MNI EUROPEAN MARKETS ANALYSIS: Middle East Tensions Continue

- Oil rose and US equity futures fell in the first part of trade, as headlines crossed from US President Trump, who stated residents should evacuate Tehran immediately. He also cut short his G7 trip and returned to the US. Headlines have continued during the day of around explosions and missile launches between Israel and Iran.

- As expected, the BoJ held rates steady. The central bank did announce that it would trim bond buying by 200bn/per quarter from April 2026 next year. The current pace had been at a reduction of 400bn per quarter.

- Later US May retail sales, trade prices, IP, April business inventories and NAHB June housing index are released but the attention is on Wednesday’s FOMC decision and outlook. The euro area/German June ZEW also print today.

MARKETS

The TYU5 range has been 110-15+ to 110.23 during the Asia-Pacific session. It last changed hands at 110-20, up 0-05 from the previous close.

- The US 2-year yield moved lower; it is trading around 3.948%, down 0.02 from its close.

- The US 10-year yield moved lower, it is trading around 4.43%, down 0.02 from its close.

- "WHITE HOUSE DISCUSSING WITH IRAN POSSIBILITY OF MEETING BETWEEN U.S. ENVOY STEVE WITKOFF AND IRANIAN FOREIGN MINISTER ABBAS ARAGHCHI, TRUMP TEAM PROPOSES IRAN TALKS THIS WEEK ON NUCLEAR DEAL, CEASEFIRE - AXIOS" - RTRS

- US President Trump has posted on Truth Social, stating that Iran should have signed the deal he told them to sign, while also re-iterating that Iran cannot have a nuclear weapon. He also noted that everyone should evacuate Tehran immediately.

- The 10-year yield has bounced strongly off its 4.30/35% support, this area needs to hold if yields are to move higher. The range looks to be 4.30% - 4.60% for now a break either side would provide a clearer direction. It seems traders for the moment are more concerned with the move in oil and the implications it has for inflation and the FOMC this week than buying treasuries as a safe haven.

- Data/Events: Retail Sales, Industrial Production, Business Inventories, NAHB Housing Market Index

JGBS: Cheaper After BoJ Decision To Trim Bond Buying

JGB futures have weakened to session lows, -38 compared to settlement levels, following the BoJ Policy Decision.

- The BoJ kept rates at 0.50%, as widely expected. That decision from the central bank board was unanimous. The bond buying program is unchanged through to the end of March 2026. The central bank did announce that it would trim bond buying by 200bn/per quarter from April 2026 next year. The current pace had been at a reduction of 400bn per quarter. There was one dissenter to this decision, board member Tamura, who wanted to keep the pace around 400bn. He also argued that long term rates should be determined by the market.

- The BoJ emphasised that tapering will proceed in a predictable and cautious manner, but left the door open to adjustments if market conditions require.

- The BoJ views price trends as broadly in line with its 2% inflation target in the second half of its outlook period.

- Cash JGBs are 1-4bps cheaper across benchmarks, with the 7-10-year underperforming. The benchmark 10-year yield is 4.4bps higher at 1.482% versus the cycle high of 1.596%.

- The swaps curve has bear-steepened, with rates are 2-5bps higher. Swap spreads are mostly wider.

- Tomorrow, the local calendar will see Trade Balance and Core Machine Orders data.

BOJ: On Hold As Expected, Pace Of Bond Taper Slows

The BoJ kept rates at 0.50%, as widely expected. That decision from the central bank board was unanimous. The bond buying program is unchanged through to end March 2026. The central bank did announce that it would trim bond buying by ¥200bn/per quarter from April 2026 next year. The current pace had been at a reduction of ¥400bn per quarter. There was one dissenter to this decision, board member Tamura, who wanted to keep the pace around ¥400bn. He also argued that long term rates should be determined by the market.

- The BoJ said it would also respond nimbly to rapid yield rises.

- Elsewhere the central bank noted the price trend is likely to meeting its goal in the second half of the outlook. A well outlined expectation from the central bank. It also reiterated that uncertainties remain extremely high.

- The market reaction has been relatively muted, with USD/JPY last near 144.75/80, close to unchanged for the session. JGB yields are a touch higher.

- The shift in bond purchases announced by the BoJ from march next year, was within the range expected by the market.

- The next focus point is Ueda's press conference, due in a little over 2.5 hours.

AUSSIE BONDS: Weaker & At Cheaps On A Data-Light Session, Jobs Data On Thur

ACGBs (YM -4.0 & XM -2.5) are weaker and trading near Sydney session lows on a local data-light day.

- Cash US tsys are ~1bp richer in today's Asia-Pac session after paring earlier strength. Today’s US calendar will see Retail Sales, Industrial Production, Business Inventories and the NAHB Housing Market Index.

- US President Trump has posted on Truth Social, stating that Iran should have signed the deal he told them to sign, while also reiterating that Iran cannot have a nuclear weapon. He also noted that everyone should evacuate Tehran immediately.

- Cash ACGBs are 3bps cheaper with the AU-US 10-year yield differential at -18bps.

- The bills strip is cheaper, with pricing -1 to -3.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in July is given an 85% probability, with a cumulative 76bps of easing priced by year-end.

