MNI EUROPEAN MARKETS ANALYSIS: Calmer End to the Week

- Oil's rally slowed into week's end as markets paused and waited for the next phase in the Israel - Iran conflict.

- Major equity bourses had a positive end to the week with the KOSPI in Korea the standout.

- Major data focus was CPI out of Japan which surprised to the upside and China's Loan Prime Rates which remain on hold.

- Later we have PSNB from the UK and Retail Sales, Manufacturing Confidence in France, PPI in German and in the US the Philadelphia Fed Business Outlook.

MARKETS

US TSYS: Asia Wrap - Short-End Yields Edge Lower

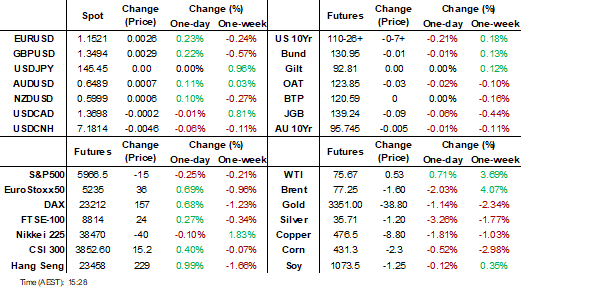

The TYU5 range has been 110-26+ to 110.30 during the Asia-Pacific session. It last changed hands at 110-28+, up 0-03 from the previous close.

- The US 2-year yield has edged lower trading around 3.9225%, down 0.02 from its close.

- The US 10-year yield trades around 4.39%, unchanged from its close.

- This has seen the yield curve steepen in Asia - 2s10s +1.29 at 45.816, 5s30s +2.01 at 91.627.

- (Bloomberg) -- “Bloomberg - “Australian investors, including State-owned Funds SA and Queensland Investment Corp., are reducing their holdings of US Treasuries due to concerns over President Donald Trump's tariff and tax plans.”

- The June FOMC communications had a hawkish tilt overall, despite the immediate dovish reaction to the updated Dot Plot retaining the median expectation of 50bp in rate cuts by end-2025.

- The 10-year yield continues to find decent supply back towards its 4.30/35% support, this area needs to hold if yields are to move higher. The range looks to be 4.30% - 4.60% for now a break either side would provide a clearer direction.

- Data/Events: Philadelphia Fed Business Outlook, Leading Index

JGBS: Twist-Steepener Holds After Core CPI Beat

JGB futures are weaker and hovering near session lows, -9 compared to settlement levels.

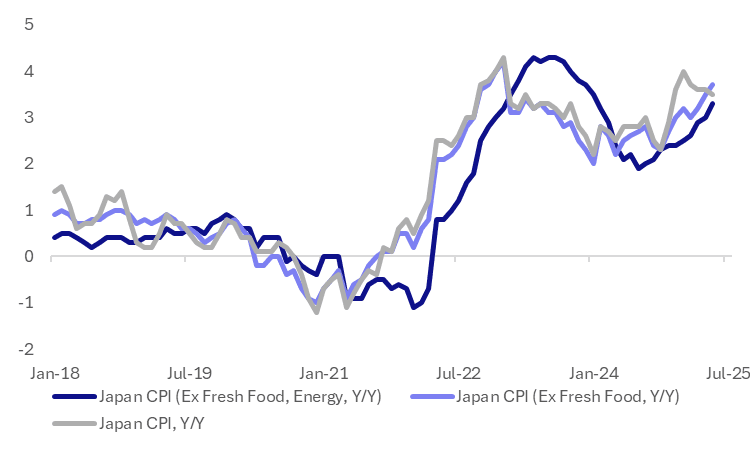

- Japan's May nationwide CPI saw headline at 3.5%y/y, which was as expected (the April outcome printed at 3.6%). The ex-fresh food core measure rose 3.7%y/y (against a 3.6% forecast and 3.5% prior outcome). The measure, which excludes fresh food and energy, was 3.3%y/y, also above expectations and prior outcomes (3.2% forecast and 3.0% in April).

- Our Japan policy team noted, "Services prices, a key BOJ focus for assessing the strength of the wage-price cycle, rose 1.4% y/y in May, slightly up from 1.3% in April, but remained below the 2% mark, indicating weak momentum and the need for further gains to achieve the BOJ's inflation target sustainably."

