BOC: MNI BoC Review-Jan 2026: Uncertainty Remains The Watchword

Jan-28 16:46

We've just published our review of the Bank of Canada's January meeting - Download Full Report Here:...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

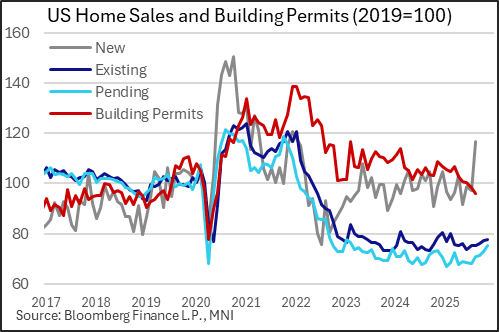

US DATA: Pending Home Sales Pickup Another Sign Frozen Housing Market Is Thawing

Dec-29 16:39

The latest pending home sales data for November reinforces other indications of a pickup in housing market activity as we head into 2026. The National Association of Realtors reported a pending sales index of 79.2 for the month, a 3.3% M/M improvement to the highest level in 33 months (all on a seasonally-adjusted basis).

- This bodes for a further improvement in future months in existing home sales, which had already posted a 9-month high in November. This index reading indicates that sales are nearing 80% of 2001 levels; they bottomed out closer to 70% at the turn of the year but remain well down from the peak of 125% set in October 2021.

- Regional gains were led by the West (+9.2% M/M) but there was an improvement across all of the other 3 regions.

- There aren't many further details in the report to explain the pickup - NAR Chief Economist Lawrence Yun is quoted as saying "Improving housing affordability–driven by lower mortgage rates and wage growth rising faster than home prices–is helping buyers test the market. More inventory choices compared to last year are also attracting more buyers to the market."

- The government shutdown means residential construction activity is only coming out with an extensive lag; we only get a combined September/October report for housing starts/permits on January 9 for example. Those series had been very soft through the summer, with permitting hitting multi-year lows.

- However there is a subtle but noticeable upturn in buyer activity as reflected in this report, in addition to mortgage purchase applications hitting post-2023 highs in November, and NAHB homebuilder sentiment picking up since September.

- These are all still at depressed levels but suggest that the market is stabilizing and potentially gaining some traction going into 2026.

US STOCKS: Midday Equities Roundup: Unwinding Longs

Dec-29 16:35

- Stocks are running weaker ahead midday, scaling off last week's highs as accounts took profits going into year end. Volumes improved with European bourses back from extended Christmas holidays.

- Currently, the DJIA trades down 240.28 points (-0.49%) at 48476.49, S&P E-Mini Futures down 31.5 points (-0.45%) at 6948.5, Nasdaq down 143.6 points (-0.6%) at 23450.81.

- Materials, IT and Discretionary sector shares led declines in the first half, mining stocks unwinding support as Gold fell sharply from Friday's record highs (4335.0 current vs. 4533.21 Frida): Newmont -5.02%, Albemarle -3.01%, Freeport-McMoRan -2.38% and Martin Marietta Materials -1.75%.

- Concerns over AI-related valuations weighed on Tech stocks (again): Sandisk Corp -3.60%, NVIDIA -2.00%, ON Semiconductor -1.69% and Oracle -1.30%.

- Meanwhile, luxury travel related shares trade weaker: Norwegian Cruise Line -2.63%, Tesla -1.90%, MGM Resorts -1.65%, Royal Caribbean -1.55%.

- On the positive side, Utilities and Energy sector shares led advances ahead midday: Devon Energy +2.07%, Diamondback Energy +1.87%, Expand Energy +1.59% and Exxon Mobil +1.59%.

- While PG&E gained +1.43%, Edison International +1.09%, Southern Co +1.00%, NextEra Energy +0.86% and Eversource Energy +0.83%.

FED: US TSY 26W BILL AUCTION: HIGH 3.500%(ALLOT 87.64%)

Dec-29 16:32

- US TSY 26W BILL AUCTION: HIGH 3.500%(ALLOT 87.64%)

- US TSY 26W BILL AUCTION: DEALERS TAKE 49.03% OF COMPETITIVES

- US TSY 26W BILL AUCTION: DIRECTS TAKE 8.69% OF COMPETITIVES

- US TSY 26W BILL AUCTION: INDIRECTS TAKE 42.28% OF COMPETITIVES

- US TSY 26W BILL AUCTION: BID/CVR 2.52