- Tomorrow, the local calendar will see the Westpac Leading Index. May's jobs data is on Thursday. Bloomberg consensus sees a 20k rise in new jobs, in line with the 3-month average, with the unemployment and participation rates stable at 4.1% and 67.1% respectively.

- The AOFM plans to sell A$900mn of the 2.75% 21 June 2035 bond tomorrow and A$800mn of the 1.00% 21 December 2030 bond on Friday.

BONDS: NZGBS: Closed Modestly Richer, Mthly Prices Mixed, Q1 GDP On Thurs

NZGBs closed near session bests, with benchmark yields 1-2bps lower.

- Cash US tsys are ~1bp richer in today's Asia-Pac session.

- The NZ-US and NZ-AU 10-year yield differentials were 3-4bps tighter on the day.

- Monthly price data was mixed in May, with food, power, accommodation and alcohol seeing a rise in inflation, while air travel, rents and petrol fell. The series released account for 46.5% of the quarterly CPI, with Q2 due to be released on July 21, which the RBNZ expects to rise 0.5% q/q & 2.6% y/y. June monthly indices print earlier on July 17. RBNZ and NZIER compiled consensus accept a near-term pick-up in inflation but continue to have it returning to the mid-point of the 1-3% target band.

- Swap rates closed 1bp lower.

- RBNZ dated OIS pricing closed slightly firmer across meetings. 4bps of easing is priced for July, with a cumulative 27bps by November 2025.

- Tomorrow, the local calendar will see Westpac Consumer Confidence, Q1 Current Account and Non-Resident Bond Holdings data. Q1 GDP is due for release on Thursday.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 2.75% Apr-37 bond and NZ$50mn of the 2.75% May-51 bond.

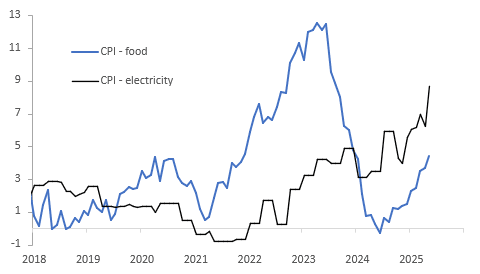

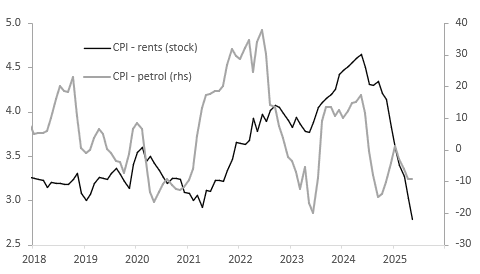

NEW ZEALAND: Food & Power Inflation Higher As Petrol & Rents Ease

Monthly price data was mixed in May with food, power, accommodation and alcohol seeing a rise in inflation, while air travel, rents and petrol fell. The series released account for 46.5% of the quarterly CPI with Q2 due to be released on July 21, which the RBNZ expects to rise 0.5% q/q & 2.6% y/y. June monthly indices print earlier on July 17. RBNZ and NZIER compiled consensus accept a near-term pick up in inflation but continue to have it returning to the mid-point of the 1-3% target band.

- Food prices rose 0.5% m/m to be up 4.4% y/y up from 3.7% y/y in April. They have been trending higher since the June 2024 trough of -0.3% y/y. There has been a sharp increase in annual dairy and beef inflation. Groceries fell 0.7% m/m to be steady at 5.2% y/y in May.

NZ inflation y/y%

- Existing rents rose 0.1% m/m to be up 2.8% y/y, lowest rate in over 10 years and a moderation from April’s 3.0%. They have been trending lower since reaching 4.6% y/y in May 2024.

- Petrol prices fell 2.7% m/m, the fourth consecutive monthly decline, to be down 9.4% y/y after -9.2% in April. This component should put downward pressure on Q2 headline inflation.

NZ inflation y/y%

Source: MNI - Market News/Statistics NZ

- Power prices were higher though with electricity up 2.3% m/m & 8.7% y/y after 6.2% y/y and gas +0.7% & 15.4% down slightly from April’s 15.8%. They have been trending higher since November and August 2024 respectively.

- Both domestic and overseas air travel were down sharply in May after a strong rise in April to be down on the year, but accommodation rose to be 5.6% y/y higher up from 4.4%.

