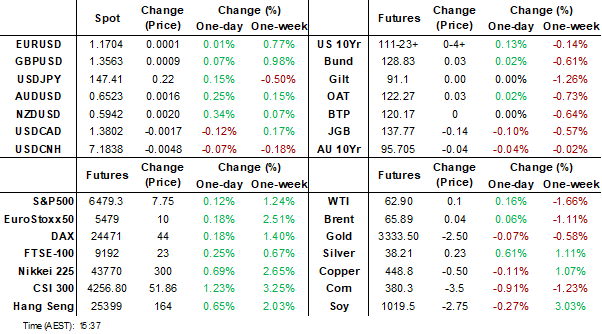

MNI EUROPEAN MARKETS ANALYSIS: China & Indian Equities Higher

- Crude prices fell at the open of trading on what appeared to be some progress towards a Ukraine peace deal with Ukraine’s President Zelenskyy and other European leaders to meet with US President Trump today. Russia is apparently offering to hold its frontlines in Kherson and Zaporizhzhia in exchange for the Donbas. US special envoy Witkoff said that the US/European security guarantee could “effectively offer Article-5 like language” (NATO), as reported by the BBC.

- Elsewhere, equity sentiment was mostly positive, particularly for China and Indian markets. Various drivers look to be in play. The USD was mixed, with higher beta FX outperforming at the margins. US yields were down a touch.

- Later the Fed’s Bowman speaks. In terms of data, euro area June trade and August US NY services & NAHB housing indices print.

MARKETS

US TSYS: Asia Wrap - Yields Leak Lower

The TYU5 range has been 111-19 to 111-24 during the Asia-Pacific session. It last changed hands at 111-23+, up 0-04+ from the previous close.

- The US 2-year yield has edged lower trading around 3.742%, down 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.304%, down 0.01 from its close.

- Yields extended higher on Friday, approaching the pivotal resistance area within the greater 4.10%-4.65% range. The 4.35% area in 10-Year yields should still see demand initially, but the way the market keeps bouncing off levels just below 4.20% will be disconcerting for longs..

- Fortune - “Wall Street overwhelmingly expects the Federal Reserve to cut rates next month, and Chairman Jerome Powell’s speech on Friday will give him a chance to hint at which direction policymakers are headed. But some analysts don’t think a September rate cut is in the bag, and even some that do expect a cut are doubtful that Powell will tease it at Jackson Hole.”

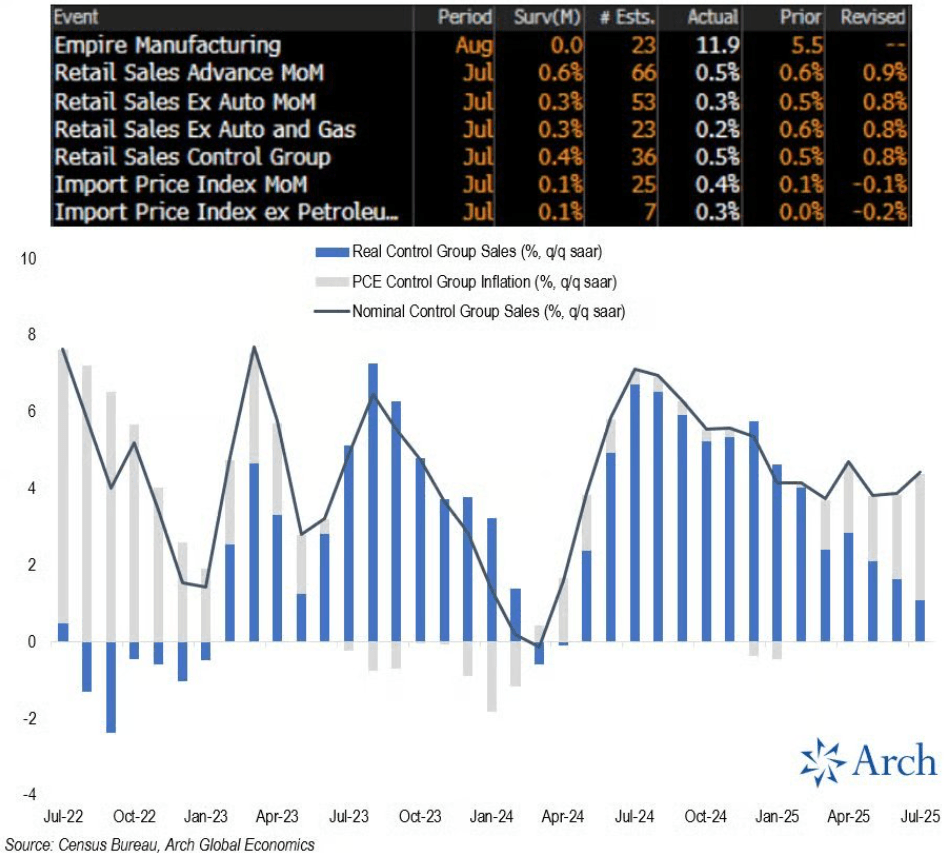

- Daily Chartbook on X: "On the surface: steady and solid consumer momentum. Under the hood: a rising share of sales growth is being 'paid for' by inflation."@Econ_Parker. See Fig.1 Below.