- "AKAZAWA: JULY 9 IS NOT DEADLINE FOR JAPAN-US TRADE TALKS, TO EXAMINE WHAT KEPT FROM REACHING A TRADE DEAL" – BBG

- Cash US tsys have twist-steepened, with yields 2bps lower to 1bp higher, in today's Asia-Pac session after yesterday's holiday.

- Cash JGBs are mixed across benchmarks, with the curve steeper and yields 1bp lower to 3bps higher. The benchmark 20-year yield is 0.3bp higher at 2.376% ahead of Tuesday's supply.

- The swap curve has bear-steepened, with rates 1-3bps higher.

- On Monday, the local calendar will see Jibun Bank PMIs.

JAPAN DATA: Core Measures Post Upside Surprise, But Services Inflation Modest

Japan's May nationwide CPI saw headline at 3.5%y/y, which was as expected (the April outcome printed at 3.6%). The ex fresh food core measure rose 3.7%y/y (against a 3.6% forecast and 3.5% prior outcome). The measure which excludes fresh food and energy was 3.3%y/y, also above expectations and prior outcomes (3.2% forecast and 3.0% in April).

- The chart below plots these three inflation metrics in y/y terms. The core measures continue to accelerate and are tracking towards recent cycle highs, particularly for core, ex fresh food.

- The core measure which excludes all food and energy was 1.6%y/y, unchanged from the April outcome.

- In m/m terms, the headline rose 0.3%, and the core measures maintained positive trends. Goods prices rose 0.5%m/m, while services were +0.2%, although this often gets revised to flat. Our Japan policy team noted, "Services prices, a key BOJ focus for assessing the strength of the wage-price cycle, rose 1.4% y/y in May, slightly up from 1.3% in April, but remained below the 2% mark, indicating weak momentum and the need for further gains to achieve the BOJ’s inflation target sustainably."

- In terms of the sub-indices we had fresh food down -2.6%m/m, but aggregate food +0.3%m/m. Utilities rose 2.8%m/m, while household goods and entertainment were also up in the month. Transport and education both fell modestly.

- Given growth/trade uncertainties, today's print is unlikely to shift BoJ near term thinking. A point reinforced by the still sub 2%y/y level for services inflation.

Fig 1: Japan May Inflation Y/Y - Core Measures Post Slight Upside Surprise

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Little Changed, Subdued Session To End Week

ACGBs (YM flat & XM +0.5) are little changed on a subdued data-light Sydney session.

- Cash US tsys have twist-steepened, with yields 2bps lower to 1bp higher, in today's Asia-Pac session after yesterday's holiday.

- The June FOMC communications had a hawkish tilt overall, despite the immediate dovish reaction to the updated Dot Plot retaining the median expectation of 50bp in rate cuts by end-2025. Fed Chair Powell was far from emphatic about the prospect of rate cuts, all but taking a cut at the July meeting off the table. (See MNI Fed Review Hidden PDF)

- Cash ACGBs are little changed, with the AU-US 10-year yield differential at -17bps.

- The bills strip is modestly richer, with pricing +1 to +2.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in July is given a 79% probability, with a cumulative 72bps of easing priced by year-end.

- On Monday, the local calendar will see S&P Global PMIs.

- Next week, AOFM plans to sell A$1000mn of the 1.75% 21 November 2032 bond on Monday and A$1000mn of the 3.50% 21 December 2034 bond on Wednesday.

FOREX: Asia Wrap - Market Quick To Sell USD's Again

The BBDXY has had a range of 1207.12 - 1209.76 in the Asia-Pac session, it is currently trading around 1207. The market has very quickly reversed the moves pricing in the imminent participation of the US into the Middle East conflict, from being almost 1.2% down the market has come back to almost where it started. ESU5 -0.2%, NQU5 -0.2%. Interesting though Seymour Hersh printed an article on his substack reporting that “heavy American bombing” will begin this weekend.

- EUR/USD - Asian range 1.1495 - 1.1530, Asia is currently trading 1.1525. EUR has rejected the move above 1.1600 but dips should continue to find demand, first support back towards the 1.1400 area then 1.1100/1200. Price action does not look great in the short-term with a potential false break above 1.1500/1.1600.