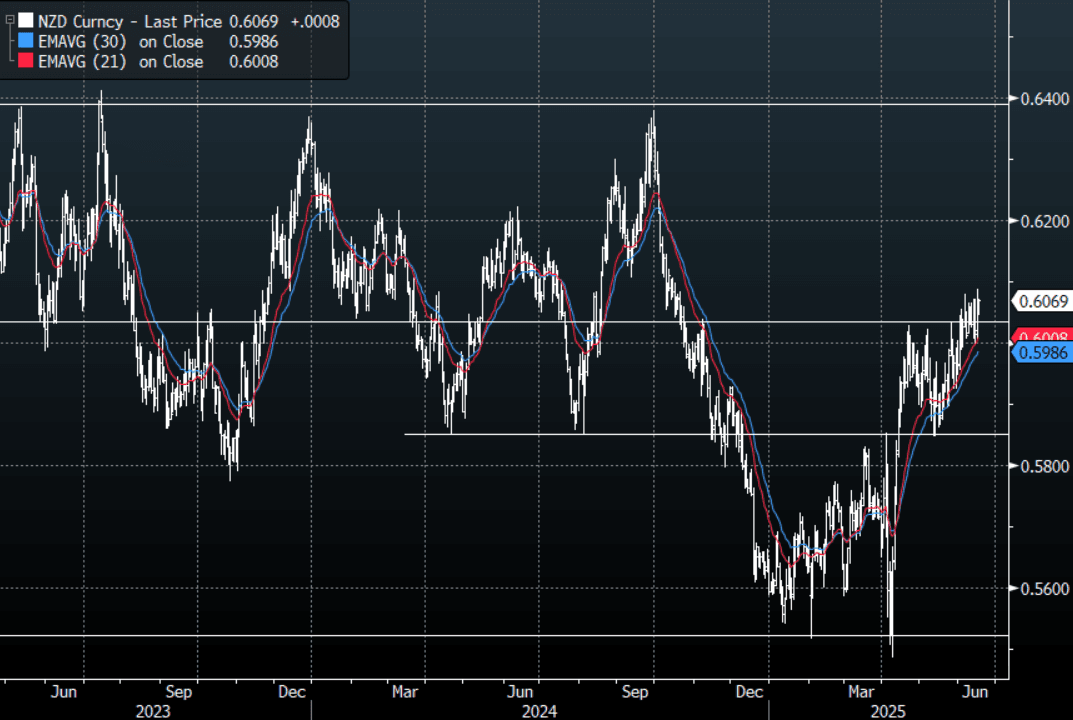

NZD: Asia Wrap - Building For A Move Higher

The NZD/USD had a range of 0.6045 - 0.6072 in the Asia-Pac session, going into the London open trading around 0.6070. A relatively quiet session for the NZD, as it continues to build for an extension higher.

- NZ Data - Food & Power Inflation Higher As Petrol & Rents Ease. Monthly price data was mixed in May with food, power, accommodation and alcohol seeing a rise in inflation, while air travel, rents and petrol fell.

- GDP Preview - Q1 GDP Likely To Be Robust Due To Agriculture & Manufacturing. The focus of the week will be on Thursday’s Q1 GDP release. Bloomberg consensus is forecasting another 0.7% q/q increase in production-based GDP, driven by the primary and manufacturing sectors, leaving the annual rate still down 0.8% y/y but up from Q4’s -1.1% y/y. Thus, expenditure-based GDP should see a significant contribution from agricultural and also services (tourism) exports. This is stronger than the RBNZ’s May forecast of a 0.4% q/q rise.

- The USD’s inability to bounce given the geopolitical backdrop is a worrying sign, the NZD will continue to benefit from its malaise.

- The NZD continues to find solid support around the 0.6000 area and has built a decent base from which to push higher from.

- While the support around 0.5850 holds in NZD/USD there should be buyers around on dips. A clear sustained break above 0.6050/0.6100 and the move could start to accelerate forcing some shorts to further reduce positioning.

- CFTC Data showed Asset managers paring back their shorts slightly over the week, the leverage community did likewise.

AUD/NZD range for the session has been 1.0757 - 1.0777, currently trading 1.0760. A top looks in place now just above 1.0900, the cross topped out last week towards the 1.0800/25 sell area, the first target looks to be around 1.0650.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

FOREX: Asia FX Wrap - The USD Continues To Struggle

The BBDXY has had a range of 1201.63 - 1203.68 in the Asia-Pac session, it is currently trading around 1201.”FX traders will be impressed at the PBOC’s confidence in the yuan, despite all the uncertainty around the Middle East. Meanwhile, US importers are increasingly being asked by their foreign counterparties to settle transactions in currencies other than the US dollar, including renminbi.”(BBG)

- EUR/USD - Asian range 1.1543 - 1.1567, Asia is currently trading 1.1565. EUR has rejected the move above 1.1600 but dips should continue to find demand, first support back towards the 1.1400 area then 1.1100/1200. EUR/USD looked to have broken the pivotal 1.1500 area last week, this needs to be sustained to signal a larger move higher.

- GBP/USD - Asian range 1.3558 - 1.3580, Asia is currently dealing around 1.3575. The GBP continues to hold above its Weekly pivot around 1.3500, it needs a catalyst for the move higher to regain momentum. First support seen back towards 1.3400/50.

