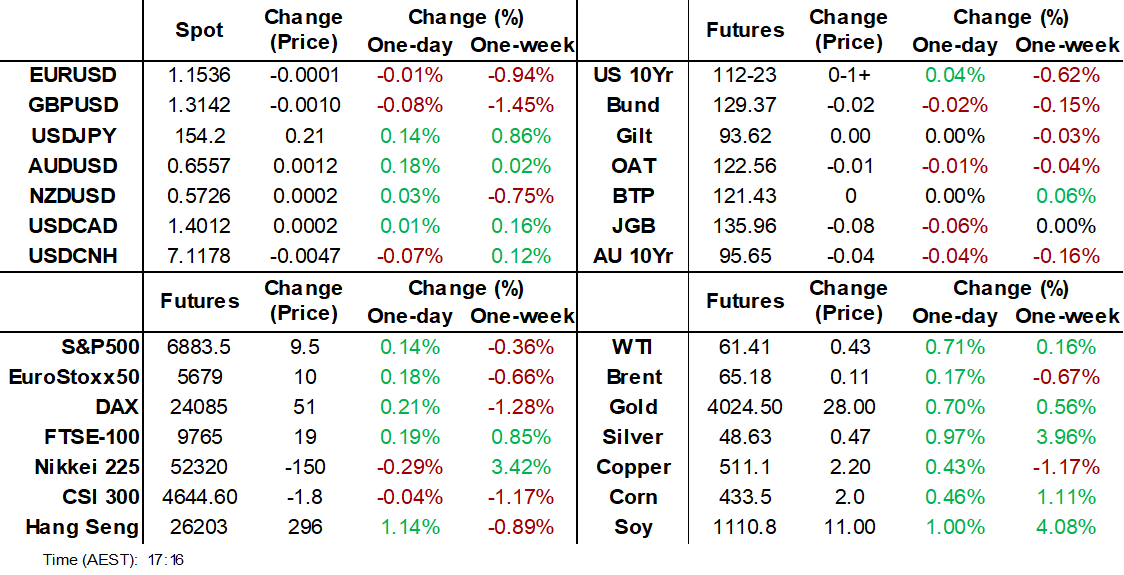

MNI EUROPEAN MARKETS ANALYSIS: Au Pricing Almost No Cut Chance

- News that Nvidia has signed deals with Korean semi conductor companies like Samsung continue to underpin the rally in the KOSPI that is reaching new levels daily, and looking overbought on many valuation metrics.

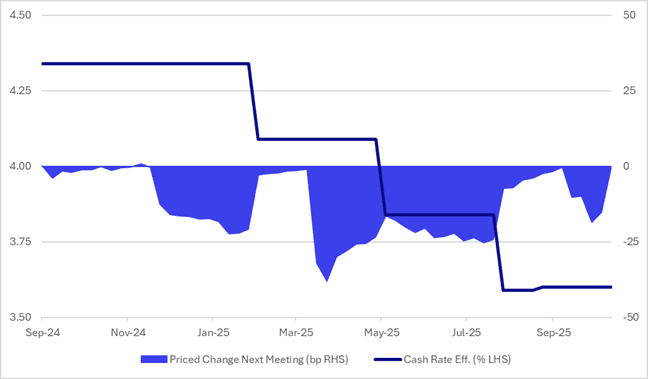

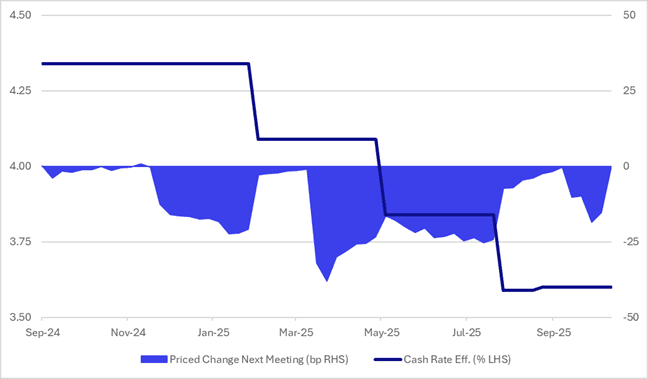

- Going into tomorrow’s RBA policy decision, RBA-dated OIS pricing implies almost no chance of an easing, with just a 2% probability assigned.

- Later the Fed’s Daly and Cook appear with Cook speaking on the economy and monetary policy. The US October manufacturing PMI & ISM data are likely to be watched closely. European October manufacturing PMIs are also released and the ECB’s Lane speaks.

MARKETS

AUSSIE BONDS: Weaker Ahead Of Tomorrow's RBA Policy Decision

ACGBs (YM -5.0 & XM -5.5) are weaker and at or near session lows.