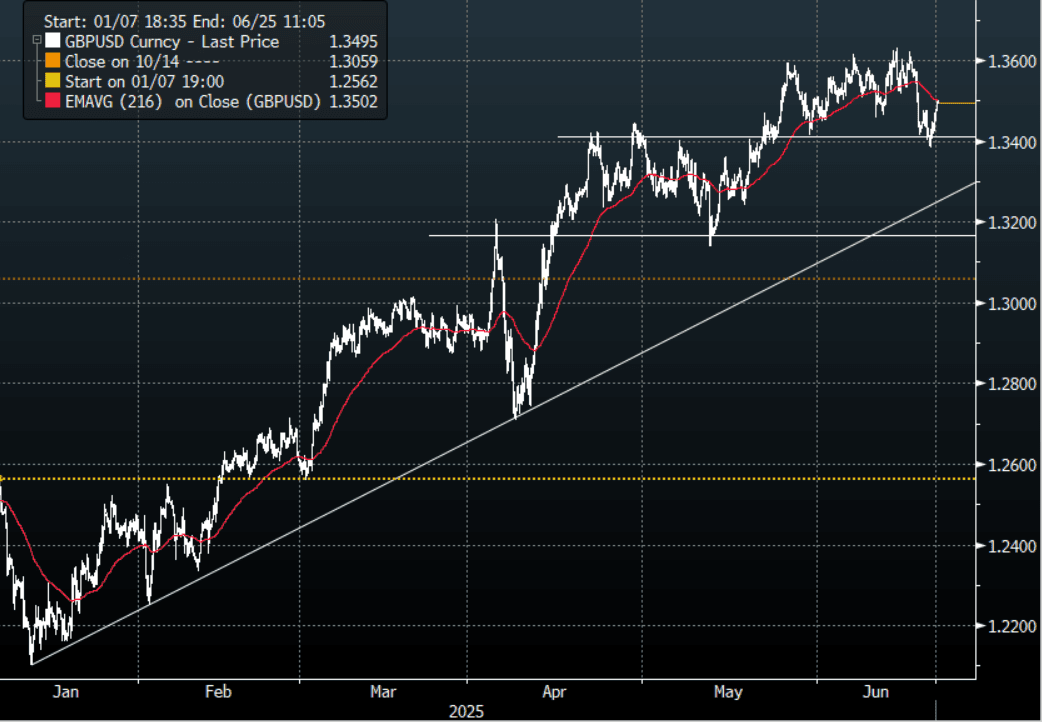

- GBP/USD - Asian range 1.3450 - 1.3500, Asia is currently dealing around 1.3495. The GBP bounced nicely off its support around 1.3400 and is now looking back towards the Weekly 1.35/36 pivot. First support is seen around the 1.3400 area, a sustained move back below here and we could see a deeper correction unfold.

- USD/CNH - Asian range 7.1771 - 7.1874, the USD/CNY fix printed 7.1695. Asia is currently dealing around 7.1815. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX -0.2%, Gold $3355, US 10-Year 4.39%, BBDXY 1207, Crude oil $75.67