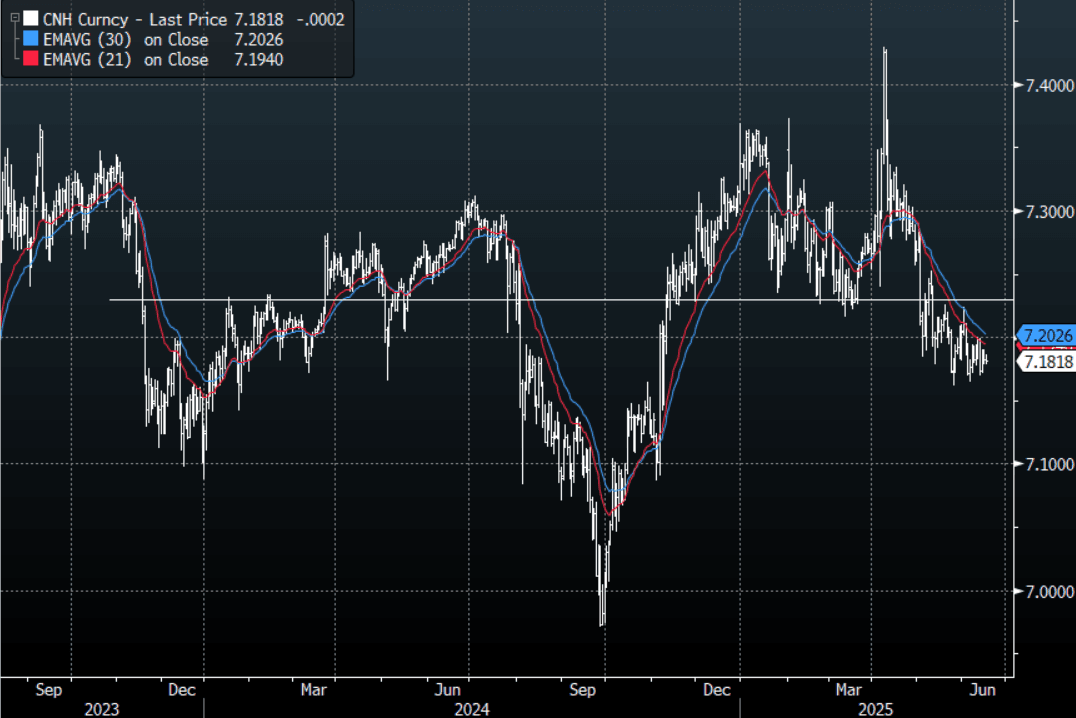

- USD/CNH - Asian range 7.1787 - 7.1860, the USD/CNY fix printed 7.1746. Asia is currently dealing around 7.1820. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX -0.40%, Gold $3390, US 10-Year 4.436%, BBDXY 1201, Crude oil $72.18

Data/Events : Germany ZEW Survey

Fig 1: USD/CNH Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - Probes Lower After BOJ, Focus Turns To Press Conference

The Asia-Pac USD/JPY range has been 144.50 - 145.11, Asia is currently trading around 144.60. USD/JPY has tested lower after the BOJ but has stalled again back towards the 144.50 area, the focus will now turn to the press conference. A market that is very long JPY is having its conviction tested at the moment, especially in the crosses.

- On Hold As Expected, Pace Of Bond Taper Slows : The BoJ kept rates at 0.50%, as widely expected. That decision from the central bank board was unanimous. The bond buying program is unchanged through to end March 2026. The central bank did announce that it would trim bond buying by 200bn/per quarter from April 2026 next year. The current pace had been at a reduction of 400bn per quarter. There was one dissenter to this decision, board member Tamura, who wanted to keep the pace around 400bn. He also argued that long term rates should be determined by the market.

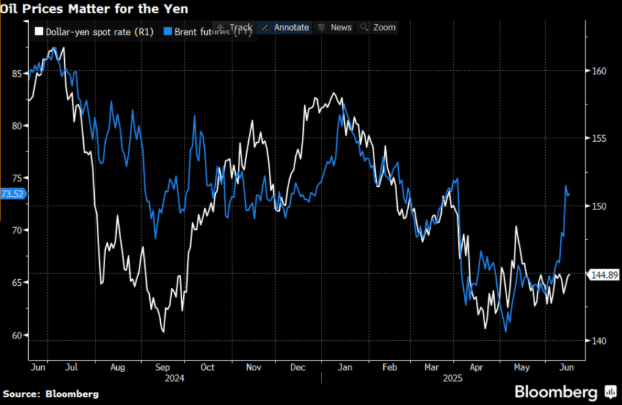

- (Bloomberg)- “Asian currencies are looking increasingly vulnerable as oil prices climb on the back of escalating Middle East tensions, threatening to reverse the supportive backdrop that’s buoyed regional FX in recent months. Historically, falling oil prices have gone hand-in-hand with stronger Asian currencies, given that the region’s biggest economies including China, Japan, India and South Korea are major energy importers.” See Graph Below

- USD/JPY continues to hold above its support back towards the 142.00 area, with oil surging again and US yields bouncing this pair has drifted back to the middle of its recent range. The JPY longs are feeling the pressure in the crosses.

- Price is back in its recent 142.00 - 147.00 range and will need a break either side of that to get a clearer direction. The large interest around 145.00 expired overnight.

- The market still seems very confident of a move lower in USD/JPY but with positioning quite large now we have seen the risk of pullbacks increase. A break above 147.00 would be needed to challenge the conviction of any shorts.

Options : Close significant option expiries for NY cut, based on DTCC data: 143.25.($350m). Upcoming Close Strikes : 146.00($1.85b June 20).

Fig 1 : USD/JPY Vs Brent Futures

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - Finds Support On Dip Back To 0.6500

The AUD/USD has had a range of 0.6503 - 0.6536 in the Asia- Pac session, it is currently trading around 0.6530. The AUD tried lower initially as Trump told Tehran to evacuate, later headlines proposing talking between the US and Iran saw it bounce off the 0.6500 area.

