MNI EUROPEAN MARKETS ANALYSIS: JGBs Boosted Post 30yr Auction

- Japan has remained a focus point, with lots of headlines today, as the government is looking at cost of living relief but is also mindful of fiscal constraints. We also had stronger than expected household spending data, while FinMin Kato jawboned recent FX weakness. USD/JPY is little changed at this stage. JGB futures rebounded post a strong 30yr auction.

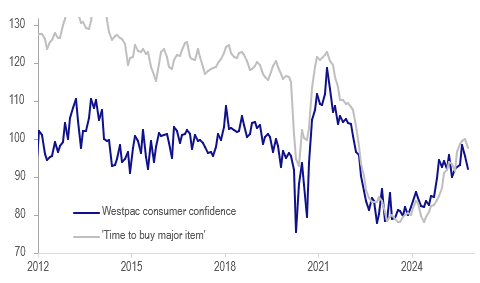

- In Australia, Westpac consumer confidence fell for the second straight month in October as higher inflation prints appear to have weighed on assessments of family finances and the economy.

- The USD is mostly higher against the majors, but aggregate moves aren't large. Regional equities, particularly those with tech exposure, saw positive spill over from US moves.

- Later the Fed’s Bostic, Bowman, Miran and Kashkari as well as the ECB’s Lagarde and Machado speak. September NY Fed 1-year inflation expectations and August Germany factory orders are released.

MARKETS

US TSYS: Yields Unchanged In A Quiet Session

The TYZ5 range has been 112-12+ to 112-15 during the Asia-Pacific session. It last changed hands at 112-14, up 0-01+ from the previous close.

- The US 2-year yield is trading 3.586%.

- The US 10-year yield is trading around 4.15%.

- 10-Year yields bounced on the back of global politics but remains subdued below 4.20% as the market works through the US shutdown. I suspect buyers continue to be around 4.20% initially and look to fade the move higher.

- Bloomberg - “Global Long Bonds Can Breathe Easier After 30-Year JGB Sale. Japan’s thirty-year auction went off smoothly with a higher bid-to-cover ratio than the previous sale, which will be a relief for investors across G-10 long-term debt. Traders will also be reassured with MUFJ-MS taking up the biggest slice of the bonds, along with Japan’s other big primary dealers.”

- Gavekal on X: “With the Bureau of Labor Statistics temporarily dark due to the US government shutdown, investors and the Federal Reserve must rely on other employment data. Worryingly, ADP’s private payroll estimate showed its most significant contraction of this cycle. That could be the result of the immigration crackdown reducing the supply of available workers. It is also possible that slack is starting to appear in the labor market, perhaps due to the temporary fiscal contraction from tariffs or AI causing unemployment, especially among young graduates. The recent decline in jobless claims is encouraging, but it is worth noting that many young graduates do not have prior work history and thus may not be eligible to claim unemployment benefits.”

JGBS: 30Y Auction Result Sparks A Massive Long-End Rally

JGB futures remain weaker, -6 compared to settlement levels, but well off lows after today’s less weak than feared 30-year auction.

- The 30-year JGB auction delivered mixed results. However, the 30-year has rallied strongly following the result, suggesting that the recent bear-steepening was overdone. Although newly elected Liberal Democratic Party leader Sanae Takaichi is perceived to have an expansionary fiscal and monetary policy stance, a lot of these expectations appear to have been priced into the market.

- MNI - Japan household spending for August was stronger than forecast (+2.3%y/y, versus 1.2% forecast, 1.4% prior). We are below earlier 2025 highs from a y/y momentum standpoint, but the trend has steadily improved from late 2024 lows. It should add, albeit at the margins, to the case for a further BoJ rate hike, although little is priced for the Oct meeting.

- Cash US tsys are little changed in today's Asia-Pac session.

- Cash JGBs have twist-flattened across benchmarks after today’s 30-year auction. The benchmark 30-year yield is 3.9bps lower at 3.267% after setting a fresh cycle high of 3.351% earlier in the session.

- Swap rates are flat to 7bps lower, with swap spreads tighter.

- Tomorrow, the local calendar will see Cash Earnings, BoP Current Account Balance and Trade Balance data.

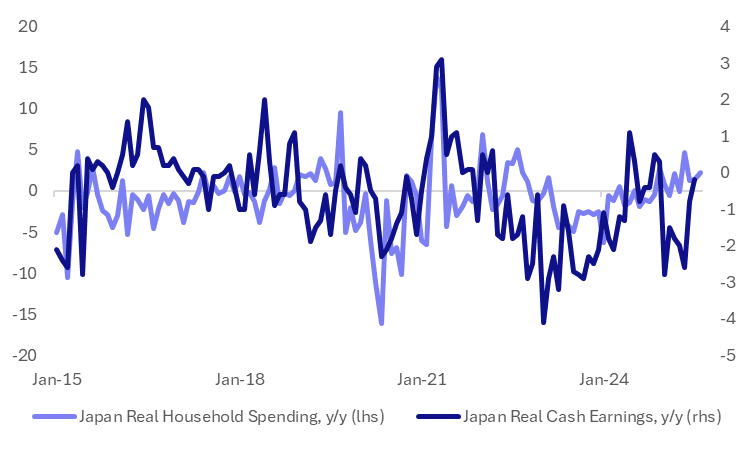

JAPAN DATA: Household Spending Above Forecasts, Supports BoJ Hike Plans

Japan household spending for August was stronger than forecast (+2.3%y/y, versus 1.2% forecast, 1.4% prior). We are below earlier 2025 highs from a y/y momentum standpoint, but the trend has steadily improved from late 2024 lows. It should add, albeit at the margins, to the case for a further BoJ rate hike, although little is priced for the Oct meeting (implied rate of 0.52%, versus a current effective rate of 0.477%). On the political side, ahead of Takaichi's first formal actions in government, one of her primary policy advisers Honda stated that Takaichi wants the Bank of Japan to proceed "cautiously" on interest rates, and that an October rate hike is "difficult". While the comments appeared to pressure the Bank away from tightening policy, the view that a December hike is not a problem was notable

- In m/m terms spending was up 0.6%. The strongest sub categories in y/y terms were transport, education and culture, recreation, which all recorded rises above 10%y/y.

- The chart below plots this real household spending measure against real labour earnings, both in y/y terms. Note the Aug update for earnings will be out tomorrow.

- The market expects real earnings to dip -0.5%y/y for August, against a -0.2% prior. Recall the July estimate was revised down from +0.5%y/y originally reported.

