MNI EUROPEAN Market Analysis: US Government Shutdown In Focus

- The focus now turns to the potential US shutdown as Trump stands firm against the Democrats.

- Gold reached a new record high driven by concerns over the US debt ceiling.

- President Xi is likely to use Taiwan independence as part of his trade negotiations.

- Russia makes it clear that they wouldn't attack an EU / NATO member.

- Later we see EU Consumer confidence, US we have Dallas Fed Manufacturing and Bullard and Williams speaking.

MARKETS

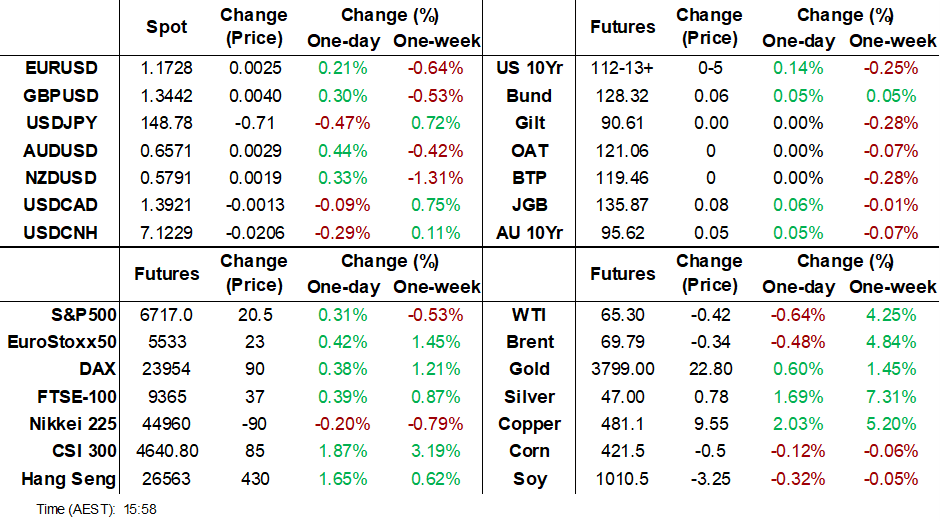

US TSYS: Asia Wrap - Yields Drift Lower As A Shutdown Looms

The TYZ5 range has been 112-08+ to 112-14 during the Asia-Pacific session. It last changed hands at 112-13+, up 0-05 from the previous close.

- The US 2-year yield has edged lower trading 3.631%, down 0.01 from its close.

- The US 10-year yield has moved lower and is trading around 4.158%, down 0.02 from its close.

- 10-Year yields persisted with its probe of the 4.20% area on Friday night, I suspect buyers continue to be around 4.20% initially and look to fade the move higher. The jobs data if released will be key this week. The threat of a US shutdown has seen yields edge lower putting a top in place for now.

- Sean D.Emory on X: “Government shutdown headlines always spark fear. But history tells a calmer story. Looking back at every shutdown since 1976: The S&P 500 has been flat on average during shutdowns (0.0%) and actually up +0.6% the week after. The 10-year Treasury barely moves, average change of +0.03% during, then reversing after. In other words, the market tends to look through shutdown noise quickly.”

- "TRUMP TELLS CBS GOVT SHUTDOWN LIKELY UNLESS DEMOCRATS BACK DOWN, TRUMP CONFIDENT VOTERS TO SIDE WITH HIM IF FUNDING LAPSES: CBS"

- “Guy LeBas, chief fixed-income strategist for Janney Montgomery Scott. “The next thing to get priced in is probably a government shutdown, which has historically been a bad thing for short-term economic growth and pulled US Treasury yields down,” LeBas said.” - BBG