- Data/Events: New York Fed Services Business Activity, NAHB Housing Starts

Fig 1: Retail & Inflation

Source: MNI - Market News/@dailychartbook/Arch

JGBS: Modest Bear-Steepener Ahead Of Tomorrow's 20Y Supply

JGB futures are weaker, -15 compared to settlement levels

- Japan tertiary industry index rose 0.5% in June from a month earlier, compared to economists’ estimate at +0.2%.

- Cash US tsys are 1-2bps richer in today's Asia-Pac session after Friday's bear-steepener.

- (Bloomberg) "Japanese bonds are in for a rough week with Tuesday's 20-year debt sale looming as the next curve disruptor. It's a tricky tenor, neither a benchmark, nor an ultra-long. The duration is one of the least popular for investors with a history of sloppy outcomes which scatter the JGB playing field. Secondary JGB levels don't help either. Buyers at the seven previous auctions this year are underwater on a mark-to-market basis. Even sharply reducing the size of the July debt sale barely improved its overall metrics. Which augurs badly for this week when there is also Japanese CPI data on Friday that is unlikely to knock the BOJ off its rate hike path."

- Cash JGBs are flat to 3bps cheaper across benchmarks. The benchmark 10-year yield is 0.5bp higher at 1.577% versus the cycle high of 1.616%.

- Swap rates are flat to 1bp lower, with swap spreads tighter.

- Tomorrow, the local calendar will see 20-year supply.

AUSSIE BONDS: Cheaper But Off Cheaps

ACGBs (YM -2.5 & XM -4.5) are weaker but off cheaps on a data-light session.

- (Bloomberg) “Some 42% of respondents named US tariffs as their top concern compared with 37% who cited the strategic threat from China, according to a Newspoll published Monday in The Australian. A further 21% said neither bothered them, the survey conducted Aug. 11-14 for the newspaper showed.”

- Cash US tsys are 1-2bps richer in today's Asia-Pac session. This week's US calendar includes residential sector data (housing starts, homebuilder sentiment, existing home sales) and flash August PMI data as well as a few Fed speakers (notably Waller and Bowman) ahead of Friday's keynote speech by Fed Chair Powell as part of the annual Jackson Hole symposium Aug 21-23.

- Cash ACGBs are 3-4bps with the AU-US 10-year yield differential at -4bps.

- The bills are -1 to -3, with the strip steeper.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in September is given a 28% probability, with a cumulative 36bps of easing priced by year-end.

- Tomorrow, the local calendar will see Westpac Consumer Confidence.

- This week, the AOFM plans to sell A$1500mn of the 1.25% 21 May 2032 bond on Wednesday and A$300mn of the 4.75% 21 June 2054 bond on Friday.

BONDS: NZGBS: Cheaper But A Subdued Start To A RBNZ Policy Week Week

NZGBs closed slightly off worst levels, 2bps cheaper, after a relatively subdued start to the week.

- NZ-US and NZ-AU 10-year yield differentials closed 1-2bps tighter.

- RBNZ publishes Tara-ā-Umanga Business Expectations Survey, for September quarter. Average 1-year ahead inflation expectation rises to 2.53% from 2.44% in 2q. 2-year rises to 2.64% from 2.54%. 5-year rises to 3.16% from 3.06%. 10-year falls to 3.57% from 3.94%.

- NZGBs held by international investors increased to 62.8% from a month earlier (62.7%) in July.

- The highlight of the week will be Wednesday's RBNZ decision, where the MPC is likely to cut rates 25bp to 3% after pausing in July. It will also release updated forecasts, and Governor Hawkesby will hold a press conference. On Thursday, he will appear before a parliamentary committee to talk about the latest Monetary Policy Statement

- Swap rates closed 2-3bps higher.

- RBNZ dated OIS pricing closed little changed across meetings. 23bps of easing is priced for this week, with a cumulative 41bps by November 2025.

- Tomorrow, the local calendar will see PPI data.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 1.75% May-41 bond.

