MNI EUROPEAN MARKETS ANALYSIS: A$ Challenging Friday Lows

- Risk appetite has weakened amid fresh US-China tensions. China announced curbs on US shipping entities via Hanwha Ocean, a large South Korean shipbuilder. The authorities also provided details on a broader probe into the impact of the US investigation into China shipping.

- Equities are softer, likewise bond yields, while AUD/USD is challenging Friday lows in the FX space. Gold and silver continue to outperform.

- Later Fed Chair Powell speaks on the economic outlook and monetary policy. The Fed’s Bowman, Waller and Collins, ECB’s Machado, Cipollone and Donnery, and BoE’s Bailey and Taylor also appear. US September NFIB small business optimism prints.

MARKETS

US TSYS: Move Higher in Yields Stalls in the Afternoon

- As treasuries began trading in the Asia trading day, yields across the curve opened 1-3bps higher before taking back some of the early moves.

- The US 2-Yr traded up at 3.515%, but rallied back to again test a near term support of 3.50% that it has been unable to hold below.

- The US 5-Yr is back to flat at 3.63% having been +2bps higher in the morning session.

- The US 10-Yr is up +1bps to 4.04%, having opened at 4.06%. Last week it failed to test 4.00% and looks likely to remain in the 4.00% - 4.20% range for now, seeking a fresh catalyst to break out. With FED speakers in coming days and the FEDs Powell's economic address at the NABE meeting, treasury traders will be looking for signals for monetary policy that could challenge this current range.

- The US 30-Yr is up +2bps at 4.64% just off the Tuesday morning high of 4.65%.

- Futures are edging lower too as TYZ5 is has not traded too far from where it started the day and is currently +01 at 113-06

JGBS: Futures Bid On Risk Aversion, But Sub Resistance, Tamaki PM Odds Firm

Like elsewhere, JGB futures have caught a bid as fresh US-China tensions (this time centered on the shipping sector), drive safe haven flows into bonds. The 10yr future was last 136.39, +.49, versus settlement levels. Key short-term resistance has been defined at 137.30, the Sep 8 high, so we are still some distance away but this bounce is challenging the recent bearish break of 136.19, the Sep 4 low.

- The China announcement targets US shipping entities via Hanwha Ocean, a large South Korean shipbuilder. The authorities also provided details on a broader probe into the impact of the US investigation into China shipping (mkt jitters with be heightened given the potential for escalation from here).

- In the cash JGB yield space, shifts lower have accelerated, led by the 7yr down 5bps. to 1.41%. The 10yr is back to 1.66%, while the 30 and 40yr tenors are holding around 2bps higher.

- The 2/30s curve is maintaining a steepening bias, last +234bps, +5.5bps.

- The other focus point remains domestic politics. "*TAMAKI: WILL HOLD 3-WAY DPP, ISHIN, CDP SEC-GEN MEETING TODAY" (via BBG). There is a possibility of former LDP coalition partner Komeito backing a non-LDP candidate for PM (based off comments yesterday). Tamaki's, the leader of the DPP, PM odds have risen to +17.5, per Polymarket. Note earlier this year Tamaki "urged the BOJ to loosen, not tighten, monetary policy to keep the yen from rising and hurting the export-reliant economy." (via Asahi).

- Note tomorrow has a 20yr debt auction.

AUSSIE BONDS: Futures Bid Fresh On US-China Tensions, AU-US 10yr Spread Lower

Futures have caught an afternoon bid amid renewed risk aversion centred on US-China tensions. 10yr futures (XM) were last +4bps to 95.73, while 3yr (YM) were at 96.505, +3bps. Upside focus will rest on Sep 12 highs, 95.78 for the 10yr and 96.615 for the 3yr. Broader risk aversion is higher, as China imposed curbs on the US units of Hanwha Ocean, a large South Korean shipbuilder. It also provided details on a broader probe into the impact of the US investigation into China shipping).