- Tomorrow, the local calendar will see the RBA Policy Decision.

- The Q3 trimmed mean print at 3.0% y/y up from 2.7% and at the top of the 2-3% target band was a “material miss” for the RBA and meant that the Board is now highly likely to leave rates at 3.6% at its 4 November decision.

- The Board is likely to remain highly data-dependent and cautious given inflation’s renewed shift higher and the emerging domestic recovery, but easing labour market conditions. (see MNI RBA Preview here)

- Cash ACGBs are 5bps cheaper.

- The bills strip is -2 to -6 across contracts, with a steepening bias.

- RBA-dated OIS pricing implies almost no chance of an easing, with just a 2% probability assigned. As it currently stands, the OIS market has only an 80% chance of a 25bp cut by mid-2026. (see chart)

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond on Wednesday and A$800mn of the 3.00% 21 November 2033 bond on Friday.

Figure 1: RBA-Dated OIS – Cash Rate Vs. Priced Change Next Meeting

Source: Bloomberg Finance LP / MNI

STIR: Market Gives A RBA Cut Tomorrow No Chance

Going into tomorrow’s RBA policy decision, RBA-dated OIS pricing implies almost no chance of an easing, with just a 2% probability assigned.

- In the wake of the surprise rise in the September unemployment rate to 4.5% in mid-October, markets had briefly priced as much as an 80% probability of a 25bp rate cut in November.

- However, that confidence faded in the lead-up to last week’s Q3 CPI release.

- Compared with previous episodes in this easing cycle, markets appeared noticeably less certain about a November 4 cut ahead of the CPI release.

- That caution proved justified, with the Q3 CPI printing well above expectations.

- As it currently stands, the OIS market has only an 80% chance of a 25bp cut by mid-2026.

Figure 1: RBA-Dated OIS – Cash Rate Vs. Priced Change Next Meeting

Source: Bloomberg Finance LP / MNI

RBA: MNI RBA Preview-November 2025: CPI Outlook Key To Rates

- Download Full Report Here

- The Q3 trimmed mean print at 3.0% y/y up from 2.7% and at the top of the 2-3% target band was a “material miss” for the RBA and meant that the Board is now highly likely to leave rates at 3.6% at its 4 November decision.

- The Board is likely to remain highly data dependent and cautious given inflation’s renewed shift higher and the emerging domestic recovery but easing labour market conditions.

- Updated staff forecasts will be released and the underlying inflation path is likely to be the focus to see how far out the return to the 2.5% band mid-point has been pushed out.

- The Board will need to see inflation resuming its trend lower towards 2.5% before it is likely to consider cutting rates again. Thus, rates are probably on hold in December and the Q4 CPI data on 28 January will be a key input into the 3 February decision.

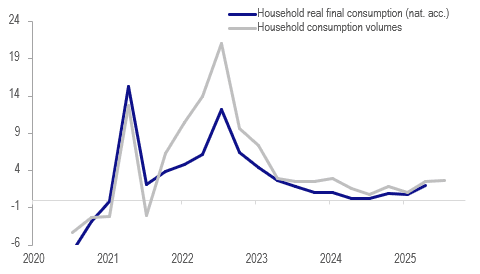

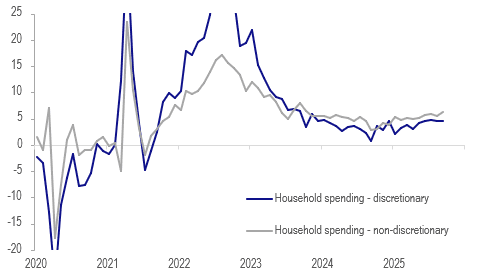

AUSTRALIA DATA: Ex Alcohol & Tobacco, Q3 Consumer Spending Robust

September household spending was softer than expected rising 0.2% m/m to be up 5.1% y/y after a downwardly-revised 4.9% y/y. Q3 consumption volumes rose 0.2% q/q, the lowest rate since Q3 2024 but the fifth consecutive quarterly rise. Growth continued to recover rising 2.7% y/y, the highest since Q1 2024 but pressured by contracting alcohol & tobacco expenditure. The data point to a continued gradual recovery in private consumption. While the RBA is widely expected to be on hold this week, its consumption forecasts will be monitored for upward revisions.

Australia real household consumption y/y%

Source: MNI - Market News/ABS

- In September, the RBA was uncertain if “households have become more comfortable consuming as real incomes and wealth rise”. The Q3 data are consistent with a consumer recovery and excluding alcohol & tobacco (-6.8% q/q) were a lot stronger than the headline.