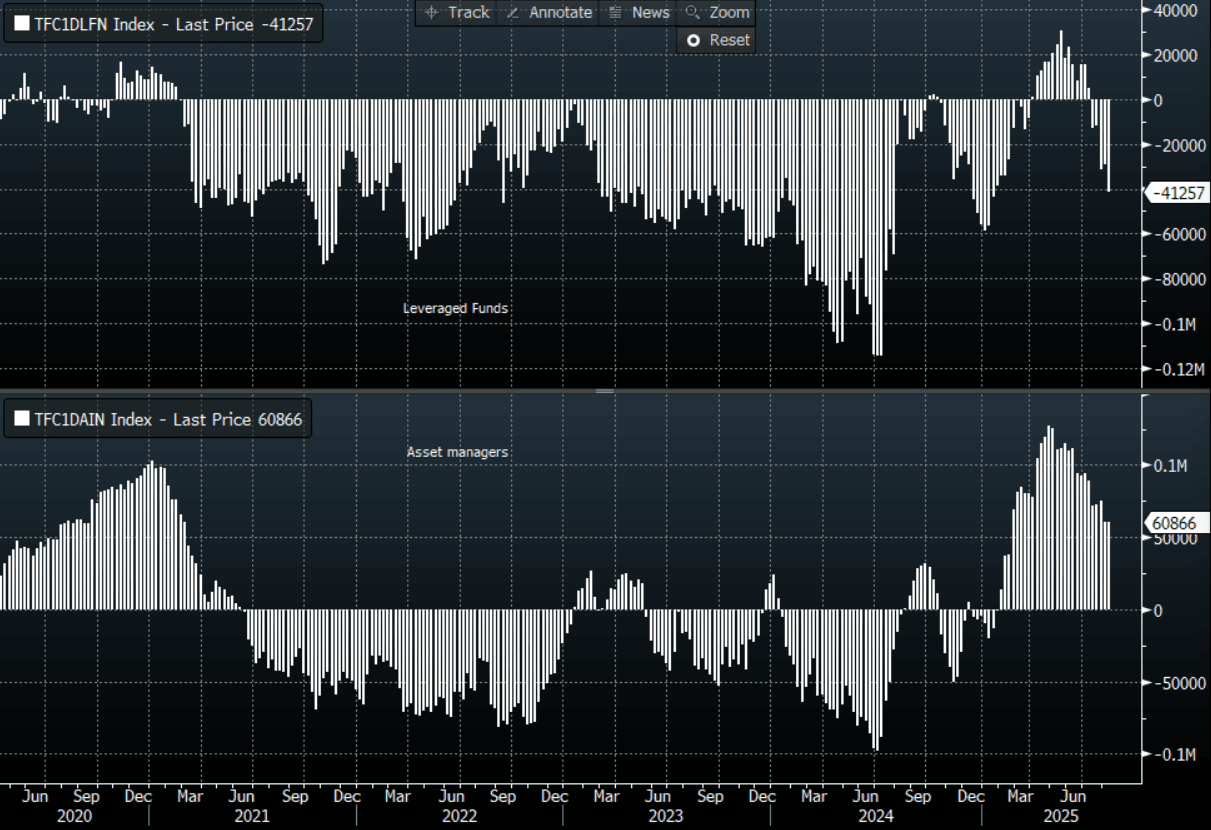

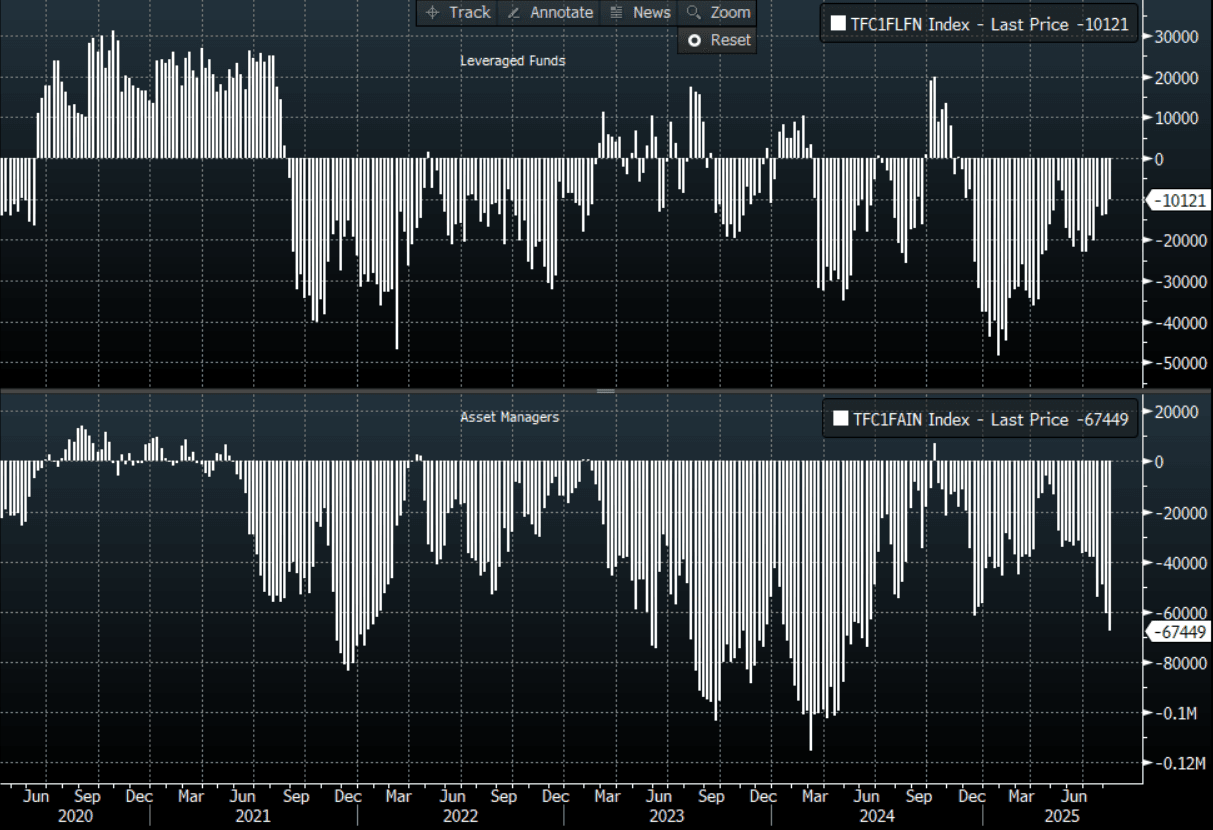

FOREX: EUR Longs Added To By Leveraged Investors & Asset Managers - CFTC

CFTC FX position shifts were mixed in the week ending the 12th of August, see the table below. Fresh additions to EUR longs were arguably the standout.

