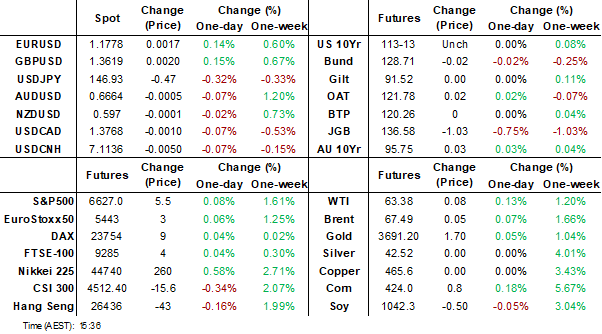

MNI EUROPEAN MARKETS ANALYSIS: Japan Election Race Heats Up

- USD/JPY came under selling pressure in our session moving back down towards 147.00 as Koizumi says he will run for the LDP leadership. Finance Minister Kato also stated he would support Koizumi's leadership bid. Koizumi would arguably be more centralist in terms of the BoJ outlook compared with known dove Takaichi. JGB futures are also softer.

- In New Zealand, the August monthly CPI series generally showed a slowdown in increases with food inflation up 0.3% m/m after 0.7% stabilising the annual rate at 5%.

- Equity sentiment was mostly positive throughout the region, particularly tech sensitive plays.

- Today US August retail sales, trade prices, IP, September NY Fed services and NAHB housing print, as well as UK labour market, euro area July IP, September ZEW survey and August Canadian CPI data.

MARKETS

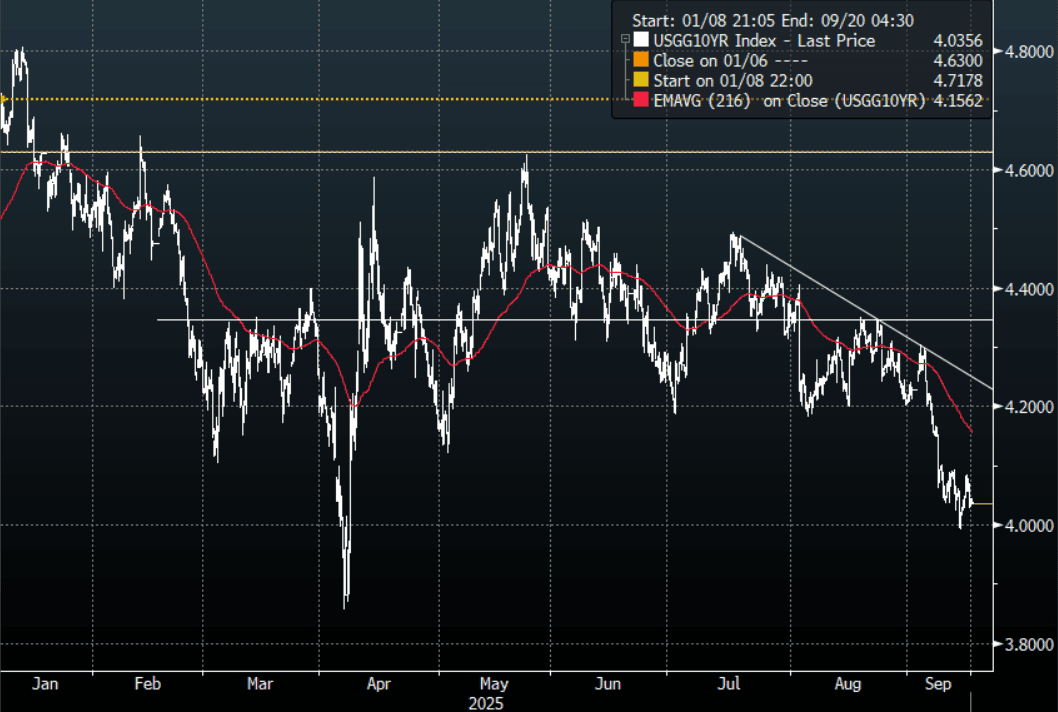

US TSYS: Asia Wrap - Quiet Session

The TYZ5 range has been 113-11 to 113-14 during the Asia-Pacific session. It last changed hands at 113-13+, down 0-01+ from the previous close.

- The US 2-year yield has edged lower trading 3.533%.

- The US 10-year yield is trading around 4.035%.

- 10-Year Yields continue to do work just above 4.00% as the market looks towards the FOMC this week. The first buy-zone is now back towards the 4.20% area where I suspect decent demand should return initially. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area. The market does seem confident of a dovish outcome, the risk is Powell does not deliver.

