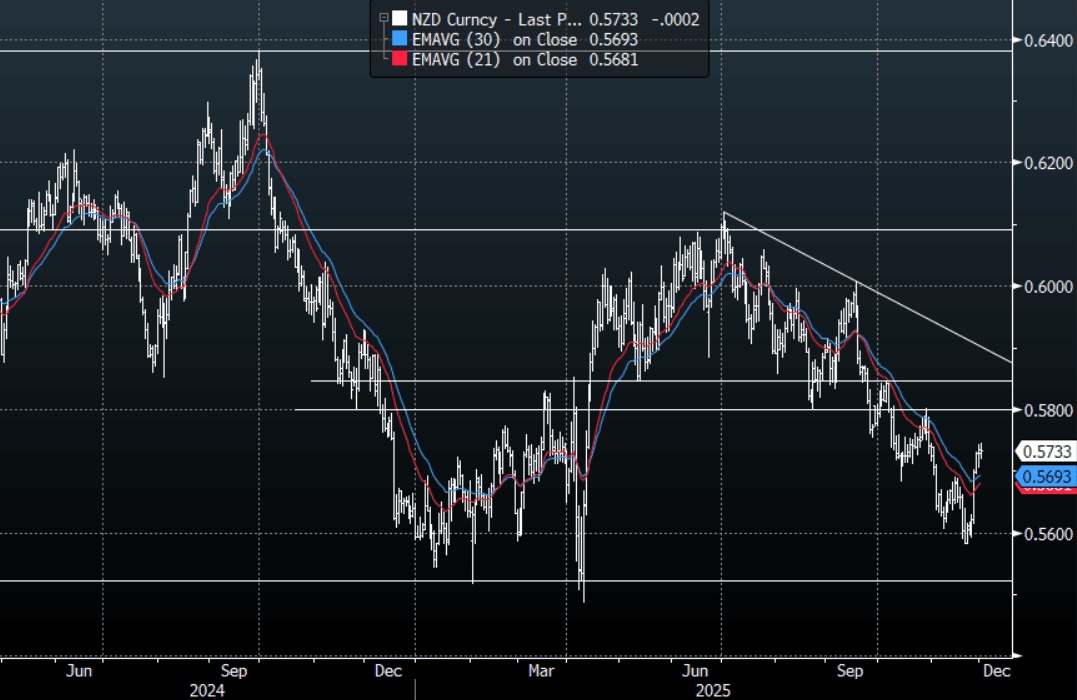

NZD/USD - Consolidates Toward 0.5750, Little Reaction To Move In Risk

The NZD/USD had a range today of 0.5723 - 0.5745 in the Asia-Pac session, going into the London open trading around 0.5735, -0.02%. The NZD/USD has had a subdued session considering the risk-off start to the week. Asia has broadly sold the USD as USD/JPY trades lower, but if this risk-off start to the week turns into something more I would watch for the USD to potentially bounce against risk currencies. On the day I suspect we could see a dip back toward the 0.5670/0.5690 area where buyers should re-emerge, the market needs a clear break back above 0.5760 to turn its attention toward the more important 0.5800-50 resistance.

- "NZ OCT. HOME-BUILDING APPROVALS FALL 0.9% M/M"(prior +7.3%m/m) - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5665(NZD309m), 0.5940(NZD427m). Upcoming Close Strikes : 0.5575(NZD547m Dec 3), 0.5700(NZD4356m Dec 2) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 43 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