- AUD/USD is the weakest performed in the FX space, and will remain quite sensitive to US-China related developments, particularly from a proxy/risk standpoint.

- ACGB yields are lower across the board, off 2-3.5bps. As we noted yesterday, fresh US-China tensions, with no off ramp, could bring RBA easings back to play if it impacts the global/China growth outlook enough.

- The AU-US 10 spread is off recent highs, last +22bps (from +33bps on Friday).

- Earlier, the September NAB business survey showed the gradual recovery in the Australian economy continued. While, the RBA minutes clearly reflected the Board’s caution at the 30 September decision to keep rates unchanged. Its “decisions”, ie. not just last month’s, “remain cautious and data dependent”. Thus the outcomes of releases between now and 4 November are very important and the tone of the minutes was clear that a rate cut at that meeting is not a given.

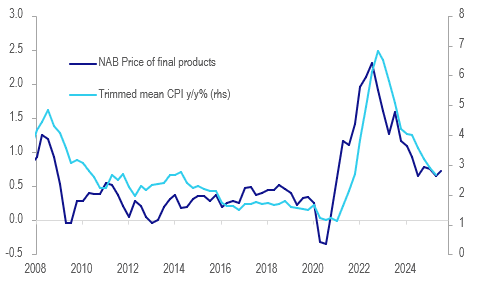

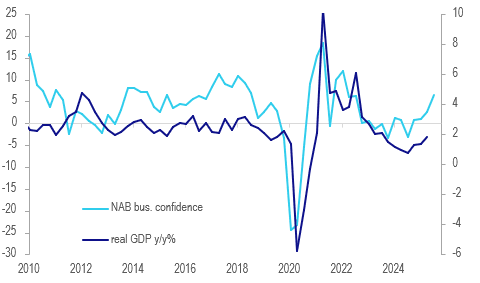

AUSTRALIA DATA: NAB Survey Shows Recovery Continued & Inflation Stable In Q3

The September NAB business survey showed the gradual recovery in the Australian economy continued. Business confidence rose to 7.3 from 4.3 while conditions were similar to August at 7.6. The Q3 averages though were their highest since Q1 2022 and Q2 2024 respectively, suggesting stronger Q3 GDP growth. While the price/cost components were a bit higher in September, they were little changed in Q3 signalling steady inflation. The data are consistent with activity picking up and concerns that disinflation has stalled, and so with the RBA remaining cautious.

Australia NAB business prices vs trimmed mean CPI %

- Given the volatility amongst some of the components of the monthly NAB survey, it is worth looking at Q3 averages to gauge the recovery and inflation picture in the quarter. Its measure of labour demand fell over 2 points to 2.9 in September but the Q3 average was stable at 3.5 consistent with the RBA’s assessment that labour market conditions are “broadly stable”. September jobs print Thursday and a 0.1pp rise in the unemployment rate to 4.3% is forecast.

- The increase in September business conditions was driven by a pickup in trading to 16.0, its highest since November 2023, and profitability to 5.9, best in almost 18 months. However, forward orders declined to -2.3 from +1.1 but while still weak in Q3 improved one point to -0.5.

- Average Q3 labour cost growth was steady at 1.6% 3m/3m while purchase costs moderated 0.1pp to 1.4% (it has held around 1.5% for 6 consecutive quarters). Final product prices rose 0.7% 3m/3m, in line with 2025 average, while retail prices increased 0.8% down from Q2’s 1.0%, lowest since Covid-impacted Q4 2020. Cost, retail and final product price growth rose in September while labour costs fell 0.1pp.

Australia NAB business confidence vs GDP y/y%

Source: MNI - Market News/LSEG

RBA: Minutes Reflect More Caution Than Downside Concerns, Nov Hold Plausible

The RBA minutes clearly reflected the Board’s caution at the 30 September decision to keep rates unchanged. Its “decisions”, ie. not just last month’s, “remain cautious and data dependent”. Thus the outcomes of releases between now and 4 November are very important and the tone of the minutes was clear that a rate cut at that meeting is not a given. Today’s September NAB business survey was consistent with an ongoing recovery in activity.