- Data/Events: Pending Home Sales, Dallas Fed Manf. Activity

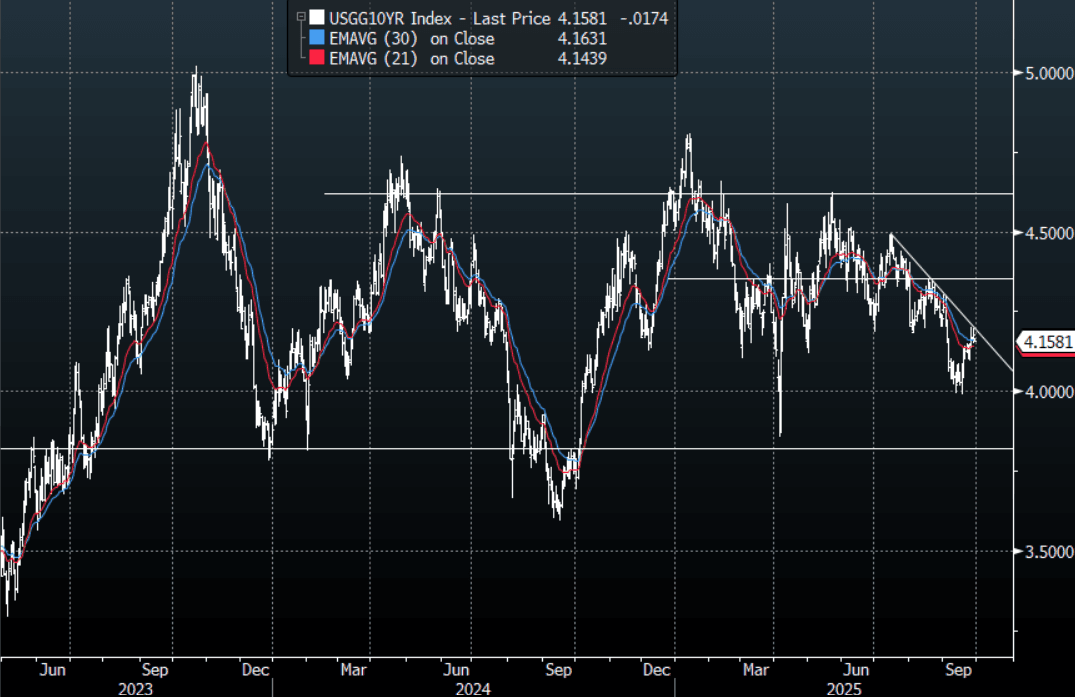

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Good Start to the Week for JGBs

- JGBs are up to 2.5bs tighter in yield today as the whole curve rallied.

- Best performance came from the 20-Yr and 30-Yr which are -2.5bp lower.

- Futures are higher in price with the 10-Yr up +0.24 to 136.03 yet remains below all major moving averages. The 20-day EMA is at 136.36.

- The Japan Final July Coincident Index came in at 114.1, from 115.9 in June and the Leading index was 106.1 from 105.

- This week sees a 2-Yr and 10-Yr JGB auction.

AUSTRALIA: Decent Rally Ahead of RBA

- ACGBs have staged a decent rally today ahead of tomorrow's RBA decision and on headlines that the budget deficit has narrowed.

- Market consensus remains for no change from all of the estimates on BBG currently, with rates set to remain at 3.60%.

- A rally across the yield curve sees lower yields by 3.5-4.5bps with the 10-Yr and 15-Yr the best performers.

- Australia's 10-Yr bond future is up +0.04 to 95.61, below all major moving averages with the 20-day EMA at 95.66.

- The 3-Yr bond future is up +0.04 at 96.42 and is also below all major moving averages.

- This week sees Australia sell A$1.2bn of 2034 bonds on Oct 1, A$1bn 133-day bills and A$1bn 70-day bills on October 2 and A$1bn of 2032 bills on October 3rd.

- There remains only 6bps of cuts priced in over the next month with 16bps over the next three.

NEW ZEALAND: BONDS NZGBS: Strong Start to the Week for Bonds

- NZGBs ended Monday with bond yields 2-2.5bps lower across the yield curve.

- A good start to the week for NZGBS as bonds rallied across the curve. Best performance came in the 2-5 Yr which fell over 2bps whilst the 10-Yr was down 2bps also

- Swap rates closed up to 3bps lower in the front end with the 10-Yr lower by 1bps

- Limited key economic data out today with August Filled Jobs SA MoM in line with July at +0.2%.

- RBNZ dated OIS pricing closed little changed across meetings. 25bps of easing is priced for October, with a cumulative 57bps by November 2025.

- Issuance tomorrow will be $100m 105-day bills, $100m 161-day bills and $50m 357-day bills.

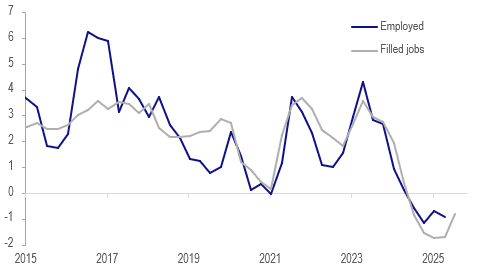

NEW ZEALAND: Labour Market Weak But Turning

August filled jobs rose 0.2% m/m after a downwardly revised flat July. This is the first increase in hiring since January and while the labour market appears to have stabilised conditions remain weak with filled jobs down 0.7% y/y. On a positive note, the August increase was across sectors with the good-producing industries the strongest. The next RBNZ decision is on October 8 and it is expected to ease again but it remains uncertain if it will be by 25bp or 50bp.