- "WHITE HOUSE DISCUSSING WITH IRAN POSSIBILITY OF MEETING BETWEEN U.S. ENVOY STEVE WITKOFF AND IRANIAN FOREIGN MINISTER ABBAS ARAGHCHI, TRUMP TEAM PROPOSES IRAN TALKS THIS WEEK ON NUCLEAR DEAL, CEASEFIRE - AXIOS" - RTRS

- The AUD saw good demand sub 0.6500 and is back to testing the 0.6550 area.

- Price remains in the 0.6350 - 0.6550 range for now, a sustained break above 0.6550/0.6600 is needed for the move higher to accelerate. The way the USD is trading across the board points to this being tested at some point.

- Expect buyers to continue to be around on dips while the support in the AUD/USD holds, a close back below 0.6350 is needed to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6600(AUD 1.1b June 19)

- CFTC Data shows Asset managers maintaining their shorts, the Leveraged community though continued to build up their shorts again.

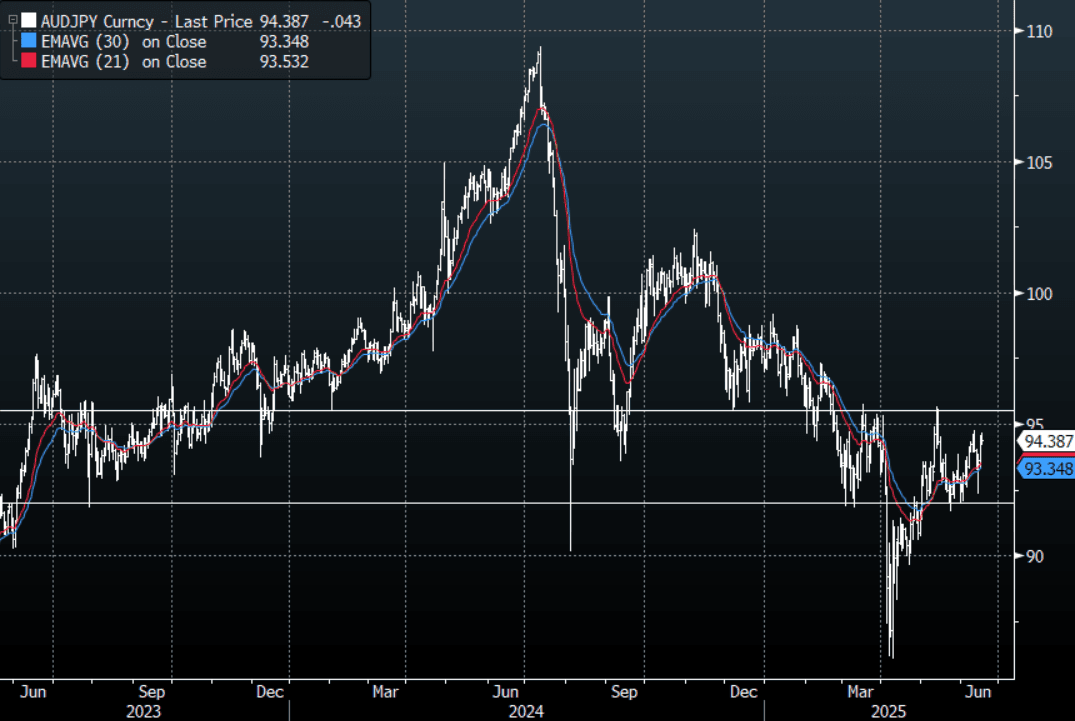

AUD/JPY - Today's range 94.18 - 94.66, it is trading currently around 94.50. Choppy price action as the pair establishes a range between 92.00 - 96.00. A break back below 91.50/92.00 is needed to see the move lower regain momentum and the focus turn back to the year's lows again.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - Probes Lower After BOJ, Focus Turns To Press Conference

The Asia-Pac USD/JPY range has been 144.50 - 145.11, Asia is currently trading around 144.60. USD/JPY has tested lower after the BOJ but has stalled again back towards the 144.50 area, the focus will now turn to the press conference. A market that is very long JPY is having its conviction tested at the moment, especially in the crosses.

- On Hold As Expected, Pace Of Bond Taper Slows : The BoJ kept rates at 0.50%, as widely expected. That decision from the central bank board was unanimous. The bond buying program is unchanged through to end March 2026. The central bank did announce that it would trim bond buying by 200bn/per quarter from April 2026 next year. The current pace had been at a reduction of 400bn per quarter. There was one dissenter to this decision, board member Tamura, who wanted to keep the pace around 400bn. He also argued that long term rates should be determined by the market.

- (Bloomberg)- “Asian currencies are looking increasingly vulnerable as oil prices climb on the back of escalating Middle East tensions, threatening to reverse the supportive backdrop that’s buoyed regional FX in recent months. Historically, falling oil prices have gone hand-in-hand with stronger Asian currencies, given that the region’s biggest economies including China, Japan, India and South Korea are major energy importers.” See Graph Below

- USD/JPY continues to hold above its support back towards the 142.00 area, with oil surging again and US yields bouncing this pair has drifted back to the middle of its recent range. The JPY longs are feeling the pressure in the crosses.