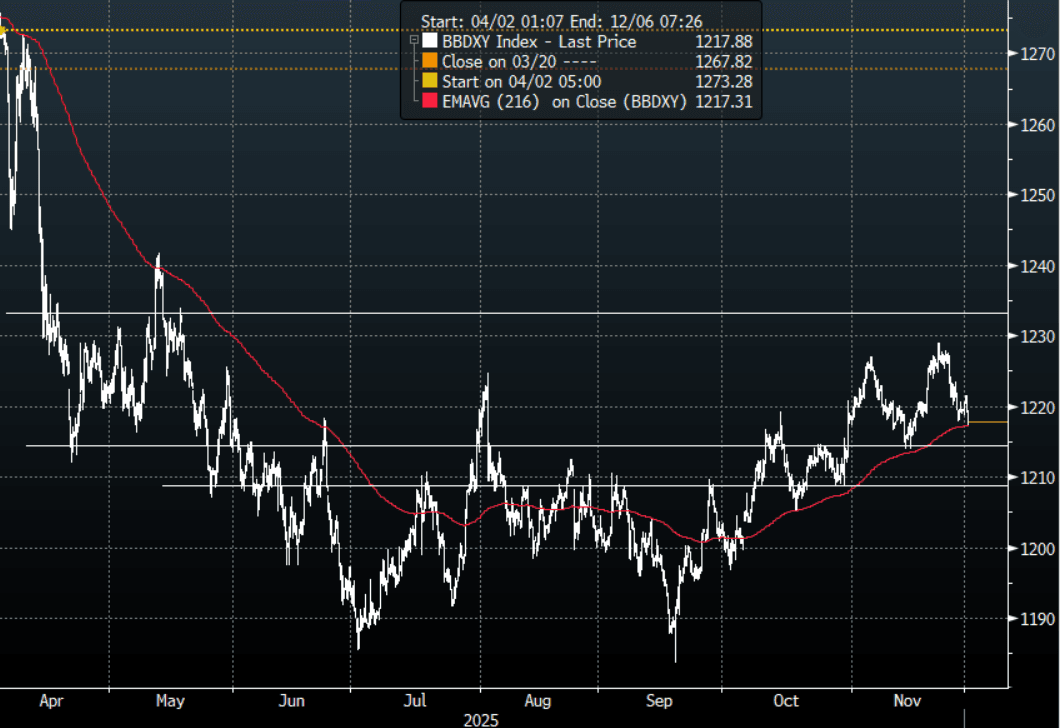

FOREX: USD - BBDXY Dragged Lower With USD/JPY, Can London Differentiate ?

The BBDXY has had a range today of 1216.55 - 1218.42 in the Asia-Pac session; it is currently trading around 1217, -0.05%. Risk has turned very quickly to start the week in Asia thanks to a combination of poor Chinese PMI’s over the weekend and Japanese yields continuing to extend higher as the market prices in a potential December BOJ rate hike. The USD moved lower initially as Asia tends to follow the moves seen in USD/JPY, I suspect we might see this start to differentiate once London comes in. On the day I will be watching to see if the USD can bounce against risk currencies should this risk-off start to the week expand on its initial moves. On the day resistance is back towards the 1222-1224 area where sellers should remerge initially, a sustained break back above here and the market would again turn its focus to the pivotal 1230-1240 area.

- EUR/USD - Asian range 1.1590 - 1.1616, Asia is currently trading 1.1600. The pair is consolidating around 1.1600. On the day I will be watching to see if price stalls toward the 1.1600-25 area as risk turns lower. If price fails up here then look for a retest of the 1.1545-50 support.

- GBP/USD - Asian range 1.3222 - 1.3249, Asia is currently dealing around 1.3230. The pair is consolidating its recent gains around 1.3250. I remain skewed toward shorts but I feel this move does signal the need to be patient. On the day GBP needs to hold above 1.3200 to attempt to extend higher so watch for a break sub 1.3180-1.3200 area which could signal the correction higher has stalled.

- Cross asset : SPX -0.70%, Gold $4240, US 10-Year 4.036%, BBDXY 1217, Crude Oil $59.60

- Data/Events : Germany HCOB Germany Manufacturing PMI, France HCOB France Manufacturing PMI, Spain HCOB Spain Manufacturing PMI, EZ HCOB Eurozone Manufacturing PMI, Italy HCOB Italy Manufacturing PMI/Budget Balance

Fig 1: BBDXY Spot 4H Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: UEDA Spooks Japanese Stocks; Korea and Taiwan Follow Suit

Global rate expectations continue to impact investor optimism with risk appetite strong in most major bourses today. Whilst US rate sensitive markets continue to position for a rate cut in the US, markets are seeing a potential BOJ rate hike in December, which has caused the yen to firm and the Nikkei to fall. Governor Kazuo Ueda has indicated the bank will consider the pros and cons of an increase. In India, stronger than expected GDP results came ahead of this week's Reserve Bank of India's decision on rates which is widely expected to see a rate cut to stem the decline in inflation. The focus on AI tech remains a key thematic with names like TSMC's fall today a key driver to the decline of the TAIEX in what local press are suggesting is profit taking. This is likely to be an ongoing theme into year end given the extraordinary run up in recent months of AI / Tech names like TSMC and key equities in Korea and Japan.