- There was strong real consumption of food (+1.1% q/q), clothing & footwear (+0.8%), health (+1.8%) and miscellaneous goods & services (+1.2%). Recreation fell 0.5% q/q following strong growth in the previous three quarters and transport was flat. Household items rose 0.4% q/q, the fourth straight positive quarter.

- September nominal spending was driven by essential items, suggesting that consumers were reluctant to spend on discretionary items, especially if discounts aren’t offered. Non-discretionary rose 0.6% m/m to be up 6.2% y/y after 5.6% in August, whereas discretionary was flat to be steady at 4.5% y/y.

- Services spending was flat in September after rising solidly earlier in the quarter. It is now up 7.2% y/y down from 7.9% y/y. However, goods expenditure rose 0.4% m/m to be up 3.4% y/y after 2.4%.

Australia household consumption values y/y%

Source: MNI - Market News/ABS

BONDS: NZGBS: Modest Bear-Steepener After A Subdued Session Of Trading

NZGBs closed showing a modest bear-steepener, with yields 1-3bps higher.

- The session was relatively subdued, with no cash US tsys trading due to the Japanese market being closed.

- The key event in NZ this week is the Q3 labour market and wages data released on Wednesday. Filled jobs for the quarter signal a stabilization, but employment is likely to have remained weak, with consensus forecasting it to rise only 0.1% q/q to be still down 0.2% y/y. The unemployment rate is expected to rise 0.1pp to 5.3%, in line with the RBNZ's August projections. Soft labour demand is likely to weigh on private wage growth, which is forecast to rise around 0.4% q/q after 0.6%.

- “The RBNZ said that the results of its 2025 bank stress tests showed that large banks are well placed to withstand and manage the impact of heightened geopolitical risks, according to a Monday statement.” - MTN

- RBNZ dated OIS pricing is little changed across meetings. 23bps of easing is priced for November, with a cumulative 30bps by February 2026.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 5.00% May-54 bond.

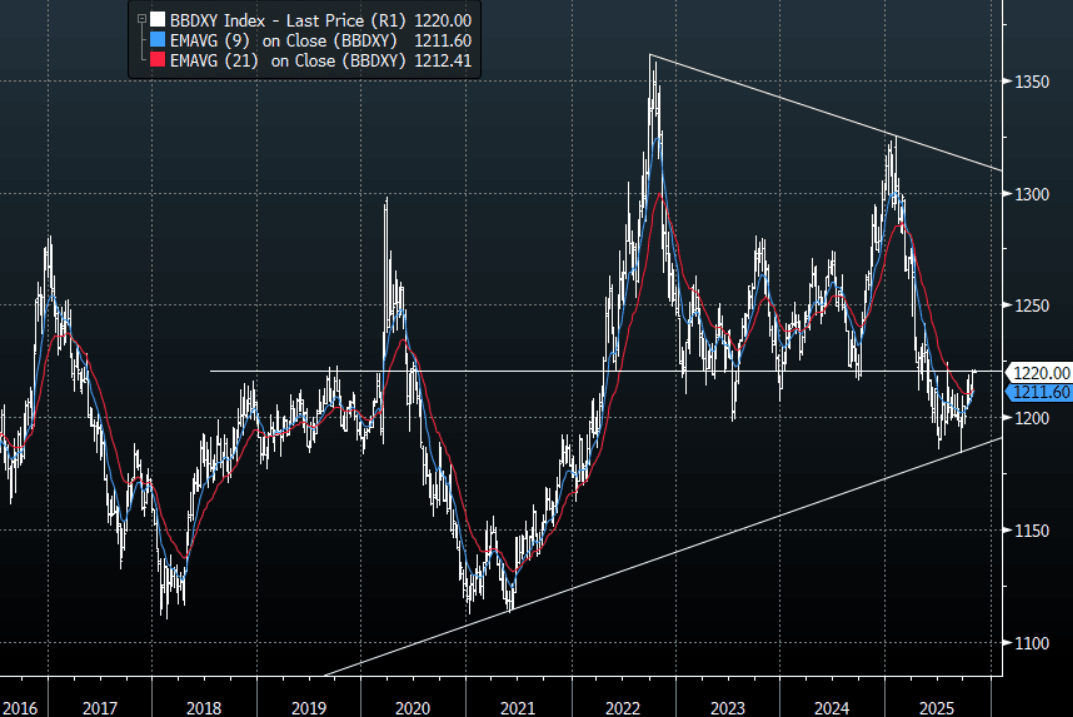

FOREX: Asia-Pac FX - BBDXY Moves Into Pivotal Resistance

The BBDXY has had a range of 1220.25 - 1221.11 in the Asia-Pac session; it is currently trading around 1220, -0.05%. The USD built on its gains from last week into the month-end. The 1220-30 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the longer-term USD shorts. Risk/Reward does still favour fading this moving initially but the price action is starting to look more constructive as higher lows are being made on the Daily chart through October. A sustained move back above 1230 would potentially signal a medium term low is in place and a deeper pullback is on the cards.

