JPY: Asia Wrap - Probes Lower After BOJ, Focus Turns To Press Conference

The Asia-Pac USD/JPY range has been 144.50 - 145.11, Asia is currently trading around 144.60. USD/JPY has tested lower after the BOJ but has stalled again back towards the 144.50 area, the focus will now turn to the press conference. A market that is very long JPY is having its conviction tested at the moment, especially in the crosses.

- On Hold As Expected, Pace Of Bond Taper Slows : The BoJ kept rates at 0.50%, as widely expected. That decision from the central bank board was unanimous. The bond buying program is unchanged through to end March 2026. The central bank did announce that it would trim bond buying by 200bn/per quarter from April 2026 next year. The current pace had been at a reduction of 400bn per quarter. There was one dissenter to this decision, board member Tamura, who wanted to keep the pace around 400bn. He also argued that long term rates should be determined by the market.

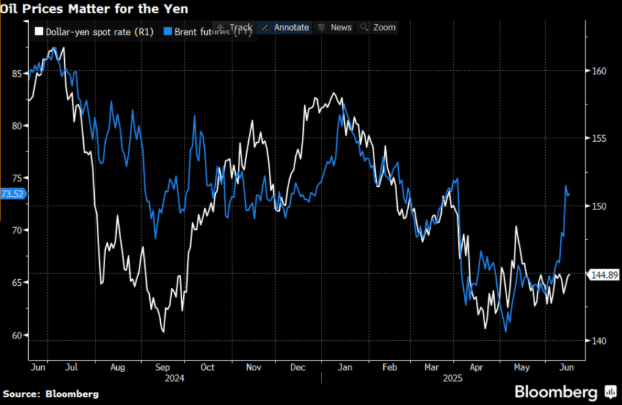

- (Bloomberg)- “Asian currencies are looking increasingly vulnerable as oil prices climb on the back of escalating Middle East tensions, threatening to reverse the supportive backdrop that’s buoyed regional FX in recent months. Historically, falling oil prices have gone hand-in-hand with stronger Asian currencies, given that the region’s biggest economies including China, Japan, India and South Korea are major energy importers.” See Graph Below

- USD/JPY continues to hold above its support back towards the 142.00 area, with oil surging again and US yields bouncing this pair has drifted back to the middle of its recent range. The JPY longs are feeling the pressure in the crosses.

- Price is back in its recent 142.00 - 147.00 range and will need a break either side of that to get a clearer direction. The large interest around 145.00 expired overnight.

- The market still seems very confident of a move lower in USD/JPY but with positioning quite large now we have seen the risk of pullbacks increase. A break above 147.00 would be needed to challenge the conviction of any shorts.

Options : Close significant option expiries for NY cut, based on DTCC data: 143.25.($350m). Upcoming Close Strikes : 146.00($1.85b June 20).

Fig 1 : USD/JPY Vs Brent Futures

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RATINGS: Moody's Downgrades US's AAA Rating As Deficits Seen Ballooning

Moody's has downgraded the US's long-term credit rating to Aa1 trom Aaa. The move may not have been fully expected today. But it was the last holdout among they S&P and Fitch to demote the USA from the top rating, and they placed negative outlook on the US last year (now stable). Fiscal deterioration, both past and anticipated as Congress wrangles with the Republican fiscal bill, is cited as the key factor. From the release (link):

- “While we recognize the US’ significant economic and financial strengths, we believe these no longer fully counterbalance the decline in fiscal metrics."

- "This one-notch downgrade on our 21-notch rating scale reflects the increase over more than a decade in government debt and interest payment ratios to levels that are significantly higher than similarly rated sovereigns...We do not believe that material multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration."

- "If the 2017 Tax Cuts and Jobs Act is extended, which is our base case, it will add around $4 trillion to the federal fiscal primary (excluding interest payments) deficit over the next decade. As a result, we expect federal deficits to widen, reaching nearly 9% of GDP by 2035, up from 6.4% in 2024, driven mainly by increased interest payments on debt, rising entitlement spending, and relatively low revenue generation."

- "We anticipate that the federal debt burden will rise to about 134% of GDP by 2035, compared to 98% in 2024."

- "Federal interest payments are likely to absorb around 30% of revenue by 2035, up from about 18% in 2024 and 9% in 2021. The US general government interest burden, which takes into account federal, state and local debt, absorbed 12% of revenue in 2024, compared to 1.6% for Aaa-rated sovereigns."

US FISCAL: "Extraordinary Measures" Continue To Dwindle Amid Debt Impasse

The "extraordinary measures" available to Treasury to stave off a debt default were down to $82B as of May 14, per a Treasury Department release today.

- That compares unfavorably with a high of $335B in January when the debt limit impasse began. Combined with $562B in Treasury cash on hand, though, after April's large tax intakes, that makes for around $644B in available resources before the "x-date" is reached.

- Resources are gradually being eroded since reaching nearly $800B in mid-April.

- Per Tsy Sec Bessent's letter to Congress last week, "after reviewing receipts from the recent April tax filing season, there is a reasonable probability that the federal government's cash and extraordinary measures will be exhausted in August while Congress is scheduled to be in recess. Therefore, I respectfully urge Congress to increase or suspend the debt limit by mid-July, before its scheduled break, to protect the full faith and credit of the United States."

CANADA DATA: Sales Activity Points To Potential Marking Up Of GDP Ests

There was mixed news on the housing and wholesale/manufacturing sales fronts this week, which on net look to slightly upwardly bias Q1 GDP estimates, pending next week's retail sales reading.

Housing starts blew through expectations at 278.6k in April (226.2k expected, 214.2k prior). This came after building permits fell a worse-than-expected 4.1% M/M in March as reported Wednesday.

- Meanwhile, he Canadian Real Estate Association reported existing home says April sales unexpectedly contracted -0.1% M/M (+1.0% expected, -4.8% prior). Sales are now down 9.8% Y/Y, while prices fell 1.2% M/M (3.6% Y/Y on the price index). (Link)

- Overall, confidence appears subdued, which is likely to translate into subdued activity.

On the sales front, March data was soft but positive versus expectations and could add a slight upward drift to Q1 GDP expectations.

- Manufacturing sales were less negative than expected at -1.4% M/M (-1.9% expected/flash estimate, -0.2% prior rev up 0.4pp). The decline was led by primary metals -6.5%, an area hit by U.S. tariffs, and oil -4.2%. Overall Q1 factory sales grew +1.6% vs prior +1.1%.(Link)

- Wholesales ex-petroleum and grains rose 0.2% in March, vs the advance estimate / consensus -0.3%. Sales volumes fell 0.3%. Overall Q1 wholesales rose 2.5%, led by machinery/equipment and autos/parts.