MNI EUROPEAN MARKETS ANALYSIS: China Services PMI Eases

- US equity futures struggled for upside today, perhaps waiting for further positive announcements on trade deals before rallying further. The USD tried to bounce but follow through was limited. USD/TWD did stabilize after the recent sharp sell-off.

- On the data front, Australian household spending was weaker than expected, while the China services PMI (Caixin) also printed below expectations.

- Later US March trade data are released as well as Canadian trade & PMI and European services/composite PMIs for April.

MARKETS

US TSYS: Asia Wrap - Futures Edge Lower

TYM5 has traded lower within a range of 110-30 to 111-03 during the Asia-Pacific session. It last changed hands at 110-30, down 0-03 from the previous close.

- Futures are trading lower in Asia as China returns from holidays, China’s April's PMI services unexpectedly dipped in April in signs that the US tariff war is hurting.

- The CAIXIN PMI services had printed above 51 for six successive months and market expectations were for a continuation of this theme and a print of +51.8.

- April's result of +50.7 is the lowest since September and could be an early warning sign that the economy is slowing quicker than first thought.

- Risk in Asia has traded on the backfoot for most of our session following on from the poor close in the US.

- No cash market today with a holiday in Japan.

- The 10-year Yield range seems to be 4.10% - 4.45%, price has moved above the 4.30% pivot and with more supply to come this week a push back to 4.45% is possible before the buyers come in.

- Data/Events : US Trade balance

AUSSIE BONDS: Cheaper But Subdued Trading With Japan Out, Apr-37 Supply Tomorrow

ACGBs (YM -3.0 & XM -6.0) are weaker and near Sydney session cheaps.

- Outside of the building approvals and household spending, there hasn't been much by way of domestic drivers to flag.

- Q1 HH spending volume data showed no growth on the quarter, in line with retail sales, to be up only 0.9% y/y after +1.6% q/q & 2.3% y/y in Q4, consistent with the view that the RBA is likely to ease 25bp on May 20. Private consumption in the national accounts is likely to be close to flat in Q1 when it is released on June 4.

- Cash US tsys dealings in today's Asia-Pac session with Japan out. TYM5 is slightly cheaper.

- Cash ACGBs are 3-6bps cheaper, with the 3/10 curve steeper.

- The bills strip has bear-steepened, with pricing flat to -5 across contracts.

- RBA-dated OIS pricing is flat to 3bps firmer across meetings today. A 50bp rate cut in May is given a 3% probability, with a cumulative 103bps of easing priced by year-end.

- Tomorrow, the local calendar will see Foreign Reserves data.

- The AOFM plans to sell A$1000mn of the 3.75% 21 April 2037 bond tomorrow and A$700mn of the 2.75% 21 November 2029 bond on Friday.

AUSTRALIA DATA: Q1 Spending Volumes Flat, March Saw Cyclone Impact

March household spending was weaker-than-expected falling 0.3% m/m to be up 3.5% y/y after an upwardly-revised +0.3% m/m & 3.6% y/y. Q1 volume data was also released, which is now seasonally adjusted. It showed no growth on the quarter, in line with retail sales, to be up only 0.9% y/y after +1.6% q/q & 2.3% y/y in Q4, consistent with the view that the RBA is likely to ease 25bp on May 20. Private consumption in the national accounts is likely to be close to flat in Q1 when it is released on June 4.

Australia household consumption volumes q/q% sa

- The decline in March was impacted by Cyclone Alfred with it falling 1.3% m/m in Queensland but food spending there rose 2.9% m/m.

- The March weakness was driven particularly by services spending which fell 0.7% m/m but is still up 5.1% y/y. Goods rose 0.1% m/m to be up 2.3% y/y.

- Non-discretionary expenditure continues to exceed discretionary as cost-of-living pressures persist. The former was flat in March to be up 4.4% y/y, while the latter fell 0.4% m/m to be steady at 3.0% y/y.

- The softness in Q1 volumes was driven by alcohol & tobacco spending (-5.9% q/q & -16.5% y/y) and hotels & restaurants (-1.2% q/q & -0.7% y/y). Recreation & culture posted another solid quarterly rate.