- There were a number of observations that suggest the Board may hold again. It noted that “early indicators” for Q3 showed private demand could be recovering a bit faster than expected, so not just the backward-looking Q2 GDP data, and that it may have underestimated consumption growth in August. Also on growth, the US is “steady” and the risk from “higher tariffs” has “diminished”, while fiscal policy should support a weaker China.

- Not only do the July/August CPI outcomes suggest Q3 inflation may be higher than the RBA expected in August but that combined with “broadly stable labour market conditions” may imply that it underestimated the extent of capacity pressures. As Governor Bullock noted, elevated services in other countries may have “potential lessons for Australia” too.

- Monetary policy is deemed “restrictive” but the RBA doesn’t know by how much. It is seeing the impact of previous easing on housing and credit growth and it knows that it hasn’t fully fed through. It seems to be slightly uncomfortable with the current effect of easier financial conditions.

- There was little discussion of downside risks with the only consideration in the minutes that staff projections “were not taking sufficient signal” from “persistent weakness in consumer sentiment”, softer employment and “timely indicators of wages”.

- Key data coming up include 29 October Q3 CPI, 16 October September jobs, 31 October September private credit and 3 November September household spending.

BONDS: NZGBS: Softer Yields, Sep Card Spend Down, RBNZ Eases LVR

NZGB yields have held modestly softer across most of the benchmarks as Tuesday's session unfolded. Outside of a steady 2yr at 2.60%, most other parts of the curve are close to 1bps (although the 10yr is little changed at 4.075%). This comes despite US Tsys resuming cash trading with a firmer bias, this has faded as the session progressed, with fresh China shipping curbs on the US weighing on risk appetite (10yr back under 4.04%). Earlier data showed card transactions falling in Sep, while the RBNZ adjusted loan regulations (essentially easing NZ financial conditions), helping relative NZ yield trends.

- The NZ-US 10yr rate differential is slightly lower, last at +5bps, up a touch from recent lows sub 0bps. So far in Oct, this spread hasn't been able to sustain +10bps levels.

- New Zealand 2yr swap is near 2.37%, little changed for the session, but still close to recent lows near 2.35% and maintaining a downtrend bias.

- September retail card transactions fell 0.5% m/m after rising 0.6%, the first negative after three consecutive increases. Annual growth slowed to 1.2%. Despite the soft end to Q3, the quarter saw a 0.6% q/q increase in nominal retail spending.

- The Reserve Bank of New Zealand will ease mortgage loan-to-value ratio (LVR) restrictions from Dec 1, increasing the share of new lending allowed at higher LVRs, the central bank said in a statement Tuesday. For owner-occupiers, the limit on loans with an LVR above 80% will rise to 25% from 20%, while for investors, the limit on loans with an LVR above 70% will increase to 10% from 5%.

- Looking ahead, Thursday delivers Sep food prices, ahead of the all important Q3 CPI, out next Monday.

FOREX: AUD/USD Testing Friday Lows Amid Fresh US-China Tensions

Higher beta FX, most notably AUD, has underperformed in the Asia Pac afternoon session, particularly against yen. AUD/USD is at 0.6475/80, down 0.60%, and challenging lows from late Friday (when Trump announced a fresh tariff threat against China). NZD/USD is near 0.5700, which is fresh multi month lows. USD/JPY is back under 152.00, against earlier highs of 152.61. Risk aversion has returned after The China announcement targets US shipping entities via Hanwha Ocean, a large South Korean shipbuilder. The authorities also provided details on a broader probe into the impact of the US investigation into China shipping.

- US equity futures are lower, off 0.35% for Eminis, while Bitcoin losses sit close to 2% for the session. Bond markets have seen a safe haven bid. Sentiment has been whipsawed after more positive comments from the US over the week and yesterday (while China tried to play down its rare earth export controls) aided a risk rebound on Monday.