- If this is how the print evolved it would re-open the wedge between earnings and spending, although not as large as it was earlier in the year. From yesterday, via our Tokyo policy team: Regional firms expressed differing views on wage and price policies. A transportation company plans to maintain high wage levels in fiscal 2026, similar to this year, while a food and beverage firm in the same area intends to limit pay increases amid falling profits (from the BoJ's Regional Economic Report).

Fig 1: Japan Real Household Spending & Real Labour Earnings Y/Y

Source: Bloomberg Finance L.P./MNI

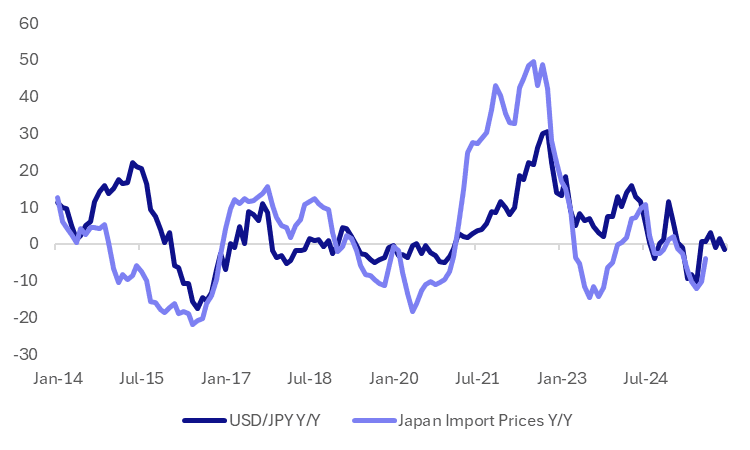

JPY: USD/JPY Levels Implying Less Import Disinflation Into year End

The other point of focus for yen weakness is what it does to the BoJ outlook, as concerns around import price pressures may rise. Given the high end point for USD/JPY at the end of last year (above 157.00), even if USD/JPY continues to rally into year end, the pass through to y/y import price momentum may not be that strong. Still, less deflation impetus from import prices would likely add to the BoJ's tightening case.

- The chart below plots USD/JPY y/y changes against import prices, also in y/y terms. The y/y rate for USD/JPY to the end of 2025 is generating assuming the pair rises 155.00 over this period.

- If these trends are maintained, it does point to the import pulse, which was -3.9%y/y (in August) shifting back closer to flat, or slightly into positive territory over this period. Even if USD/JPY stays around current levels it implies reduced import price y/y falls into year end/early Q1 next year.

- This could add to the case around BoJ tightening bias before year end/early 2026, which the new government led by Takaichi may be more comfortably with (as opposed to a Oct hike this year).

Fig 1: USD/JPY & Import Prices Y/Y (Assuming 155.00 By Year End)

Source: Bloomberg Finance L.P./MNI

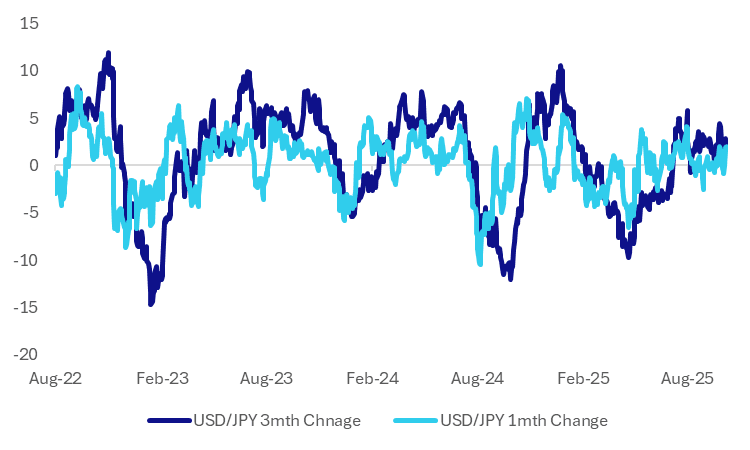

JPY: FX Jawboning Returns, But Mkt Concerns May Remain Low At This Stage

Earlier remarks from Japan FinMin Kato highlight that the recent break higher in USD/JPY hasn't gone unnoticed by the authorities. His remarks around closely watching FX moves and that markets will be monitored closely for excessive and disorderly movements. This is a reminder for markets around FX intervention risks, although as we argue in this bullet it is probably too soon for the market to be significantly concerned by such risks.

- We aren't too far away from spot levels that prevailed in the 2022 intervention episode. However, as the chart below highlights, USD/JPY's 1 month and 3 month rate of change is comfortably below levels that prevailed during this intervention episode and for those in 2024 as well. Both metrics are around +2% firmer, which is elevated but well within historical norms.

- We saw earlier that USD/JPY reacted little to the stronger household spending print. While not a tier one release, it speaks to the market comfort that a BOJ hike is likely to be off agenda in the near term.

- More broadly, with global risk appetite very well supported, this all feeds further into the carry trade.; The focus will now turn toward the pivotal 151/152 area a break of which will potentially start another leg higher. Expect dips to now find support unless there is push back on the market's views of Takaichi's policies.

- The over caveat is that USD/JPY looks too high relative to US-JP yield differentials, which may become a headwind if we test into the 151-152 area.

Fig 1: USD/JPY 1mth & 3mth Rate Of Change - Within Historical Norms

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Modestly Richer After Weak Data, Mar-36 Supply Tomorrow

ACGBs (YM +1.5 & XM +0.5) sit modestly higher after today’s weak data.

- "Australia's consumer confidence slipped to a six-month low this month on renewed doubts about hopes of future interest rate cuts given recent strength in inflation." - BBG

- ANZ-Indeed job advertisements dropped 3.3% from a month earlier in September, the largest monthly decline since February 2024.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session after today’s 30Y JGB auction sparked a relief rally in global bonds. Cash US tsys had been 1bp cheaper earlier. Although newly elected Liberal Democratic Party leader Sanae Takaichi is perceived to have an expansionary fiscal and monetary policy stance, a lot of these expectations appear to have been priced into the market.

- Cash ACGBs are 2-6bps cheaper, after being closed yesterday, with the AU-US 10-year yield differential at 24bps.

- The bills strip is +1 to +2 across contracts.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in November is given a 39% probability, with a cumulative 13bps of easing priced by year-end (based on an effective cash rate of 3.60%).