- EUR/USD - Asian range 1.1522 - 1.1538, Asia is currently trading 1.1530. The pair has moved back toward its support just above 1.1500. A break under this support could signal a deeper correction, first target 1.1400 and then the 1.1100/1.1200 area.

- GBP/USD - Asian range 1.3130 - 1.3142, Asia is currently dealing around 1.3140. The pair looks to be building some downward momentum. This 1.3100/1.3150 area has proved to be supportive on more than 1 occasion this year so some work around this level could be expected. I continue to favor fading rallies though as GBP attempts to put in a medium term top.

- USD/CNH - Asian range 7.1178 - 7.1249, the USD/CNY fix printed at 7.0867, Asia is currently dealing around 7.1190. The support below 7.1000 looks to be pretty solid for now as USD/Asia moves in sympathy with a higher USD/JPY. The range of 7.08-7.16 looks set to continue for now.

- Cross asset : SPX +0.15%, Gold $4007, US 10-Year 4.0775%, BBDXY 1220, Crude Oil $61.18

- Data/Events : Italy HCOB Italy Manufacturing PMI/Budget Balance, Germany HCOB Germany Manufacturing PMI, EZ HCOB Eurozone Manufacturing PMI, France HCOB France Manufacturing PMI, Spain HCOB Spain Manufacturing PMI

Fig 1: BBDXY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

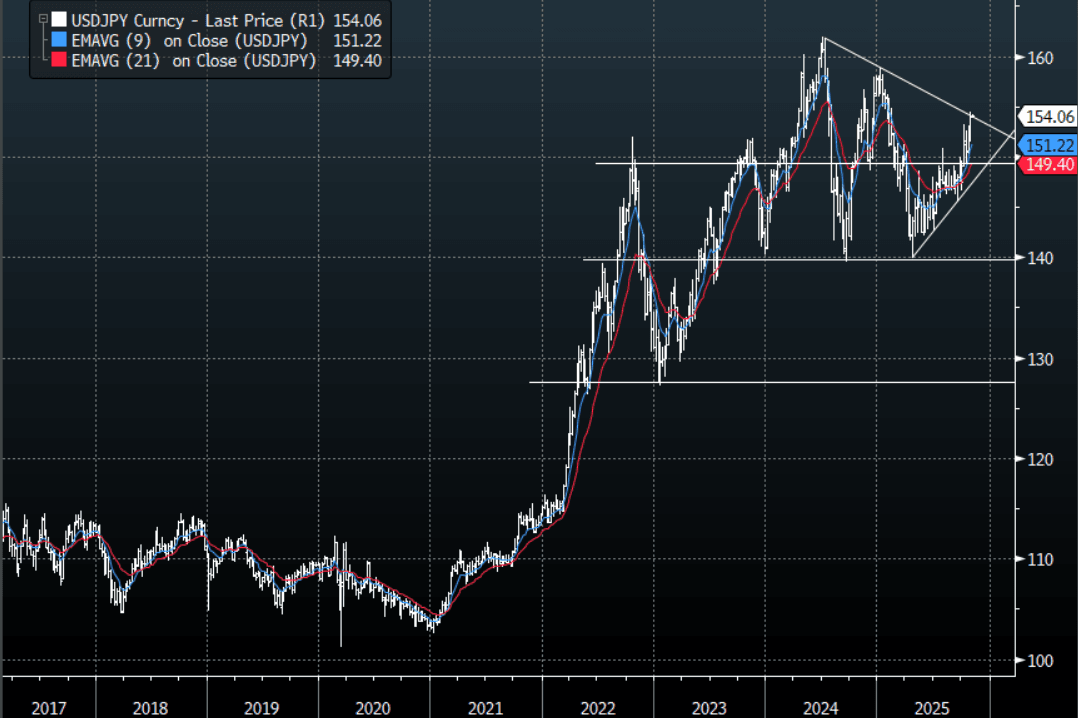

JPY: Asia-Pac - USD/JPY Consolidates Around 154.00

The USD/JPY range has been 154.00 - 154.25 in the Asia-Pac session, it is currently trading around 154.10, -0.05%. The pair remains well supported thanks to a combination of a hawkish FED and a BOJ that is still unsure about when it will raise rates. We are approaching some resistance back toward the 154/155 area and I would expect we might to do some work around here initially. I also suspect any sustained break back above 155 could see the move begin to accelerate and with that the potential for further intervention, though personally I think they will wait for levels closer to 160 to get involved. Look for dips to continue to be supported while above 149-150.