Australia consumption discretionary vs non-discretionary y/y%

Source: MNI - Market News/ABS

BONDS: NZGBS: Closed With A Bear-Steepener, Q1 Employment Report Tomorrow

NZGBs closed showing a bear-steepener, with benchmark yields finishing 1-4bps higher but slightly off the session’s worst levels. The NZ-AU 10-year yield differential was unchanged at +21bps. There were no cash dealings in US tsys in today's Asia-Pac session with Japan out. TYM5 is slightly cheaper.

- NZ’s commodity export prices were unchanged from a month earlier in April.

- Swap rates closed flat to 4bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed little changed across meetings. 26bps of easing is priced for May, with a cumulative 76bps by November 2025.

- Q1 labour market data are released on Wednesday, and forecasts are in a narrow range across the major components. Bloomberg consensus expects the unemployment rate to rise 0.2pp to 5.3%, above the RBNZ’s 5.2% and would be the highest since Q4 2016, and employment to rise 0.1% q/q, signalling a stabilisation in the labour market.

- Private wages are expected to rise 0.5% q/q, slightly slower than Q4. Outcomes close to these are unlikely to alter the RBNZ’s probable 25bp rate cut on May 28.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.25% May-36 bond and NZ$50mn of the 2.75% May-51 bond.

NEW ZEALAND: Higher Unemployment Rate, Could Be Signs Of Stabilisation

Q1 labour market data are released on Wednesday and forecasts are in a narrow range across the major components. Bloomberg consensus expects the unemployment rate to rise 0.2pp to 5.3%, above the RBNZ’s 5.2% and would be the highest since Q4 2016, and employment to rise 0.1% q/q, signalling a stabilisation in the labour market. Private wages are expected to rise 0.5% q/q, slightly slower than Q4. Outcomes close to these are unlikely to alter the RBNZ’s probable 25bp rate cut on May 28.

- The RBNZ forecast flat Q1 employment in its February staff forecasts resulting in the annual rate down 0.6% y/y. Consensus is slightly higher projecting a 0.1% q/q increase (forecast range 0.0% to +0.2% q/q) with the annual rate down 0.5%. Of the major local banks ANZ and Kiwibank are in line with consensus, while ASB and BNZ expect a flat quarterly outcome.

- Unemployment rate expectations are between 5% and 5.3%. ANZ, BNZ, Kiwibank and Westpac are all at consensus’ 5.3%, while ASB is slightly lower at 5.2%. A rise is expected due to an increase in the labour supply.

- Private wages rose 0.6% q/q in Q4 and forecasts for Q1 range from 0.4% to 0.6%. The RBNZ expected 0.6% again in February. ASB, ANZ and BNZ are in line with consensus at 0.5%, while Westpac is below at 0.4% and Kiwibank above at 0.6%. Lower inflation should mean less pressure on wage growth as well as more spare capacity in the labour market.

FOREX: G10 Wrap - USD Struggling To Catch A Bid

The BBDXY has had an Asian range of 1221.53 - 1225.17, Asia is currently trading around 1222. USD/Asia has stabilized with China back from holidays. Bloomberg - “The ECB is poised to continue cutting rates, according to Yannis Stournaras. The Greek central bank chief expects a clear slowdown of inflation in Europe due to US tariffs, and believes the continent will respond selectively to any US measures.” The lower China services PMI saw risk trade heavy in our session providing a bid to safe havens like the JPY.

- EUR/USD - Asian range 1.1280 - 1.1320, Asia is currently trading 1.1315. Intra-day support is around the 1.1250 area, should this area not hold demand should remerge on dips back to 1.1100.

- GBP/USD - Asian range 1.3260 - 1.3300, Asia is currently dealing around 1.3295. Intra-day support is around the 1.3250 area, then the pivotal 1.30/31 support is next.

- USD/JPY - Asian range 143.56 - 144.28, has drifted sideways for most of the Asia session. Look for some support initially back towards 143.00, we would probably need another catalyst to test below that again.

- USD/CNH - Asian range 7.2002 - 7.2352, the USD/CNY fix printed 7.2008. The capitulation in USD/Asia has taken a breather today, rallies should now find sellers who could not get out because of the pace of the move. First resistance 7.2600 Area and then back towards 7.3000.

- Cross asset : SPX -0.2%, Gold $3360, US TYM5 110-30, BBDXY 1221, Crude oil $58.02.