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond tomorrow.

- Tomorrow, the local calendar will also see Foreign Reserves data.

AUSTRALIA DATA: Stall In Disinflation Weighing On Consumer Confidence

Westpac consumer confidence fell for the second straight month in October as higher inflation prints appear to have weighed on assessments of family finances and the economy. Thus, Q3 CPI on 29 October is likely to be important for households too. The RBA’s decision to leave rates at 3.6% and cautious tone appear to have actually reassured consumers. Sentiment was down 3.5% m/m to 92.1, the lowest in 6 months. Households remain cautious but are prepared to spend at the right price. Q3 expenditure growth improved compared to Q2 with signs of a pickup in discretionary spending.

- The RBA noted in September that private consumption was stronger than it expected as financial conditions have eased and real incomes higher. Previously Deputy Governor Hauser noted that consumer confidence may be impacted by a “scarring effect” from the previous fall in real incomes. Quarterly consumption volumes in the September release on 3 November before the 4 November RBA decision will be monitored.

- Westpac expects a November rate cut but it states that it is “far from assured”.

- Westpac observed that responses following the RBA’s 30 September decision were around 2-3 points higher than prior. A bit more than half expected rates to rise over the coming year before the decision but that fell to about a third afterwards. Mortgage rate expectations over 12 months increased 15.6% to 101.7.

- Family finances over the next 12 months fell to 97.1, its lowest in just over a year. This sentiment appears to be impacting purchasing decisions with “time to buy a major item” down 1.1% to 97.2, well below the series average.

- Unemployment expectations fell 2.9% to be just below average signalling ongoing confidence in labour market stability.

- House price expectations continued rising in October up 2.1% with the over 75% of respondents expecting further increases over the year.

Australia Westpac consumer sentiment vs "time to buy"

Source: MNI - Market News/LSEG

RBNZ: MNI RBNZ Preview-October 2025: How Much To Ease?

- Download Full Report Here

- After Q2 GDP fell 0.9% q/q, more than the RBNZ’s -0.3% projected in August, expectations of a 50bp rate cut increased. Now 10 out of 25 analysts surveyed by Bloomberg are forecasting 50bp of easing on 8 October.

- The weaker GDP print means that there was more excess capacity in the economy than the RBNZ assumed in August, but the data are prone to large revisions and so it may want to stick to the 25bp rate cuts for October and November signalled in August.

- Two MPC members voted for a 50bp rate cut at the last meeting but recent and upcoming personnel changes on the committee add to the uncertainty around the October decision.

- 36bps of easing is priced for Wednesday’s meeting, with a cumulative 63bps by November 2025.

NEW ZEALAND: QSBO Signals Soft Jobs Market & Demand, Higher Chance Of 50bp

With the NZIER’s Quarterly Survey of Business Opinion (QSBO) showing a deterioration in the assessment of the outlook and only 4% of firms expecting to hire in Q4, the possibility of a 50bp rate cut on October 8 has increased. A net 15% believe that economic conditions will improve over the coming months down from 26%, which is concerning given 250bp of easing and a less uncertain global backdrop.

- The NZIER is forecasting a 25bp rate cut on Wednesday with another on 26 November.

- There was an increase in firms raising prices with a net 11% in Q3 up from 1% reducing them in Q2. The NZIER expects inflation to rise just above 3% before moderating to 2%, the band’s mid-point, over the next 12 months pressured by excess capacity.

- The Q3 labour market data may also be poor as a net 23% of firms reduced staffing while only 3% said that finding employees was a constraint on business. Both indicators suggest excess capacity in the labour market.

- A net 14% recorded a fall in Q3 business but 9% expect it to improve in Q4. NZIER notes that firms have been disappointed compared to their expectations for the last year. Lack of sales is the main business constraint.

- More firms plan to reduce investment over the year ahead in both plant & equipment and building. Uncertainty regarding the global economy remains a problem.

- In terms of sectors, manufacturing was the least optimistic regarding the outlook while retail was the most positive. Construction reported continued lacklustre demand with a net 20% cutting prices.

BONDS: NZGBS: Solid & Relative Performance Ahead Of Tomorrow’s RBNZ Decision

NZGBs closed just off session bests, 1-2bps richer, ahead of tomorrow’s RBNZ Policy Decision.

- On a relative basis, NZGBs' performance was even more impressive with the NZ-US and NZ-AU 10-year yields differentials finishing 4bps tighter on the day.

- Cash US tsys are flat in today's Asia-Pac session after yesterday's modest sell-off.

- After Q2 GDP fell 0.9% q/q, more than the RBNZ’s -0.3% projected in August, expectations of a 50bp rate cut increased. Now 10 out of 25 analysts surveyed by Bloomberg are forecasting 50bp of easing on 8 October.

- The weaker GDP print means that there was more excess capacity in the economy than the RBNZ assumed in August, but the data are prone to large revisions and so it may want to stick to the 25bp rate cuts for October and November signalled in August.

- Two MPC members voted for a 50bp rate cut at the last meeting, but recent and upcoming personnel changes on the committee add to the uncertainty around the October decision. (See MNI RBNZ Preview here)

- RBNZ dated OIS pricing closed slightly softer across meetings. 36bps of easing is priced for tomorrow, with a cumulative 63bps by November 2025.