- Options : Close significant option expiries for NY cut, based on DTCC data: 152.50($1.42b). Upcoming Close Strikes : 150.00($1.13b Nov 3) - BBG.

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

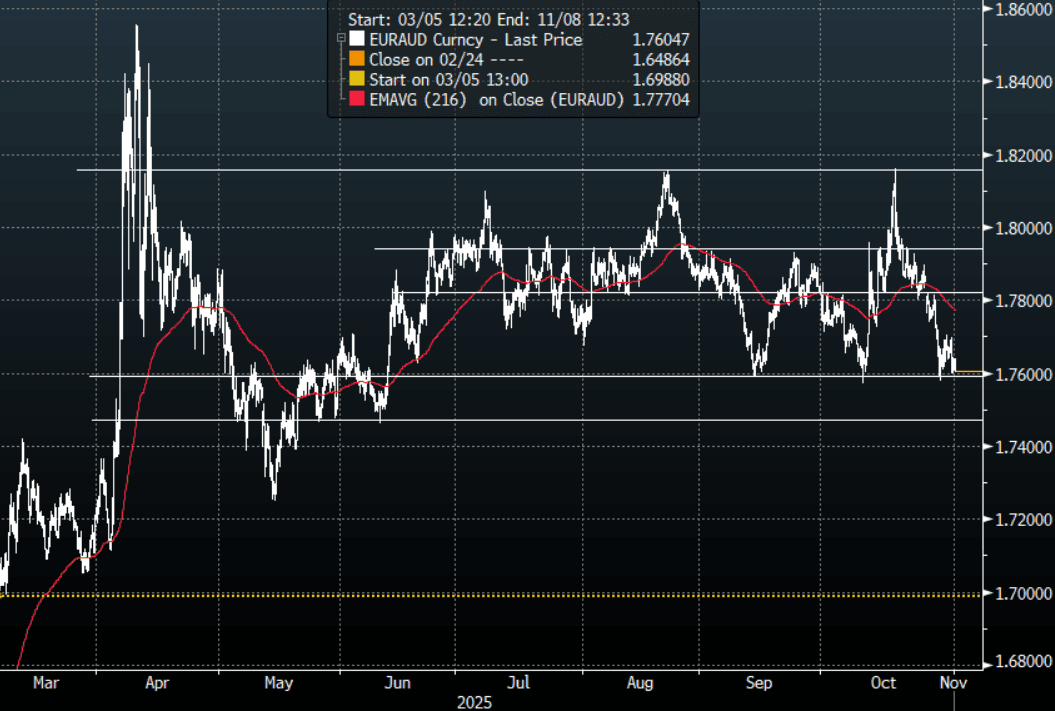

AUD: Asia-Pac - AUD/USD Consolidates Around 0.6550 In A Quiet Session

The AUD/USD has had a range of 0.6539 - 0.6551 in the Asia- Pac session, it is currently trading around 0.6545, +0.03%. US yields retraced on Friday night but the USD continues to grind higher challenging levels last seen in July/August. The AUD/USD is back within its recent 0.6400-0.6650 range with the pivot being around 0.6500-0.6550 where I would expect some demand first up, RBA tomorrow but the market is not expecting them to move.

- Ex Alcohol & Tobacco, Q3 Consumer Spending Robust: September household spending was softer than expected rising 0.2% m/m to be up 5.1% y/y after a downwardly-revised 4.9% y/y. Q3 consumption volumes rose 0.2% q/q, the lowest rate since Q3 2024 but the fifth consecutive quarterly rise. Growth continued to recover rising 2.7% y/y, the highest since Q1 2024 but pressured by contracting alcohol & tobacco expenditure. The data point to a continued gradual recovery in private consumption. While the RBA is widely expected to be on hold this week, its consumption forecasts will be monitored for upward revisions.

- Bloomberg is reporting that “Pimco is betting on a rebound in Australian government bonds on expectations the RBA will resume easing next year, favoring the five- to 10-year part of the yield curve.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD 338m). Upcoming Close Strikes : 0.6625(AUD944m Nov 4), 0.6300(AUD600m Nov 4) - BBG

- EUR/AUD - Asia-Pac range 1.7602 - 1.7638, Asia is currently trading around 1.7605. The pair topped out again around 1.7700 and is once again testing the support in the 1.75-1.76 area. I suspect rallies toward 1.7700/1.7800 would now be faded but a break under the 1.7500 area is needed to signal a potential deeper pullback toward the 1.7000 area.

