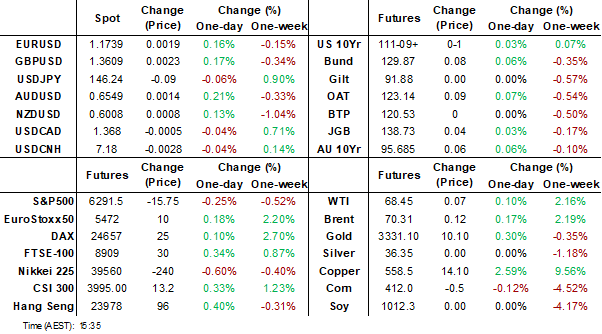

MNI EUROPEAN MARKETS ANALYSIS: Copper Up On 50% Tariff

- Trump threatened Brazil with 50% tariffs late in US trade on Wednesday. Following this he confirmed a 50% tariff for copper would come into effect on Aug 1. Broaqder risk sentiment hasn't been impacted much outside of some modest weakness in US equity futures. Copper prices are higher as well. BRL lost 2.3% for Wednesday's session.

- Japan's June PPI was touch below forecasts, but the down move in import prices may stabilize if USD/JPY holds its recent bounce. As expected the BOK held rates steady, citing financial stability concerns.

- Looking ahead, we have German final CPI for June. In the US, initial jobless claims are out.

MARKETS

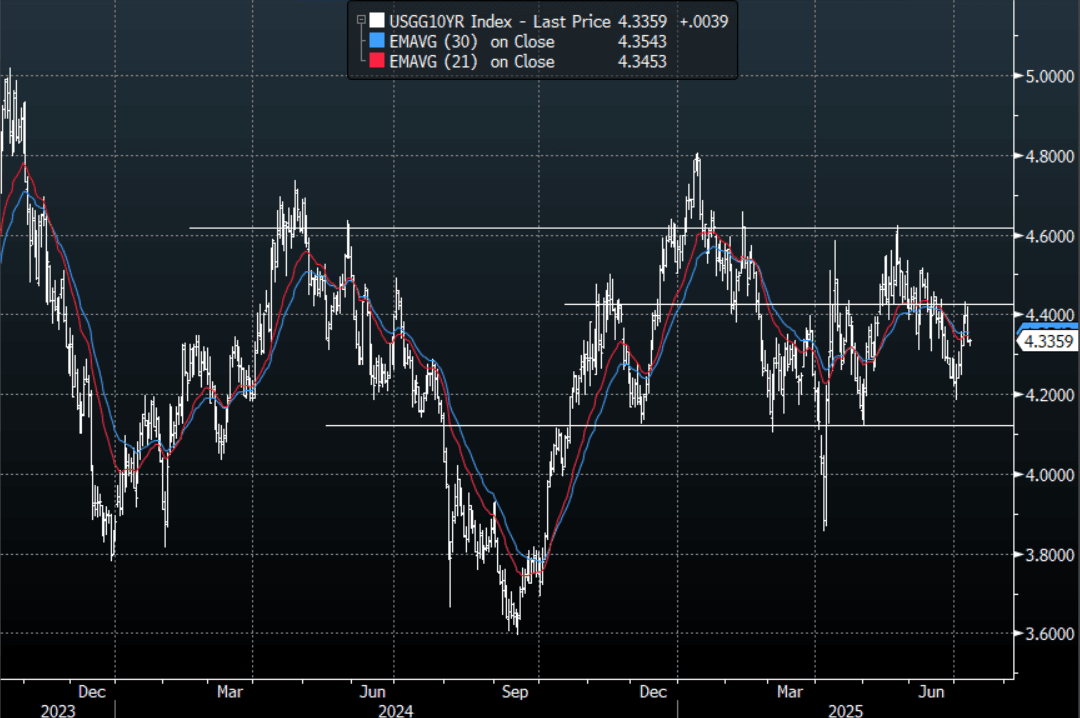

US TSYS: Front-End Yields Edge Higher In Quiet Session

The TYU5 range has been 111-09 to 111-13+ during the Asia-Pacific session. It last changed hands at 111-10, up 0-01+ from the previous close.

- The US 2-year yield has edged higher trading around 3.85%, up 0.01 from its close.

- The US 10-year yield has edged higher trading around 4.335%, up slightly from its close.

- The 10-year yield has topped out just above the 4.40% area, giving the bulls some reprieve. No clear long-term direction though has seen the 10-year chop around in a wider 4.10% - 4.60% range for most of the year, with the 4.40% area being the pivot. A sustained close back above the 4.45% area could see more of the longs pared back but while this area holds they should be happy to stick with their position looking for a move back to the lower end of the range.

- Nick Timiraos on X: ”The next few months of inflation data will offer a key test of competing theories about whether tariffs will prove inflationary and animate potential Fed divisions over how to manage any costs if forecasts are wrong—in either direction.”

- (Bloomberg) -- “Investors will monitor ultra-long bond auctions in Japan and the US later Thursday to gauge concerns of how fiscal discipline may impact demand.”

- "JAPAN 20-YEAR BOND BID-COVER RATIO 3.15 VS 12-MONTH AVG 3.29" - BBG

- Data/Events: Initial Jobless Claims, US To Sell $22 Bln 30-year Bond.

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Bull-Flattener After 20Y Auction, BoJ Regional Assessment Out

JGB futures are slightly firmer, +9 compared to settlement levels.

- Outside of the previously outlined PPI and International Investment Flows, there hasn't been much by way of domestic drivers to flag.

- Today’s 20-year JGB auction delivered mixed results across key metrics. The low price underperformed dealer forecasts, which were set at 100.10 according to a Bloomberg poll. However, the cover ratio increased to 3.1462x from 3.1070x in the previous auction and the auction tail shortened to 0.18 from 0.28.