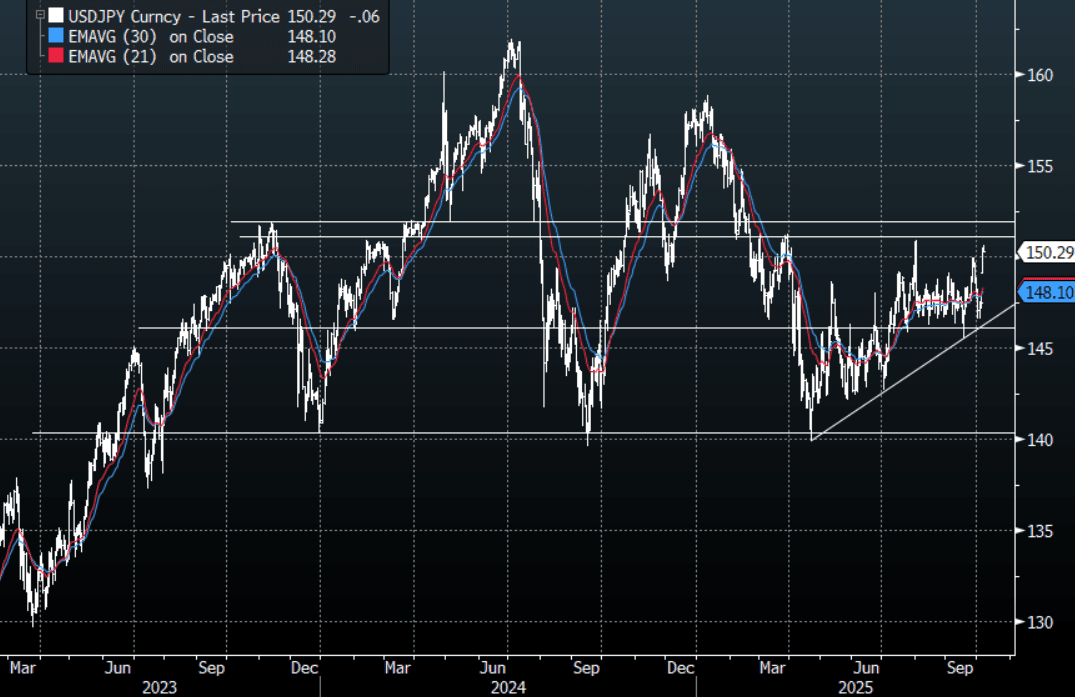

JPY: Asia Wrap - USD/JPY Consolidates Gains Above 150.00

The USD/JPY range has been 150.24 - 150.62 in the Asia-Pac session, it is currently trading around 150.30, -0.03%. The pair looks to be consolidating its gains above 150.00 after the surge higher in reaction to Sanae Takaichi’s victory. The market's attention has quickly returned to a potential looser fiscal and monetary policy on this outcome and looks to be pushing back the likelihood of an imminent rate hike. With risk roaring higher this all feeds further into the carry trade, the focus will now turn toward the pivotal 151/152 area a break of which could potentially start another leg higher. Expect dips to now find support unless there is push back on the market's views of Takaichi’s policies. There was some jaw-boning today about FX moves but realistically I would not expect any action until we cross back above the 155 area.

- The last CFTC data available showed Asset Managers remained significantly long JPY, should these moves begin to gather momentum, they could be forced to first pare back their longs and then if significant levels are broken begin to rebuild JPY shorts. Many crosses are breaking through some pivotal areas(CNH/JPY Above 21.00) and unless the government says something to contradict the markets thinking these could begin to gather momentum.

- MNI - Household Spending Above Forecasts, Supports BoJ Hike Plans : Japan household spending for August was stronger than forecast (+2.3%y/y, versus 1.2% forecast, 1.4% prior). We are below earlier 2025 highs from a y/y momentum standpoint, but the trend has steadily improved from late 2024 lows. It should add, albeit at the margins, to the case for a further BoJ rate hike, although little is priced for the Oct meeting (implied rate of 0.52%, versus a current effective rate of 0.477%).

- "KATO: KEY FOR FX TO MOVE STABLY WHILE REFLECTING FUNDAMENTALS, REFRAINING FROM COMMENTING SPECIFICALLY ON MARKET MOVES" - BBG

- "SUZUKI: CAN'T IGNORE FISCAL DISCIPLINE, CAN'T ACHIEVE JAPAN GROWTH WITHOUT INVESTMENT” - BBG

Options : Close significant option expiries for NY cut, based on DTCC data: 149.75($895m), 150.00($796m), 151.00($776m). Upcoming Close Strikes : 147.00($1.47b Oct 8) - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

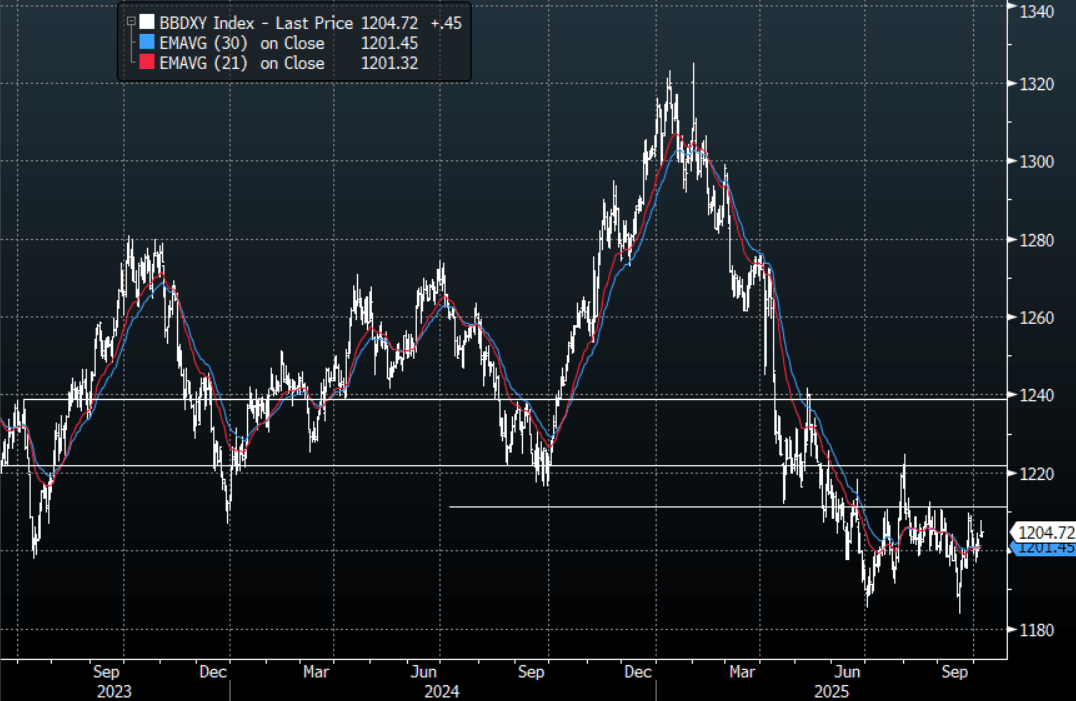

FOREX: Asia FX Wrap - The BBDXY Consolidates Gains Back Above 1200

The BBDXY has had a range of 1203.59 - 1204.88 in the Asia-Pac session; it is currently trading around 1204, -0.02%. The USD got a welcome reprieve from the surge in USD/JPY, after failing to build any downward momentum below 1200 once more can the USD build on this? The USD has historically not done well during shutdowns, but tends to bounce back quite hard when they eventually end so the market will be waiting for any signs of a breakthrough. The 1215-1225 area remains tough resistance, only a close back above 1230 would start to get USD shorts to challenge their conviction.