- Price is back in its recent 142.00 - 147.00 range and will need a break either side of that to get a clearer direction. The large interest around 145.00 expired overnight.

- The market still seems very confident of a move lower in USD/JPY but with positioning quite large now we have seen the risk of pullbacks increase. A break above 147.00 would be needed to challenge the conviction of any shorts.

Options : Close significant option expiries for NY cut, based on DTCC data: 143.25.($350m). Upcoming Close Strikes : 146.00($1.85b June 20).

Fig 1 : USD/JPY Vs Brent Futures

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Geopolitics Dragging Markets Lower

Major bourses in Asia were lower today as the uncertainty in the Middle East weighs on sentiment, in a day light on economic news in the region. Korea's KOSPI had closed in on 3,000 early in the trading day only for a complete turnaround and head lower, following the lead from elsewhere.

- In China, the Hang Seng drifted marginally lower by -0.13% and remains down by -0.55% over the last five trading days. The CSI 300 followed, down -0.15%, the Shanghai Composite down -0.19% and the Shenzhen Composite is down a mere --0.04% and is barely positive over the last five trading days.

- The KOSPI is down -0.34% in what was a complete turnaround having rallied early. It remains one of the strongest in the region over the last five trading days up over 2%

- The FTSE Malay KLCI is down -0.39% following yesterday's modest gains.

- The Jakarta Composite is up by +0.70% taking back yesterday's losses of -0.68% to stem four consecutive days of losses.

- The FTSE Straits Times in Singapore is up +0.28% whilst the PSEi in the Philippines has gained +0.53%

- The NIFTY 50 in India is down -0.36% given back from yesterday's gains of +0.92%

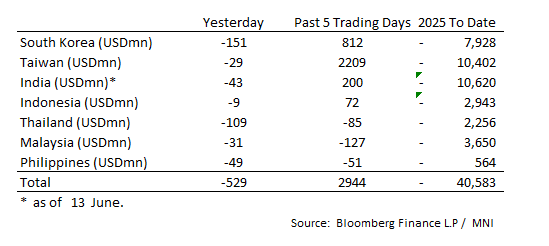

ASIA STOCKS: Outflows Increasing Across Major Markets

After a strong period of inflows, recent days have seen outflows beginning to become more consistent.

- South Korea: Recorded outflows of -$151m yesterday, bringing the 5-day total to +$812m. 2025 to date flows are -$7,928. The 5-day average is +$162m, the 20-day average is +$171m and the 100-day average of -$81m.

- Taiwan: Had outflows of -$29m as of yesterday, with total inflows of +$2209 m over the past 5 days. YTD flows are negative at -$10,402. The 5-day average is +$442m, the 20-day average of +$34m and the 100-day average of -$103m.

- India: Had outflows of -$43m as of the 13th, with total inflows of +$200m over the past 5 days. YTD flows are negative -$10,620m. The 5-day average is +$40m, the 20-day average of -$70m and the 100-day average of -$85m.

- Indonesia: Had outflows of -$9m yesterday, with total inflows of +$72m over the prior five days. YTD flows are negative -$2,943m. The 5-day average is +$14m, the 20-day average +$15m and the 100-day average -$29m.

- Thailand: Recorded outflows of -$109m as of yesterday, with outflows totaling -$85m over the past 5 days. YTD flows are negative at -$2,256m. The 5-day average is -$17m, the 20-day average of -$27m and the 100-day average of -$21m.

- Malaysia: Recorded outflows of -$31m as of yesterday, totaling -$127m over the past 5 days. YTD flows are negative at -$3,650m. The 5-day average is -$27m, the 20-day average of -$29m and the 100-day average of -$23m.

- Philippines: Saw outflows of -$49m yesterday, with net outflows of -$51m over the past 5 days. YTD flows are negative at -$564m. The 5-day average is -$10m, the 20-day average of -$17m the 100-day average of -$5m.

OIL: Crude Higher As Conflict Continues In The Middle East

Oil prices have unwound some of Monday’s losses after US President Trump said that Iran should have signed a nuclear deal when it had the chance and that people should evacuate Tehran. He left the G7 meeting early to return to Washington to discuss the Iran-Israel situation. Brent is up 0.7% to $73.76/bbl after a high of $74.85 earlier. WTI is 0.8% higher at $72.35/bbl following a peak of $73.69. The USD index is down slightly.

- Activity around the key Strait of Hormuz, that sees around 30% of global oil exports transit through, remains a major watch point. There are the risks that Iran closes it as a protest or Israel strikes infrastructure in the area. There was a shipping warning today following a fire sighted off the UAE coast but Ambrey confirmed that it was “not security related”, according to Bloomberg. Shipping around the Middle East has already been disrupted by the conflict.

- On Monday, there were reports that Iran was looking to restart negotiations on a nuclear agreement assuming the US doesn’t join the conflict. At this stage, Israel seemed unwilling to agree to a ceasefire as it wants to significantly damage Iran’s nuclear and military infrastructure.