- (RTRS) The BoJ reports in its regional assessment that some firms are delaying or reviewing capital spending due to global trade policy uncertainty. While the impact of US tariffs has been limited so far, firms are concerned about weakening global demand and rising US prices. Many regions saw strong wage hikes, though some firms may cut bonuses if profits fall. Views on future wage increases are mixed. Firms continue raising prices to offset rising costs.

- Cash US tsys are flat to slightly cheaper, with a flattening bias, in today's Asia-Pac session.

- Cash JGBs are flat to 6bps richer across benchmarks, with a flatter curve. The benchmark 20-year yield is 3.1bps lower at 2.484% versus the cyclical high of 2.596%.

- Swap rates are flat to 3bps lower.

- Tomorrow, the local calendar will empty.

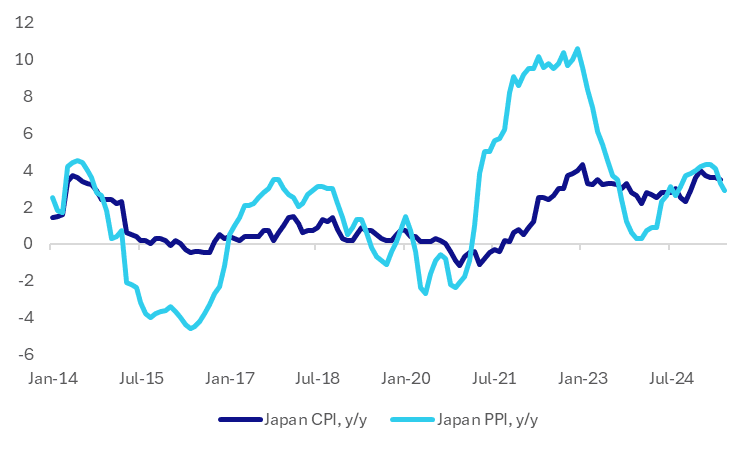

JAPAN DATA: PPI Slightly Below Forecasts, Import Prices Down Sharply Y/Y

The Japan June PPI saw the m/m outcome fall -0.2%, against a +0.1%m/m forecast. The prior outcome was revised a touch to -0.1% (originally reported as a 0.2% dip). In y/y terms, the PPI was 2.9% in line with market forecasts, but down from the revised 3.3% May pace.

- The chart below overlays the PPI against headline Japan CPI, both in y/y terms. At face value the PPI is suggesting some further loss of momentum in headline CPI pressures. The PPI, not surprisingly, has historically been more volatile than CPI outcomes.

- In terms of the PPI detail, manufacturing PPI was down 0.2%, the third straight monthly fall. Petroleum, coal was down 4.5% m/m, which was another monthly drag. This sub category and iron and steel were the weakest in y/y terms.

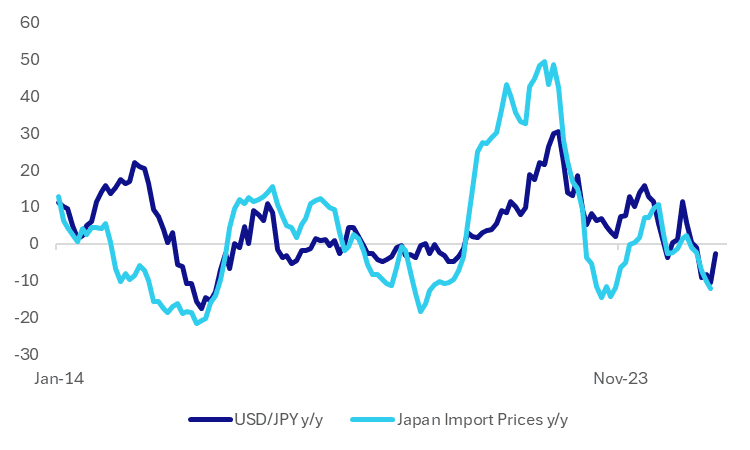

- Import prices continued to fall, down 1.7% m/m. In y/y terms we fell -12.3%. The second chart below overlays import prices versus USD/JPY y/y changes. The end July read for USD/JPY y/y assumes that the current spot levels (near 146.00) are maintained.

- This suggests the downside impetus to import prices (in y/y terms) may start to wane if USD/JPY holds the bulk of its recent correction higher.

Fig 1: Japan PPI and CPI, Y/Y

Source: Bloomberg Finance L.P./MNI

Fig 2: Japan Import Prices and USD/JPY, Y/Y

Source: Bloomberg Finance L.P./MNI

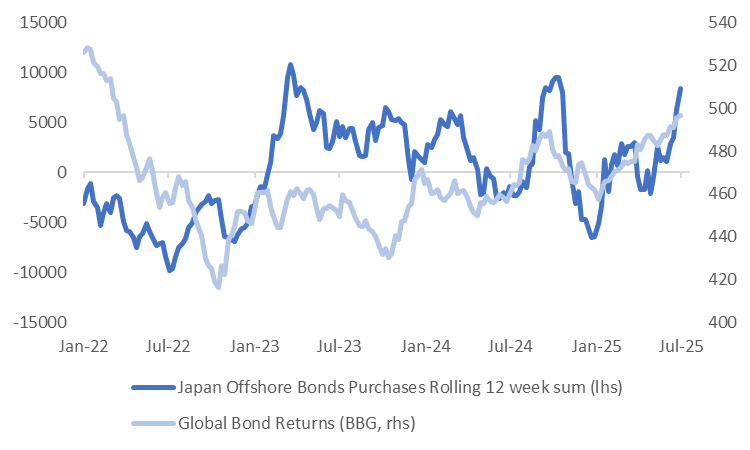

JAPAN DATA: Local Investors Buy Offshore Bonds In Size

The standout for last week's investment flows was Japan buying of overseas bonds, see the table below. The +¥1.65trln in net buying was the fourth straight week of net buying for this segment. It was also the largest weekly flow since mid May. The trend for buying offshore bonds has been reasonably firm in recent months, with just under ¥8trln of net purchases of offshore bonds since the start of May. This positive backdrop fits with the continued rise in global bond returns. The chart below overlays the rolling 12 week sum of net bond purchases against global bond returns.