- EUR/USD - Asian range 1.1697 - 1.1716, Asia is currently trading 1.1700. The pair found bids back toward 1.1650 overnight. The EUR remains stuck in a range with no clear direction, 1.1550-1.1850 has captured most of the move in the last few months.

- GBP/USD - Asian range 1.3473 - 1.3487, Asia is currently dealing around 1.3470. The pair could not break through its support around the 1.3300 area, price has bounced back into the range. The market should find supply towards the 1.3500 area initially, the wider 1.3300-1.3700 range continues to dominate.

- USD/CNH - Asian range 7.1361 - 7.1445, Asia is currently dealing around 7.1370. The area around 7.1500/1600 has proved to be solid resistance for now, it looks likely we could consolidate 7.09-7.16 for the moment.

- Cross asset : SPX -0.05%, Gold $3975, US 10-Year 4.148%, BBDXY 1204, Crude Oil $61.77

- Data/Events : Germany Factory Orders, France Trade Balance, Italy Istat Releases Data on Households Consumptions in 2024

Fig 1: BBDXY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

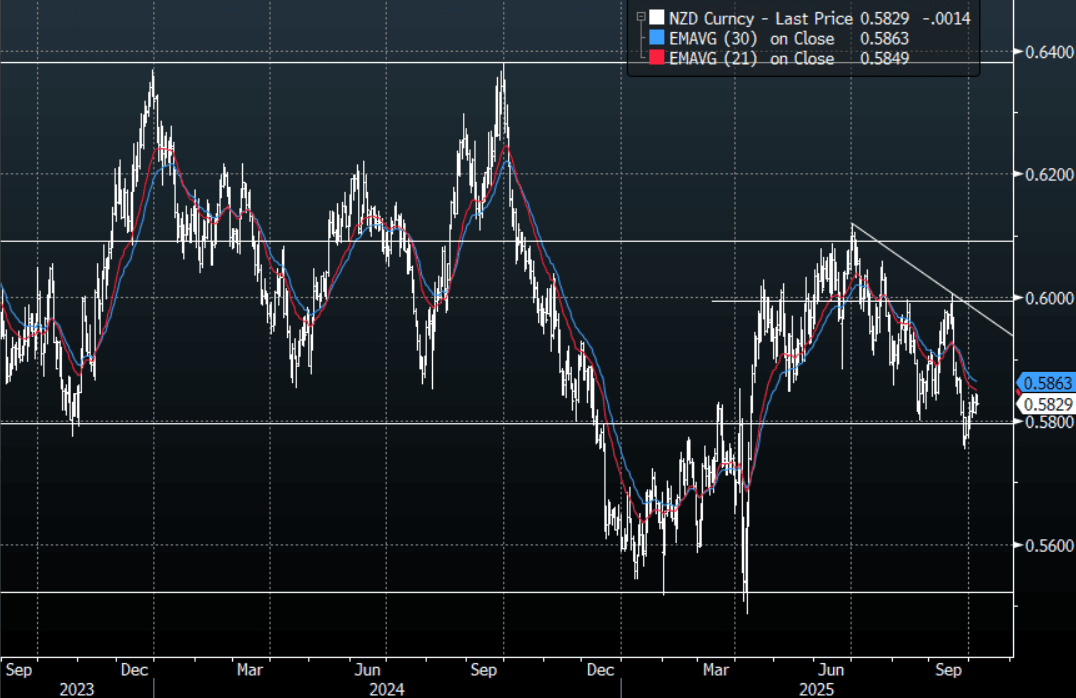

NZD: Asia Wrap - NZD/USD Trades Heavy Toward 0.5850

The NZD/USD had a range of 0.5824 - 0.5843 in the Asia-Pac session, going into the London open trading around 0.5830, -0.25%. US stocks continue to shrug off global politics and the US shutdown, the USD though got a boost from the reaction in USD/JPY. The NZD drifted higher, helped by the way risk continues to push up and probably some NZD/JPY demand as the JPY crosses turn back higher. The first sell zone should be between the 0.5850/0.5900 area for those still wanting to express a short.

- MNI - RBNZ Preview-October 2025: How Much To Ease? After Q2 GDP fell 0.9% q/q, more than the RBNZ’s -0.3% projected in August, expectations of a 50bp rate cut increased. Now 10 out of 25 analysts surveyed by Bloomberg are forecasting 50bp of easing on 8 October. The weaker GDP print means that there was more excess capacity in the economy than the RBNZ assumed in August, but the data are prone to large revisions and so it may want to stick to the 25bp rate cuts for October and November signalled in August.

- Two MPC members voted for a 50bp rate cut at the last meeting but recent and upcoming personnel changes on the committee add to the uncertainty around the October decision. 36bps of easing is priced for Wednesday’s meeting, with a cumulative 63bps by November 2025.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5820(NZD305m). Upcoming Close Strikes : none - BBG

- AUD/NZD range for the session has been 1.1324 - 1.1354, currently trading around 1.1350. The Cross has seen some selling to cap the move above 1.1400 for now, price action suggests we could potentially see more reversion back to the mean but expect dips back towards 1.1200 to now be supported.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Tech Related Plays Continue To Rally, Thailand Up Ahead Of BoT

Regional equity markets are still disrupted by holidays with China and South Korea remaining out, while Hong Kong markets are also out today. For those markets which are open, the tone is mostly positive, particularly tech sensitive plays. The on-going rally in US tech related indices amid AI/chip related gains is a positive for the region. The SOX rose 2.89% in Monday US trade, as AMD, the chip maker, announced a deal with OpenAI.

- Japan markets are tracking higher, with the NKY 225 up a further 0.75%, while the Topix is up 0.40%. There have been lots of headlines today, as the government looks to provide of cost of living relief but is also mindful of fiscal constraints (high debt to GDP the country faces). We also had stronger than expected household spending data, while FinMin Kato jawboned recent FX weakness. USD/JPY is little changed at this stage.

- The Topix Transport sub index is up a further 1.05%, while the banks index is down 0.49% (following yesterday's 1.89%). Incoming advisors to new PM Takaichi stated an Oct hike could be too soon for the BoJ.

- The Taiex index in Taiwan is up close to 2%, the fresh record highs. Chip bellwether TSMC continues to surge in local trade.