- Industry-based data on US inventories are released Tuesday and will be monitored for signs of falling demand given current trade and global uncertainty.

- Later US May retail sales, trade prices, IP, April business inventories and NAHB June housing index are released but the attention is on Wednesday’s FOMC decision and outlook. The euro area/German June ZEW also print today.

GOLD: Bullion Slightly Higher Today After Trump Advises Tehran To Evacuate

Gold prices are off the intraday low of $3374.18/oz to be up 0.2% to $3393.1 and have traded in a relatively narrow range today. They reached a high of $3403.31 early in the session following US President Trump comments that Iran should have signed a nuclear deal when it had the chance and that people should evacuate Tehran. He will leave the G7 meeting early to return to Washington to discuss the Iran-Israel situation.

- Bullion has found some support from a slightly lower US dollar and US yields.

- Citibank believes that weaker demand and Fed rate cuts will drive gold prices back below $3000/oz over coming quarters, according to Bloomberg.

- Silver is 0.3% higher today at $36.43 to be up 10.5% in June, reinforcing the bullish trend. It is off its intraday low of $36.15. It continues to trade between initial support at $34.84, 20-day EMA, and resistance at $36.89, 9 June high.

- Equities are generally lower with the Hang Seng down 0.1%, S&P e-mini -0.4% but Nikkei up 0.5%. Oil prices are higher with WTI +0.8% to $72.33/bbl. Copper is down 0.4%.

- Later US May retail sales, trade prices, IP, April business inventories and NAHB June housing index are released but the attention is on Wednesday’s FOMC decision and outlook. The euro area/German June ZEW also print today.

INDONESIA: MNI BI Preview-June 2025: Consecutive Cuts Unlikely

- Download Full Report Here

- Bank Indonesia's (BI) decision is announced on June 18 and it is likely to keep rates at 5.5% after cutting them 25bp in May, although 9 out of 31 analysts on Bloomberg expect another 25bp reduction.

- With the focus remaining on the currency, we believe that BI will be cautious regarding back-to-back easing given that the Fed is widely expected to be on hold this month and it isn’t expected to resume cutting until later this year.

- With the economy slowing and inflation “controlled”, BI is likely to retain its easing bias, be cautious and look for opportunities to ease further going forward depending on global and Fed developments.

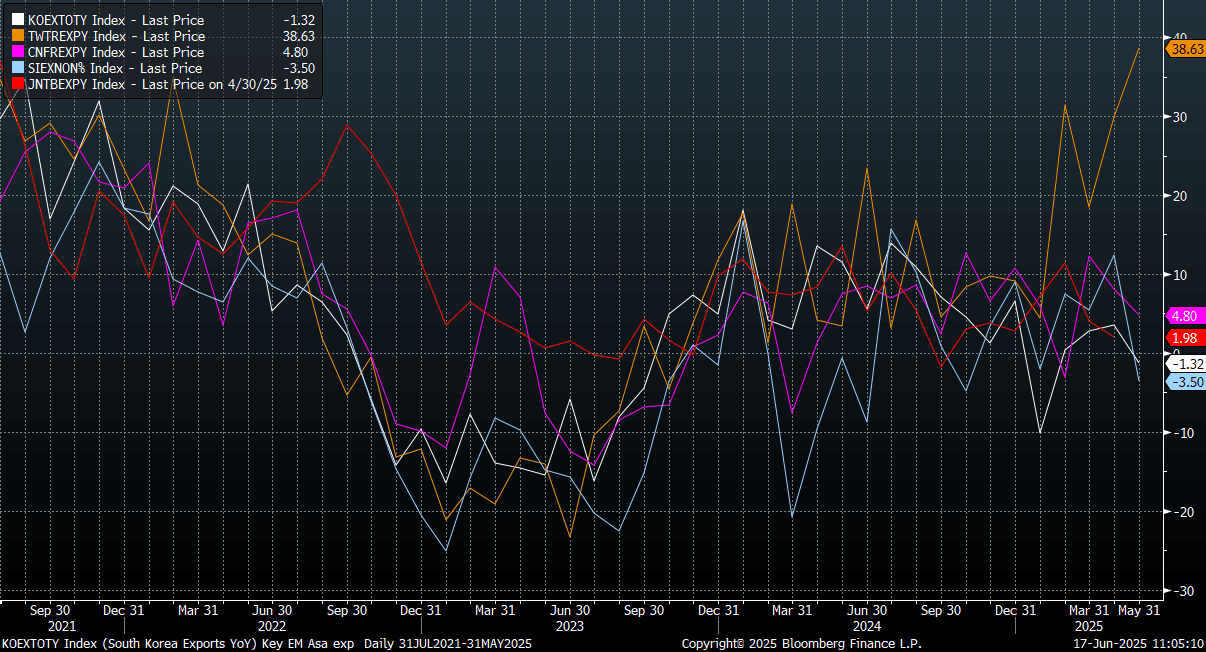

Singapore Exports Below Forecast, Exports To US Slump

Singapore exports for May were below forecasts. The headline fell -3.5%y/y, versus a +7.8% forecast (the April rise was 12.4%). Electronic exports slowed to 1.7%y/y from a revised 23.4% gain in April.