- UEDA's comments wasn't well received by the NIKKEI with it starting the month and the week off with a fall of -1.8%, dragging the KOSPI with it with falls of -0.16%.

- China's major bourses are all up with the Hang Seng leading the way with gains of +0.80%, followed by the CSI 300 up +0.75%

- The TAIEX in Taiwan is down modestly by -0.44% with risk sentiment looking less robust into year end.

- The NIFTY 50 was buoyed by the better than expected GDP and talk of a rate cut this week sees it start Monday up +0.28% to a new high of 26,278

- SE Asia' s bourses are starting the month off strongly with the FTSE Malay KLCI leading the way up +1.1% following better than expected Manufacturing PMIs.

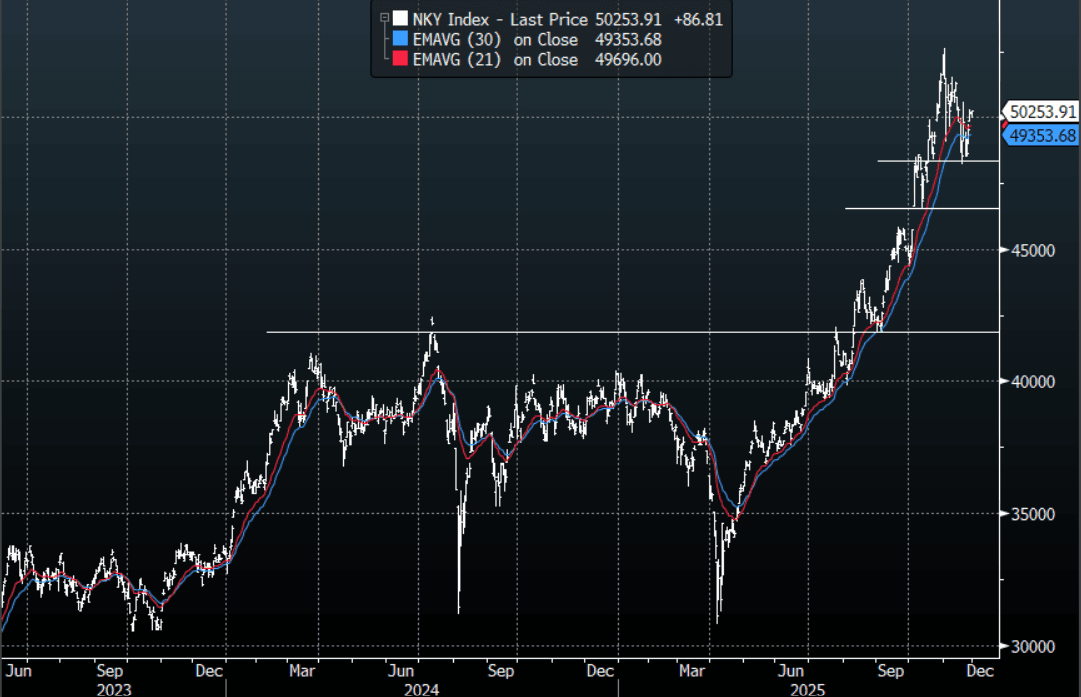

JAPAN: Nikkei(NHZ5) - Can It Build Momentum Above 50000

The Nikkei(NHZ5) contract Friday night range was 50095 - 50315, Asia is currently trading 50275 +0.10%. The (NHZ5) contract drifted sideways on Friday in a very quiet session. The Nikkei 225 technically remains in an uptrend while the support toward 48000 holds, albeit a very steep one. Can the Asian session build on this strong momentum in risk, it has come a long way very quickly but while this theme dominates then dips should continue to be supported. In the Asian session I suspect dips back toward 49500-49800 will now be supported initially. If the contract can sustain the move back above 50000 it will target 50600-50800 first and then the 51500-51700 area.