- In South East Asia the nest performer is Thailand up over 1.4%. This puts the index back above the 1300 level, back close to mid Sep highs. We ahve the BoT meeting tomorrow, where a rate cut is expected. Via the Bangkok Post: "The first set of measures focuses on simplifying initial public offering (IPO) rules to streamline listing procedures, reduce regulatory barriers and make the Thai market more competitive compared with regional peers." (announced by a Capital market taskforce) is also potentially helping sentiment.

- Other markets in the region are higher, although Malaysia is a laggard, down around 0.75%.

GOLD: Political Instability Supportive, Tuesday Sees Numerous Fed Speakers

Gold made another record high during Tuesday’s APAC trading despite little change in either the US dollar or yields. Safe-haven flows continue to push bullion towards psychological round number support at $4000 given ongoing government instability in the US, Japan and France. Gold reached $3977.44/oz earlier but then fell to $3956.02. It is currently up 0.3% to $3974.5.

- The US shutdown appears no closer to a resolution although both sides are willing to talk but the issue may be forced as 14 October approaches, when military personnel will miss their first paycheck. Polymarket has higher odds of the shutdown lasting 10-29 days rather than more than 30. The impasse is delaying key US data increasing opacity at a time of economic uncertainty and as the Fed resumes easing.

- With no political group having a majority in the French parliament and an unwillingness to cooperate, instability is likely to continue. The latest PM, Lecornu, resigned on Monday but President Macron has asked him to find a solution. The situation has unsettled markets given France’s high deficit and debt positions.

- Policy under Japan’s new PM Takaichi is also uncertain given her desire to reduce the consumption tax and previous comments against BoJ rate hikes.

- ETF inflows and central bank purchases have driven a $600 upward revision to Goldman Sachs’s end-2026 gold projection to $4900/oz, according to Bloomberg.

- Silver is little changed at $48.55 after reaching $48.653 below Monday’s high of $48.767.

- Later the Fed’s Bostic, Bowman, Miran and Kashkari as well as the ECB’s Lagarde and Machado speak. September NY Fed 1-year inflation expectations and August Germany factory orders are released.

OIL: Crude Holds Onto Post-OPEC Gains, US EIA Energy Report Out Later Today

Oil prices have continued their post-OPEC relief rally during today’s APAC session following Monday’s 1.5% rise as it unwinds some of last week’s sharp sell off. The market had worried that the November increase would exceed October’s but in the end it was in line. There was also another strike on a Russian refinery, a trend that may pick up pace as Ukraine tries to impact funds for Russia’s war and it receives more US intelligence.

- WTI moved in a narrow range and is up 0.3% to $61.87/bbl slightly off the intraday high of $61.94. It had fallen to $61.65 early in the session. Brent is 0.3% higher at $65.67/bbl after reaching $65.73.

- The market has been driven by geopolitical developments, especially related to Ukraine-Russia, and excess supply worries, which have diverging effects on oil prices. Later today the EIA short-term energy outlook will be published with the IEA and OPEC’s monthly reports next week.

- The EIA has said that it is continuing its normal schedule for now despite the US shutdown, which also includes its weekly energy data. Industry-based inventories will be released on Tuesday. Stock data remain important as builds are expected as the market shifts into surplus.

- Later the Fed’s Bostic, Bowman, Miran and Kashkari as well as the ECB’s Lagarde and Machado speak. September NY Fed 1-year inflation expectations and August Germany factory orders are released.