- MNI BRIEF: Senate Confirms White House's Miran As Fed Governor. The Senate late Monday confirmed White House Council of Economic Advisers Chair Stephen Miran to join the Federal Reserve Board of Governors, serving the final four months of a 14-year term vacated by Adriana Kugler. The vote was 48 to 47. Miran in an unprecedented arrangement is taking an unpaid leave of absence from the White House while serving out the remainder of Kugler's term

- MNI BRIEF: Trump Cannot Fire Fed's Cook, Appeals Court Rules. President Donald Trump cannot fire Federal Reserve Governor Lisa Cook, according to the U.S. Court of Appeals for the D.C. Circuit, a ruling the Justice Department will likely appeal to the Supreme Court. The ruling means that Cook, a member of the Fed’s board of governors, can participate in the two-day FOMC meeting that begins Tuesday.

- Data/Events: Retail Sales, New York Fed Services Business Activity, Industrial Production, NAHB Housing Market Index

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Weaker & Hovering Near Cheaps, 20Y Supply Tomorrow

JGB futures are weaker, -7 compared to settlement levels, after giving up early gains as trading resumed following the long weekend.

- Japan’s tertiary industry index rose 0.5% in July from the previous month, compared with economists’ estimate of +0.1%.

- (Bloomberg) "JGB traders are leaning hawkish as Shinjiro Koizumi taps Finance Minister Kato to steer his campaign. Traders see that pairing as the stronger ticket in the LDP race, and one that could give the Bank of Japan room to raise interest rates before year-end."

- (Bloomberg) "The next pain point for bond traders may come in the five-year part of the curve, according to Goldman Sachs Group Inc. strategists. Five-year notes are particularly vulnerable in Japan and Germany, where the economic outlook is improving and the country is headed toward a more sustainable tightening cycle."

- Cash US tsys are marginally richer in today's Asia-Pac session after yesterday's modest rally.

- Cash JGBs are flat to 2bps cheaper across benchmarks. The benchmark 10-year yield is 0.8bp higher at 1.602% versus the cycle high of 1.649%.

- Swap rates are flat to 3bps higher. Swap spreads are wider.

- Tomorrow, the local calendar will feature trade balance data alongside 20-year supply.

AUSSIE BONDS: Stronger & At Bests On Another Data Light Day

ACGBs (YM +4.0 & XM +6.5) are stronger and at session highs.

- "RBA'S HUNTER: CONSUMPTION LOOKING BETTER, POSITION STARTING TO TURN OVER, MONITORING VERY CLOSELY THE UNDERLYING STRENGTH OF CONSUMER SPENDING, WANT TO KEEP ECONOMY NEAR FULL EMPLOYMENT - [RTRS]"

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's modest rally.

- Cash ACGBs are 4-6bps richer with the AU-US 10-year yield differential at +18bps.

- The bills strip is +1 to +4 across contracts, with a flattening bias.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in September is given a 9% probability, with a cumulative 29bps of easing priced by year-end.

- Tomorrow, the local calendar will see Westpac Leading Index data and RBA Jones' Fireside Chat.

- The focus this week, however, will be on Thursday's August jobs data. Employment is forecast to rise 21k after July's +24.5k with the unemployment rate expected to remain at 4.2%. It will also be important to monitor underemployment, the split between full-time & part-time and hours worked. The RBA is currently expected to leave rates unchanged on September 30 as it waits for Q3 CPI on October 29.

- This week, the AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond tomorrow and A$1000mn of the 1.00% 21 December 2030 bond on Friday.

BONDS: NZGBS: Closed Richer, Monthly CPI Series Supportive

NZGBs closed 3-4bps richer across benchmarks.

- The August monthly CPI series generally showed a slowdown in increases, with food inflation up 0.3% m/m after 0.7% stabilising the annual rate at 5%. The RBNZ forecast Q3 headline inflation at 3.0% y/y in August, the top of its band, with the risk it could temporarily be above. It remains focused on the medium-term outlook, though, as it says, it can do little to impact the near term. However, the stabilisation or moderation in August is likely to be welcomed.

- The monthly price data account for around 46.5% of the quarterly CPI.

- Swap rates closed 4-5bps lower.

- RBNZ dated OIS pricing closed softer across meetings. 22bps of easing is priced for October, with a cumulative 40bps by November 2025.

- Tomorrow, the local calendar will see Q3 current account data and Westpac Q3 consumer confidence.

- The focus of the week will be on Thursday’s Q2 GDP data release. Bloomberg consensus is in line with the RBNZ’s August forecast of -0.3% q/q, bringing the annual rate to flat after declining 0.7% y/y in Q2. 25bp rate cuts are expected at both the October 8 and 26 November meetings.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond and NZ$225mn of the 4.25% May-34 bond.