- For AUD/USD, it is likely to remain particularly sensitive to US-China developments. Today's softness undermines the recent bullish theme and instead signals scope for a deeper retracement, potentially towards key support at 0.6415, the Aug 21 and 22 low. Initial resistance to watch is 0.6560, the 50-day EMA.

- AUD/JPY is back close to 95.40, still above Friday lows sub 98.00.

- For NZD/USD we haven't been sub 0.5700 since April of this year.

- USD/JPY has also been aided by further jawboning from FinMin Kato, although it didn't appear to represent a step up on recent FX rhetoric. Japan politics remains in focus as minor parties meet to potentially put forward a candidate for PM.

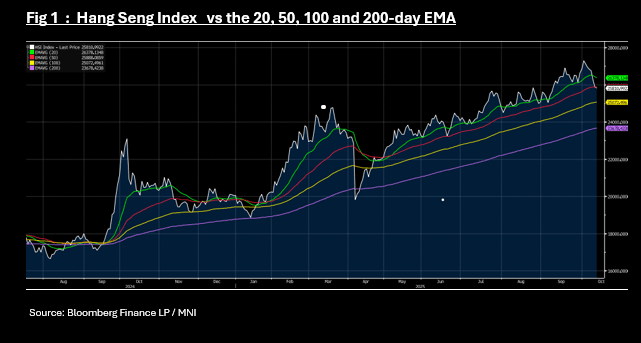

ASIA STOCKS: Equities Remain Weak as HSI Breaks Through Key Technical

With Japan back today playing catch up from yesterday's weakness, most key markets in the region have moved lower Tuesday. This comes despite the better global risk tones on Monday, as Trump softened his language around China (after tariff threats late on Friday).

Having closed at new highs Thursday, the NIKKEI's falls started Friday on apparent profit taking which was then over ran by Trump's comments as risk appetite declined. Out yesterday for a public holiday, Japanese investors continued to sell today taking the NIKKEI lower by -1.30%.

In Hong Kong the Hang Seng fell -0.45% today, despite trying to open stronger and traded through the 50-day EMA of 25,886. Were the HSI to hold below the 50-day EMA it would be the first time since the trade war induced sell off from April which then resulted in a near on five month rally to new highs. Other key Chinese bourses did little holding near to opening levels.

The KOSPI was a regional exception jumping +0.50% today as the 19% constituent - Samsung - beat profit estimates for its most recent quarter and its biggest quarterly profit in three years.

Following a terrible end to September for the NIFTY 50, it has rallied seven out of nine trading days in October. Against the regionally weak backdrop yesterday, the NIFTY 50's fall of -0.23% was a relative outperformance and in opening trade Tuesday it has recovered yesterday's falls.

OIL: Crude Range Trading As Watching US-China & Supply/Demand Developments

Oil prices are slightly higher but have been trading within a narrow range during today’s APAC session with no new developments to give it direction. Later on Tuesday though, the IEA’s October report, US industry-based inventory data and Fed Chair Powell comments on the economy have the potential to move crude. Brent is up 0.4% to $63.56/bbl off the intraday low of $63.41 following a peak of $63.63. WTI is 0.4% higher at $59.72/bbl after reaching $59.82. The USD index is slightly lower.

- OPEC left its oil market outlook unchanged with demand forecast to rise by 1.3mbd in 2025 and 1.4mbd in 2026. The IEA releases its monthly report Tuesday and tends to be less optimistic than OPEC. It has been projecting a record market surplus for 2026.

- US-China working-level trade talks occurred on Monday and China reiterated today its right to control rare earth exports and that the US should negotiate. Oil is likely to sell off if there is any deterioration in the situation as it remains concerned about the impact on energy demand from increased protectionism.