- Data/Events : SW PMI’s, FR Industrial Production & PMI’s, Spain Unemployment, Spain PMI’s, Italy PMI’s, Germ PMI’s, EU PPI, US Trade Balance

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg

FOREX: Antipodean Wrap - AUD & NZD Rise Falters As US Stocks Stall

The Asian session started off on the back foot with US stocks closing poorly even after a better than expected ISM Services PMI overnight. The lower China services PMI saw Asia remain under pressure providing headwinds for both the AUD and NZD. MNI - AU Building approvals in March were significantly weaker than expected falling 8.8% m/m with the more stable private houses component down 4.5% m/m. Bloomberg - “ANZ is forecasting a 0.2pp rise in the NZ Q1 unemployment rate to 5.3%, which would be the highest since Q4 2016, as growth in labour supply exceeds labour demand. It doesn’t think the data or the upcoming budget on May 22 will change the RBNZ monetary policy outlook and that the updated forecasts for the May 28 meeting will be more important, especially given the global environment.”

- AUD/USD - Asian range 0.6443 - 0.6470, the AUD is currently dealing around 0.6455. The AUD move higher seems to be running out of steam as risk runs into resistance. Support should be seen back towards 0.6400, a break below 0.6300 needed to reverse direction.

- AUD/JPY - Asian range 92.76 - 93.05, price goes into London trading around 92.85. Price is stalling towards the resistance seen around 94.00 as risk struggles in Asia. Support seen initially back towards the 92.00 area.

- NZDUSD - Asian range 0.5944 - 0.5973, going into London trading around 0.5965. The NZD continues to hold up well and is consolidating within a 0.5875/0.6025 range. On the day dips back to 0.5900 should continue to find support.

- AUD/NZD - Asian range 1.0819 - 1.0849, the Asian session is currently trading 1.0825. Sellers have returned back towards the 1.0850 area.

Fig 1 : AUD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: China Shares Up Post Holidays.

In their first trading day back post the five day Labour Day holidays, China’s major bourses all rose as expectations that the US trade war could ease. The equity gains are after Treasury Secretary Scott Bessent’s said the US could see some “substantial progress in the coming weeks” in trade talks with China and President Donald Trump‘s suggesting that said he is willing to lower tariffs on China at some point.

- China’s Shenzhen Composite lead the way as the index rose +1.90% whilst Shanghai and CSI 300 were up +0.95%. The Hang Seng was strong today also rising +0.65%.

- The FTSE Malay KLCI fell -0.33% today following on from yesterday’s fall of -0.19% leaving the index down over 6% year to date.

- The Jakarta Composites good run continues rising +0.95% following yesterday's gains of -0.19% to leave it down just -2.5% year to date

- The FTSE Straits Times rose a modest +% whilst the PSEi in the Philippines climbed +0.75%.

- India’s NIFTY 50 is down -0.25% in the morning trade following on from yesterday’s rise of +0.47% on trade deal optimism. Year to date the NIFTY 50 is up over 3% setting it apart from its regional peers.

ASIA STOCKS: Strong Inflows Continue for Taiwan

Taiwan has experienced very strong inflows as signs of a thawing in the trade war resonate with investors.

- South Korea: Recorded outflows of -$65m as of Friday, bringing the 5-day total to +$722m. 2025 to date flows are -$12,329m. The 5-day average is +$144m, the 20-day average is -$254m and the 100-day average of -$144m.

- Taiwan: Had inflows of +$779m as of yesterday, with total inflows of +$2,397m over the past 5 days. YTD flows are negative at -$16,436. The 5-day average is +$479m, the 20-day average of +$91m and the 100-day average of -$164m.

- India: Had inflows of +$335m as of the 2nd, with total inflows of +$1,515m over the past 5 days. YTD flows are negative -$11,931m. The 5-day average is +$303m, the 20-day average of +$43m and the 100-day average of -$106m.

- Indonesia: Had inflows of +$5m as of yesterday, with total inflows of +$12m over the prior five days. YTD flows are negative -$3,050m. The 5-day average is +$2m, the 20-day average -$51m and the 100-day average -$36m

- Thailand: Recorded outflows of -$41m as of 2nd, outflows totaling -$12m over the past 5 days. YTD flows are negative at -$1,645m. The 5-day average is -$2m, the 20-day average of -$24m the 100-day average of -$19m.

- Malaysia: Recorded outflows of -$22m as of yesterday, with inflows totaling +$177m over the past 5 days. YTD flows are negative at -$2,601m. The 5-day average is +$35m, the 20-day average of -$13m and the 100-day average of -$31m.