- Data/Events : Ger PPI, FRA Buss Confidence, EZ M3 Money Supply,

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

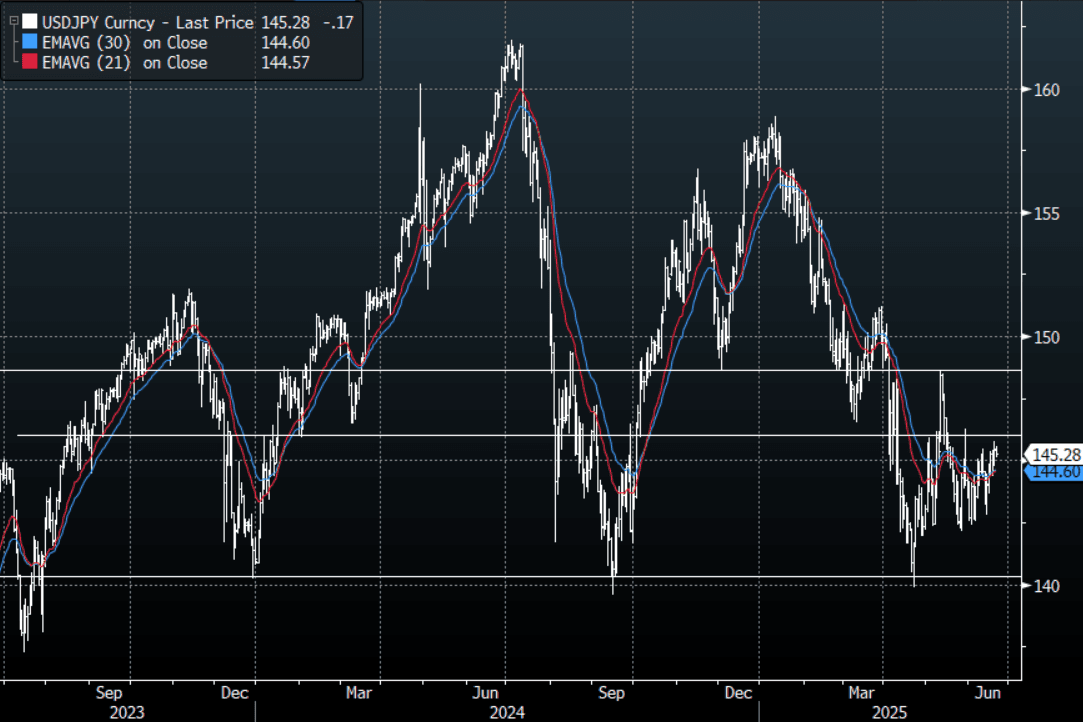

JPY: Asia Wrap - JPY Underperformance In The Crosses, USD/JPY Steady

The Asia-Pac USD/JPY range has been 145.12 - 145.56, Asia is currently trading around 145.25, -0.13%. USD/JPY has drifted lower in a muted Asian session, the JPY underperformed in the crosses though as risk bounced back on the hopes the US would not be joining the conflict this weekend. Based on their recent history though it would be unwise to think there is a zero risk of this weekend seeing the US starting to drop bombs in Iran.

- Our Japan policy team noted, "Services prices, a key BOJ focus for assessing the strength of the wage-price cycle, rose 1.4% y/y in May, slightly up from 1.3% in April, but remained below the 2% mark, indicating weak momentum and the need for further gains to achieve the BOJ's inflation target sustainably."

- “JAPAN GOVT MULLS BUILDING STATE-OWNED SHIPYARD, NIKKEI SAYS" - BBG

- "AKAZAWA: JULY 9 IS NOT DEADLINE FOR JAPAN-US TRADE TALKS, TO EXAMINE WHAT KEPT FROM REACHING A TRADE DEAL" - BBG

- USD/JPY price action continues to point to a market that is positioned long JPY.

- Price is back in its recent 142.00 - 146.50 range and will need a break either side of that to get a clearer direction.

- The market believes we could see a decent move lower in USD/JPY but with positioning at extremes we have seen the risk of pullbacks increase. A break above 146.50/147.00 would begin to challenge the conviction of any shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.00($1.92b). Upcoming Close Strikes : 144.50($1.18b June 25)