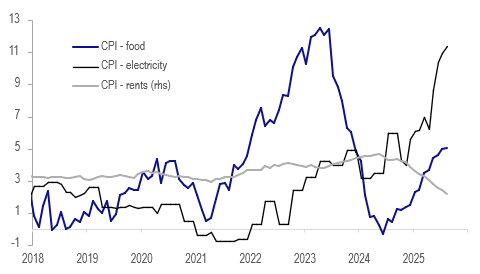

NEW ZEALAND: August Price Rises Moderate

The August monthly CPI series generally showed a slowdown in increases with food inflation up 0.3% m/m after 0.7% stabilising the annual rate at 5%. The RBNZ forecast Q3 headline inflation at 3.0% y/y in August, the top of its band, with the risk it could temporarily be above. It remains focussed on the medium-term outlook though as it says it can do little to impact the near term. However, the stabilisation or moderation in August is likely to be welcomed.

- The monthly price data account for around 46.5% of the quarterly CPI.

- There was a further pickup in fruit & veg inflation in August to 8.9% y/y from 7.3%, the highest in over two years but grocery price pressures moderated to 4.7% y/y from 5.1%. There have been sharp rises in dairy products as global prices rose 16.2% y/y in August, but that also helps NZ’s exporters.

- Existing rents rose only 0.1% m/m to be up 2.1% y/y, the lowest since April 2011. The soft rental increases reflect a generally weaker housing market with the REINZ reporting that the average house price and sales were lower in August compared to a year ago.

- Power prices continue to rise with electricity up 0.4% m/m and 11.4% y/y in August up from 11% y/y, the highest since the series began in 2012. The Q3 average is up 3.1% q/q. Gas price inflation also rose at 4.5% y/y after 4.1%. The increase has been due to changes in government policy.

- Petrol prices fell again in August after rising in July but Q3 to date is lower than Q2. They were down 2.4% y/y last month.

- Tourism-related prices fell on the month driving a moderation in annual inflation rates.

NZ monthly CPIs y/y%

Source: MNI - Market News/Statistics NZ

FOREX: Asia FX Wrap-BBDXY Breaks Below 1195 In Asia, Can It Extend Ahead Of FOMC

The BBDXY has had a range of 1193.03 - 1195.49 in the Asia-Pac session; it is currently trading around 1193, -0.10%. The USD continues to grind slowly lower, pressing and probing its recent support. A sustained break below 1195 is needed to regain the momentum lower and retest the year's lows towards 1180 where demand should return initially. A break sub 1180 would be extremely bearish, should the USD start another leg lower it would have big implications for FX and potentially see a lot of the recent ranges in G10 broken. The USD is trying to break its recent support ahead of the FOMC with the market pricing in a dovish outcome, there are obvious risks to this buy the rumour strategy. I would prefer to have optionality around FOMC and trade the event than going in naked short with a low bar to disappoint.

- EUR/USD - Asian range 1.1757 - 1.1787, Asia is currently trading 1.1775. The pair consolidated has drifted higher into the FOMC as the USD breaks down. EUR is still within its wider 1.1350-1.1850 range with a bias to the topside.

- GBP/USD - Asian range 1.3598 - 1.3625, Asia is currently dealing around 1.3615. The pair is probing the top-end of its recent 1.3350-1.3650 range, price action suggests it may be looking to break these highs and reassert its momentum higher. A sustained break above 1.3650 will initially target the year's highs just below 1.3800, though here it would open a move back to the 1.4200/1.4300 area.

- USD/CNH - Asian range 7.1119 - 7.1198, the USD/CNY fix printed 7.1134, Asia is currently dealing around 7.1130. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.10%, Gold $3682, US 10-Year 4.034%, BBDXY 1193, Crude Oil $63.46

- Data/Events : Germany ZEW Survey Expectations, Italy CPI, EZ ZEW Survey Expectations/ Labour Costs/ Industrial Production