- The Q3 average to date filled jobs are up 0.1% q/q, which if sustained would be the first positive after 5 quarterly contractions. September filled jobs are published on 28 October and Q3 labour data on 5 November.

NZ filled jobs vs employment y/y%

Source: MNI - Market News/LSEG/Statistics NZ

- Good-producing industries increased filled jobs by 0.6% m/m in August with the primary sector up 0.2% and services +0.1%. Over the last year construction has been the weakest down 5.1% y/y followed by professional, scientific and technical services -2.7% y/y, while healthcare and education were both up 1.7% y/y.

- The weakness in the jobs market has been concentrated in the under 35s with 15-19 years -8.2% y/y, 20-24 years -3% y/y and 25-29 years -3.5%. Due to this many people have stayed in education.

- Another tentative sign of a stabilisation in the jobs market is the SEEK new job ads index which was up 4.4% y/y in August after contracting since November 2022. The index is at its highest since May 2024.

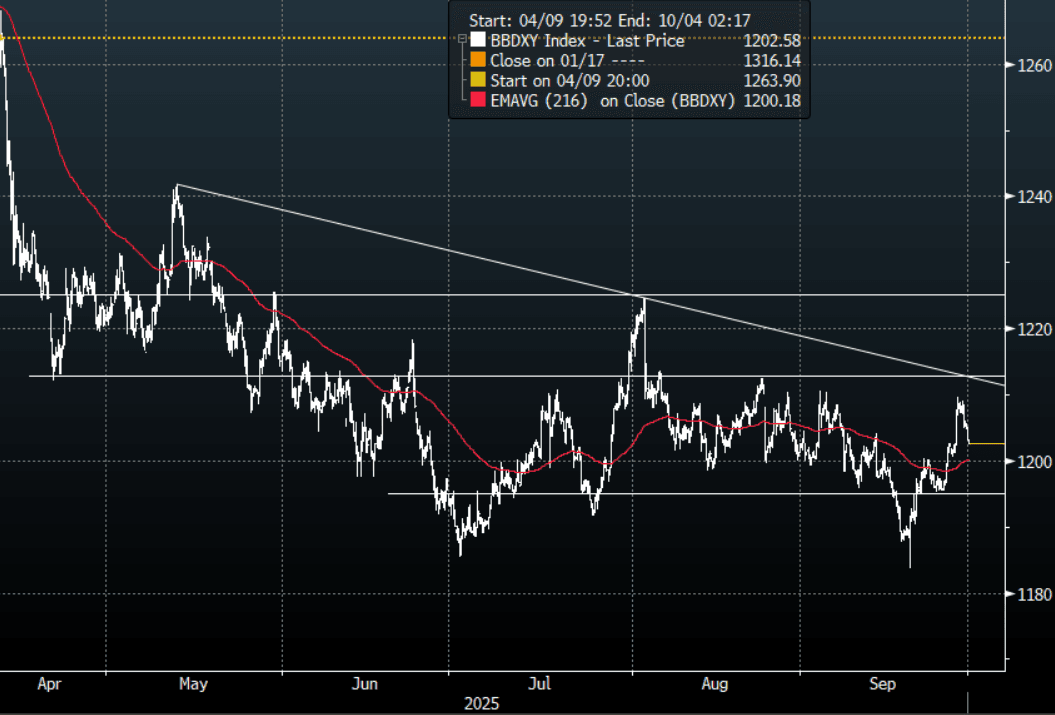

FOREX: Asia FX Wrap - The USD Slips Lower As Shutdown Looms

The BBDXY has had a range of 1202.41 - 1205.07 in the Asia-Pac session; it is currently trading around 1202, -0.25%. The USD topped out towards 1210 again on Friday and has drifted lower very easily, the follow through this morning being aided by US shutdown fears. I can’t see any big directional moves this week until the market sees the Payroll number. Next resistance is back towards the 1215-1225 area where I would expect sellers to remerge initially. The big question is at what level do the global asset managers return to selling for hedging purposes. First support back towards the 1200 area and then 1195. Quarter-end for Asset managers likely to see some USD selling to rebalance portfolios.

- EUR/USD - Asian range 1.1702 - 1.1729, Asia is currently trading 1.1730. The pair has drifted back above 1.1700, I suspect sellers could reemerge above 1.1750 initially. The deeper correction looks to have been put on hold for now as the focus turns toward the payroll number.

- GBP/USD - Asian range 1.3394 - 1.3434, Asia is currently dealing around 1.3435. The pair could not break through its support around the 1.3300 area, price has bounced back into the range. The market should be looking for bounces to fade, first sell zone back towards the 1.3500 area.

