US TSYS: Front-End Yields Edge Higher In Quiet Session

Jul-10 04:14

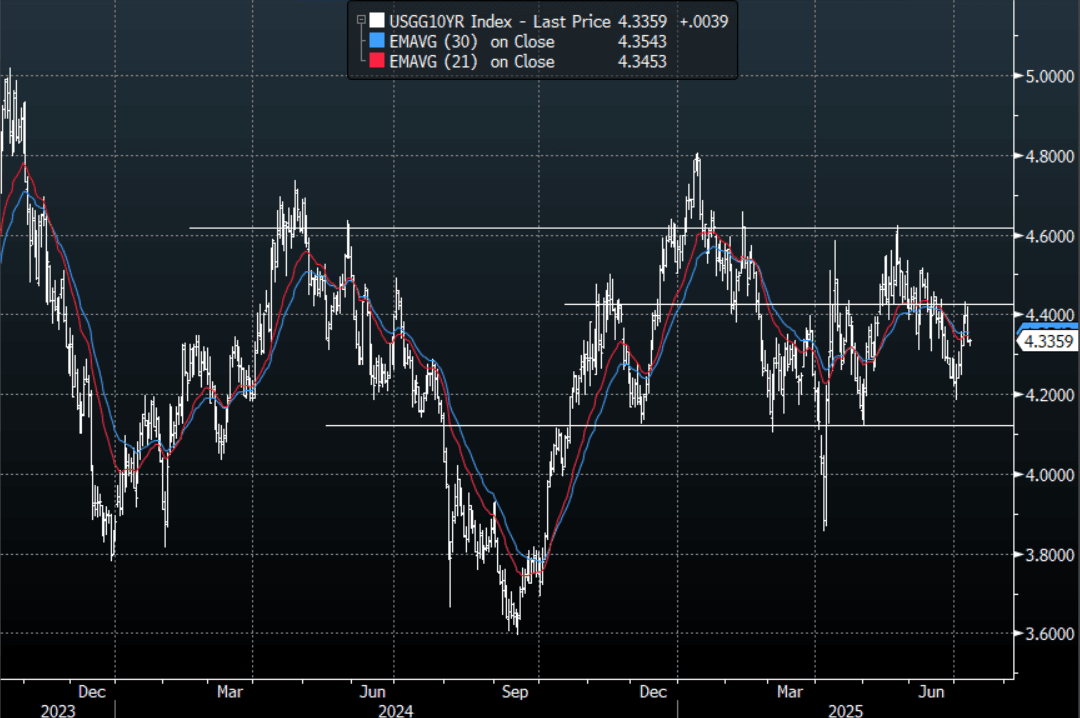

The TYU5 range has been 111-09 to 111-13+ during the Asia-Pacific session. It last changed hands at 111-10, up 0-01+ from the previous close.

- The US 2-year yield has edged higher trading around 3.85%, up 0.01 from its close.

- The US 10-year yield has edged higher trading around 4.335%, up slightly from its close.

- The 10-year yield has topped out just above the 4.40% area, giving the bulls some reprieve. No clear long-term direction though has seen the 10-year chop around in a wider 4.10% - 4.60% range for most of the year, with the 4.40% area being the pivot. A sustained close back above the 4.45% area could see more of the longs pared back but while this area holds they should be happy to stick with their position looking for a move back to the lower end of the range.

- Nick Timiraos on X: ”The next few months of inflation data will offer a key test of competing theories about whether tariffs will prove inflationary and animate potential Fed divisions over how to manage any costs if forecasts are wrong—in either direction.”

- (Bloomberg) -- “Investors will monitor ultra-long bond auctions in Japan and the US later Thursday to gauge concerns of how fiscal discipline may impact demand.”

- "JAPAN 20-YEAR BOND BID-COVER RATIO 3.15 VS 12-MONTH AVG 3.29" - BBG

- Data/Events: Initial Jobless Claims, US To Sell $22 Bln 30-year Bond.

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Asia Wrap - A Quiet Session, Focus On Upcoming CPI

Jun-10 04:10

The TYU5 range has been 110-02 to 110-07 during the Asia-Pacific session. It last changed hands at 110-04, down 0-01 from the previous close.

- The US 2-year yield is unchanged, dealing around 4.0075%.

- The US 10-year yield has edged higher, trading around 4.48%, up 0.1 from its close.

- Bloomberg - “Negotiations in London wrapped on Monday with an extension of the talks into a second day, offering little lifeline to the struggling greenback. US Commerce Secretary Howard Lutnick called the discussions “fruitful,” while Treasury Secretary Scott Bessent described it as a “good meeting.”

- Bloomberg - “Senator Ted Cruz has proposed eliminating the interest paid to banks that deposit cash at the Federal Reserve, which could save the government around $1 trillion over a decade.”

- “JPMorgan strategists warn that this move could significantly impact banks' profitability, liquidity management strategies, and short-term interest rates, and risk the Fed losing control of money market rates.”

- The 10-year yield held its support around the 4.35% area last week. While this level holds focus will remain on potentially extending higher, CPI tomorrow will be a very important input.

- Data/Events: NFIB Small Business Optimism

STIR: RBA Dated OIS 2026 Pricing Remains 25bps Softer Than Pre-RBA Levels

Jun-10 03:54

RBA-dated OIS pricing is mildly firmer across meetings today.

- Nevertheless, pricing is 12-24bps softer than pre-RBA (May Meeting) levels.

- A 25bp rate cut in July is given an 82% probability, with a cumulative 73bps of easing priced by year-end.

Figure 1: RBA-Dated OIS – Current Vs. Pre-RBA Level

Source: Bloomberg Finance LP / MNI

CHINA: Bond Futures Flat after OMO Withdraws Liquidity

Jun-10 03:46

- Bond futures are steady in the morning trading session, following the Central Bank's withdrawal of liquidity during the OMO.

- The 10YR future is flat at 108.97 and remains above all major moving averages. The nearest being the 20-day EMA at 108.82

- The 2YR future is flat at 102.44, sitting just above the 20-day EMA of 102.43

- The CBG 10YR is at 1.69%