Fig 1: BBDXY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

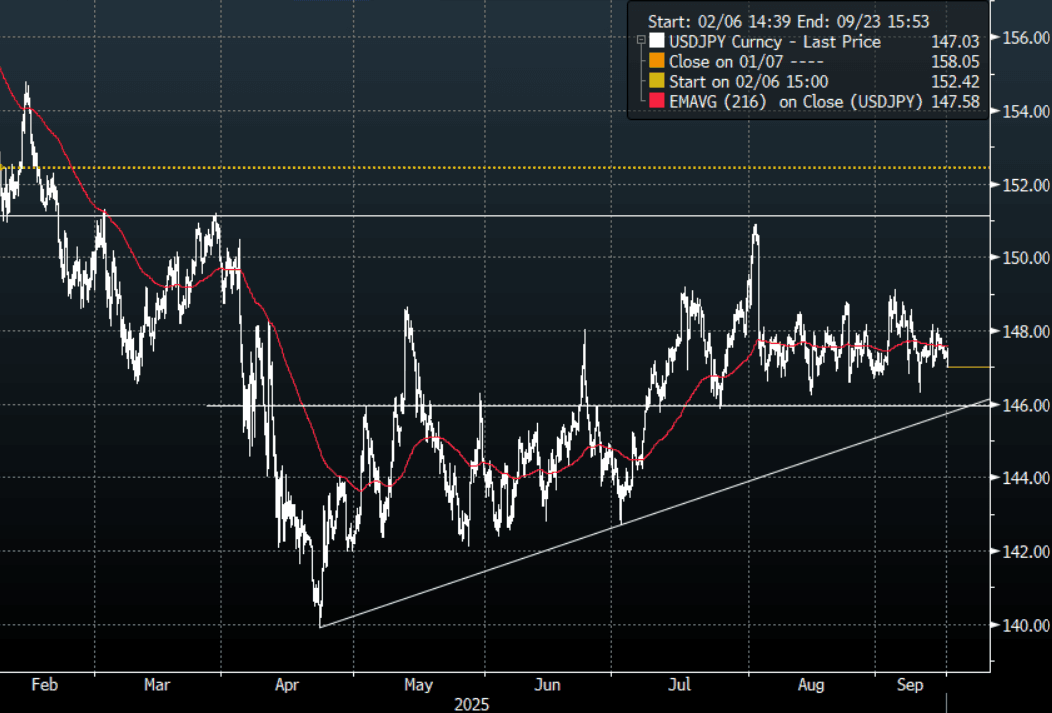

JPY: Asia Wrap - USD/JPY Moves Lower As Koizumi Enters The Leadership Fray

The USD/JPY range has been 146.97 - 147.54 in the Asia-Pac session, it is currently trading around 147.05, -0.25%. USD/JPY came under selling pressure in our session moving back down towards 147.00 as Koizumi says he will run for LDP leadership. The price remains in the middle of its recent 146-149 range, and we need a convincing break to see a clearer direction again. CFTC data shows leveraged funds paring back some of their short JPY position last week but remain core short, looking for this support to continue to hold. A move back below 145/146 is needed to potentially start seeing these positions being flushed out.

- (Bloomberg) - "JGB Traders See Koizumi-Kato Team Endorsing BOJ Hike. JGB traders are leaning hawkish as Shinjiro Koizumi taps Finance Minister Kato to steer his campaign. Traders see that pairing as the stronger ticket in the LDP race, and one that could give the Bank of Japan room to raise interest rates before year-end."

- "JAPAN CHIEF CABINET SECRETARY HAYASHI, SPEAKING AS CANDIDATE FOR LDP LEADERSHIP RACE: WILL INCLUDE POLICY MEASURES TO KEEP BUDDING MOMENTUM OF ECONOMIC RECOVERY GOING, WILL SEEK PARTNERSHIP WITH OTHER OPPOSITION PARTIES AFTER SOLIDIFYING KEY POLICIES" RTRS

- MNI BOJ WATCH: Board To Hold, Focus On CPI, Trade. The Bank of Japan board is likely to keep its policy rate unchanged at 0.50% at the two-day meeting ending Friday as it assesses the impact of tariffs on the U.S. and Japanese economies.

- Options : Close significant option expiries for NY cut, based on DTCC data: 150.00($1.49b), 146.00($1.41b), 145.00($838m).Upcoming Close Strikes : 145.00($1.32b Sept 19), 145.70($1.22b Sept 17), 146.40($797m Sept 19) - BBG.

- CFTC data shows last week asset managers again added to their JPY longs again as they look to rebuild their position +87239( Last +78427), leveraged funds reduced their short position perhaps losing confidence the support will continue to hold -49591(Last -66914).