- In the leveraged space, yen shorts were added to, while GBP longs were pared. EUR longs were added to modestly, while AUD and NZD shorts were cut marginally.

- Aggregate shifts from leveraged investors elsewhere were modest. Yen outright shorts remain the largest for this investor base.

- On the asset manager side, additions to EUR longs were the standout, while the other notable flows were selling of both the AUD and CAD, which added to existing shorts for both currencies.

- Finally, GBP shorts were cut by asset managers, while there was little net change to JPY positions from this segment.

Table 1: FX CFTC Positioning Change & Outright Positions By Currency

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | -11949 | -41257 | 334 | 60866 |

| EUR | 4701 | 14415 | 20351 | 391816 |

| GBP | -5814 | 31455 | 7560 | -72783 |

| AUD | 3702 | -10121 | -6720 | -67449 |

| NZD | 2588 | -4190 | -1868 | -3679 |

| CAD | 46 | -31798 | -8647 | -70354 |

| CHF | 1516 | -1723 | -2194 | -37080 |

| MXN | -1247 | 16698 | 5109 | 38791 |

Source: CFTC/Bloomberg Finance L.P./MNI

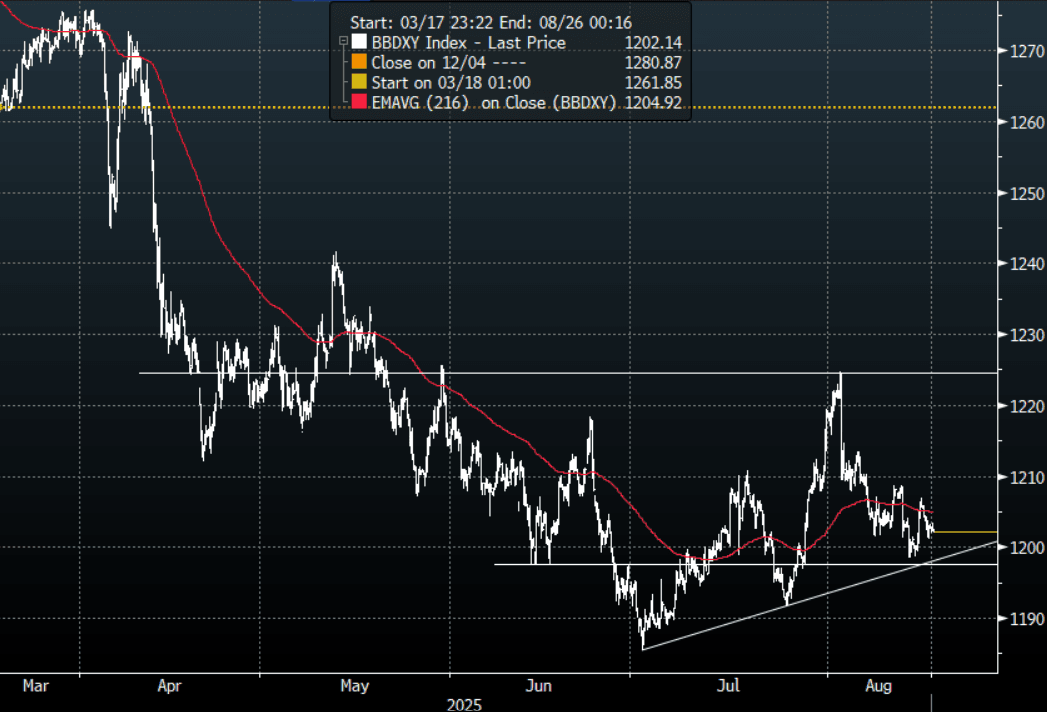

FOREX: Asia FX Wrap - USD Starts The Week Soft

The BBDXY has had a range of 1201.04 - 1203.32 in the Asia-Pac session, it is currently trading around 1202, -0.05%. The USD drifted lower again going into the weekend back towards its support just below 1200. This is clearly the side the market is more comfortable trading. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows.

- EUR/USD - Asian range 1.1694 - 1.1716, Asia is currently trading 1.1705. The market moved very quickly back to 1.1700 where it stalled on its first attempt to challenge this area. The pair continues to consolidate around 1.1700 trying to build momentum to again move towards the year's highs.

- GBP/USD - Asian range 1.3549 - 1.3567, Asia is currently dealing around 1.3560. Having broken back above its pivot look for dips to again be supported, first support seen now back towards 1.3400/1.3500.

- USD/CNH - Asian range 7.1818-7.1891, the USD/CNY fix printed 7.1322, Asia is currently dealing around 7.1820. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.15%, Gold $3355, US 10-Year 4.305%, BBDXY 1202, Crude Oil $62.92

- Data/Events : Spain Trade Balance, EZ Trade Balance

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

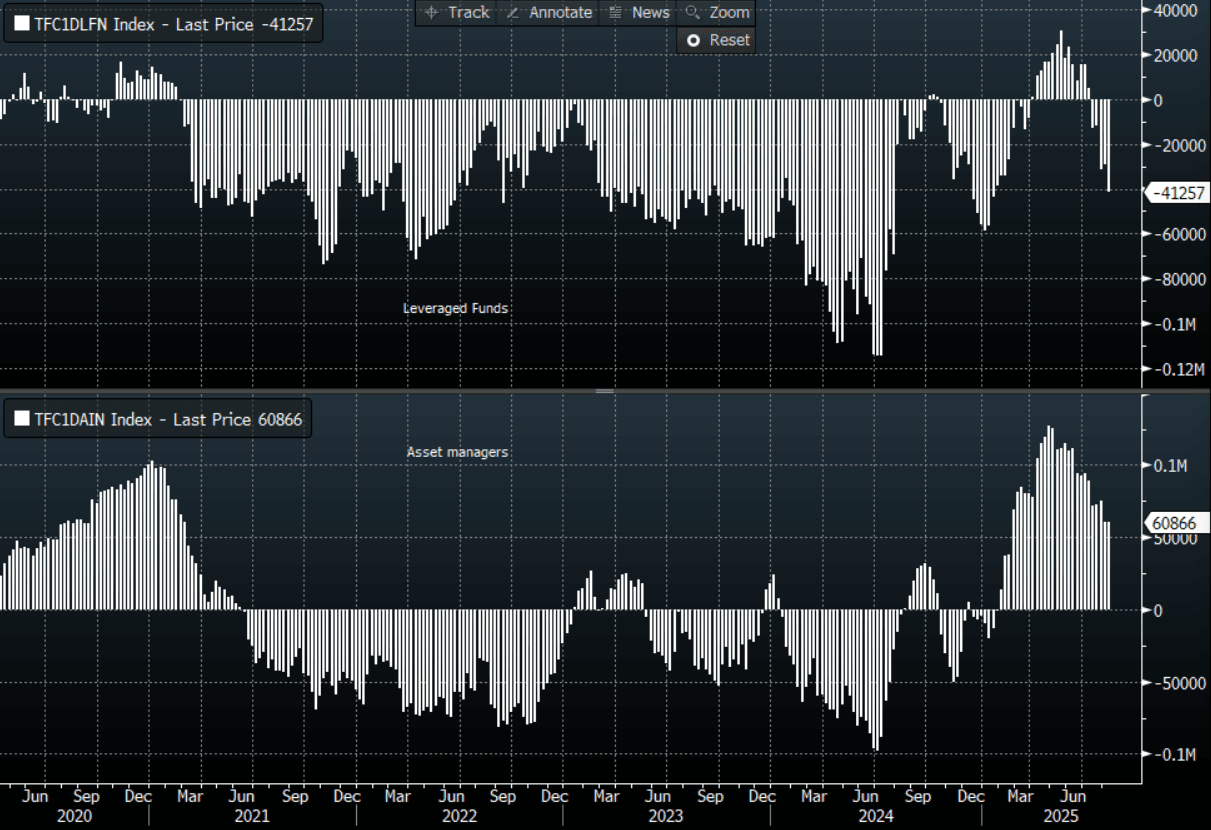

JPY: Asia Wrap - USD/JPY Bouncing Off Support, Leveraged Funds Bought The Dip

The Asia-Pac USD/JPY range has been 147.08-147.58, Asia is currently trading around 147.40, +0.15%. USD/JPY again found good demand on a 146 handle. Price continues to hold above the support area between 146.00/147.00, a sustained move below this support is needed to turn the momentum potentially lower again. While this plays out it looks to be more range trading within the wider 146.00-151.00 range. CFTC Data shows leveraged funds have bought this dip in USD/JPY betting the support remains intact.

- (Bloomberg) -- “Japan, the European Union, and South Korea are waiting for the US to implement concessions on tariffs, with Japan’s chief trade negotiator Ryosei Akazawa saying “the bleeding hasn’t stopped” for the country’s car industry.”

- "Japan’s CPI may show that inflation eased. But with rice prices still high and wage growth strong, price pressures are building. That puts the Bank of Japan on course to reduce stimulus." - BBG

- "Japan plans to tighten oversight of foreign workers with specialist expertise, after reports some are engaged in work not permitted by their visas, Kyodo said." - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.00($385m), 148.40($354m).Upcoming Close Strikes : 146.80($1.19b Aug 21), 150.00($1.06b Aug 21) - BBG.

- CFTC data shows last week asset managers maintained their JPY longs +60866( Last +60532), leveraged funds used the dip to add to their newly built short JPY position -41257(Last -29308).

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Pushes Off 0.6500

The AUD/USD has had a range of 0.6507 - 0.6521 in the Asia- Pac session, it is currently trading around 0.6520, +0.18%. US Equities momentum higher seemed to stall and the USD drifted lower again into the weekend. The AUD continues to consolidate around 0.6500, firmly in the middle of its 0.6350-0.6650 range with no clear direction. Risk has opened trade a little firmer in our session E-minis +0.15%, NQU% +0.25%.

- AU MNI: Productivity Roundtable This Week, Also Survey Data. The federal government’s productivity round table will be held this week from August 19 to 21 with RBA Governor Bullock scheduled to speak on the first day. In the August RBA press conference, she said that she will speak on how increasing productivity growth improves economic resilience. In terms of data, the focus will be on survey releases.

- (AFR - Mark Trevarthen) "Having witnessed at close quarters the changing behaviour of bond markets across four decades now, it has become increasingly clear that Australia has matured into a high-quality destination, and the market is expanding to reflect this, not only through the broader range of corporates coming to the market to issue Australian dollar bonds, but also the wider investor base beyond Australian shores, with offshore participation in primary issuance and the secondary market increasing significantly in the past year."

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6475(AUD541m), 0.6500(AUD424m), 0.6575(AUD395m). Upcoming Close Strikes : 0.6515(AUD744m Aug 19), 0.6600(AUD1.34b Aug 21) - BBG

- CFTC Data shows Asset managers added to their shorts -67449(Last -60729), the Leveraged community though reduced their own shorts -10121(Last -13997).

- AUD/JPY - Asia-Pac range 95.77 - 96.15, Asia is trading around 96.10. The pair found good demand last week towards 95.50, price is now firmly back into the 94.50-97.50 range looking for clearer direction.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - NZD/USD Bouncing Off 0.5900

The NZD/USD had a range of 0.5921 - 0.5938 in the Asia-Pac session, going into the London open trading around 0.5935, +0.22%. US equities' momentum higher seemed to stall and the USD drifted lower again into the weekend. The NZD/USD found some demand back towards 0.5900 and is bouncing off this support in our session. While still firmly in the 0.5850-0.6150 range it's tough to discern any real direction. Risk has opened a little higher this morning, E-minis +0.15%, NQU5 +0.25%.

- NZ MNI: RBNZ Expected To Cut Rates On Wednesday, Governor Speaks. The highlight of the week will be Wednesday’s RBNZ decision where the MPC is likely to cut rates 25bp to 3% after pausing in July. It will also release updated forecasts and Governor Hawkesby will hold a press conference. On Thursday he will appear before a parliamentary committee to talk about the latest Monetary Policy Statement.

- "Reserve Bank of New Zealand publishes Tara-ā-Umanga Business Expectations Survey, for September quarter. Average 1-year ahead inflation expectation rises to 2.53% from 2.44% in 2q. 2-year rises to 2.64% from 2.54%. 5-year rises to 3.16% from 3.06%. 10-year falls to 3.57% from 3.94%.” -BBG

- "RBNZ BUSINESS SURVEY SHOWS TWO-YEAR INFLATION EXPECTATION 2.64%" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5925(NZD400m Aug 20), 0.5980(NZD660m Aug 21). - BBG

- CFTC Data shows Asset Managers have cut their longs completely and started to rebuild a short adding slightly in the NZD -3679(Last -1811), the Leveraged community though reduced their own shorts slightly -4190(Last -6778).

- AUD/NZD range for the session has been 1.0974 - 1.0993, currently trading 1.0985. The Cross is trying to push higher but will need a sustained break above the 1.1000 area. Until then the range looks to be 1.0850-1.1000.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: China & India Outperform, South Korea Lags

Asian equity markets are mostly on the front foot in the first part of Monday dealings, although there are some pockets of weakness. The lead from US markets on Friday was softer, particularly in the tech space. US futures are up a touch in the first part of Monday dealings, while EU futures are also higher. Market attention remains on US-Ukraine talks later, with focus on whether a peace deal to end the Russia-Ukraine conflict can be reached. The knee-jerk reaction from any peace deal reached is likely to be positive for risk appetite.

- China markets are outperforming. The CSI 300 was last up around 1.5%, putting the index near 4266, which is fresh intra-session highs back to early Oct last year. Hopes of fresh stimulus after disappointing July data is aiding sentiment, while there is also talk of outflows from bonds into equities (the 10yr yield is up 4bps to 1.78%). US President Trump also stated late last week that he will hold off raising China tariffs over their Russian oil purchases.

- Indian markets are also up firmly (+1.5%. For the Nifty, we are back above the 25000 region, last seen in late July. If the better equity tone sees offshore investors return, we could see further gains. This follows a period of underperformance for Indian shares. The proposal by PM Modi to the lower the GST is seen as a positive for consumer sentiment, and more broadly growth, particularly if we can be matched with a more reform orientated government. Another equity market positive is potentially closer India-China ties.

- Japan markets are higher, the Topix +0.60%, the NKY 225 up close to 0.80%. South Korean markets have returned after Friday's break and are off over 1%, putting the Kospi back under 3200. Taiwan stocks are holding up better, despite a Friday slump in the US SOX index.

- Australia's markets is around flat, as we sit near record highs.

- In South East Asia, trends are mixed. Singapore is softer, but Malaysia and the Philippines have ticked higher. Indonesian markets are out today.

ASIA STOCKS: Indonesia Enjoys Best 5 Day Run Of Inflows Since Sep 2024

Both Indian and South Korea markets were out on Friday, limiting the equity update for the region. Both markets return today. Elsewhere, Taiwan flows were positive, marginally bringing the 5 day sum of inflows back into positive territory. On Friday, local equities closed just short of recent highs. The authorities also revised higher the 2025 growth forecast to 4.45% from 3.1% (on Friday Q2 preliminary GDP rose 8%y/y, close to the initial estimates). Tech equity sentiment in the US was softer in Friday trade though, with the SOX down over 2%.

- Indonesian positive inflow momentum continued on Friday, bringing inflows last week to just over $400mn. This is the best run for a 5 day period in terms of inflows since late Sep last year. Local equities faltered on Friday, but remain close to recent record highs. The budget deficit projection of 2.48% of GDP for 2026 is slightly tighter than this year's (just beyond 2.5% of GDP), and is likely to be welcomed by the market that was fearful of fiscal slippage under Prabowo's Presidency. Indonesian markets are out today.

- Elsewhere Malaysian outflows continued, with 16 straight sessions of outflows by offshore investors.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn)** | -26 | 510 | -4467 |

| Taiwan (USDmn) | 172 | 90 | 4662 |

| India (USDmn)* | -258 | -977 | -12699 |

| Indonesia (USDmn) | 81 | 412 | -3333 |

| Thailand (USDmn) | -17 | -240 | -1937 |

| Malaysia (USDmn) | -40 | -134 | -3354 |

| Philippines (USDmn) | -9 | 22 | -603 |

| Total (USDmn) | -97 | -317 | -21730 |

| * Data Up To Aug 13 | |||

| ** Data Up To Aug 14 |

Source: Bloomberg Finance L.P./MNI

OIL: Crude Range Trading Ahead Of Monday’s Ukraine Meeting

Oil prices are slightly higher today after falling over a percent on Friday. WTI is up 0.2% to $62.91/bbl after falling to $62.46 early in the session. Brent is 0.1% higher at around $65.89/bbl after a low of $65.47. Prices fell on the open of trading on what appeared to be some progress towards a Ukraine peace deal with Ukraine’s President Zelenskyy and other European leaders to meet with US President Trump today. The market is also relieved that punitive tariffs on China for buying Russian fuel currently seem off the table.

- Russia is apparently offering to hold its frontlines in Kherson and Zaporizhzhia in exchange for the Donbas. US special envoy Witkoff said that the US/European security guarantee could “effectively offer Article-5 like language” (NATO), as reported by the BBC.

- Trump wants an agreement with him stating on Truth Social that “Ukraine can end the war with Russia almost immediately”. It is worth noting that Ukraine has to hold a referendum though to agree to official territory changes.

- If Russia walks away from negotiations then US sanctions are likely to be extended including punitive tariffs on those who buy its fuel which could impact supplies and push oil prices higher.

- Later the Fed’s Bowman speaks. In terms of data, euro area June trade and August US NY services & NAHB housing indices print.

GOLD: Bullion Higher, European Leaders Meet Trump Later

After range trading on Friday, gold is 0.5% higher today at $3351.2/oz, close to the intraday high of $3351.81. It appears to have been supported by slightly lower US yields and greenback, and possibly also by some doubt regarding the prospects for a Ukraine peace deal. Russia is demanding the Donbas, not all of which it currently occupies, while Ukraine is not prepared to cede territory, especially if unoccupied. Ukraine’s President Zelenskyy and other European leaders meet with US President Trump today.

- Silver is up 0.3% to $38.120, close to today’s peak of $38.138. It fell to $37.820 early in trading.

- Equities are generally stronger with the S&P e-mini up 0.1%, Hang Seng +0.6%, Nikkei +0.9% but KOSPI down 1.1%. Oil prices are slightly higher with WTI +0.1% to $62.90/bbl. Copper is up 0.1%.

- Later the Fed’s Bowman speaks. In terms of data, euro area June trade and August US NY services & NAHB housing indices print.

CHINA: Country Wrap: Infrastructure Investment Leads

- China’s infrastructure investment is gaining momentum in 2025, driven by an increase in issuance of of local government special bonds according to an article in the Securities Daily. Year to date infrastructure investment rose over 3% YoY, outperforming the 1.6% growth by overall investment, report cites data by the National Bureau of Statistics . Local government issuers issued new special bonds totaling 2.8369 trillion yuan ($395 billion) this year, up 39.7% from the same period in 2024, report cites data provided by Wind. (source China Securities Daily)

- Local governments are increasing efforts to stabilize the real estate market by optimizing housing policies and accelerating urban renewal initiatives, Shanghai Securities News reported, citing analysts. Urban renewal has become a pivotal turning point in city development. By upgrading existing assets and stimulating domestic demand, it helps reinforce market stability and supports the transformation of the real estate industry: industry experts (source Shanghai Securities)

- China's major bourses have started the week off positively with the Hang Seng up +0.62%, the CSI 300 +1.5%, the Shenzhen Comp +1.2% and Shenzhen up +2%.

- Yuan Reference Rate at 7.1322 Per USD; Estimate 7.1812

- The CGB10 year continues to drift higher, following on from moves on Friday. Having finished Friday at 1.74%, it is up +3bp today at 1.77%, the highest level of the month.

INDIA: Country Wrap: US Cancels Trade Visit

- New Delhi: A planned visit by US trade negotiators to New Delhi from Aug 25 to 29 has been cancelled, delaying talks on a proposed bilateral trade agreement, Indian business and financial news network NDTV Profit says, citing people familiar with the matter. The current round of negotiations for the proposed bilateral trade agreement is now likely to be deferred to another date, the report last Saturday said, dashing hopes of some relief before the Aug 27 deadline for the additional tariff on Indian goods kicks in. (source The Star)

- India expects consumption tax cuts announced by Prime Minister Narendra Modi will give a boost to the economy without hurting the government’s fiscal deficit, helping to offset the fallout from higher US tariffs. Officials in New Delhi said on the weekend the proposed changes to the goods and services tax — which will see the number of tax categories reduced to two from four — would benefit a broad range of sectors, including consumers and small businesses. The adjustments would have a limited effect on government revenue, officials told reporters, requesting anonymity in order to discuss the plans. (source BBG)

- The NIFTY 50 is up strongly in morning trade, reacting to Modi's pledges and has gained +1.4%.

- The Rupee is up +0.2% at 87.37

- Bonds : the 10yr yield has jumped +4bp in early trade to 6.45%

SOUTH KOREA: Country Wrap: Government Debt on the Increase

- Government debt is expected to rise, accelerated by the expansionary fiscal policy under the Lee Jae Myung administration, observers said Sunday. Further straining the fiscal outlook is Korea’s low potential growth, coupled with tariff uncertainties. This, along with years of tax shortfalls under the previous Yoon Suk Yeol administration, leaves debt financing as a source of government spending. Whether the expansionary fiscal drive can lead to growth and a subsequent increase in tax revenue remains to be seen. (source Korea Times)

- Container shipping costs from Korea to the United States declined last month, largely due to a decrease in trade volume influenced by U.S. tariff policies, the customs agency said Monday. The average shipping cost for a 40-foot container from Korea to the U.S. east coast dropped 4.5 percent from a month earlier to 6.4 million won ($4,610) in July, according to data from the Korea Customs Service. Shipping rates to the U.S. west coast dropped 8.5 percent to 5.53 million won during the same period. (source Korea Times)

- The KOSPI is one of the worst performers of its regional peers today down -1.2%

- The Won is the best performer of its regional peers with gains of +0.40% to 1,383.36

- Bonds have had a strong sell off with yield up to +4bps higher. KTB 10yr 2.84% (+4bps)

ASIA FX: Most USD/Asia Pairs Lower, KRW Plays Catch Up As Onshore Returns

USD/Asia pairs are mostly lower in the first part of Monday trade. The won has outperformed, up around 0.40%, as onshore markets return. This looks to be catch up to the weaker USD trend seen while onshore markets were shut on Friday. Gains are fairly modest elsewhere, while MYR and TWD have lagged a touch.

- Spot USD/KRW is back around 1384/85, off 0.40% versus end Thursday levels. This keeps us within recent ranges and largely looks to be catch up with softer USD trends. Onshore equities have struggled today, the Kospi down over 1%, but this hasn't dented FX sentiment.

- USD/CNH is down a touch, but still above 7.1800, keeping us firmly within recent ranges. Onshore China equities have outperformed, the CSI 300 up over 1.6%. A number of positives look to be in play. Hopes of fresh stimulus after disappointing July data is aiding sentiment, while there is also talk of outflows from bonds into equities (the 10yr yield is up 4bps to 1.78%). US President Trump also stated late last week that he will hold off raising China tariffs over their Russian oil purchases.

- Spot USD/TWD is holding above 30.00 at this stage, while SD/HKD spot is near recent lows, last close to 7.8250.

- USD/MYR has edged higher, last above 4.2200, up around +0.20%. USD/SGD is down a touch to 1.2820.

- USD/THB is little changed, holding near 32.43. Q2 GDP was a touch above market forecasts, up 0.6%q/q, versus 0.5% forecast. This took y/y growth to 2.8%, versus 2.7% forecast but down from 3.2% prior.

- Indonesian markets are out today.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 18/08/2025 | 0900/1100 | * | Trade Balance | |

| 18/08/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 18/08/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 18/08/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 18/08/2025 | 1430/1530 | DMO likely to publish FQ3 consultation agenda | ||

| 18/08/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 18/08/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 19/08/2025 | 0800/1000 | ** | EZ Current Account | |

| 19/08/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 19/08/2025 | 1230/0830 | *** | CPI | |

| 19/08/2025 | 1230/0830 | *** | Housing Starts | |

| 19/08/2025 | 1230/0830 | *** | Housing Starts | |

| 19/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index |