- Elsewhere, we saw local investors sell overseas stocks. Local investors have now sold offshore stocks in seven out of the last eight weeks. Last week's small net purchase briefly interrupted this selling trend.

- In terms of inflows into Japan assets, offshore investors remained net buyers of local stocks. This has been the dominant trend in this space going back to the start of April. We have only had one week of outflows during this period.

- Offshore investors sold local bonds last week, after strong net buying in the week prior.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending July 4 | Prior Week |

| Foreign Buying Japan Stocks | 611.7 | 651.3 |

| Foreign Buying Japan Bonds | -164.6 | 1059.1 |

| Japan Buying Foreign Bonds | 1656.8 | 182.8 |

| Japan Buying Foreign Stocks | -512.7 | 190.6 |

Source: Bloomberg Finance L.P./MNI

Fig 1: Japan Offshore Bond Purchases & Global Bond Returns

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Richer, Treasurer Chalmers & RBA Board Agree On Communication

ACGBs (YM +4.0 & XM +7.0) sit richer, hovering near Sydney session bests, on a data-light day.

- (Bloomberg) -- Australian Treasurer Jim Chalmers and the Reserve Bank's interest-rate setting board have agreed that members will conduct at least one speech or public engagement a year, as well as publishing unattributed votes.

- Cash US tsys are flat to slightly cheaper, with a flattening bias, in today's Asia-Pac session. Today's US calendar: Initial Jobless Claims and $22 Bln 30-year bond auction.

- (Bloomberg) "At the end of the day, however, the US isn't the main game for Australian exports - the bigger threat to the economy from tariffs stems from the impacts on China and Japan, and on consumer and business confidence."

- Cash ACGBs are 5-7bps richer with the AU-US 10-year yield differential at -6bps.

- The bills strip has bear-flattened, with pricing flat to +4.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in August is given a 90% probability, with a cumulative 62bps of easing priced by year-end.

- Tomorrow, the local calendar will be empty apart from the AOFM’s planned sale of A$1000mn of the 2.75% 21 November 2029 bond.

BONDS: NZGBS: Closed With A Bull-Flattener

NZGBs closed showing a solid bull-flattener, with benchmark yields 4-9bps lower.

- With the NZ-US and NZ-US 10-year yield differentials little changed on the day, today’s move looks to have been driven from abroad.

- Cash US tsys are flat to slightly cheaper, with a flattening bias, in today's Asia-Pac session. Today's US calendar: Initial Jobless Claims and $22 Bln 30-year bond auction.

- Today’s weekly supply showed cover ratios ranging from 2.64x (Apr-29) to 3.50x (May-35).

- Swap rates closed 3-8bps lower, with the 2s10s curve flatter.

- MNI RBNZ Review (see link): The central bank considered cutting rates, largely due to concerns around faltering economic momentum. However, with near term inflation pressures expected to be firmer, the case to hold presented a more compelling argument. The central bank maintained an easing bias, subject to medium-term inflation pressures subsiding. Note Q2 CPI data prints on July 21.

- RBNZ dated OIS pricing closed little changed across meetings. 18bps of easing is priced for August, with a cumulative 33bps by November 2025.

- Tomorrow, the local calendar will see BusinessNZ Manufacturing PMI.

RBNZ: MNI RBNZ Review-July 2025: On Hold, Easing Bias Still Intact

- As widely expected the RBNZ left rates on hold at the July policy meeting.

- The central bank considered cutting rates, largely due to concerns around faltering economic momentum. However, with near term inflation pressures expected to be firmer, the case to hold presented a more compelling argument.

- The central bank maintained an easing bias, subject to medium term inflation pressures subsiding.

- Note Q2 CPI data prints on July 21.

- See the full review here:

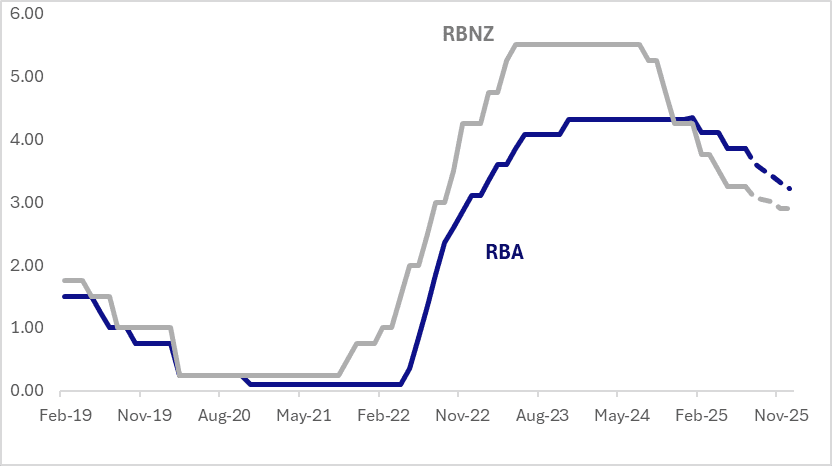

STIR: Expected YE-2025 AU-NZ Policy Rate Differential Widens On The Week

RBNZ dated OIS pricing is little changed across meetings today and versus yesterday’s pre-RBNZ levels.

- 18bps of easing is priced for the August meeting, with a cumulative 33bps by November 2025.