- BOJ Governor Kazuo Ueda speaks in Nagoya.

- The Nikkei 225 Index Average True Range(ATR) for the last 10 Trading days: 895 Points

Fig 1: Nikkei 225 Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

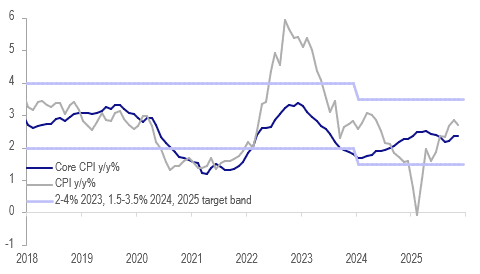

INDONESIA: BI Looking To Cut Again, Inflation Stable But Need Stronger IDR

Headline inflation moderated 0.2pp to 2.7% y/y as volatile fresh food inflation eased 1.1pp to 5.5% y/y in November. Core held steady at 2.4% y/y, which was slightly more than consensus forecast. Bank Indonesia Governor said today there is room for further easing and that it just depends on timing and the stabilisation in inflation should allow it to cut rates again when it is confident that the rupiah has stabilised.

- USDIDR is down 0.5% to 16,661 since the 19 November BI decision to keep rates unchanged but this has been helped by a weaker US dollar as Fed rate cut expectations have increased. The BIS IDR NEER was flat in November which is a step in the right direction towards FX stability.

- The S&P Global November PMI reported that cost pressures increased in Indonesia due to the weaker IDR and raw materials and were passed on resulting in highest selling inflation in more than 18 months. This is a trend that will be monitored.

- In October a large jump in personal care & others inflation to 11.9% y/y from 9.9% drove the increase in core inflation. The rise was due to higher global gold prices. They were up almost another 6% over November and so it is not surprising that personal care & others picked up further to 12.5% y/y keeping underlying inflation at 2.4%. Other components saw steady rates.

- The drop in fresh food inflation fed into lower price changes for dining out and general food & drinks components.

Indonesia CPI y/y%

Source: MNI - Market News/LSEG

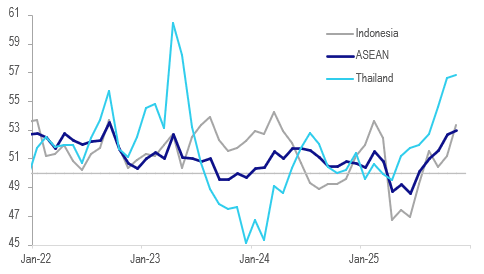

ASIA: November Growth Up But Domestically Driven, Export Demand Weak

S&P manufacturing PMIs across most of ASEAN were higher in November signalling stronger growth in activity across the sector. Only in the Philippines did it contract due to typhoon-related disruptions, while in Malaysia it stagnated. The aggregate ASEAN PMI rose to 53.0 from 52.7, the best performance since September 2022, with Thailand again posting the fastest growth followed by Vietnam. ASEAN economies are showing resilience following the reduction in global trade uncertainty but it appears to be domestically driven with export orders contracting. There were signs of cost pressures in the data though.

ASEAN S&P manufacturing PMIs

Source: MNI - Market News/Bloomberg Finance L.P.

- ASEAN manufacturing activity was driven by higher domestic orders as overseas contracted. Production was up driving an increase in purchasing but employment was steady.

- Thailand continued to outperform at 56.8 (October 56.6), highest since May 2023 with manufacturers also very positive about the outlook. Growth was driven by stronger production and domestic orders and subsequent hiring. However, overseas demand contracted at a faster pace. Cost inflation rose in November but wasn’t passed on with output inflation steady.

- Indonesia saw a material improvement with the PMI up to 53.3 from 51.2, the highest since February and back above ASEAN as a whole. The move was due to the fastest growth in new orders in over 2 years driven by domestic demand as overseas fell at the sharpest in over a year. Domestic strength drove an increase in employment and purchasing activity though. The outlook remains positive but less so than last month.

- Indonesian cost pressures increased due to the weaker IDR and raw materials and were passed on resulting in highest selling inflation in more than 18 months. Rates have been cut 125bp this year and inflation has turned higher.