- USD/CNH - Asian range 7.1199 - 7.1432, the USD/CNY fix printed 7.1089, Asia is currently dealing around 7.1230. The pair stalled toward 7.1500 and collapsed lower again very easily. The area just below 7.1000 has proved to be well supported recently lets see if that continues.

- Cross asset : SPX +0.35%, Gold $3798, US 10-Year 4.158%, BBDXY 1202, Crude Oil $65.31

- Data/Events : Spain CPI/Retail Sales, EZ Consumer Confidence

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - USD/JPY Slips Back Below 149.00 As US Shutdown Looms

The USD/JPY range has been 148.89 - 149.52 in the Asia-Pac session, it is currently trading around 148.95, -0.35%. The USD’s bout of strength stalled as the data on Friday came in as expected. This saw USD/JPY fail toward 150.00 and the drift lower has extended this morning as the market begins to price in a US shutdown. Having closed back above 149.00 to end the week the JPY bears would be hoping that dips remain supported. Non-Farms this week if released could have a significant bearing on price, so the market will be setting up for this to start the week. First Support is around the 148.50/149.00 area, if this doesn't hold due to shutdown fears we will go into payrolls back in familiar ranges.

- “LDP contender Sanae Takaichi hinted at a review of Japan’s $550 billion investment fund that was part of its pact with the US.” - BBG

- "JAPAN TO CONVENE EXTRAORDINARY DIET SESSION MID-OCT: YOMIURI" - BBG

- (Reuters) - “The Bank of Japan will probably raise its benchmark interest rate at least four more times to 1.5% before Governor Kazuo Ueda's term ends in early 2028, former central bank board member Makoto Sakurai told Reuters. Sakurai, who retains close contact with incumbent policymakers, forecast another hike by year-end, two more increases in fiscal 2026, and one or two hikes in the year ending March 2028.”

- Bloomberg - “Dollar-Yen Risk Is Overlooked by Investors, Morgan Stanley Says. Morgan Stanley says markets are underpricing the risk that the dollar will push lower against the yen. It recommends buying options ahead of US jobs data, a potential US US government shutdown and the party leadership election in Japan.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 150.70($410m). Upcoming Close Strikes : 146.50($1.09b Oct 1) - BBG.