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

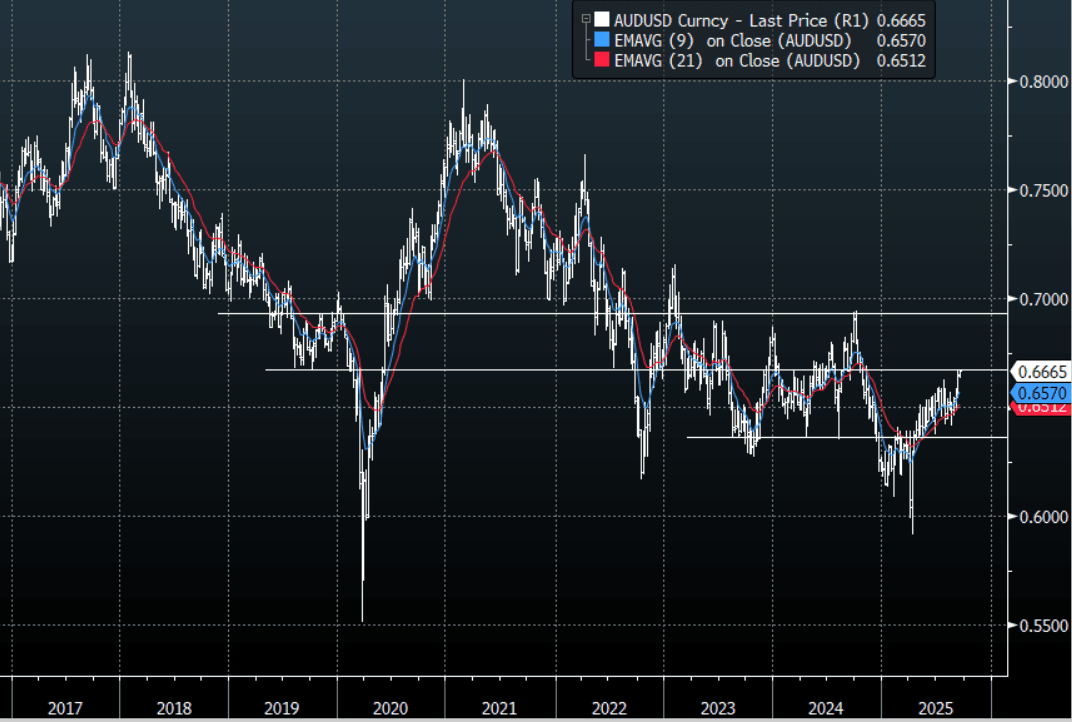

AUD: Asia Wrap - AUD/USD Consolidates Just Above 0.6650

The AUD/USD has had a range of 0.6663 - 0.6676 in the Asia- Pac session, it is currently trading around 0.6665, -0.05%. US stocks continue to push higher, the risk is the market is getting ahead of itself looking for a potential positive outcome from the FOMC, so the bar for disappointment is being lowered. The AUD continues to be supported and grinds higher. Should the USD break and extend lower we could see the AUD gain momentum above 0.6650/0.6700 and potentially target levels back towards 0.6900/0.7000. The price action suggests dips will be supported for now as we await confirmation of this potential break higher, the first buy-zone is back towards the 0.6550 area.

- "RBA'S HUNTER: CONSUMPTION LOOKING BETTER, POSITION STARTING TO TURN OVER, MONITORING VERY CLOSELY THE UNDERLYING STRENGTH OF CONSUMER SPENDING, WANT TO KEEP ECONOMY NEAR FULL EMPLOYMENT - [RTRS]"

- Bloomberg - “Investors Cut Dollar Exposure at Record Pace, Deutsche Bank Says. “The FX implications are clear: foreigners may have returned to buying US assets (albeit as we wrote last week at a reduced pace), but they don’t want the dollar exposure that goes with it,” Saravelos wrote. “For every hedged dollar asset that is bought, an equivalent amount of currency is sold to remove the FX risk.”

- This adds credence to recent reports of Aussie Pension/Super funds looking to increase their hedging ratios as the AUD starts to move higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD549m). Upcoming Close Strikes : 0.6600(AUD894m Sept 18), 0.6750(AUD1.16b Sept 19) - BBG

- CFTC Data last week shows Asset managers slightly increasing their shorts -68333(Last -66025), the Leveraged community pulled back the shorts they had just started to rebuild -5081(Last -11860).

- AUD/JPY - Asia-Pac range 98.04 - 98.39, Asia is trading around 98.00. The pair continued to consolidate its recent gains, the focus now turns back towards the 99.00/100.00 area. Dips back towards 96.50/97.00 should be expected to be supported now first up.