- In contrast, Australian rates are sharply higher on the week following Tuesday’s surprise ’no-change’ decision from the RBA.

- As a result, the expected year-end AU-NZ policy rate differential, currently +60bps, has increased by 20–25bps since late June and stands at +31bps.

Figure 1: AU-NZ Official Rates Vs. End-2025 Expectations

Source: Bloomberg Finance LP / MNI

FOREX: Asia FX Wrap - USD Flat In A Quiet Session After Drifting Lower Early

The BBDXY has had a range of 1194.34 - 1196.30 in the Asia-Pac session, it is currently trading around 1195. The USD drifted lower in early trading but has since bounced back in a quiet Asia-Pac session, -0.08%. "China Likely to Ramp Up Fiscal Support for Economy in 2H: Paper. China’s fiscal policy is expected to both “accelerate” and “expand” in the second half of the year, Shanghai Securities News reports, citing industry insiders." BBG

- EUR/USD - Asian range 1.1715 - 1.1750, Asia is currently trading 1.1735. The pair has seen solid demand again just below the 1.1700 area allowing it to bounce in our session. The price is still starting to look a little stretched in the short term and is vulnerable to any correction in the USD, first support is back towards 1.1600 then more importantly the 1.1450 area.

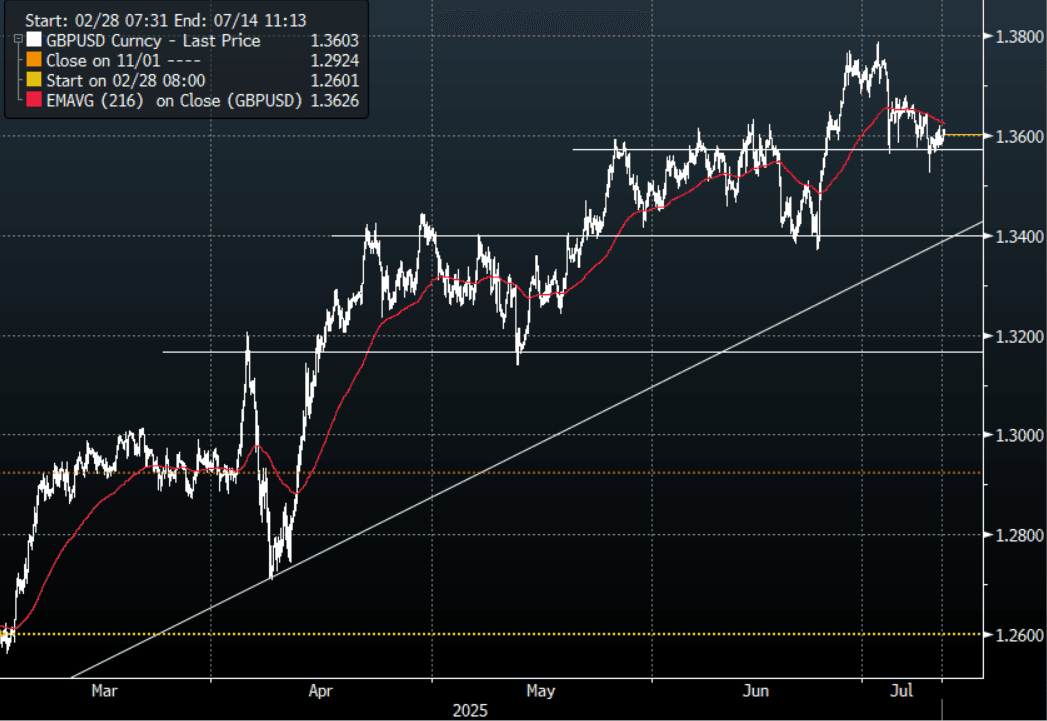

- GBP/USD - Asian range 1.3584 - 1.3613, Asia is currently dealing around 1.3605. Decent support seen around the 1.3580 area in a quiet session. Price has rejected the move higher but the USD would need to gain momentum higher for GBP/USD to extend lower in the short-term. First support around 1.3500 and then more importantly the 1.3350/1.3400 area.

- USD/CNH - Asian range 7.1782 - 7.1834, the USD/CNY fix printed 7.1510, Asia is currently dealing around 7.1820. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX -0.25%, Gold $3317, US 10-Year 4.334%, BBDXY 1195, Crude oil $68.48