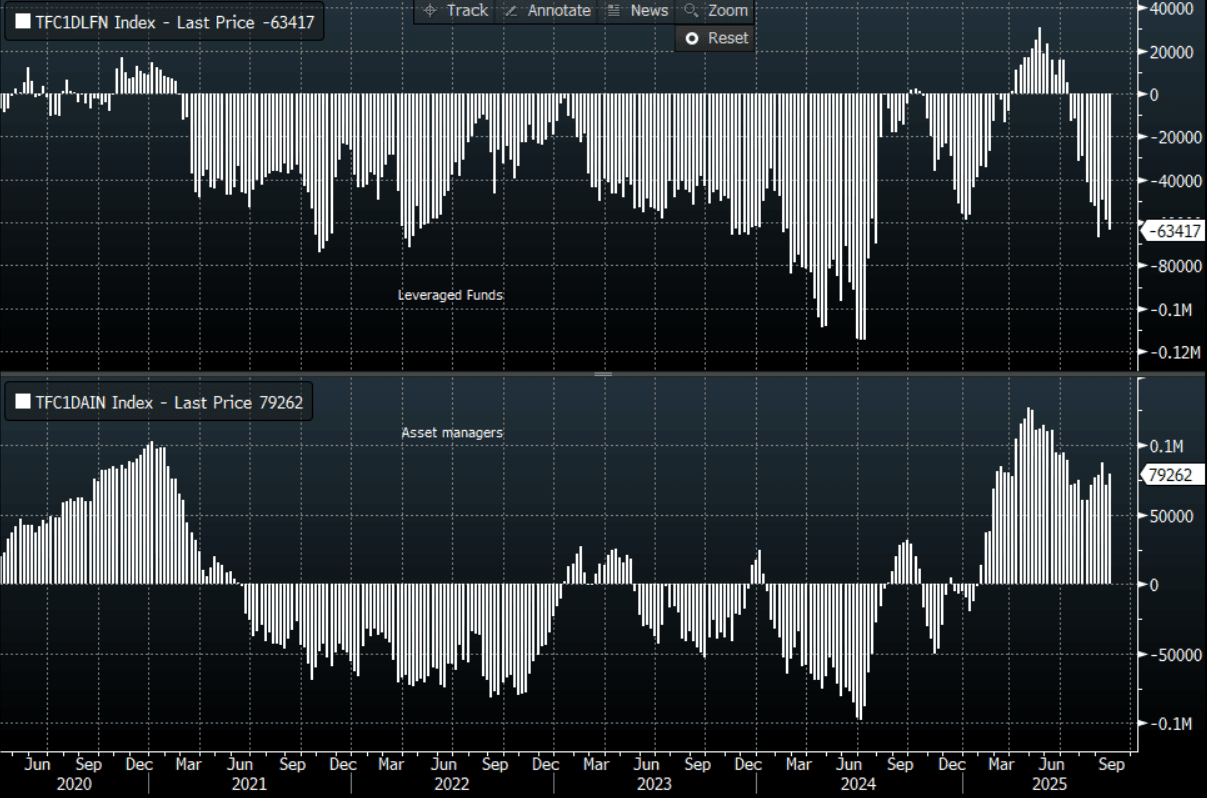

- CFTC data shows last week asset managers increased their JPY longs slightly +79262( Last +71162), leveraged funds though again used the dip to add to their short position as the support held, -634171(Last -58811). The diverging views amongst investors continue to build.

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Bounces As USD Gets Hit On Shutdown Fears

The AUD/USD has had a range of 0.6547 - 0.6567 in the Asia- Pac session, it is currently trading around 0.6565, +0.35%. US stocks found some support and the USD’s bout of strength stalled as the data on Friday came in as expected. The AUD found some demand back towards the 0.6500 area and is trying to bounce, getting an added nudge this morning as the risk of a US government shutdown increases. Price is back in the range and the market will be turning its attention towards the Fridays Payroll number. RBA is tomorrow.

- MNI AU - RBA Widely Expected To Hold On 30 September. The focus of the week will be Tuesday’s RBA decision followed by Governor Bullock’s press conference. As it is widely expected to keep rates at 3.6% and there won’t be an updated set of forecasts, the tone of the statement and Bullock’s comments will be scrutinised after disinflation appears to have stalled in Q3 and the Governor said to a parliamentary committee last week that "domestic data have been broadly in line with our expectations or if anything slightly stronger". The Board is likely to remain highly data dependent.

- “Australia’s fiscal 2025 budget deficit is set to be just under A$10 billion ($6.56 billion) compared with the government’s forecast of A$27.9 billion.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6550(AUD405m), 0.6625(AUD1.29b), 0.6725(AUD1.19b). Upcoming Close Strikes : 0.6600(AUD943m Oct 1), 0.6600(AUD1.57b Oct 2), 0.6700(AUD1.64b Oct 1) - BBG