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

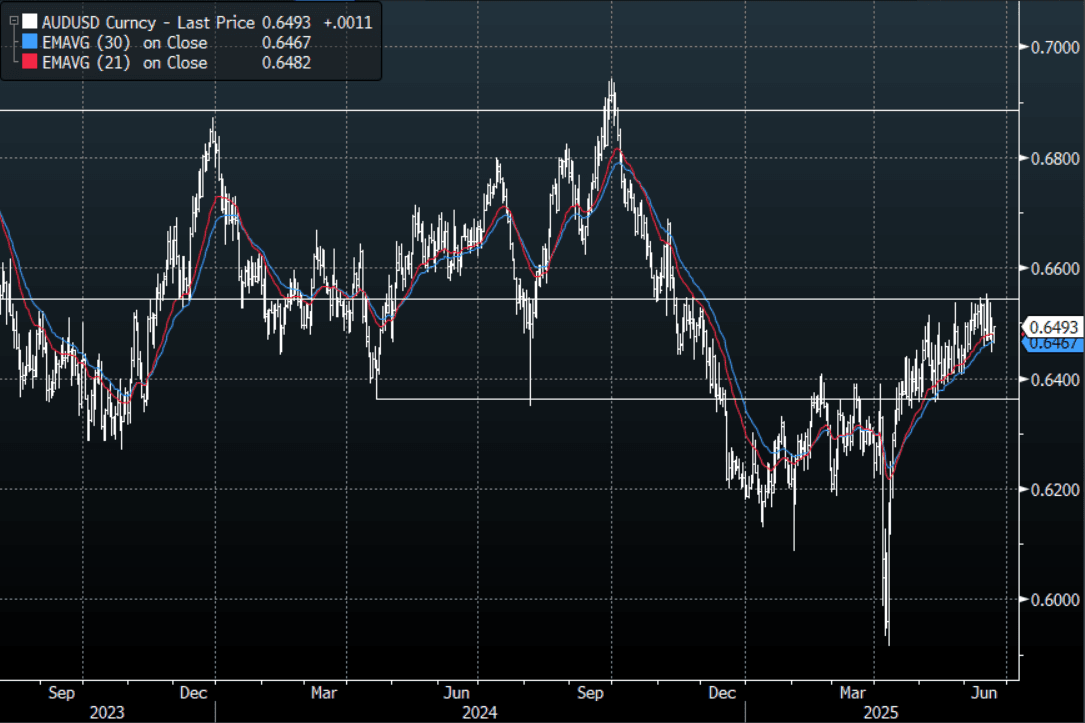

AUD: Asia Wrap - AUD/USD Bounces As Market Prices Out US Entering Conflict

The AUD/USD has had a range of 0.6463 - 0.6495 in the Asia- Pac session, it is currently trading around 0.6495. The AUD has edged higher in our session +0.2% as the market prices out the chances of the US joining in the conflict. Recent history reminds us that there is still every chance we see some sort of US strike this weekend, and the article printed by Seymour Hersh points to that very fact.

- Seymour Hersh: "This is a report on what is most likely to happen in Iran, as early as this weekend, according to Israeli insiders and American officials I’ve relied upon for decades. It will entail heavy American bombing. I have vetted this report with a longtime US official in Washington, who told me that all will be “under control” if Iran’s Supreme Leader Ali Khamenei “departs.” Just how that might happen, short of his assassination, is not known.”

- (AFR) "Interest rates in Australia and the United States may be on hold for longer than the market and borrowers are hoping, thanks to resilient jobs numbers that suggest there is no pressing need to cut rates aggressively."

- The AUD looked as if it might trade back down to its 0.6350/0.6400 support before that statement, but has bounced overnight off the 0.6450 area.

- Price remains in the wider 0.6350 - 0.6550 range for now, a sustained break above 0.6550/0.6600 is needed for the move higher to accelerate.

- Technically buyers should continue to be around on dips while the support in the AUD/USD holds, a close back below 0.6350 is needed to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6650(AUD708m). Upcoming Close Strikes : none

AUD/JPY - Today's range 93.97 - 94.35, it is trading currently around 94.30.Choppy price action as the pair establishes a range between 92.00 - 96.00. A break back below 91.50/92.00 is needed to see the move lower regain momentum and the focus turn back to the year's lows again.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