- Philippines: Saw outflows of -$1m as of yesterday, with net inflows of +$37m over the past 5 days. YTD flows are negative at -$253m. The 5-day average is +$7m, the 20-day average of -$2m the 100-day average of -$4m.

OIL: Crude Unwinds Yesterday’s Losses On Technicals

Oil prices have recovered most of Monday’s losses today driven by technicals. Also Asia including China returned from holidays. WTI is up 1.7% to $58.07/bbl, close to the intraday high, to be down only 0.4% this week. Brent is 1.6% higher at $61.21/bbl and only down 0.1% since Friday. The USD index is off its intraday high to be up only 0.1%.

- Bloomberg is reporting that the 9-day relative strength index flashed oversold which drove today’s bounce in both WTI and Brent.

- After OPEC’s decision to increase output by over 400kbd from June following a similar rise in April, supply trends are going to remain firmly in focus. Saudi Arabia warned that there could be further rises if its members don’t stick to their quotas. Iraq and Kazakhstan have been constant overproducers.

- Later today US industry-based inventory data are released, which will give an insight into demand/supply trends there ahead of the official data on Wednesday.

- Later US March trade data are released as well as Canadian trade & PMI and European services/composite PMIs for April.

Gold’s Rally Returns with Strong Gains Today

- Gold’s overnight rally continued into the Asia trading day delivering a +0.80% gain.

- With equities strong across the region, bonds quiet and the dollar stronger against regional crosses, it was a day possibly where gold could have fallen.

- With positioning much lighter in longs than previously and money managers more neutral than they have been in over a year, the rally today looked like the re-establishment of longs given the recent sell off.

- Gold markets will be actively watching the FED this week as expectations for rate cuts diminish following the stronger than expected labour market.

- Gold opened the day at US$3,334.12 and rallied to $3,359.70 by mid afternoon.

- Bolivia’s released details of its reserves today showing that the Central Bank are another of the ever growing list of Central Banks adding to their gold reserves having purchased 4.94 tons of locally-produced gold in the first quarter of 2025.

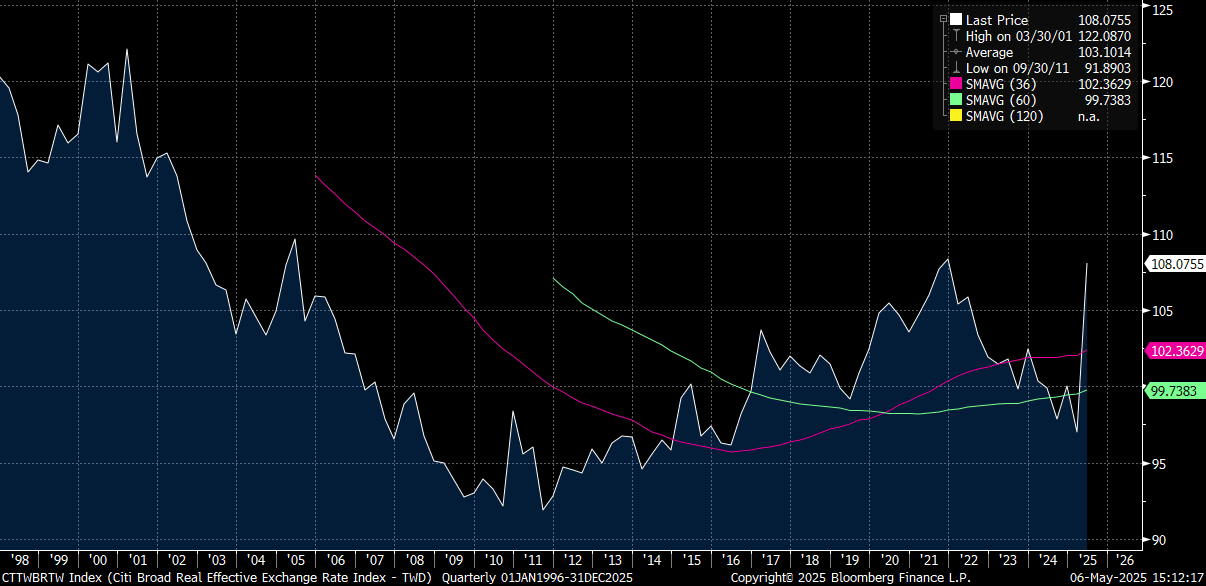

ASIA FX: USD Sell-off Pauses, TWD REER Back Close To 2021 Highs

In North East Asian markets, recent USD weakness has consolidated today. Focus remains on USD/TWD, where spot losses have stabilized above 30.00, while the 1month NDF has lost around 4% in TWD terms. USD/CNH is higher but away from the best levels. The 1 month USD/KRW NDF is higher as well, but like USD/CNH away from best levels.