- Data/Events : Germany CPI, Italy Industrial Production,

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

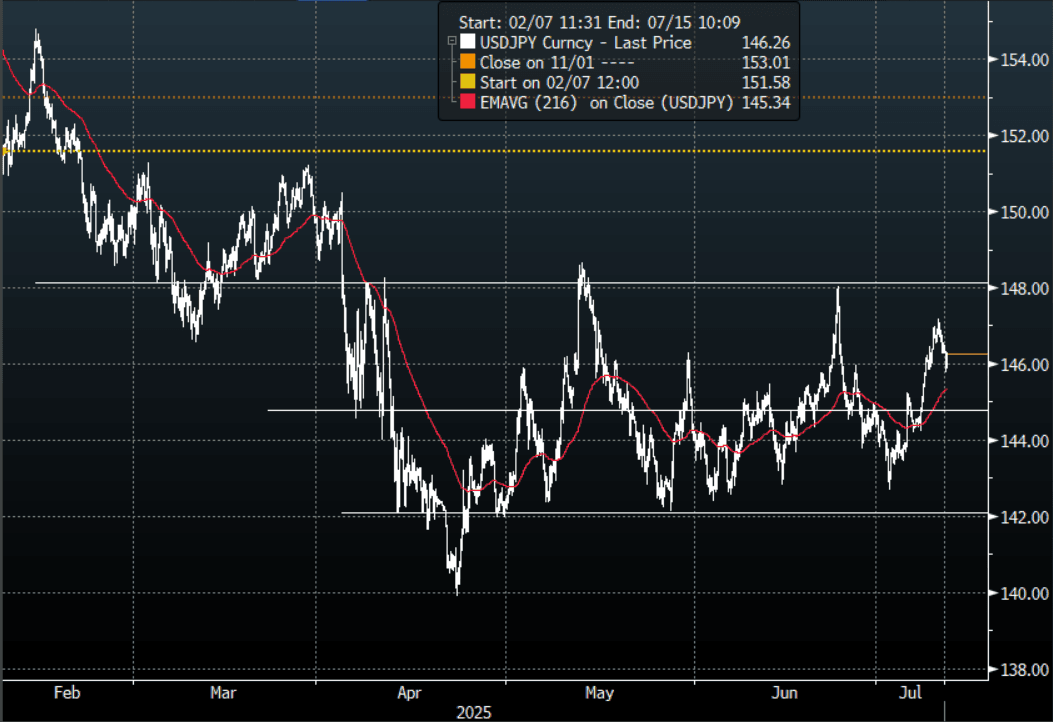

JPY: USD/JPY - Sees Sellers Into the Fix But Good Bids Emerge Below 146.00

The Asia-Pac USD/JPY range has been 145.76 - 146.38, Asia is currently trading around 146.25, -0.06%. The pair fell away pretty easily in early trading down 0.40% at one point but found bids again towards 145.75 and has since clawed back most of its early losses . USD/JPY finally topped out above 147.00 overnight after moving almost 400 points in 5 days, getting relief from a move lower in US yields. The USD/JPY relentless march higher has been pretty telling, challenging a market positioned the wrong way. Dips back towards 144.50/145.00 should now find support first up.

- (MT Newswires) via BBG: “The Bank of Japan (BOJ) will likely delay another interest rate hike until at least next March to assess potential economic damage from US tariffs, Reuters reported Wednesday, citing former BOJ policymaker Makoto Sakurai.”

- JGBS AUCTION Mixed Demand Metrics For 20Y Auction: The 20-year JGB auction delivered mixed results across key metrics. The low price underperformed dealer forecasts, which were set at 100.10 according to a Bloomberg poll. However, the cover ratio increased to 3.1462x from 3.1070x in the previous auction and the auction tail shortened to 0.18 from 0.28.

- JAPAN DATA PPI Slightly Below Forecasts, Import Prices Down Sharply Y/Y.

- USD/JPY has lost all downside momentum for now and is back in its wider 142.00 - 148.00 range. The Market is long JPY and should the USD manage to continue to correct higher the risk is a move back to the top end of the range to further challenge the conviction of the shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.00($832m).Upcoming Close Strikes : 143.50($960m July 15).

Fig 1 : USD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

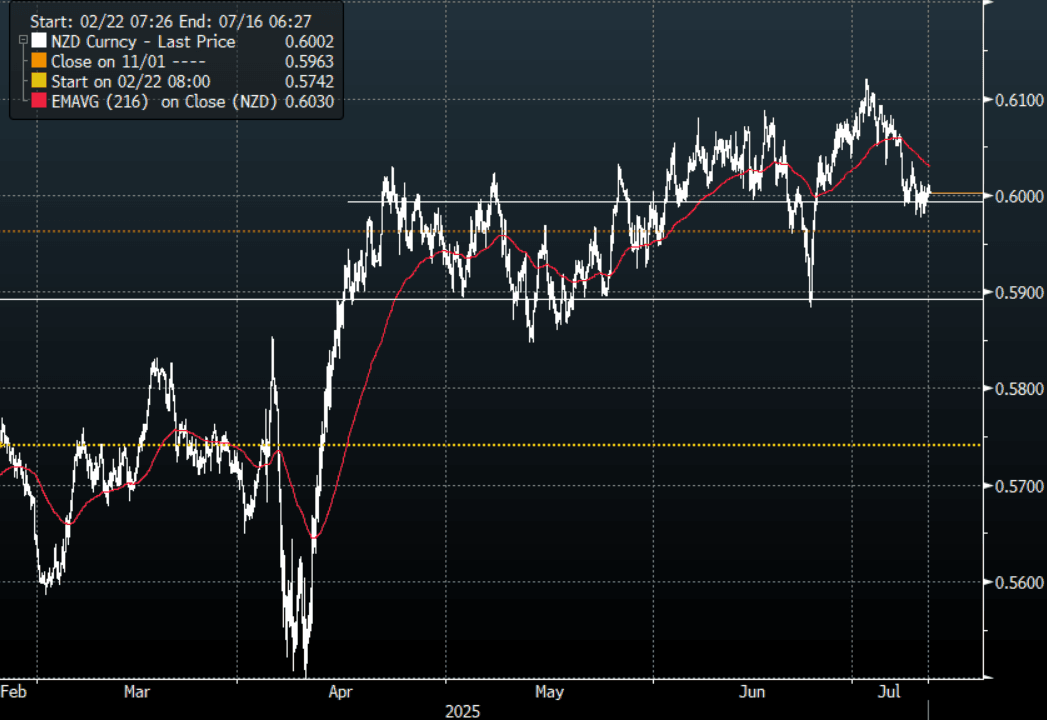

NZD: Asia Wrap - NZD/USD Holding Above 0.6000 Support For Now

The NZD/USD had a range of 0.5997 - 0.6012 in the Asia-Pac session, going into the London open trading around 0.6005, +0.05%. The pair has edged slightly higher in a very quiet session. If there is a deeper correction in risk and the USD can squeeze higher then the risk to the NZD is a move back towards the 0.5850/0.5900 area, but while the support just below 0.6000 continues to hold the bulls will be looking for a base from which to extend higher.