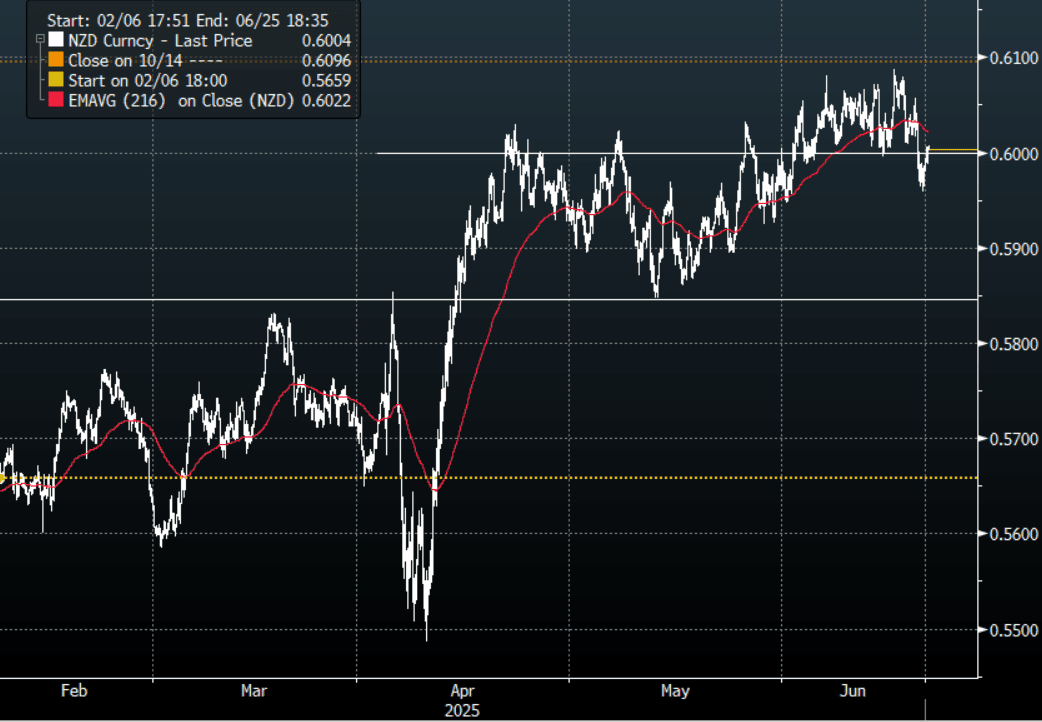

NZD: Asia Wrap - NZD/USD Reclaims 0.6000 As Risk Reverses

The NZD/USD had a range of 0.5979 - 0.6008 in the Asia-Pac session, going into the London open trading around 0.6005, +0.2%. The NZD has bounced in our session as the timeline for the US to enter the war is pushed out, not sure how far it can go until we get this weekend out of the way and the risk it still presents.

- (BBG): Trump Plans to Decide Within Two Weeks on Whether to Strike Iran. White House spokeswoman Karoline Leavitt said Trump’s message on Thursday is that “based on the fact that there’s a substantial chance of negotiations that may or may not take place with Iran in the near future, I will make my decision whether or not to go within the next two weeks.”

- The NZD bounced off the 0.5960 area on this news and has looked to challenge the 0.6000 area again in our session. Can the market completely price out the risk the US still goes in this weekend ?

- Technically while the support around 0.5850 holds in NZD/USD there should be buyers around on dips towards this area. A clear sustained break above 0.6050/0.6100 is needed for the pair to get momentum to push higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5830(NZD300m June 23)

- AUD/NZD range for the session has been 1.0805 - 1.0823, currently trading 1.0815. The cross is struggling to get any momentum back above 1.0800, it needs to hold above here and start extending higher to put a higher low in place. A failure to hold up here and the drift lower would be back on.

Fig 1: NZD/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: The KOSPI Leads in Challenging Week

Major bourses put in a strong end to what has been a challenging week, given the happenings in the middle east. The KOSPI is the stand out for the week with solid returns whilst most others are down.

- The Hang Seng is up over +1.1% today for a strong finish to the week, yet down by -1.6% in the last five days. The CSI 300 is up just +0.24% today and down -0.31% for the week. The Shanghai Comp is up just +0.08% and down -0.36% for the week. The Shenzhen Comp is the outlier down -0.28% Friday and down -1.29% for the week.

- In Taiwan, the TAIEX fell -0.39% today and is down -0.70% for the week.

- The KOSPI is up +0.85% today and better by almost 4% for the week on hopes of a new government stimulus.

- The FTSE Malay KLCI is up just +0.22% and down -0.35% for the week.

- The Jakarta Composite is down -0.72% today and -3.4% for the week

- The FTSE Straits Times is up +0.09% today, and down -0.35% for the week whilst the PSEi in the Philippines is flat and down -1.6% for the week.

- The NIFTY 50 in India is up +0.37% today and holding on to gains of +0.60% for the week.

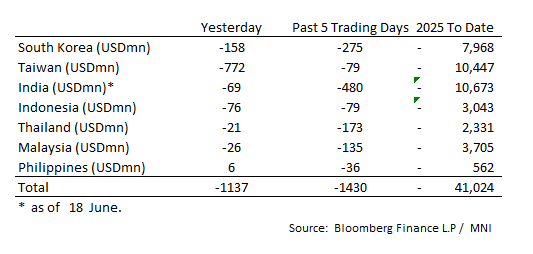

ASIA STOCKS: Outflows Resume for Major Markets

Large OutFlows for Korea and Taiwan

- South Korea: Recorded outflows of -$158m yesterday, bringing the 5-day total to -$275m. 2025 to date flows are -$7,968. The 5-day average is -$55m, the 20-day average is +$177m and the 100-day average of -$85m.