Fig 1: EUR/AUD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia-Pac - NZD/USD Finds Support Towards 0.5700

The NZD/USD had a range of 0.5713 - 0.5727 in the Asia-Pac session, going into the London open trading around 0.5725, +0.05%. US yields retraced on Friday night but the USD continues to grind higher challenging levels last seen in July/August. The NZD found some demand back toward 0.5700 and consolidated in a tight range over month-end. While price remains below the 0.5800/50 area I suspect rallies continue to be faded looking for a potential move back towards the 0.5500/0.5600 area. NZD continues to stand out as a short against a resurgent USD but it is worth noting that because of the size of the market the market can very quickly become all positioned the same way, so I think the USD will need to build on its challenge higher for the NZD to test those lows.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5650(NZD1.1b Nov 5), 0.5675(NZD1b Nov 5), 0.5750(NZD604m Nov 5) - BBG

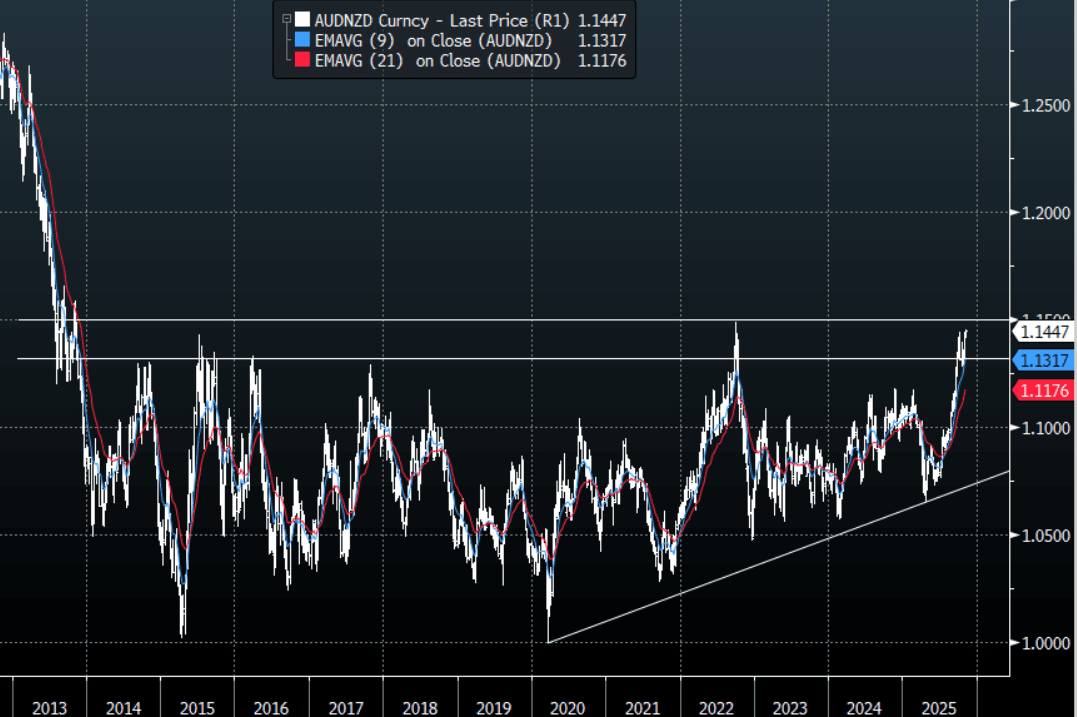

- AUD/NZD range for the session has been 1.1423 - 1.1453, currently trading around 1.1445. The Cross has bounced hard after finding solid demand back toward 1.1300. This 1.1400/1.1500 area remains tough resistance but the price action suggests the market wants to test it. Above 1.15/16 and the markets focus will start to turn toward 1.2000 and beyond.

Fig 1: AUD/NZD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: KOSP Hits New Highs on Tech Rush

News that Nvidia has signed deals with Korean semi conductor companies like Samsung continue to underpin the rally in the KOSPI that is reaching new levels daily, and looking overbought on many valuation metrics. The rally now is the strongest in more than 20 years as Asia and particularly Korea position themselves in the global tech race. In China, gold related stocks were hit after a tax rebate on gold was ended by the government and could potentially increase costs. With Japan out, it was down to China to lead and despite the KOSPI's rally, China stocks were mixed on the day.