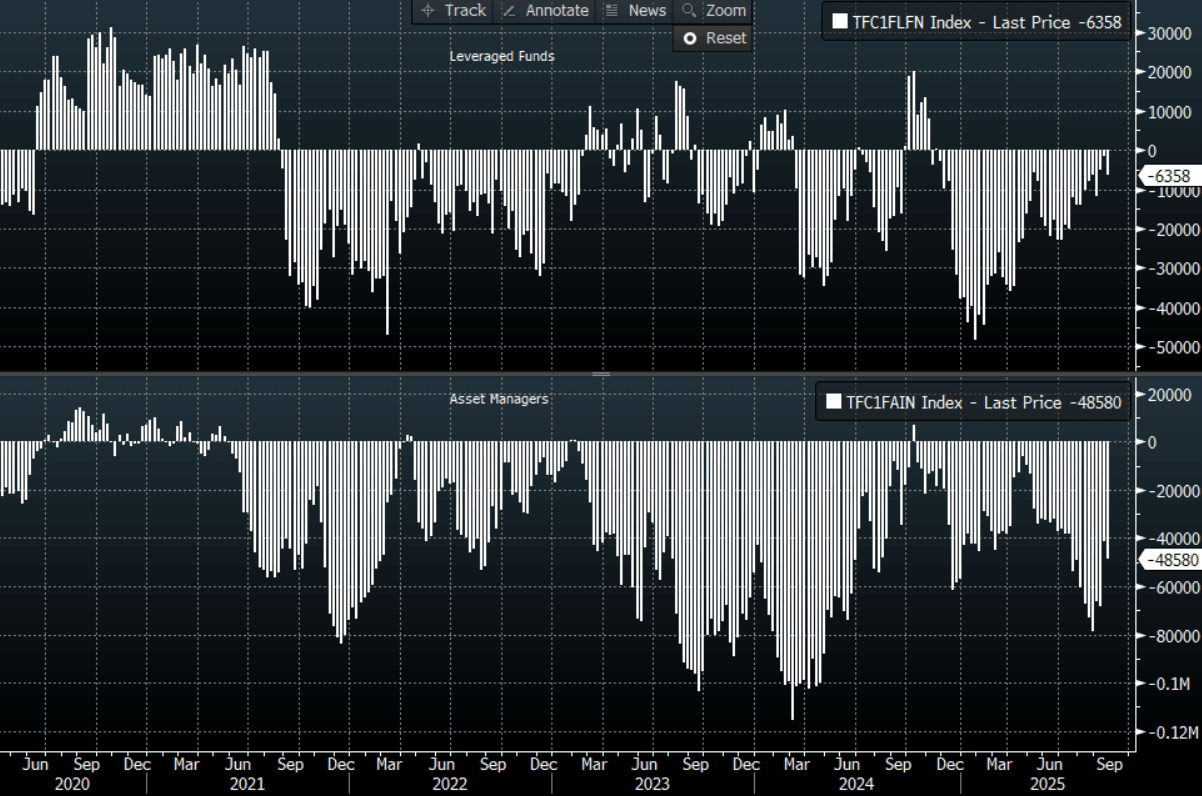

- CFTC Data last week shows Asset managers added back to their recently reduced shorts, -48580(Last -41095). The Leveraged community did likewise, -6358(Last -1519).

- AUD/JPY - Asia-Pac range 97.67 - 97.99, Asia is trading around 97.70. The pair found solid demand back towards 97.00 and bounced last week with the help of the AU CPI print. While above 97.00 the focus will remain on September’s highs toward 98.50.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - NZD/USD Weakness Gets A Reprieve

The NZD/USD had a range of 0.5771 - 0.5786 in the Asia-Pac session, going into the London open trading around 0.5785, +0.25%. US stocks found some support and the USD’s bout of strength stalled as the data on Friday came in as expected. The NZD found some demand back towards the 0.5750 area and is trying to bounce, getting an added nudge this morning as the risk of a US government shutdown increases. The NZD broke through its pivotal 0.5800 support last week which should keep the pair under pressure heading into payrolls. The first sell zone would be back towards the 0.5850/0.5900 area.

- Bloomberg - “RBNZ Says Pandemic Inflation Taught It Lessons for Future Shocks. The Reserve Bank’s Monetary Policy Committee has gained valuable insights into how economic activity, price setting by businesses and inflation expectations evolve during periods of high inflation and economic volatility, Conway said Monday in Wellington after releasing a review of monetary policy in recent years.”

- “Guy LeBas, chief fixed-income strategist for Janney Montgomery Scott. “The next thing to get priced in is probably a government shutdown, which has historically been a bad thing for short-term economic growth and pulled US Treasury yields down,” LeBas said.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5785(NZD904m Sept 30), 0.5875(NZD372m Sept 30) - BBG