Fig 1: AUD/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

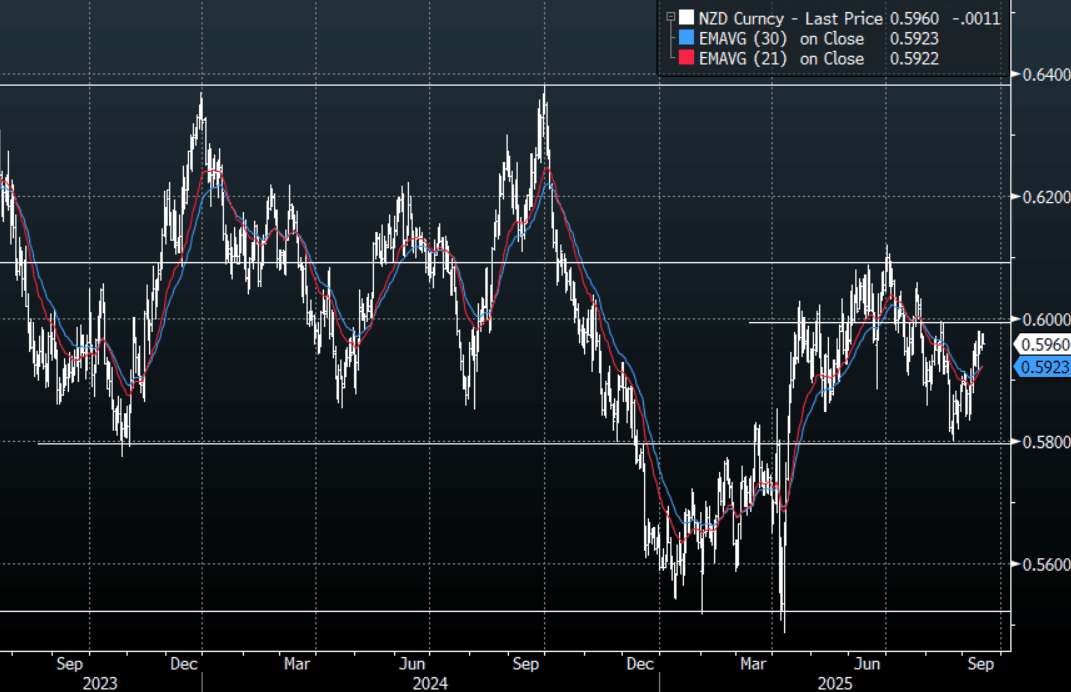

NZD: Asia Wrap - NZD/USD Stalls Towards 0.6000

The NZD/USD had a range of 0.5956 - 0.5975 in the Asia-Pac session, going into the London open trading around 0.5960, -0.18%. US stocks continue to push higher, the risk is the market is getting ahead of itself looking for a potential positive outcome from the FOMC, so the bar for disappointment is being lowered. The USD continues to look vulnerable, which continues to support the NZD. A close back above 0.6000 would negate any semblance of the downward pressure it was exhibiting, but for those that have a bearish view this remains a decent entry point to express that.

- August Price Rises Moderate: The August monthly CPI series generally showed a slowdown in increases with food inflation up 0.3% m/m after 0.7% stabilising the annual rate at 5%. The RBNZ forecast Q3 headline inflation at 3.0% y/y in August, the top of its band, with the risk it could temporarily be above. It remains focussed on the medium-term outlook though as it says it can do little to impact the near term. However, the stabilisation or moderation in August is likely to be welcomed

- Westpac Expects Inflation To Be Below 3% By End 2025. NZ food inflation stabilised at 5.0% y/y in August, its highest since November 2023, while increases for existing rents moderated 0.3pp to 2.1% y/y, the lowest since 2011. The stabilisation or moderation, especially travel-related prices, in August is likely to be welcomed by the RBNZ as it sees a risk that Q3 could print above 3%, the top of the band. Westpac believes that it will be below this level by year end.

- “NZ AUG. GOVT. BONDS HELD BY FOREIGNERS FALL TO 61.5%" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5825(NZD1.01b Sept 17), 0.5900(NZD860m Sept 17), 0.5935(NZD537m Sept 18) - BBG

- AUD/NZD range for the session has been 1.1158 - 1.1191, currently trading 1.1175. The Cross is consolidating above 1.1100, dips back towards 1.1000/1.1050 should be supported now. A break above the multiple highs towards the 1.1200 area is needed to regain the momentum higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: New Highs for the KOSPI (amended)

Following on from record highs from the NIKKEI, the KOSPI has reached new all time highs following the withdrawal of the Capital Gains Tax changes and expectations that the earnings from key chip manufacturers are going to continue to strengthen. The NIKKEI is up on optimism on tech stocks following the moves in the US overnight and in Beijing a ruling that Nvidia violated anti-monopoly laws, gave China's chip stocks a boost too.

- Despite the tech news and the positivity elsewhere, China's stocks did very little today with the Hang Seng barely up, CSI 300 down -0.38%, Shanghai down -0.10% and Shenzhen flat.

- The NIKKEI continues to track higher and is up +0.55% today and over 12% in the last 5 trading days.

- The KOSPI rallied over 1.1% to reach new all time highs.

- The TAIEX in Taiwan caught a bid and is up over 1%.

- The Jakarta Composite is one of the few decliners, down -0.23%.

- The NIFTY 50 has kicked off the Tuesday trading day, up +0.43%

ASIA STOCKS: Inflows Mostly Positive, Some Slowing For South Korea & Taiwan

Most EM Asia markets saw positive inflows to start the week (although Malaysia remained closed, returning tomorrow). The pace of inflows was positive for both South Korea and Taiwan, albeit down from recent highs. The 5-day sums for both markets remains quite healthy and some slowdown in inflows is not that surprising given the recent surge into these markets from a flow standpoint. Taiwan for September to date has already seen +$7.45bn in net inflows, which is close to 2025 highs, and we only around halfway through the month.