- Later Fed Chair Powell speaks on the economic outlook and monetary policy. The Fed’s Bowman, Waller and Collins, ECB’s Machado, Cipollone and Donnery, and BoE’s Bailey and Taylor also appear. US September NFIB small business optimism, UK labour market data and German September HICP and euro area October ZEW print.

Gold Continues Rally Without New Drivers

Gold has continued to rally today despite a flat US dollar, 2-year yields and S&P e-mini as it appears to be carried by momentum with no new fresh catalysts. It is now up 7.8% in October and currently 1.3% higher at $4164.0/oz today, around the record high of $4164.24, above resistance at $4161.7. US-China working-level trade talks occurred on Monday and China reiterated today its right to control rare earth exports and for the US to negotiate. Gold & silver are looking even more stretched.

- After rising over 4% on Monday, silver continued to rally Tuesday driven by momentum and significant liquidity issues in London. The metal is up 1.6% to $53.20 today after an all-time high of $53.465 earlier in the APAC session, above the fourth resistance level at $52.689, a Fibonacci projection. It is now up over 14% this month.

- Societe Generale revised up its gold forecast to $5000/oz for end-2026, according to Bloomberg, due to strong ETF and central bank flows, which had exceeded its expectations.

- The ongoing US government shutdown is also supporting precious metals with no apparent progress to end the impasse. Wednesday military personnel will miss their first pay but President Trump has said money will be found. It would be the first time in modern US history if it occurs.

- US September CPI was scheduled for 15 October but has now been delayed to 24 October contributing to difficulty in gauging where the economy is ahead of the 29 October Fed decision.

- Later Fed Chair Powell speaks on the economic outlook and monetary policy. The Fed’s Bowman, Waller and Collins, ECB’s Machado, Cipollone and Donnery, and BoE’s Bailey and Taylor also appear. US September NFIB small business optimism, UK labour market data and German September HICP and euro area October ZEW print.

SINGAPORE: MAS Holds On Resilient Growth, Easing Risks To Persist Into 2026

As expected, the MAS kept its policy parameters unchanged at the Oct policy meeting. Market reaction has been muted, with USD/SGD down a touch, last near 1.2990. We dipped towards 1.2980 post the on hold outcome. The SGD NEER per Goldman Sachs estimates is a touch firmer at -0.94% from the top end of the band, we were closer to -1% prior to the decision. The market bias is likely to fade SGD NEER bounces, with easing risks likely to persist from the MAS as we head into 2026 (as growth comes off the boil). For USD/SGD broader USD trends will be important in the near term, SGD FX maintains a positive correlation with USD/JPY moves. If USD/SGD can test through the 200-day EMA (1.3015) a move up to 1.3100 could be targeted. The 100-day EMA support point is back at 1.2910/15.

- The central bank noted, "MAS has eased monetary policy twice this year. Singapore’s economic growth has turned out stronger than expected and the output gap will remain positive in 2025 and come in around 0% next year. MAS Core Inflation should trough in the near term and rise gradually over the course of 2026 as temporary factors dampening inflation fade. MAS will therefore maintain the prevailing rate of appreciation of the S$NEER policy band. There will be no change to its width and the level at which it is centred."

- With the policy announcement came the advanced Q3 GDP print, which was stronger than expected, up 1.3% q/q (versus 0.6% forecast), while in y/y terms we printed at 2.9% (2.0% was forecast and 4.5% was the Q2 outcome). This reinforces today's on hold outcome.

- On growth, the central bank noted: "In 2026, GDP growth is projected to slow in line with external developments to a near-trend pace, such that the output gap narrows to around 0%. The GDP growth forecasts for 2025 and 2026 will be announced in November by MTI.

- On inflation: "All in, MAS Core Inflation is forecast to trough in the near term and rise gradually thereafter. It should average around 0.5% for 2025 as a whole and come in between 0.5−1.5% in 2026.... The inflation outcome is subject to risks. Supply shocks, including those stemming from geopolitical developments, could lift some imported and shipping costs abruptly. Conversely, core inflation could stay lower for longer should growth be more hesitant and weaker than projected. Another significant decline in global oil prices could also temporarily tamp down the pace of price increases."