- The Hang Seng and CSI 300 were again going in opposite direction with the HSI up +0.58% and the CSI 300 down -0.45% whilst the Shanghai Comp was close to flat, whilst Shenzhen fell -0.61%

- The KOSPI hit 4,202 to be up +2.25% today to continue its run, now up over 70% YTD.

- The FTSE Malay KLCI has had a quiet period but is up today by +0.58% whilst the JCI in Indonesia is having its best start to a trading week in a fortnight with gains of +1.10%

- The NIFTY 50 posted new highs last week, before fading back and has started the week slowly flat at 25,727.

OIL: Crude Post-OPEC Gains Unwinding As Excess Supply Remains A Concern

Oil prices rose moderately when the APAC session started today following OPEC’s decision to increase output in December by 137kbd, in line with November, but announced it would pause production rises through Q1, which is a time of lower demand. It has been increasing quotas to regain market share but a jump in both non-OPEC and OPEC output is driving excess supply with a record surplus forecast for 2026.

- WTI reached a high of $61.48/bbl early in the session and has trended lower since and is currently +0.2% to around $61.12, close to the intraday low. Initial support is at $59.64. Brent rose to $65.26/bbl to start with and then fell to a trough of $64.89, above support at $63.37. It is currently up 0.3% to $64.95.

- It appears that the latest US/EU sanctions targeting Russian oil majors Rosneft and Lukoil are having an impact with reports that refiners in China are looking to alternatives. Bloomberg reports that around 400kbd are impacted or around 45% of China’s Russian oil imports, which is pressuring prices for Russian grades.

- Morgan Stanley has lifted its Brent forecast $2.50 to $60/bbl for Q1, as OPEC decides to leave production targets unchanged over Jan-Mar, according to Bloomberg.

- Later the Fed’s Daly and Cook appear with Cook speaking on the economy and monetary policy. With US data still scarce due to the government lockdown, the October manufacturing PMI & ISM data are likely to be watched closely. European October manufacturing PMIs are also released and the ECB’s Lane speaks.

GOLD: Softer USD Helps Gold Recover From China VAT Change Losses

Gold prices dipped to $3962.59/oz early in the APAC session driven by news that China was removing the retail tax exemption on gold but they have since recovered to make a high of $4015.42 supported by a weaker US dollar (BBDXY -0.1%). They are currently up 0.1% to $4005.5.

- China’s retailers will no longer be able to offset VAT on gold sales including bars and jewellery, which is likely to reduce demand through higher prices. The main impact is likely to be on sentiment which has contributed to gold’s major rally in 2025, according to Bloomberg.

- Silver is 0.2% higher at $48.80, close to the intraday peak at $48.911 but holding below initial resistance at $49.456.

- Equities are generally stronger with the S&P e-mini up 0.2% and Hang Seng +0.6%. Oil prices are higher with WTI +0.4% to $61.19/bbl. Copper is flat.

- Later the Fed’s Daly and Cook appear with Cook speaking on the economy and monetary policy. With US data still scarce due to the government lockdown, the October manufacturing PMI & ISM data are likely to be watched closely. European October manufacturing PMIs are also released and the ECB’s Lane speaks.

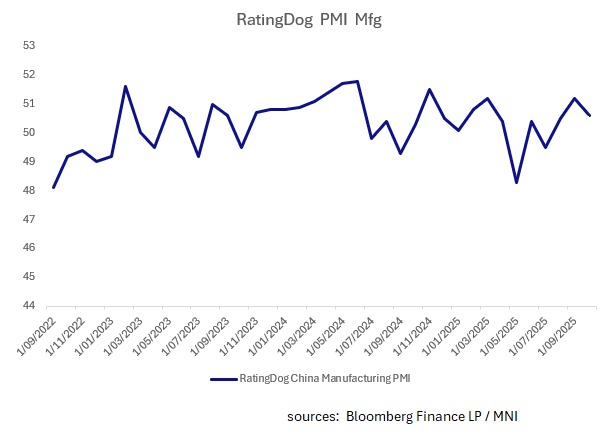

CHINA: Rating Dog Manufacturing PMI Moderates

- The September expansion of the RatingDog PMI manufacturing seemed to reflect a period of expansion ahead of the Xi Trump meeting.

- Whilst today's release for the October data will not capture the impact of the meeting, it is more reflective of the type of expansion that is occurring we think.

- Up +50.6 in October it is a significant decline from the +51.2 in September, but importantly is the third month in a row of expansion.

- Output declined to +50.8 from 52.0 and new orders declined from the month prior.