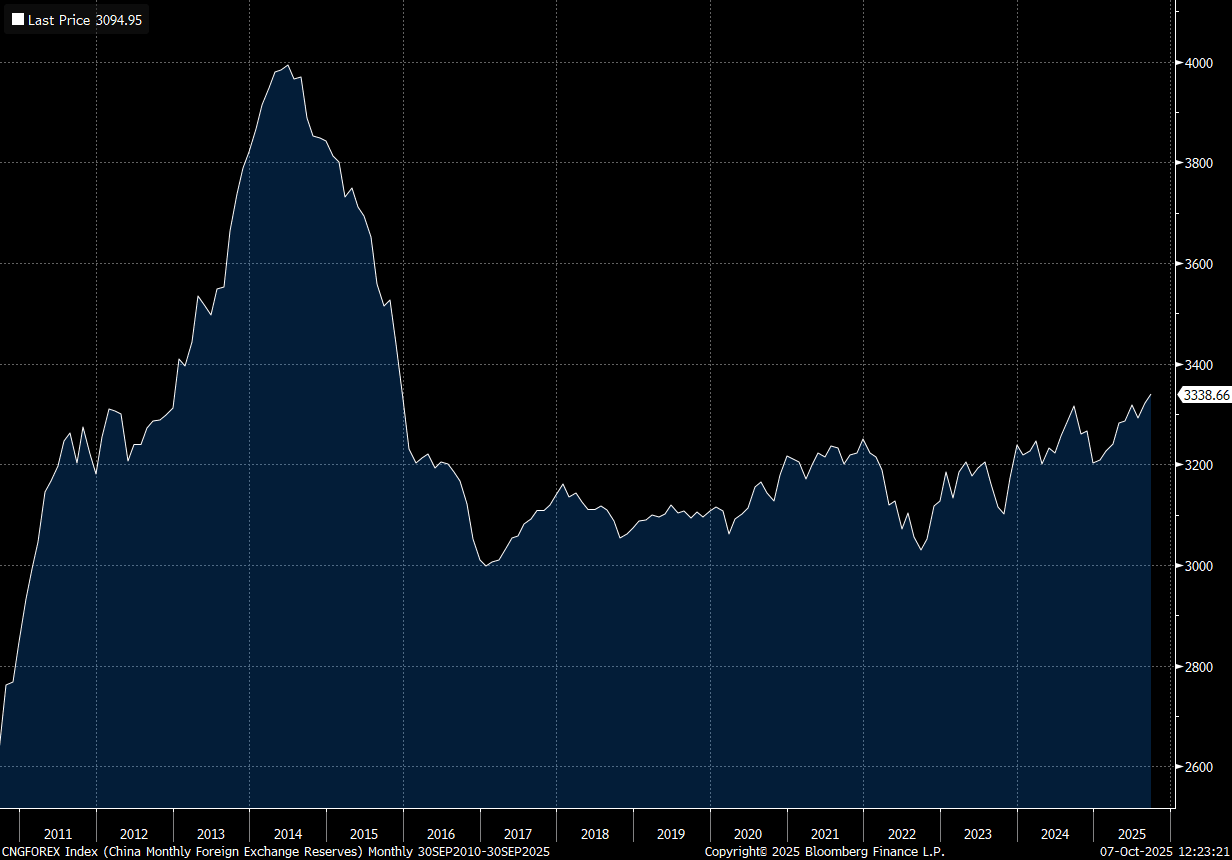

CHINA DATA: FX Reserves At Multi Year Highs, Consensus Is For Higher CNY

China markets remain closed until Thursday for National Day celebrations, but we have seen Sep FX reserves figures print. The headline rose to $3338.66bn, from $3322.15bn in August. This is the highest levels for FX reserves since end 2015, see the chart below. At face value this supports the backdrop of generally improved capital flow/strong current account picture as 2025 has unfolded. The general sell-side consensus is for stronger yuan levels as we approach year end, which fits with this backdrop. The consensus via BBG is for USD/CNY hit 7.1000 by year end, then 7.08 by end Q1 next year.

- China's gold holdings also ticked up. The Sep rise saw actual holdings up to 74.06m fine troy ounces, versus 74.02m in Aug. In nominal terms, holdings rose to $283.29bn, from $253.84bn, so valuation effects no doubt playing a role as gold continues to rally in spot terms.

- Central bank/reserve allocation to gold remains a well-established theme that is supporting the record high in gold prices.

Fig 1: China FX Reserves Continue To Track Higher

Source: Bloomberg Finance L.P./MNI

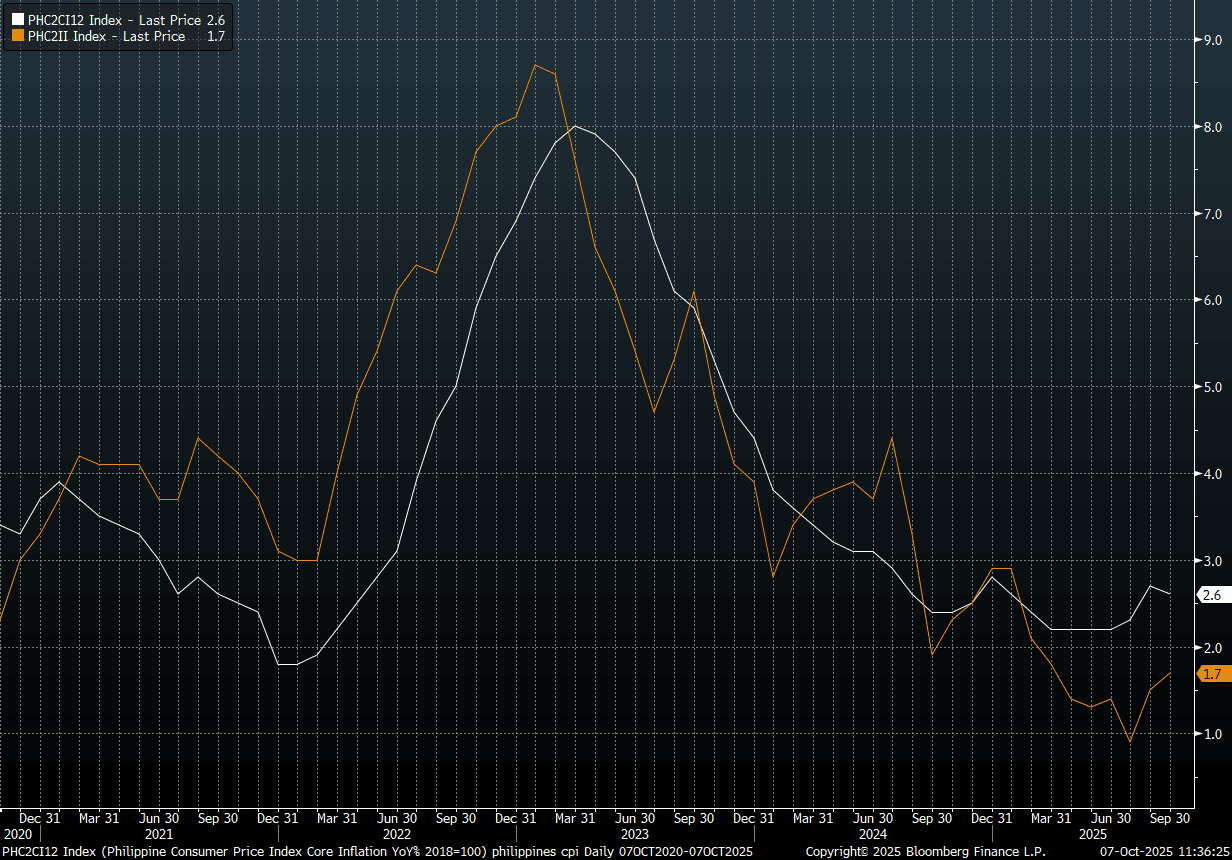

PHILIPPINES: Sep CPI Below Forecast, Y/Y Momentum Improves, BSP Seen On Hold

Philippines Sep CPI was below market forecasts for the headline. We printed flat in m/m terms, against a 0.2% forecast and 0.6% prior. In y/y terms we printed 1.7%, which was also sub forecasts (1.9%, while the Aug outcome was 1.5%). Core CPI was 2.6%y/y, down slightly from the 2.7% Aug pace. Whilst headline CPI was below expectations, it has improved from a low y/y base. The chart below plots the core (white line) and headline (orange line) CPI y/y trends. This BSP meets this Thursday and the consensus is for no change in the policy rate. Today's data is unlikely to dramatically shift thinking ahead of this meeting. There is still a case for easier policy settings, but a weaker PHP suggests some near term caution from the BSP, while previous easings this cycle are still likely working their way through the financial system. Some sell-side forecasters are looking for a 25bps cut on Thursday (6 out of 24 surveyed by BBG).

- The m/m detail didn't point to anything alarming, with most sub categories sub the m/m print that was recorded for August. Housing was 0.3%m/m (versus 0.7% in Aug), while food fell by 0.4%m/m (after a 1.2% rise in Aug).

- In y/y terms, outside of Transport, which rebounded to 1.0% (from -0.3%) we had similar outcomes to Aug.