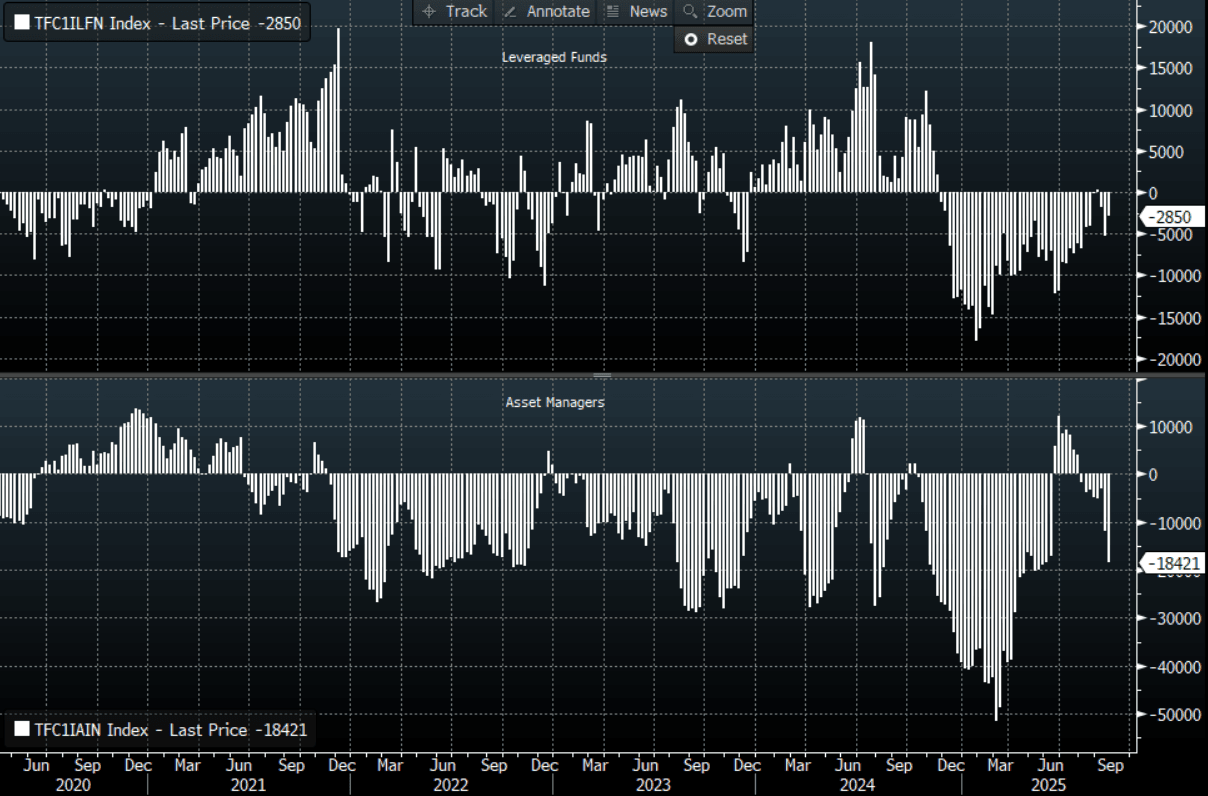

- CFTC Data of last week shows Asset Managers continuing to rebuild their short positions in the NZD, -18421(Last -11933). The Leveraged community don’t seem as convinced and reduced their own shorts, -2850(Last -5327).

- AUD/NZD range for the session has been 1.1328 - 1.1354, currently trading around 1.1350. The Cross has broken above the multiple highs around the 1.1200 area and is consolidating its extension above 1.1300, helped by the AU CPI print. Dips should now continue to be supported as the market turns its focus towards the 1.1400/1.1500 area.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

OIL: Crude Lower As Excess Supply Worries Come Back Into Focus

Oil prices have unwound Friday’s moderate gains during Monday’s APAC trading as excess supply concerns dominate with flows from Iraqi Kurdistan restarting on the weekend and OPEC due to meet on 5 October. WTI is down 0.6% to $65.36/bbl, close to the intraday high, while Brent is 0.6% lower at $69.73/bbl after reaching $69.84. The USD index is down 0.2%.

- The focus this week will be on Friday’s September US payroll data, which could be delayed if there isn’t an agreement to lift the US debt ceiling, and Sunday’s OPEC meeting to determine November’s production target. Currently, it is expected to lift it by more than October’s +137kbd but capacity within the group is becoming an issue. The IEA is forecasting a record oil surplus for 2026.

- Iraq has revised up its export forecast to 3.65mbd after the resumption of shipments from Iraqi Kurdistan through the Kirkuk-Ceyhan pipeline on the weekend after a deal was finally reached with Turkey. Flows were halted in March 2023.

- Later the Fed’s Waller, Musalem and Bostic speak as well as Cleveland’s Hammack with ECB’s Lane & BoE’s Ramsden. The ECB’s Cipollone, Schnabel and Machado also appear. In terms of data, there is US Dallas Fed September manufacturing, preliminary September Spanish CPI, September European Commission survey.

Gold & Silver Rally As US Funding Impasse Unresolved

After rising 2% last week, gold prices are currently up 1.0% to $3797.7/oz so far in Monday’s APAC session. It is not too far off the new record high at $3799.40 reached today, holding below round number resistance at $3800, the last record was $3791.1 on 23 September. It is being supported by flight-to-quality flows as a US government shutdown looms from Wednesday as Democrats and Republicans can’t agree on a debt ceiling lift. In addition, the market has almost two Fed cuts by end 2025. The US dollar has also softened further (BBDXY -0.2%) and the 2-year yield is slightly lower.

- Silver has also continued to rally after Friday’s 2% jump driven by not just safe haven flows but also tightness in the physical market. The metal is used in solar panel production. Silver is up 2.1% to $47.04 so far in Monday’s trading, above resistance at $46.092. It reached a high of $47.181 but has struggled to hold breaks above $47.

- A US shutdown could delay data releases with the key payrolls data currently scheduled for Friday. President Trump is scheduled to meet with party leaders to find a solution to the fiscal impasse.

- Equities are generally stronger with the S&P e-mini up 0.3% and Hang Seng +1.4% but Nikkei down 1.4% due to month end. Oil prices are lower with WTI -0.6% to $65.31/bbl. Copper is up 0.8%.

- Later the Fed’s Waller, Musalem and Bostic speak as well as Cleveland’s Hammack with ECB’s Lane & BoE’s Ramsden. The ECB’s Cipollone, Schnabel and Machado also appear. In terms of data, there is US Dallas Fed September manufacturing, preliminary September Spanish CPI, September European Commission survey.