- NEW ZEALAND, JAPAN WORKING ON DEFENCE LOGISTICS PACT - BBG

- RBNZ MNI RBNZ Review-July 2025: On Hold, Easing Bias Still Intact: As widely expected the RBNZ left rates on hold at the July policy meeting.

- The central bank considered cutting rates, largely due to concerns around faltering economic momentum. However, with near term inflation pressures expected to be firmer, the case to hold presented a more compelling argument.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6000(NZD517m), 0.6025(NZD373m) . Upcoming Close Strikes : none.

- AUD/NZD range for the session has been 1.0877 - 1.0903, currently trading 1.0895. The cross has broken out of its recent range and focus will now turn to the more pivotal 1.0900/50 area. The RBNZ yesterday was unable to give it another nudge.

Fig 1: NZD/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

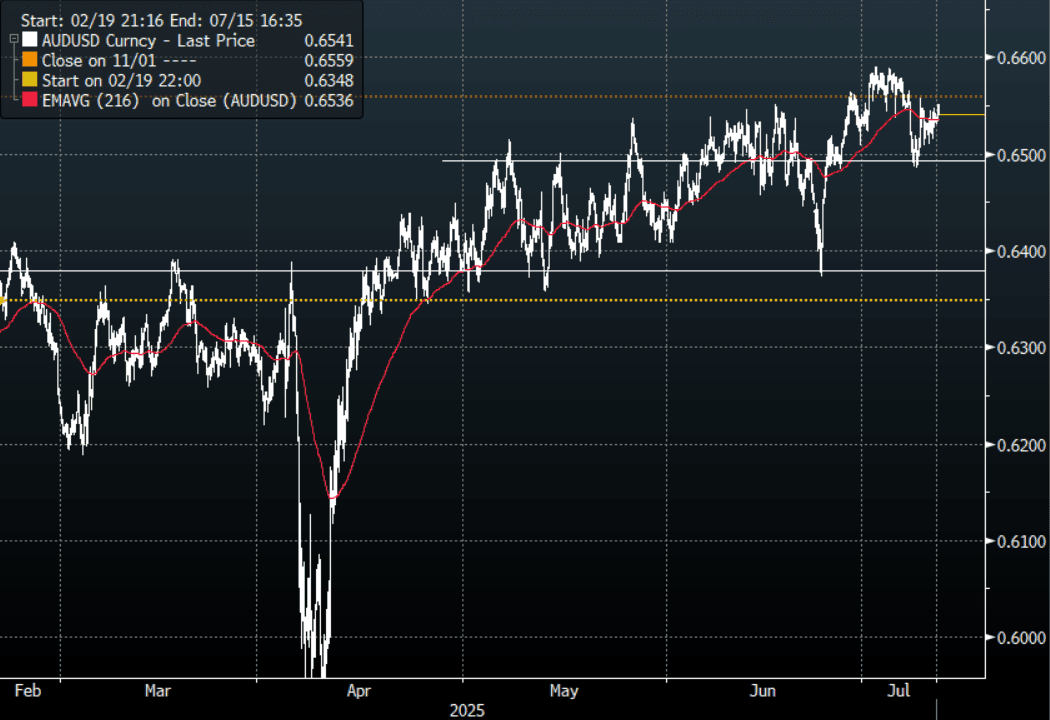

AUD/USD - Drifts Higher In A Quiet Session

The AUD/USD has had a range of 0.6530 - 0.6551 in the Asia- Pac session, it is currently trading around 0.6540, +0.10%. The pair has traded a little higher in a quiet session. The AUD needs to hold above its 0.6480/0.6500 support as a sustained move below there would see a deeper correction back to 0.6350/0.6400. While above this support though the focus will be on trying to build a base from which to potentially extend higher.

- (Bloomberg) -- Australian Treasurer Jim Chalmers and the Reserve Bank’s interest-rate setting board have agreed that members will conduct at least one speech or public engagement a year, as well as publishing unattributed votes.

- “At the end of the day, however, the US isn’t the main game for Australian exports — the bigger threat to the economy from tariffs stems from the impacts on China and Japan, and on consumer and business confidence.” - BBG

- The AUD/USD continues to hold above its support around 0.6500, looks like it's back to the 0.6500 - 0.6600 range and it should now take its cues from the USD. Watching to see if the support continues to hold as a move through there signals a deeper correction.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD598m), 0.6600(AUD 634m), 0.6650(AUD 857m). Upcoming Close Strikes : 0.6560(AUD631m July 15), 0.6650(AUD599m July 11).

- AUD/JPY - Today's range 95.40 - 95.76, it is trading currently around 95.70, +0.10%. The pair failed to extend on its break above 96.00, even with the market positioned both short AUD and long JPY. First support seen back towards 94.00/94.50 with risk moving higher this pair should have tailwinds to test higher again at some point.

Fig 1: AUD/USD spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Mixed Trends, Japan Weaker, South Korea & Taiwan Firmer

Asia equity markets are mixed, with aggregate moves less than 1% across the region at this stage. Japan weakness is a standout, while South Korean markets continue to rally strongly. US equity futures are down a touch, Eminis last off around 0.25%. This follows solid cash gains in Wednesday trade (led by the Nasdaq). Trump's 50% tariff threat against Brazil, along with confirmation that a 50% tariff on copper will come into effect from August 1 has likely weighed on sentiment.

- Japan's Topix was last off around 0.70%. Negative factors cited were tariff concerns, along with upcoming upper house elections (to be held July 20). Both the Topix and Nikkei 225 have struggled for upside momentum since the start of the month. Offshore investors have remained buyers of local stocks, per weekly flow data. On the data front, we had slightly weaker than forecast PPI figures.