- In contrast to last Friday and yesterday, USD/TWD spot has had a much quieter session. Dips just under 30.00 have been supported so far and we last tracked near 30.15/20, off 0.25% in WTD terms and close to session highs. Given the very sharp nature of the collapse in the pair over the prior two sessions, if we have more USD selling to come through from exporters/lifers etc, upticks should be sold. Equally the authorities may be mindful of further sharp gains, as exporters worry about a sharp loss of competitiveness in the near term. The Citibank TWD REER has risen quickly back close to late 2021 highs, see the chart below. The 1 month NDF was last near 29.50/55, so still with a negative basis to onshore spot, but a significantly lower gap.

- USD/CNH opened around 7.2000 but rose as the USD found some support through the session. We had a close to unchanged USD/CNY fixing, with the authorities seemingly not adding any fresh fuel to recent yuan rally. The lower than expected Caixin services PMI also reminded markets of the growth risks from US tariffs. Highs in USD/CNH were around 7.2350/55, but as the USD has lost momentum we now sit back at 7.2135/40.

- 1 month USD/KRW has risen, the pair got to highs of 1387.69, but we sit back at 1377/78 in latest dealings, around 0.35% weaker in KRW terms. Onshore markets return tomorrow, with focus likely to be on whether we can see spot levels sustain sub 1400.

Fig 1: Citi TWD REER Back Close To 2021 Highs

Source: Citi/MNI - Market News/Bloomberg

CHINA: Country Wrap: PMI Services Dip in April

- April's PMI services unexpectedly dipped in April in signs that the US tariff war is hurting. The CAIXIN PMI services had printed above 51 for six successive months and market expectations were for a continuation of this theme and a print of +51.8. April's result of +50.7 is the lowest since September and could be an early warning sign that the economy is slowing quicker than first thought. The government's official GDP growth forecast of 5% may be under threat and could bring about further policy intervention to support what looks like softening growth. The details within today's release show a modest uptick in employment from +48.6 to +49.2; yet still in contraction and prices charged relative to last month rose. (source MNI Market News)

- Hong Kong authorities sold a record HK$60.5 billion of the local dollar to defend the foreign-exchange peg as the greenback's slide threatened the currency's trading band. The intervention helped dampen Hong Kong's borrowing rates and may also help shield the economy from US tariffs, with the HKMA's sales expected to drive up its aggregate balance and provide more firepower to defend the currency. The HKMA's actions are seen as efforts to limit the currency's moves within its 7.75-7.85 per dollar trading band, with further intervention expected on the strong side of the band given the greenback weakness trend. (source HKMA via BBG)

- In their first trading day back post the five day Labour Day holidays, China's major bourses all rose as expectations that the US trade war could ease. The equity gains are after Treasury Secretary Scott Bessent's said the US could see some "substantial progress in the coming weeks" in trade talks with China and President Donald Trump's suggesting that said he is willing to lower tariffs on China at some point. China's Shenzhen Composite lead the way as the index rose +1.90% whilst Shanghai and CSI 300 were up +0.95%. The Hang Seng was strong today also rising +0.65%.

- Yuan Reference Rate at 7.2008 Per USD; Estimate 7.2465

- Bonds were very quiet today with the CGB 10YR flat at 1.63%

INDIA: Country Wrap: India Proposes Zero Auto Parts Tariffs

- India has proposed zero tariffs on steel, auto components, and pharmaceuticals up to a certain quantity of imports in its trade negotiations with the US on a reciprocal basis. The proposal was made to expedite negotiations on a bilateral trade deal expected by fall this year, with the two nations prioritizing certain sectors to strike an early deal. India has also offered to reconsider its Quality Control Orders and sign a mutual recognition agreement with the US to address Washington's concerns around non-tariff trade barriers. (source BBG)