- Headline (non-oil domestic) exports were down -12m/m, suggesting some tariff related impact. Non-electronic exports were -5.3% y/y, with weakness evident across sub categories except for Pharmaceuticals. Electronic sub categories were mixed.

- By country, exports to the US were weakest, down 20.6%y/y, from 1.2% in April. Parts of Asia were also weaker, notably Thailand and Malaysia. Exports to the EU also fell -4.8%y/y.

- The chart below plots export growth for key EM Asia economies, Singapore the light blue line, has weakened, with most other parts of the region also slowing. Taiwan, the orange line, remains the standout.

Fig 1: Key EM Asia Economies Export Growth - Y/Y

Source: Bloomberg FInance L.P./MNI

SOUTH KOREA: Import Prices Point to Further Pressure for CPI

- Import prices in Korea declined -3.7% in May due primarily to the lower oil prices and a firmer Won and for a fourth consecutive month.

- Import prices are a key input into CPI as they directly feed through to production costs

- The Year on Year decline was larger, down -5% in May

- The export price index fell 3.4 percent in May from the previous month, marking the sharpest decline since November 2023, when the index dropped 3.4 percent and has been bouncing between deflation and zero for some time.

- The last CPI print for Korea saw a steady Year on Year result of +2.1% with the Month on Month figure barely positive at +0.1%

- The BOK cut rates at their last meeting, citing concerns as to the growth dynamic.

- The bond market has moved rapidly since with no just -17bps of cuts priced in over the next 12 month and only -3bps of cuts in the next 3 months.

CHINA: Country Wrap: E-Commerce Sector Hits Growth Milestone

- China's economy continued to expand steadily in May, supported by ongoing policy measures that helped sustain recovery amid global uncertainties, official data showed on Monday.

- Key economic indicators -- industrial production, retail sales, investment and services -- extended gains last month, while employment continued its stable trend, according to the National Bureau of Statistics (NBS). (source XINHUA)

- China's cross-border e-commerce sector achieved a historic milestone in 2024, with annual exports surpassing 2 trillion yuan (about 278.59 billion U.S. dollars) for the first time, according to data from the General Administration of Customs (GAC). The sector's exports grew 16.9 percent year on year to reach 2.15 trillion yuan in 2024, while total cross-border trade volume hit 2.71 trillion yuan. (source XINHUA)

- The Hang Seng drifted marginally lower by -0.13% and remains down by -0.55% over the last five trading days. The CSI 300 followed, down -0.15%, the Shanghai Composite down -0.19% and the Shenzhen Composite is down a mere --0.04% and is barely positive over the last five trading days.

- Yuan Reference Rate at 7.1746 Per USD; Estimate 7.1819

- CGBs are little changed today with the 10Yr at 1.69%

INDIA: Country Wrap: Trade Data Contracts

- India's trade data for May was weak as the ripple effect from the trade war creates an uneven period for importers and exporters. India's YoY exports contracted -2.2% for May, following Aprils expansion of +9.0%. It is not unusual for exports in India to contract with 13 out of the last 24 months contracting. The nominal amount exported inched up as it appears that the bottlenecks created in April are starting to clear. India's YoY imports contracted -1.7% following a +19% expansion in April. As with exports, it is not unusual for imports to contract with 10 out of the last 24 months contracting. The drop in imports was underpinned by lower oil and gold imports. The resultant trade deficit narrowed to $21.8bn, from $26.4bn (source MNI)

- The Reserve Bank of India will have more policy space to boost the economy if the inflation outlook falls, said Sanjay Malhotra, the head of the central bank, in a local media interview. The RBI’s decision to shift its stance to neutral from accommodative in early June doesn’t imply an immediate reversal in the policy cycle, he told the Business Standard newspaper (source BBG)

- The NIFTY 50 in India is down -0.36% given back from yesterday's gains of +0.92%

- The rupee is barely positive today up just +0.03% at 86.04

- Bonds are in positive territory with the IGB10YR lower by -1bp at 6.26%

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 17/06/2025 | 0600/0800 | ** | Unemployment | |

| 17/06/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 17/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/06/2025 | - | FOMC Meetings with S.E.P. | ||

| 17/06/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/06/2025 | 1230/0830 | *** | Retail Sales | |

| 17/06/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/06/2025 | 1230/0830 | *** | Retail Sales | |

| 17/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 17/06/2025 | 1315/0915 | *** | Industrial Production | |

| 17/06/2025 | 1400/1000 | * | Business Inventories | |

| 17/06/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 17/06/2025 | 1400/1000 | * | Business Inventories | |

| 17/06/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 17/06/2025 | 1730/1330 | Bank of Canada Summary of Deliberations | ||

| 18/06/2025 | 2350/0850 | * | Machinery orders | |

| 18/06/2025 | 0600/0700 | *** | Consumer inflation report | |

| 18/06/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 18/06/2025 | 0730/0930 | ECB Elderson At SRB Legal Conference 2025 | ||

| 18/06/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/06/2025 | 0900/1100 | *** | HICP (f) | |

| 18/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 18/06/2025 | 1230/0830 | *** | Housing Starts | |

| 18/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 18/06/2025 | 1230/0830 | *** | Housing Starts |