- The Kospi has continued to rally, last up close to 1% and putting the index at fresh cycle highs. We aren't too far from the 3200 levels. The BOK held rates steady earlier, but maintained an easing bias. Financial stability concerns, particularly in the property market is the main factor inhibiting easing in the near term.

- The Taiex is up around 0.50%, amid a positive tech mood. Bellwether Nvidia continues to rally in the US, suggesting a firm AI-related backdrop.

- Hong Kong markets are little changed, while the CSI 300 in China is trying to establish a move above 4000.

- In SEA, trends are mixed. Indonesian stocks are up around 0.80% at this stage, while other markets are mixed.

- In Australia, the ASX 200 is up +0.70%.

OIL: Quiet Session Sees Consolidation

The Asia-Pac range for the CLQ5 contract was $68.04 - $68.41, it is trading around $68.37 as we head into the London session. Oil does not appear to have a firm trend in place with the weakness experienced seemingly done for now.

- (Bloomberg) -- “Oil steadied as traders weighed a large increase in US crude stockpiles and a wave of new tariff rates from President Donald Trump.”

- “US inventories rose by about 7.1 million barrels last week, the biggest build since January, according to official data.”

- Brent front-month futures trade around $70.22 a barrel on the ICE Futures Europe exchange heading into the London session.

GOLD: Steady After FOMC Minutes Offered Up Little New

Gold is 0.1% higher in today’s Asia-Pac session, after edging 0.3% higher yesterday.

- Little new from the June FOMC minutes, with members signalling a July hold while keeping futures policy options open. The June meeting minutes reflected a committee that was leaning slightly more hawkish than it had earlier in the year, although probably no more than should have been expected.

- The Dot Plot released at the meeting already captured most of the story: a divided Committee retains its overall easing bias but needs varying degrees of certainty before supporting a resumption of the easing cycle.

- Lower rates are typically positive for gold, which doesn’t pay interest.

- MNI’s technicals team noted that recent weakness in gold resulted in a breach of the 50-day EMA, and a trendline drawn from the Dec 30 ‘24 low and connected to the Feb 28 low. A clear break of both trend tools would signal scope for a deeper correction, and open $3,245.5, the May 29 low.

- However, the recovery from the Jun 30 low also highlights a possible false trendline break. A resumption of gains would refocus attention on $3,451.3, the Jun 16 high.

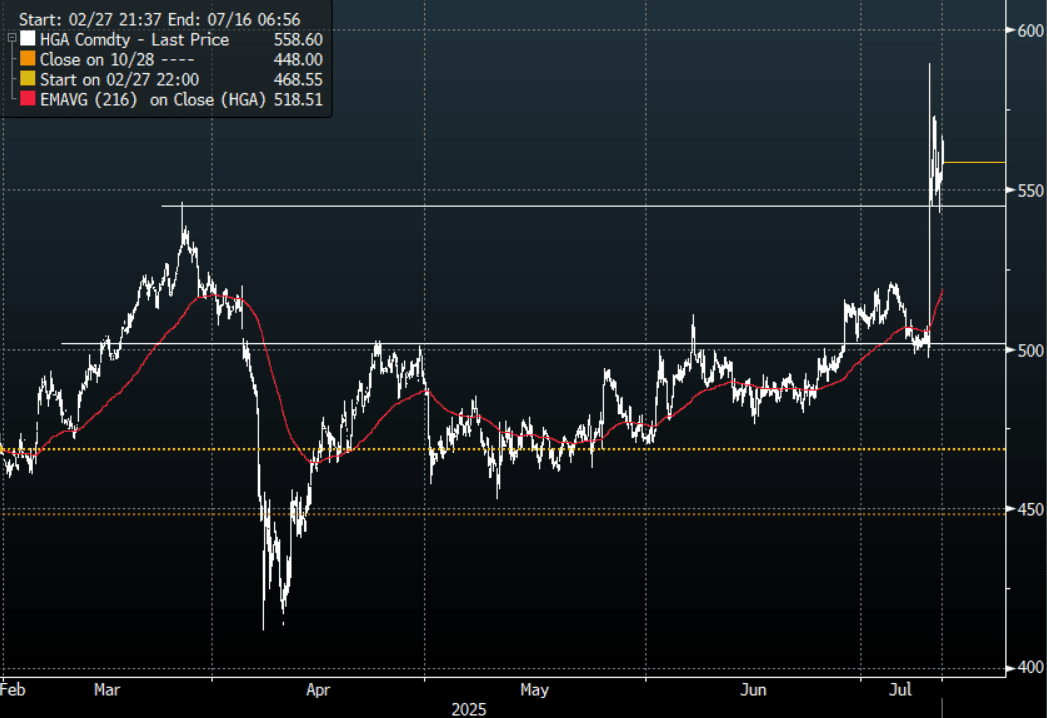

METALS: Copper Gets A Nudge Higher As Trump Confirms 50% Tariff

The range overnight for the HGU5 contract was 542.50 - 573.05, Asia is currently trading around 562, +2.5%. President Trump has confirmed his plans this morning to implement a 50% levy on Copper, effective August 1. “President Donald Trump said the US would begin levying a 50% tariff on copper imports from Aug. 1, confirming a move that will batter producers of everything from automobiles to homes and appliances who rely on the industrial metal.” - BBG

- The LME cash market closed overnight around 9652.00.

- (Bloomberg) - “Copper prices were steady Tuesday as a jump in inventories signaled that a squeeze on the London Metal Exchange might be easing. Copper stockpiles rose by the most since February on the LME, boosted by deliveries into South Korean ports.”