ASIA STOCKS: China Has Strong Start to the Week

China's major bourses were very strong today with the Hang Seng leading the way, with Korea following the lead whilst Taiwan is closed. The NIKKEI appears to be suffering from profit taking after hitting highs last week.

- The Hang Seng is up +1.40%, the CSI 300 +0.47%, Shanghai up +0.13% and Shenzhen up +0.86%.

- The NIKKEI is down -0.74% today at 45,023.

- The KOSPI is having a strong start to the week with gains of 1.40%.

- The FTSE Malay KLCI has failed to move today, unchanged for the day.

- The Jakarta Composite is up +0.60% today.

- The NIFTY 50 fell for six consecutive days, but has started this week off with a rally of +0.45% in the morning session.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 29/09/2025 | 0650/0850 | ECB Cipollone Keynote At Baltic Digital Euro Conference | ||

| 29/09/2025 | 0700/0900 | *** | HICP (p) | |

| 29/09/2025 | 0830/0930 | ** | BOE Lending to Individuals | |

| 29/09/2025 | 0830/0930 | ** | BOE M4 | |

| 29/09/2025 | 0900/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 29/09/2025 | 0900/1100 | ECB Schnabel On Current Aspects of Monetary Policy | ||

| 29/09/2025 | 1130/0730 | Fed Governor Christopher Waller | ||

| 29/09/2025 | 1200/1400 | ECB Lane In Policy Panel At Inflation Conference | ||

| 29/09/2025 | 1200/0800 | Cleveland Fed's Beth Hammack | ||

| 29/09/2025 | 1200/1300 | BOE Ramsden On ECB Inflation Panel | ||

| 29/09/2025 | 1330/0930 | NY Fed's Roberto Perli | ||

| 29/09/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 29/09/2025 | 1430/1030 | ** | Dallas Fed manufacturing survey | |

| 29/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 29/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 29/09/2025 | 1730/1330 | St. Louis Fed's Alberto Musalem | ||

| 29/09/2025 | 1730/1330 | Ex-St. Louis Fed's James Bullard | ||

| 29/09/2025 | 1730/1330 | New York Fed's John Williams | ||

| 29/09/2025 | 2200/1800 | Atlanta Fed's Raphael Bostic | ||

| 30/09/2025 | 2301/0001 | * | BRC Monthly Shop Price Index | |

| 30/09/2025 | 2350/0850 | ** | Industrial Production | |

| 30/09/2025 | 2350/0850 | * | Retail Sales (p) | |

| 30/09/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 30/09/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI | |

| 30/09/2025 | 0130/1130 | * | Building Approvals | |

| 30/09/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI | |

| 30/09/2025 | 0430/1430 | *** | RBA Rate Decision | |

| 30/09/2025 | 0600/0800 | ** | Retail Sales | |

| 30/09/2025 | 0600/0800 | ** | Import/Export Prices | |

| 30/09/2025 | 0600/0800 | ** | Retail Sales | |

| 30/09/2025 | 0600/0700 | * | Quarterly current account balance | |

| 30/09/2025 | 0600/0700 | *** | GDP Second Estimate | |

| 30/09/2025 | 0645/0845 | *** | HICP (p) | |

| 30/09/2025 | 0645/0845 | ** | PPI | |

| 30/09/2025 | 0645/0845 | ** | Consumer Spending | |

| 30/09/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/09/2025 | 0755/0955 | ** | Unemployment | |

| 30/09/2025 | 0800/1000 | ** | PPI | |

| 30/09/2025 | 0800/1000 | *** | Bavaria CPI | |

| 30/09/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 30/09/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 30/09/2025 | 0900/1100 | *** | HICP (p) | |

| 30/09/2025 | 1000/0600 | Fed Vice Chair Philip Jefferson | ||

| 30/09/2025 | 1100/1300 | ECB Cipollone In Panel At Sibos | ||

| 30/09/2025 | 1150/1250 | BOE Lombardelli Panel On MonPol, Bank of Finland | ||

| 30/09/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 30/09/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 30/09/2025 | 1250/1450 | ECB Lagarde Keynote at MonPol Conference, Bank of Finland | ||

| 30/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 30/09/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 30/09/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 30/09/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 30/09/2025 | 1300/1500 | ECB Elderson In Panel On Climate Action | ||

| 30/09/2025 | 1300/0900 | Boston Fed's Susan Collins | ||

| 30/09/2025 | 1325/1425 | BOE Mann Fireside Chat At FT | ||

| 30/09/2025 | 1342/0942 | *** | MNI Chicago PMI |