- The Reserve Bank of India has begun unwinding its short position in the dollar forward book, after a gap of seven months, on the back of a softening dollar, while simultaneously infusing funds via open market operations (OMOs) to counter the resulting liquidity drain. Data from the central bank showed that the net short dollar position in the RBI’s forward book (up to one year) stood at $64.2 billion at the end of March. Including swaps with over one year of maturity, the book stood at $84.3 billion, down from $88.75 billion in February. (Source Business Standard)

- India's PMI Services for April was released today and the result of +58.7 points to the robustness of the services sector even in the face of the trade war. The April print was marginally down from March's +59.1 result with the employment component up to +53.9 from +52.5 and prices charged up over last month. This sees a rise in the HSBC India April Composite to +59.7 from +59.5 in March and shows that the Indian economy remains well positioned to deal with the trade war challenges. The RBI cut rats at its last meeting on April 09 to 6.00% and next meets on June 06. Market implied pricing has just -9bps of cuts priced in over the next 3 months and -61bps over the next year. (source MNI Market News)

- India's NIFTY 50 is down -0.25% in the morning trade following on from yesterday's rise of +0.47% on trade deal optimism. Year to date the NIFTY 50 is up over 3% setting it apart from its regional peers.

- India’s 10YR is weaker today rising +2.5bps in yield to be 6.35%

THAILAND: Core At Bottom Of Band As Headline Goes Negative

Core CPI inflation printed at the bottom of the Bank of Thailand’s 1-3% target band in April. It rose a stronger-than-expected 1.0% y/y from 0.9%. This measure is likely to be the focus with headline impacted by government subsidies as well as lower vegetable and global oil prices. It fell to -0.2% y/y from +0.8% y/y in March, weaker than expected. After cutting rates in both February and April, further monetary easing is likely this year.

Thailand CPI y/y%

- The Bank of Thailand (BoT) is concerned about the impact of US trade policy on Thailand, especially if there isn’t a deal to reduce the proposed 36% tariff. Also, the stand-off between China and the US could put downward pressure on Thai inflation if China reduces prices to find other markets.

- The government expects inflation to stay negative in May. BoT expects headline inflation at 0.2% to 0.5% in 2025 and was revised down due to lower oil prices and government policy.

- Energy prices were down 6.7% y/y in April after -0.9% y/y as the state subsidised fuel and global oil prices fell sharply over the last few months with WTI almost 18% lower in April. Core inflation excludes private road transport and accommodation costs and so is not impacted by these factors.

- Food prices rose 1.6% y/y in April but down from 2.35% with eggs & vegetables declining over the year helped by increased supply.

INDONESIA: Country Wrap: BI Intervening Again to Smooth Rupiah

- The central bank will remain in the markets to maintain rupiah stability to be in line with the movements of peer currencies and to prevent excessive volatility, says BI’s director of monetary and asset securities management. Interventions will be carried out in a measured way and when necessary, in the spot, DNDF, offshore NDF and govt bond market in line with market needs and dynamics (source BBG)

- Indonesia’s Danantara and French miner Eramet SA are in talks to form a partnership that would invest in a nickel plant in the Southeast Asian nation, people familiar with the matter said, in what could be the state investment fund’s first major transaction. (source BBG)

- he Jakarta Composites good run continues rising +0.95% following yesterday's gains of -0.19% to leave it down just -2.5% year to date

- Having not participated in the rally yesterday the rupiah had little to give back today and finished again flat on the day at 16,446

- Bonds were very quiet with the INDOGB up +0.5bps to 6.87%

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 06/05/2025 | 0545/0745 | ** | Unemployment | |

| 06/05/2025 | 0645/0845 | * | Industrial Production | |

| 06/05/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 06/05/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 06/05/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 06/05/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 06/05/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 06/05/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 06/05/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 06/05/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 06/05/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 06/05/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 06/05/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 06/05/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 06/05/2025 | 0900/1100 | ** | PPI | |

| 06/05/2025 | - | FOMC Meeting | ||

| 06/05/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 06/05/2025 | 1230/0830 | ** | Trade Balance | |

| 06/05/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 06/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 06/05/2025 | 1400/1000 | * | Ivey PMI | |

| 06/05/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 07/05/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 07/05/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 07/05/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 07/05/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 07/05/2025 | 0645/0845 | * | Foreign Trade | |

| 07/05/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 07/05/2025 | 0800/1000 | * | Retail Sales | |

| 07/05/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 07/05/2025 | 0900/1100 | ** | Retail Sales | |

| 07/05/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 07/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index |