OIL: Crude Starts Week Higher As OPEC Pauses & Geopolitical Tensions Rise

Oil prices are higher in Monday’s APAC trading after OPEC confirmed that it would pause its production increases (reversing its previous cuts) in Q1, a time of seasonally low demand but also reflecting concern over the projected record surplus for 2026. Crude has also found support from geopolitical developments as Ukraine struck a Russian refinery and two tankers and US President Trump threatened Venezuela.

- WTI is up 1.7% to $59.56/bbl, close to the intraday high of $59.61. Brent is 1.7% higher at $63.41/bbl after reaching $63.47. They were moderately lower on Friday.

- Trump wrote on Truth Social that Venezuela’s airspace is “closed in its entirety”, which was seen as an act of aggression by Venezuela, which was the 17th largest oil exporter of oil in 2023 (IEA). He then backtracked but tensions between the two remain.

- Talks continued between the US and Ukraine in Florida over the weekend with Secretary of State Rubio saying that they were “productive” but “more work” is needed. President Trump said that Envoy Witkoff will meet President Putin this week.

- Later US November manufacturing ISM/PMI, UK October lending and European November manufacturing PMIs are released.

PRECIOUS METALS: Silver Continues Outperformance, US ISM Later

Continuing Friday’s pattern, silver is outperforming gold in Monday’s APAC session. Silver benefits from high physical demand and the market is currently tight. Prices are up 1.3% to $57.22/oz after an intraday high of $57.864, a new record, and 5.8% rise on Friday. In comparison, gold is flat today at $4238.7/oz reaching $4256.48 earlier and rising 2.0% on Friday. Both metals have found support from increased Fed rate cut pricing which is now at 23pp for the 10 December decision. Yields and the US dollar are little changed today.

- Silver moved above the bull trigger at $54.480 and three other resistance levels including $56.153, a Fibonacci projection, confirming a resumption of the primary uptrend.

- Bloomberg reported that silver inventories in the Shanghai Futures Exchange have fallen to their lowest in almost 10 years.

- However, Pepperstone Group believes that silver is being driven by “speculative flows” which given the substantially lower volumes than gold is creating the recent large price moves.

- Equities are mixed with the S&P e-mini down 0.7% and Nikkei -1.8% but Hang Seng is up 0.8% and SE Thai +0.8%. Oil prices are higher with WTI +1.6% to $59.50/bbl. Copper is up 1.5%.

- Later US November manufacturing ISM/PMI, UK October lending and European November manufacturing PMIs are released.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 01/12/2025 | 0730/0830 | ** | Retail Sales | |

| 01/12/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/12/2025 | 0845/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/12/2025 | 0850/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/12/2025 | 0855/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/12/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/12/2025 | 0930/0930 | ** | BOE Lending to Individuals | |

| 01/12/2025 | 0930/0930 | ** | BOE M4 | |

| 01/12/2025 | 0930/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 01/12/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/12/2025 | 1500/1000 | *** | ISM Manufacturing Index | |

| 01/12/2025 | 1530/1530 | DMO to hold FQ4 consultations with investors / GEMMs | ||

| 01/12/2025 | 1530/1530 | BOE Dhingra Keynote at UK Trade Policy Observatory | ||

| 01/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 01/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/12/2025 | 0001/0001 | * | BRC Monthly Shop Price Index | |

| 02/12/2025 | 0030/1130 | * | Building Approvals | |

| 02/12/2025 | 0030/1130 | Balance of Payments: Current Account | ||

| 01/12/2025 | 0100/2000 | Fed Chair Jerome Powell | ||

| 02/12/2025 | 0700/0700 | BOE Financial Stability Report | ||

| 02/12/2025 | 0745/0845 | Budget Balance | ||

| 02/12/2025 | 0900/1000 | Unemployment | ||

| 02/12/2025 | 1000/1100 | ** | EZ Unemployment | |

| 02/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 02/12/2025 | 1000/1000 | * | Index Linked Gilt Outright Auction Result | |

| 02/12/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 02/12/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 02/12/2025 | 1000/1100 | *** | EZ HICP Flash |