- These will be watch points for easing risks into 2026.

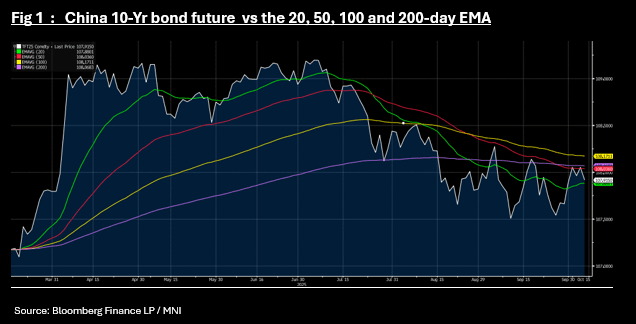

CHINA: 10-Yr Bond Future Tests Key Technical

- Bond futures are lower in morning trade, with the 10-Yr down -0.14 as equities open stronger.

- The fall in the 10-Yr saw the future trade near to the 20-day EMA of 107.87, failing to break below.

- The 2-Yr is down -0.02 at 102.346 to move further below all major moving averages.

- The 10-Yr CGB is up marginally in yield at 1.85% and continues to trade in tight ranges between 1.80% - 1.90% and has been unable to break clear of this range, despite the issuance across central and regional government and despite the absence of PBOC buying. The equity strength of late has failed to push yields dramatically higher either suggesting that we could be in this range for the near term or until further policy were to be announced.

- China is issuing CNY40 bn of 2045 bonds today as the key issuance for the week.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 14/10/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 14/10/2025 | 0750/0950 | ECB Cipollone Speech on Digital Euro | ||

| 14/10/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 14/10/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 14/10/2025 | - | *** | Money Supply | |

| 14/10/2025 | - | *** | New Loans | |

| 14/10/2025 | - | *** | Social Financing | |

| 14/10/2025 | - | ECB Lagarde and Cipollone at G20 Meeting | ||

| 14/10/2025 | 1200/1300 | BOE Taylor Remarks and Fireside Chat at University of Cambridge | ||

| 14/10/2025 | 1230/0830 | * | Building Permits | |

| 14/10/2025 | 1245/0845 | Fed Governor Michelle Bowman | ||

| 14/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 14/10/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 14/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 14/10/2025 | 1610/1210 | BOC Sr Deputy Rogers fireside talk in Vancouver | ||

| 14/10/2025 | 1620/1220 | Fed Chair Jerome Powell | ||

| 14/10/2025 | 1700/1800 | BOE Bailey Fireside Chat at Institute of International Finance | ||

| 14/10/2025 | 1925/1525 | Fed Governor Christopher Waller | ||

| 14/10/2025 | 1930/1530 | Boston Fed's Susan Collins | ||

| 15/10/2025 | 0130/0930 | *** | CPI | |

| 15/10/2025 | 0130/0930 | *** | Producer Price Index | |

| 15/10/2025 | 0430/1330 | ** | Industrial Production | |

| 15/10/2025 | 0600/0800 | *** | Final Inflation Report | |

| 15/10/2025 | 0600/0800 | *** | Final Inflation Report | |

| 15/10/2025 | 0645/0845 | *** | HICP (f) | |

| 15/10/2025 | 0700/0900 | *** | HICP (f) | |

| 15/10/2025 | 0740/0940 | ECB de Guindos at Single Resolution Mechanism Conference | ||

| 15/10/2025 | 0800/0900 | BOE Ramsden in Panel at Resolution Mechanism Conference | ||

| 15/10/2025 | 0900/1100 | ** | EZ Industrial Production | |

| 15/10/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 15/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 15/10/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/10/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/10/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/10/2025 | 1330/0930 | Fed Governor Stephen Miran |