Fig 1: Philippines Headline & Core CPI Y/Y

Source: Bloomberg Finance L.P./MNI

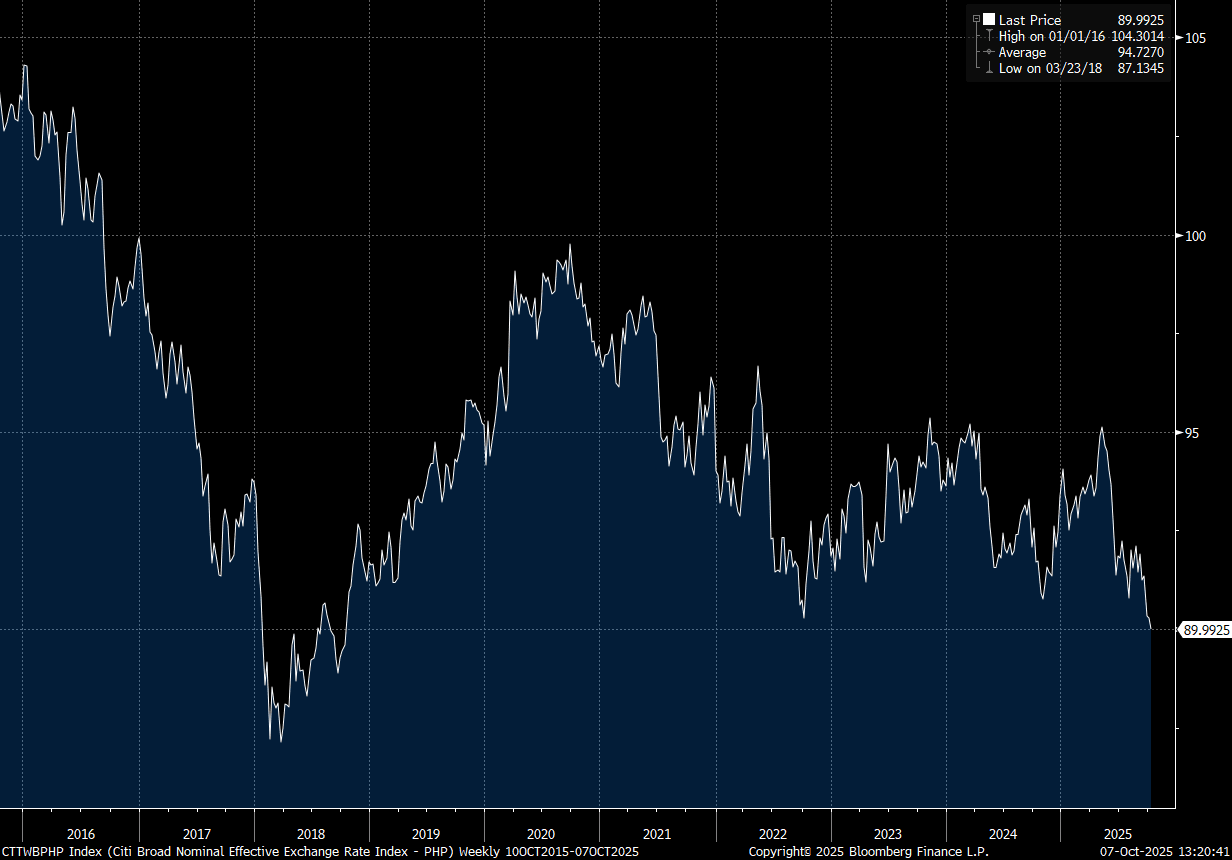

PHP: USD/PHP Continues To Find Resistance Above 58.30, NEER Quite Weak

USD/PHP continues to find resistance on moves into the 58.30/40 region. We have topped out on 5 occasions on moves into this area going back to late Sep. This suggests potential official resistance on a move beyond this region. Back in early Aug we saw a sharp move through 58.50 but this was reversed quite quickly. So again this points to official resistance around this area. We have to go back to 57.73 for the 20-day EMA support point on the downside.

- The inflation backdrop for Sep was below market forecasts, but showed sequential improvement in the headline. A further rate cut here may still be warranted from the inflation standpoint, but concern around underperforming FX trends may be a factor in helping keep the BSP to remain on hold this Thursday. The consensus is for no change, but some forecasters are expecting a 25bps cut.

- Reinforcing the point around FX weakness is the Citi PHP NEER, which is at fresh multi year lows, see below

- Growth concerns amid onshore corruption fallout, is another potential factor that could drive a rate cut (although equally the central bank may not want to show signs of panic as the government's corruption investigation continues).

- The CEO of the local stock exchange highlighted yesterday that these concerns were keeping offshore inflows away. The PCOMP is up so far today, but can't get too far away from 6000 at this stage. Offshore investors remain net sellers of local stocks.

- A similar viewpoint may be held around PHP, with offshore investors reluctant to re-engage until greater clarity is seen on the domestic/political outlook.

Fig 1: Citi PHP NEER - Continuing to Trend Lower

Source: Bloomberg Finance L.P./MNI

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 07/10/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 07/10/2025 | 0645/0845 | * | Foreign Trade | |

| 07/10/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 07/10/2025 | 1230/0830 | ** | Trade Balance | |

| 07/10/2025 | 1230/0830 | ** | Trade Balance | |

| 07/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 07/10/2025 | 1400/1000 | * | Ivey PMI | |

| 07/10/2025 | 1405/1005 | Fed's Miki Bowman | ||

| 07/10/2025 | 1430/1030 | Fed Governor Stephen Miran | ||

| 07/10/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 07/10/2025 | 1530/1130 | Minneapolis Fed's Neel Kashkari | ||

| 07/10/2025 | 1610/1810 | ECB Lagarde Speech at Business France Event | ||

| 07/10/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 07/10/2025 | 1900/1500 | * | Consumer Credit | |

| 07/10/2025 | 2005/1605 | Fed Governor Stephen Miran | ||

| 08/10/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 08/10/2025 | 2330/0830 | ** | average wages (p) | |

| 08/10/2025 | 2350/0850 | Balance of Payments | ||

| 08/10/2025 | 0100/1400 | *** | RBNZ official cash rate decision | |

| 08/10/2025 | 0500/1400 | Economy Watcher's Survey | ||

| 08/10/2025 | 0600/0800 | ** | Industrial Production | |

| 08/10/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 08/10/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 08/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 08/10/2025 | 1030/1230 | ECB Elderson In Panel at Finance Conference | ||

| 08/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 08/10/2025 | 1320/0920 | St. Louis Fed's Alberto Musalem | ||

| 08/10/2025 | 1330/0930 | Fed Governor Michael Barr |