- We also have key event risk this week in terms of the Fed decision. Declining US yields, amid rising Fed easing expectations, has no doubt been a factor in tech equity rally. Overnight the SOX index was up for the 8th straight session.

- Elsewhere, Indian inflows ended last week on a more positive, helping to drag the 5-day sum of net inflows into positive territory. Indian markets have recovered some ground since the start of the month but remain sub late Aug highs.

- Indonesian inflows were positive yesterday as sentiment continued to recover following the FinMin replacement.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 147 | 3040 | -2152 |

| Taiwan (USDmn) | 144 | 5059 | 7549 |

| India (USDmn)** | 116 | 304 | -15408 |

| Indonesia (USDmn) | 64 | -305 | -3664 |

| Thailand (USDmn) | 10 | -12 | -2543 |

| Malaysia (USDmn)* | 25 | -2 | -3808 |

| Philippines (USDmn) | -8 | -5 | -736 |

| Total (USDmn) | 497 | 8079 | -20762 |

| * Data Up To Sep 11 | |||

| * Data Up To Sep 12 |

Source: Bloomberg Finance L.P./MNI

OIL: Crude Slightly Higher As Push For More Restrictions On Russia Continues

Oil prices have continued trending higher during today’s APAC session as the market monitors sanction developments on Russia. WTI is up 0.3% to $63.48/bbl, close to the intraday high of $63.52, while Brent is 0.2% higher at $67.60/bbl after reaching $67.68 earlier. The USD index is down 0.1%.

- The US has said it will follow any new restrictions that the EU imposes but only if it stops its own imports of Russian oil. Today US Senator Graham, proponent of anti-Russia legislation, chastised Slovakia and Hungary for its consumption. The EU is apparently looking at sanctions on Indian and Chinese companies that facilitate Russia’s oil trade, according to Bloomberg.

- While currently geopolitical risk is driving oil prices, the market remains concerned about the projected surplus for 2026 and is monitoring supply and demand fundamentals. On Tuesday, US industry-based inventory data are released.

- The key event this week is the Fed’s 17 September decision. With a 25bp rate cut widely expected, attention will be on the tone of comments from Chair Powell to gauge the outlook for policy and thus US energy demand.

- Kuwait has discounted crude for delivery to Europe by $1/bbl while Asia faces a premium of over $1/bbl and the US $3.90/bbl.

- Today US August retail sales, trade prices, IP, September NY Fed services and NAHB housing print, as well as UK labour market, euro area July IP, September ZEW survey and August Canadian CPI data.

Gold Off New Record High, Waiting For Direction From Fed

Gold has moved in a narrow range today reaching $3689.37, a new record high, following news that an appeals court ruled that Fed Governor Cook can’t be removed and that President Trump’s choice to replace former Governor Kugler, Stephen Miran, was approved by the Senate. Both will sit on the FOMC at this week’s meeting. With a 25bp cut widely expected, the updated forecasts and tone of Chair Powell’s comments will guide the monetary policy outlook as well as upcoming data releases, which is then likely to drive gold’s direction.

- Gold fell to $3674.82 after reaching the new record. It is currently 0.1% higher at $3682.0 finding some support from a softer US dollar (BBDXY -0.1%) while yields are little changed. It remains below round number resistance at $3700.0.

- Silver is down 0.1% to $42.63 but off the intraday low of $42.348. It reached $42.75 before declining. Resistance to watch is $42.974.

- Equities are generally stronger with the S&P e-mini up 0.1% and KOSPI +1.3% but CSI 300 down 0.4%. Oil prices continued to trend higher with WTI +0.2% to $63.45/bbl. Copper is down 0.7%.

- Today US August retail sales, trade prices, IP, September NY Fed services and NAHB housing print, as well as UK labour market, euro area July IP, September ZEW survey and August Canadian CPI data.

INDONESIA: MNI Bank Indonesia Preview-Sep 2025: BI Pause, Monitors Events

- Download Full Report Here

- After Bank Indonesia (BI) has had to intervene to defend the rupiah over the last two weeks due to political unrest and then President Prabowo’s decision to remove respected finance minister Indrawati, rates are likely to be left at 5% on 17 September especially given the central bank’s focus on FX stability.

- BI has monthly meetings, so it can be cautious to ensure that the rupiah stabilises, that there aren’t significant portfolio outflows and to monitor political and fiscal developments.

- It expects inflation to stay within its target band this year and next and has eased 125bp so far this cycle and so it can continue to focus on FX stability and be cautious with further rate cuts. We expect it to retain its easing bias.