INDONESIA: October Inflation Higher But Well Contained In Band

Indonesia inflation was higher than expected in October and above September’s prints. Headline rose to 2.9% from 2.7% and core to 2.4% from 2.2% - still around Bank Indonesia’s 2.5% corridor mid-point. It continues to expect inflation this year and next to remain in its band as inflation expectations are anchored and softer domestic demand is likely to weigh on core. With its pro-growth stance and the economy slowing, the October increase in inflation is unlikely to prevent further rate cuts in coming months.

- While food and drink inflation remains elevated, it was stable at 5% y/y but volatile food rose 6.6% y/y from 6.4%. It was the pickup in personal care & others to 11.9% from 9.6% and transportation to +0.5% from -0.2% though that drove the increase in inflation rates. Most other categories were fairly stable.

- Headline inflation was its highest since April 2024 but it has been boosted by base effects following the expiry of temporary electricity price cuts, which is likely to be the case into Q1 2026.

Indonesia CPI y/y%

Source: MNI - Market News/LSEG

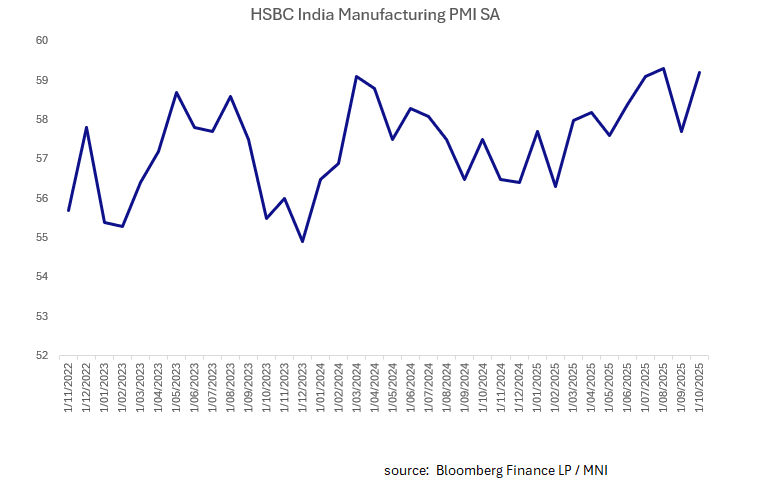

INDIA: PMI Manufacturing Back Near Recent Highs

- The final HSBC India Manufacturing PMI saw a strong improvement on the month prior, re-affirming that the manufacturing sector appears to not be hurting by US sanctions or various threats.

- India's PMIs have consistently outperformed regional peers for some time and with a moderation in September, questions were asked whether this could be the sign of things to come.

- The final result of +59.2 was marginally below the high of August of +59.3

- Output was very strong at +63.7 from 61.1 in September and new orders were higher.

- Indian markets have priced out a rate cut over the next month but continue to factor in rate cuts over the coming three months. Economic data continues to be robust at a time when ongoing weakness in the Rupee poses a threat to the forecasts on rate cuts, with the possibility that those assumptions could be priced out over time.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 03/11/2025 | 0700/0200 | * | Turkey CPI | |

| 03/11/2025 | 0730/0830 | *** | CPI | |

| 03/11/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 03/11/2025 | 0845/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 03/11/2025 | 0850/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 03/11/2025 | 0855/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 03/11/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 03/11/2025 | 0930/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 03/11/2025 | 1200/1300 | ECB Lane Lecture In Dublin | ||

| 03/11/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/11/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (final) | |

| 03/11/2025 | 1500/1000 | *** | ISM Manufacturing Index | |

| 03/11/2025 | 1500/1000 | * | Construction Spending | |

| 03/11/2025 | 1500/1000 | * | Construction Spending | |

| 03/11/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 03/11/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 03/11/2025 | 1700/1200 | San Francisco Fed's Mary Daly | ||

| 03/11/2025 | 1830/1330 | BOC Governor fireside chat at The Logic conference | ||

| 03/11/2025 | 1900/1400 | Federal Reserve Governor Lisa Cook | ||

| 04/11/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 04/11/2025 | 0330/1430 | *** | RBA Rate Decision | |

| 04/11/2025 | 0740/0840 | ECB Lagarde Keynote Speech At Bulgarian National Bank | ||

| 04/11/2025 | 0745/0845 | Budget Balance | ||

| 04/11/2025 | 0945/1045 | ECB Lagarde At Bulgarian National Bank Press Conference | ||

| 04/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 04/11/2025 | 1135/0635 | Fed Vice Chair Michelle Bowman | ||

| 04/11/2025 | 1140/1140 | BOE Breeden at International Banking Conference | ||

| 04/11/2025 | 1330/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 04/11/2025 | 1330/0830 | ** | Trade Balance | |

| 04/11/2025 | 1330/0830 | ** | Trade Balance | |

| 04/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index |