- “Copper traders are looking to shift deliveries into Hawaii and Puerto Rico to cut shipment times due to Donald Trump's plan for 50% tariffs.” - BBG

Fig 1 : Copper(HGN5) Hourly Chart

Source: MNI - Market News/Bloomberg

BOK: On Hold, Retain Easing Bias, Watching Financial Stability

As widely expected, the BoK left policy rates unchanged at 2.50%. The accompanying BOK statement noted the central bank will adjust the timing and pace of any further rate cuts, with a host of factors in play, around growth, inflation and financial stability.

- On inflation, the BoK appears fairly comfortable, albeit recognizing uncertainties surrounding the outlook (from both international and domestic drivers). It expects headline and core inflation pressures to remain fairly close to the 2% target.

- On growth, more uncertainty faces the outlook. On domestic conditions, the BoK noted that consumption is likely to improve with political uncertainty now in the rear-view mirror, while the government's recently passed extra budget should also be a positive. It noted though that construction activity remained weak. Export growth is expected to slow in H2 due to the tariff impact, although there remains significant uncertainty regarding the outlook, given on-going trade negotiations. Overall, the domestic economic is expected to see a low growth rate for some time.

- Financial stability also remains an important watch point. The central bank noted: "Regarding financial stability, as risks associated with the housing market in Seoul and its surrounding areas and with household debt have increased, it is necessary to assess the effect of the macroprudential policies while

remaining cautious about the possibility of heightened volatility in the foreign exchange market." - If we see signs of macroprudential efforts working in terms of cooling the Seoul housing market, along with curbing household debt growth, we could see the central bank turn more dovish and cut again to support the economy.

BOK: Governor Rhee- Majority Of Board Still Favor Lower Rates, Local Yields Down

Governor Rhee's press conference emphasized that financial stability is the near term focus point for the central bank, but further easing was still preferred by the majority of the board.

- The decision to hold rates steady was unanimous. However, 4 out of 6 board members saw scope to lower rates in the next 3 months, while the other 2 board members would like to see rates on hold over this period. They cited financial stability concerns as a driving a steadier outlook, while Governor Rhee noted that those members open to a cut would be monitoring data over this period.

- Rhee stressed that concerns over financial imbalances have increased greatly. Still, Rhee stated that an easing bias needs to be maintained.

- No doubt the BOK will assess how borrowing/house price trends (particularly in Seoul), before deciding on whether to ease again. This is clearly the bias though, with domestic growth still expected to slow, while inflation is seen as stable around 2%.

- FX market reaction has been quite limited, with USD/KRW relatively steady so far today, last around 1373.5 (down a touch from end Wednesday levels). The Kospi is firmer, up close to 0.90% to fresh cycle highs. Positive tech sentiment from US trade is likely helping on this front.

- Government bond yields are down across the curve, with the 10yr back to 2.82%, off 3bps. The 1y1y forward rate is down around 4bps to 2.325%, close to recent lows. The 1yr implied rate is around 2.30%, down slightly from pre-decision levels.

ASIA FX: CNH, KRW Little Changed, USD/TWD Firmer On Potential Seasonal Outflows

In North East Asia FX markets, trends have been fairly steady for CNH and KRW (with the BOK holding the policy rate steady). USD/TWD has bucked this trend and pushed higher (potentially on dividend related outflows). USD/HKD spot remains at the top of the peg band.

- USD/CNH spot was last near 7.1815, little changed for the session. We had a brief dip under 7.1800 as broader USD trends were softer but there was no follow through. The USD/CNY fixing move backed down close to recent lows. This should help cap USD/CNH upside. Local equity sentiment remains positive, with the CSI 300 trying to build a base above 4000.

- Spot USD/KRW was last near 1373, down a touch from end Wednesday levels in the pair. We remain close to recent highs near 1380. The BoK held rates as expected but maintained an easing bias. The central bank is worried around financial imbalances particularly in relation to household borrowing/house prices in Seoul. Stability on this front might be needed before the central bank eases again to support domestic growth. The Kospi continues to rally, up a further 1.3% today to fresh cycle highs. This isn't helping KRW sentiment much though.

- USD/TWD has pushed higher, last above 29.20, the pair up around 0.25% so far today. Sell-side analysts are noting the July/August dividend outflow season to offshore investors as a potential TWD headwind. Note that for USD/TWD the 20-day EMA is around 29.33. We haven't been above this resistance point since early April (outside of a brief spike in early July).

- Spot USD/HKD holds close to 7.8500.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 10/07/2025 | 0600/0800 | *** | CPI Norway | |

| 10/07/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/07/2025 | 0600/0800 | *** | HICP (f) | |

| 10/07/2025 | 0700/0900 | ECB Cipollone Digital Euro Lecture | ||

| 10/07/2025 | 0800/1000 | * | Industrial Production | |

| 10/07/2025 | - | *** | Money Supply | |

| 10/07/2025 | - | *** | New Loans | |

| 10/07/2025 | - | *** | Social Financing | |

| 10/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 10/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 10/07/2025 | 1400/1000 | St. Louis Fed's Alberto Musalem | ||

| 10/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 10/07/2025 | 1500/1600 | BOE Breeden On Climate Change | ||

| 10/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 10/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 10/07/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 10/07/2025 | 1715/1315 | Fed Governor Christopher Waller | ||

| 10/07/2025 | 1830/1430 | Fed's Mary Daly at MNI | ||

| 11/07/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 11/07/2025 | 0600/0700 | ** | Trade Balance | |

| 11/07/2025 | 0600/0700 | ** | Index of Services | |

| 11/07/2025 | 0600/0700 | ** | Index of Production | |

| 11/07/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 11/07/2025 | 0645/0845 | *** | HICP (f) | |

| 11/07/2025 | 1130/1330 | ECB Cipollone At Ukraine Recovery Conference | ||

| 11/07/2025 | 1230/0830 | *** | Labour Force Survey | |

| 11/07/2025 | 1230/0830 | * | Building Permits |