CHINA: Country Wrap: Shift to Equities Continues

Market Summary: Despite the positivity elsewhere, China's stocks did very little today with the Hang Seng barely up, CSI 300 down -0.38%, Shanghai down -0.10% and Shenzhen flat. The Yuan Reference Rate at 7.1027 Per USD; Estimate 7.1163 and the 10-Yr is a touch higher in yield at 1.80%

- China’s new household deposits contracted in July and August from the year before, while deposits from non-bank financial institutions surged, in a sign that people have been moving money out of their savings and into the stock market for the past two months amid record-low interest rates, according to the latest data. (source Yicai)

- China’s economy is expected to maintain steady growth in the third quarter despite weaker industrial and investment data in August, according to the National Bureau of Statistics. (source Yicai)

INDONESIA: Country Wrap: Three Million Jobs to be Created

Market Summary: The Jakarta Composite is one of the few decliners, down -0.23% today whilst IDR rallied +0.25% to 16,377; close to the BI target of 16,300. Bonds are strong with the yield curve shifting lower, whilst steepening. The 10-Yr is down -1bp at 6.32%

- Indonesia's Coordinating Minister for Economic Affairs has announced that five government priority programs are projected to generate more than 3 million jobs nationwide. (source Antara)

- Indonesia's Finance Minister said that the government has not set a specific funding quota for state-owned banks to finance village cooperatives. He explained that the recent Rp200 trillion (US$12.2 billion) injection into five state-owned banks from the government did not include such requirements. (source Antara)

ASIA FX: KRW & TWD Rally On Equity Gains/Inflows, USD/CNH Near YTD Lows

USD/Asia pairs are lower across the board. KRW, TWD and THB have been the best performers. USD/CNH is lower but at 7.1130 hasn't been able to test under 7.1100. The USD/CNY fix remained above 7.1000, while equity sentiment was a touch softer. Focus is on the Friday call between US President Trump and China President XI, with the two countries reportedly reaching an agreement on TikTok.

- Spot USD/KRW continues to track lower, the pair last close to 1379. We are up around 0.50% in won terms so far today. This puts the pair to fresh multi week lows. Aug 13 lows were just under 1376. Broader USD sentiment is mostly softer, although Asian currencies are outperforming the majors at this stage. The won is also benefiting from the buoyant equity mood. Onshore equities continue to rally, the Kospi up a further +1.2% today to fresh cycle highs.

- Spot USD/TWD has broken lower as well. We were last around 30.10, up 0.40% in TWD terms. The 1 month NDF is up 0.50% versus the USD and back sub 30.00. Similar drivers to the KRW are in play.

- USD/THB is back under 31.75, unwinding a good chunk of Monday's bounce (highs at 31.965). Focus remains very much on what the new government may do to curb THB outperformance. This comes after new PM Anutin met with industry leaders yesterday and pledged to address concerns over the stronger baht. The Federation of Thai Industries stated that USD/THB's ideal level is in the 34-35 region.

- USD/PHP is tracking back towards 57.00, up around 0.30% so far today in PHP terms. Peso is still lagging broader USD softness.

- USD/IDR is back towards 16375, up around 0.20% so far today. This keeps us within recent ranges. Focus tomorrow will be on the BI decision, although the central bank is widely expected to be on hold.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 16/09/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/09/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/09/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/09/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/09/2025 | 0800/1000 | *** | HICP (f) | |

| 16/09/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 16/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 16/09/2025 | 0900/1100 | ** | EZ Industrial Production | |

| 16/09/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/09/2025 | 1230/0830 | *** | CPI | |

| 16/09/2025 | 1230/0830 | *** | Retail Sales | |

| 16/09/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 16/09/2025 | 1230/0830 | *** | Retail Sales | |

| 16/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 16/09/2025 | 1315/0915 | *** | Industrial Production | |

| 16/09/2025 | 1400/1000 | * | Business Inventories | |

| 16/09/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 16/09/2025 | 1400/1000 | * | Business Inventories | |

| 16/09/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 16/09/2025 | - | Bank of Canada Meeting | ||

| 17/09/2025 | 0600/0800 | ** | Unemployment | |

| 17/09/2025 | 0600/0700 | *** | Consumer inflation report | |

| 17/09/2025 | 0730/0930 | ECB Lagarde at ECB Annual Research Conference | ||

| 17/09/2025 | 0800/1000 | ECB Cipollone At Associazione Bancaria Italiana EC Meeting | ||

| 17/09/2025 | 0900/1100 | *** | EZ HICP Final | |

| 17/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 17/09/2025 | 1115/1315 | ECB Cipollone Speaks at Netherlands Central Bank Resilience Conference | ||

| 17/09/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/09/2025 | 1230/0830 | *** | Housing Starts | |

| 17/09/2025 | 1230/0830 | *** | Housing Starts | |

| 17/09/2025 | 1345/0945 | *** | Bank of Canada Policy Decision |