JPY: Asia Wrap - JPY Underperformance In The Crosses, USD/JPY Steady

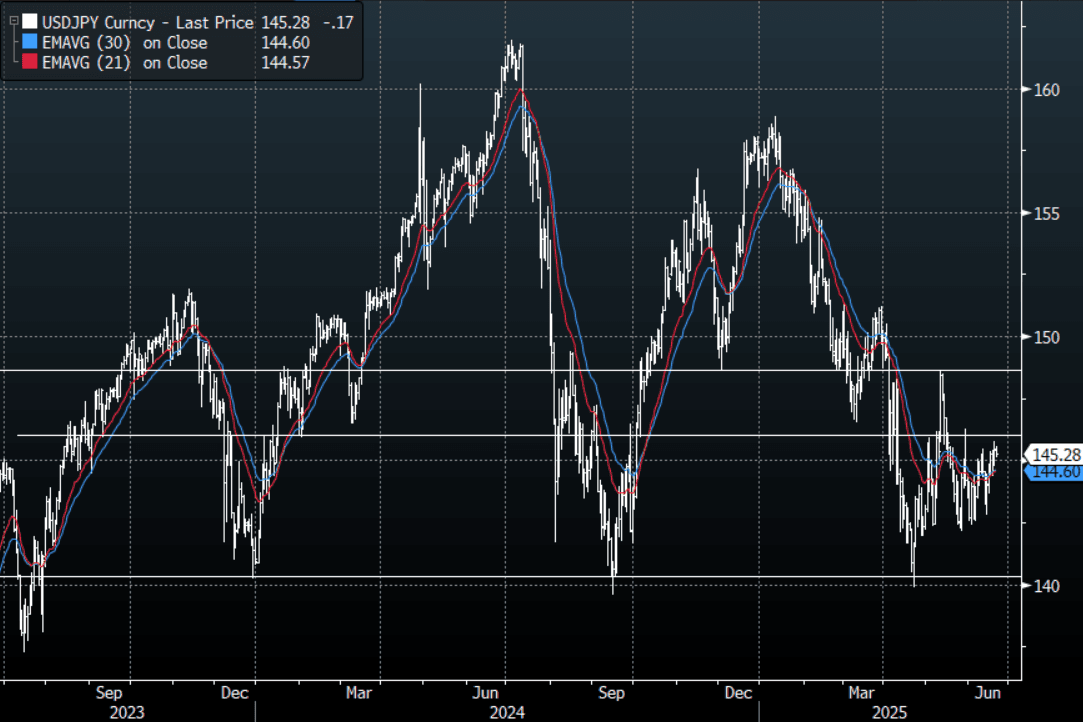

The Asia-Pac USD/JPY range has been 145.12 - 145.56, Asia is currently trading around 145.25, -0.13%. USD/JPY has drifted lower in a muted Asian session, the JPY underperformed in the crosses though as risk bounced back on the hopes the US would not be joining the conflict this weekend. Based on their recent history though it would be unwise to think there is a zero risk of this weekend seeing the US starting to drop bombs in Iran.

- Our Japan policy team noted, "Services prices, a key BOJ focus for assessing the strength of the wage-price cycle, rose 1.4% y/y in May, slightly up from 1.3% in April, but remained below the 2% mark, indicating weak momentum and the need for further gains to achieve the BOJ's inflation target sustainably."

- “JAPAN GOVT MULLS BUILDING STATE-OWNED SHIPYARD, NIKKEI SAYS" - BBG

- "AKAZAWA: JULY 9 IS NOT DEADLINE FOR JAPAN-US TRADE TALKS, TO EXAMINE WHAT KEPT FROM REACHING A TRADE DEAL" - BBG

- USD/JPY price action continues to point to a market that is positioned long JPY.

- Price is back in its recent 142.00 - 146.50 range and will need a break either side of that to get a clearer direction.

- The market believes we could see a decent move lower in USD/JPY but with positioning at extremes we have seen the risk of pullbacks increase. A break above 146.50/147.00 would begin to challenge the conviction of any shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.00($1.92b). Upcoming Close Strikes : 144.50($1.18b June 25)

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: RBA Dated OIS Pricing Much Softer After Yesterday’s RBA Policy Decision

RBA-dated OIS pricing is flat to slightly softer across meetings today as the market continues to digest yesterday’s dovish tilt from the RBA.

- RBA-dated OIS pricing is now 8-20bps softer than yesterday’s pre-RBA levels.

- A 25bp rate cut in July is given a 68% probability, with a cumulative 70bps of easing priced by year-end.

Figure 1: RBA-Dated OIS – Current Vs. Pre-RBA Level

Source: MNI - Market News / Bloomberg

US TSYS: Asia Wrap - Yields Extend Higher

TYM5 has traded higher within a range of 110-00 to 110-10+ during the Asia-Pacific session. It last changed hands at 110-0, down 0-06 from the previous close.

- The US 2-year yield has edged higher, dealing around 3.977%, up 0.01 from its close.

- The US 10-year yield has extended higher, dealing around 4.507%, up 0.02 from its close.

- “Donald Trump is losing patience with demands to raise a draft SALT cap past $30,000, a person familiar said. But some House Republicans still plan to oppose the bill unless their changes are made.”(BBG)

- “There is a clear narrative building on Wednesday in Asia as long-end bond futures extend losses, which is helping to undermine US equity contracts. While it isn’t yet a full repeat of the “Sell America” theme, there is broad weakness developing for the greenback.”(BBG)

- The 10-year found sellers again back towards 4.40% overnight. Asia is having another look back above 4.50% in our session, a sustained break above 4.55/60% needed to see another round of selling targeting the 4.75% area. Support seen back towards 4.35/40%, dips back towards here should see supply emerge once more.

- Data/Events : MBA Mortgage applications, Richmond Fed President Tom Barkin , Fed Governor Michelle Bowman to participate in a “Fed Listens” event

NEW ZEALAND: Business Inflation Expectations Broadly Higher

The RBNZ has released its first official business expectations survey for Q2 2025 after trialling it over H2 2024. It found that inflation expectations rose across time horizons from 1-year to 10-years. Data released last week also showed an increase for Q2. The RBNZ decision is announced on May 28 and it is likely to cut rates 25bp but rising inflation expectations may make its tone more cautious.

- 1-year ahead expected CPI rose to 2.44% from 2.25% in Q1 with the pickup broad-based across business size and sector, while 2-years ahead increased to 2.54% from 2.47% but was less uniform. Both 5-year and 10-year ahead are above the top of the RBNZ’s 1-3% band with the latter now close to 4%.

- The increase in expected inflation was not driven by wages, as 1-year moderated to 2.6% from 2.8% while 2-year was stable at 3.2%.

- 1-year ahead unemployment expectations fell slightly to 5.1% from 5.2% but 2-years rose 0.1pp to 4.9%. The struggling construction sector showed a larger decline than the total over both periods signalling greater optimism re the outlook.

- The survey was taken from April 22 to 30 and was likely impacted by increased global trade uncertainty.