- Taiwan: Had outflows of -$772m as of yesterday, with total outflows of -$79 m over the past 5 days. YTD flows are negative at -$10,447. The 5-day average is -$16m, the 20-day average of -$10m and the 100-day average of -$79m.

- India: Had outflows of -$69m as of the 18th, with total outflows of -$480m over the past 5 days. YTD flows are negative -$10,673m. The 5-day average is -$96m, the 20-day average of -$33m and the 100-day average of -$66m.

- Indonesia: Had outflows of -$76m yesterday, with total outflows of -$79m over the prior five days. YTD flows are negative -$3,043m. The 5-day average is -$16m, the 20-day average -$5m and the 100-day average -$29m.

- Thailand: Recorded outflows of -$21m as of yesterday, with outflows totaling -$173m over the past 5 days. YTD flows are negative at -$2,331m. The 5-day average is -$35m, the 20-day average of -$30m and the 100-day average of -$21m.

- Malaysia: Recorded outflows of -$26m as of yesterday, totaling -$135m over the past 5 days. YTD flows are negative at -$3,705m. The 5-day average is -$21m, the 20-day average of -$28m and the 100-day average of -$23m.

- Philippines: Recorded inflows of +$6m yesterday, with net outflows of -$36m over the past 5 days. YTD flows are negative at -$562m. The 5-day average is -$7m, the 20-day average of -$16m the 100-day average of -$5m.

Oil Up Again, On Track For Weekly Gain

- WTI is up +0.62% in the Asian trading day at US$75.88 bbl and up +3.6% for the week.

- The rally this month has seen oil shift from being below all major moving averages, with a bearish momentum, to above all major moving averages. The strength of the rally has dragged all moving averages slope upwards, a sign that the bullish momentum could continue.

- Brent is going in the opposite direction, down -1.9% in the Asia trading day yet remains up by over 4% for the week.

- The CEO of Shell warned of a "huge impact" on global trade if the conflict results in the blockage of the key shipping route, the Strait of Hormuz. It is estimated that as much as a quarter of the world's oil trade passes through the Strait that is the passage between the Persian Gulf and the Indian ocean with Iran having history of focusing on ships in those waters. Citibank analysts suggest an obstruction to the passage could see oil at $90 bbl rapidly.

- Already tracking data is showing fewer ships in the straits.

- News abounds in terms of apparent 'approval' for the US to strike Iran but with the time frame remaining uncertain. Oil looks like it could trade sideways waiting for further headlines on the US's next move.

- China's oil refiners are not currently concerned about potential interruptions to Middle Eastern supplies due to the nation's record stockpile of 1.18 billion barrels according to BBG. The high stock buffer, soft refining margins, and seasonal weakness in demand are giving refiners room to maneuver, and they are not in a rush to find alternative sources to Iranian crude.

- Markets are seemingly in a holding pattern waiting for the US's decision on Iran and even gold's safe haven status was not enough for it to deliver a weekly fall.

- Gold is down in the Asian trading day today by -0.45% at US$3,356.50 and thus far is down -2.2% for the week.

- Gold sits atop its 20-day EMA of $3,350.09 and if this technical is broken, the next key level is the 50-day EMA of $3,282.28

- Despite the weekly drop, gold is up +28% this year with market strategists suggesting that up to $3,500 could be the target.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 20/06/2025 | 0600/0700 | *** | Public Sector Finances | |

| 20/06/2025 | 0600/0700 | *** | Retail Sales | |

| 20/06/2025 | 0600/0800 | ** | PPI | |

| 20/06/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 20/06/2025 | - | ECB de Guindos at ECOFIN Meeting | ||

| 20/06/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 20/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 20/06/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 20/06/2025 | 1230/0830 | ** | Retail Trade | |

| 20/06/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 20/06/2025 | 1530/1630 | BOE to announce Q3 APF sales schedule | ||

| 20/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 20/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |