MNI ASIA OPEN: Weekly/Continuing Claims Rise, PPI In-Line

EXECUTIVE SUMMARY

- MNI US: Trump "Not Going To Fire" Powell But "Might Have To Force Something"

- MNI SECURITY: Trump Envoy Witkoff Will Attend 6th Round Of Iran Talks On June 15

- MNI US INFLATION: Core PCE Estimates Downgraded To 0.14-0.15% After CPI/PPI

- MNI US DATA: Continuing Claims Paint A More Worrying Picture

- MNI US DATA: PPI Trends Largely Benign, But Trade Margins Bounce Back

US

MNI US: Trump "Not Going To Fire" Powell But "Might Have To Force Something"

US President Donald Trump is delivering press remarks at a White House ceremony to sign a bill barring California electric vehicle and emissions rules. Trump addresses recent rhetoric towards Fed Chair Jerome Powell: “I like long-term cheap debt… If we were to lower the interest rate by one point… that’s $300 billion a year… But we can’t get this guy to do it,” he says, referring to Powell.

NEWS

MNI SECURITY: Trump Envoy Witkoff Will Attend 6th Round Of Iran Talks On June 15

Newswires reporting confirmation that US President Donald Trump’s special envoy to the Middle East, Steve Witkoff, will travel to Muscat, Oman, on Sunday, June 15, to attend the 6th round of US-Iran nuclear talks. As in previous rounds in Muscat and Rome, the talks are expected to take place in a mixed format of direct and indirect negotiations, with Omani officials acting as mediators. The talks come amid decreased optimism that a deal can be struck, with Iran hawks in the US pushing Trump to reject any deal that falls short of the complete neutralisation of Iran’s enrichment programme - a stated red line for Tehran.

MNI MIDEAST: GLZ-Israeli Minister & Mossad Head To Meet w/Witkoff Before Iran Talks

Israeli Army Radio (GLZ) reports that, according to an Israeli source, "[PM Benjamin] Netanyahu instructed Minster [of Strategic Affairs Ron] Dermer and the head of the Mossad [David Barnea] to go to talks tomorrow with [US Middle East] envoy [Steve] Witkoff ahead of the next round of talks between the US and Iran - in another attempt to clarify Israel's position."

MNI IRAN: Mehr News-Military Drills Launched Focusing On Monitoring Enemy Movement

Islamic Revolutionary Guards Corps (IRGC)-linked Mehr News reports that the country's armed forces are launching military drills with a "focus on [monitoring] enemy movements". Amid speculation that Israel could launch strikes on Iranian nuclear facilities "within days", and with the US evacuating non-essential personnel from embassies in the region, the prospect of an outbreak of inter-state armed conflict is as high as it has been since the tit-for-tat airstrikes between Iran and Israel that ran from April to October 2024.

US TSYS

MNI US TSYS: Rise in Weekly/Continuing Jobless Claims Lends to Early Rate Support

- Treasuries look to finish near session highs set after this morning's weekly and continuing jobless claims came out higher than expected, PPI inflation metrics more in-line with expectations. Rates gained additional risk-off support after wires reported that Israel was "considering military action against Iran" in coming days.

- At the moment, Sep'25 10Y futures trade +11 at 111-01 vs. 111-06 high, just off initial technical resistance at 111-14.5 (High Jun 5 & 61.8% of the May 1 - 22 downleg).

- Headline final demand PPI reading of 0.13% M/M was below the 0.2% expectation, and while that's offset by a decent upward revision to April (-0.24% from -0.47%), the overall index remains below its January level in seasonally adjusted terms, and up just 2.6% Y/Y.

- Initial jobless claims: 248k (sa, cons 242k) in the week to Jun 7 after a marginally upward revised 248k (initial 247k). Continuing claims: 1956k (sa, cons 1910k) in the week to May 31 after a marginally downward revised 1902k (initial 1904k).

- US $22B 30Y Bond auction re-open stopped through on decent demand, awarded 4.844% high yield vs. 4.859% WI; 2.43x bid-to-cover vs. 2.31x in the prior month.

- Focus turns to Friday's UofM sentiment and 1Y/5-10Y inflation expectations.

OVERNIGHT DATA

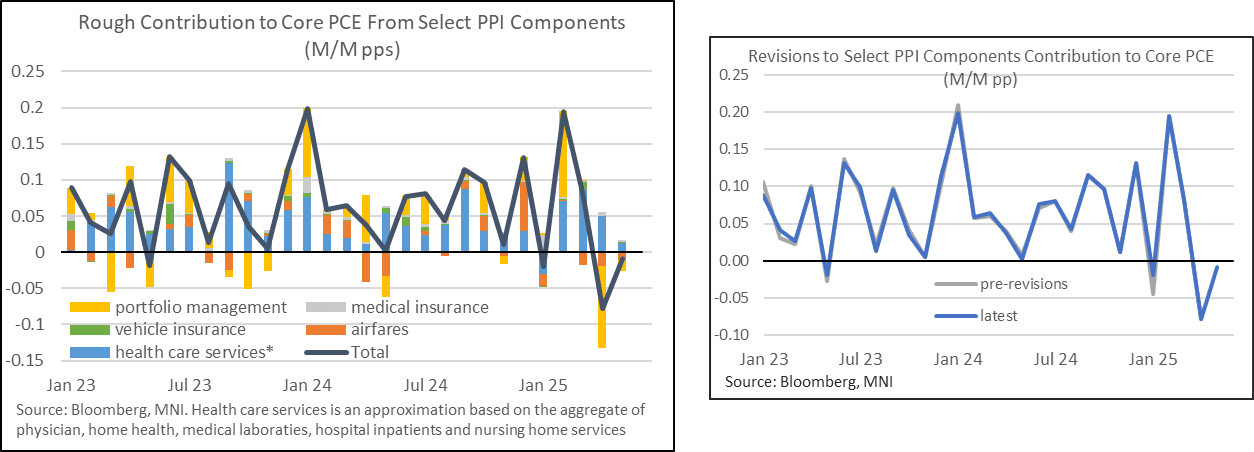

MNI US DATA: PPI Trends Largely Benign, But Trade Margins Bounce Back

May's Producer Price inflation report provided some relief to concerns that tariff-related factors would significantly push up pipeline pressures in the month. Instead, the broader trend in pipeline pressures appears to be slowing rather than accelerating.

- The headline final demand PPI reading of 0.13% M/M was below the 0.2% expectation, and while that's offset by a decent upward revision to April (-0.24% from -0.47%), the overall index remains below its January level in seasonally adjusted terms, and up just 2.6% Y/Y. Ex-food/energy rose 0.14% (0.3% expected), after an upwardly revised -0.21% (was -0.44%), but the 3M annualized run rate remained below 1% (0.9%) for a second month and the 3.0% Y/Y rate was the slowest since August 2024.

- The main measure of core PPI has effectively ground to a halt: ex-food/energy/trade 0f 0.05% M/M follows -0.13% in April (slight downward rev from -0.11%), bringing the 3M annualized rate down to 0.5% - the slowest since June 2020. The 6-month annual rate is down to 2.6%, lowest since November 2023, with the Y/Y rate clocking in at 2.7%, lowest (unrounded) since December 2023.

MNI US INFLATION: Core PCE Estimates Downgraded To 0.14-0.15% After CPI/PPI

Analysts have mostly downgraded their expectations for May core PCE inflation (released Jun 27) after this week's CPI and then PPI prints came in below-survey.

- Additionally, key PPI-derived inputs into PCE were mixed but appeared to come in on the weaker side of most analysts' expectations, particularly for portfolio management/investment advice.

- The median analyst estimate for May core PCE is now around 0.14-0.15% M/M, compared with 0.22% going into the May inflation data round.

- That would be a second consecutive uptick (after March's 10-month low 0.09%, April was 0.12%) but would still bring the 3M SA annual rate of core PCE inflation down to 1.4% (slowest since November 2020, from 2.7% prior and 4.1% as recently as February). The 6M rate would remain relatively steady at 2.8% (from 2.7% prior) and the Y/Y SA at 2.6% (2.5% prior).

In ascending order of core PCE expectations:

- JPMorgan: 0.12% (0.19% pre-PPI)

- BNP Paribas: 0.13% (0.11% pre-PPI)

- Goldman Sachs: 0.14% (0.18% pre-PPI)

- Barclays: 0.15% (0.22% pre-PPI)

- BofA: 0.16% (0.18-0.24% pre-PPI)

- Nomura: 0.169% (0.348% pre-PPI)

- Morgan Stanley: 0.17%

MNI US OUTLOOK/OPINION: Wide Range To Core PCE Estimates, PPI Portfolio Mgmt Watched

- There remains a wide range of estimates for core PCE inflation in May (0.11-0.35% M/M across analysts below, after 0.12% M/M in April) following yesterday’s CPI release.

- Today’s PPI release is likely to see a sizeable narrowing in this range. There are many, mostly services-related, components that feed into core PCE but we expect most attention this month on portfolio management & investment advice after its -6.6% M/M drop dragged circa -0.12pps from core PCE in April.

- The S&P 500 increased 8.2% M/M in May when looking at monthly averages after -5.5% in April and -5.9% in March but the lags at which these moves filter into the PPI category are uncertain.

- This category is also prone to large revisions (on the subject of which, February's 7.0% M/M jump still looks out of kilter with market moves).

Analyst estimates for % M/M core PCE inflation.

- BNP Paribas: 0.11% - assuming an 8bp drag from portfolio mgmt owing to 1-mth lag to S&P 500. [we estimate that 8 looking for a circa -4.5%]

- TD Securities: 0.16%

- Goldman Sachs: 0.18%

- JPMorgan: 0.19%

- BofA: 0.18-0.24%

- Nomura: 0.35% - eyeing portfolio mgmt & invt advice +4.4% after -6.6%

MNI US DATA: PPI Details Point To Broadly Neutral Impact On May Core PCE

- Our simple proxy for the impact of PPI details on core PCE in May came in at -0.01pps after an unrevised -0.088ps in April and +0.08pps in March.

- This looks at a range of health care services, airfares, portfolio mgt & invt advices, vehicle insurance and medical insurance.

One detail that was particularly in market focus:

- PPI portfolio management & investment advice: -0.8% M/M in May after an upward revised -6.3% (initial -6.6%).

- We'd seen some specific estimates ranging roughly between -4.5% and +4.5%

- It had a weight of 1.8% of core PCE in April, and assuming similar this month would drag only about -0.01pp off core PCE in May after a heavy -0.11p in April.

MNI US DATA: Continuing Claims Paint A More Worrying Picture

Weekly jobless claims data showed another upside surprise for initial claims but with continuing claims offering a notably more concerning push higher in signs of a more pronounced slowdown in re-hiring. Initial jobless claims: 248k (sa, cons 242k) in the week to Jun 7 after a marginally upward revised 248k (initial 247k)

- The four-week average increased to 240k from 235k, to its highest since Aug 2024.

- Continuing claims: 1956k (sa, cons 1910k) in the week to May 31 after a marginally downward revised 1902k (initial 1904k). Whilst it’s still the highest since Nov 2021, as claims were falling sharply lower having surged in the pandemic, the recent upward trend is clear to see in the charts below.

- It sees the claims rate, which started to draw some attention last week with a second week rounding to 1.3%, lift from 1.25% to 1.28% for a clearer deterioration.

- The upward trend is borne out in the NSA data as well, pushing above recent ranges having recently been tracking 2017 (one of the higher recent non-pandemic years).

- The 75k increase in NSA continuing claims looks fairly broad-based by state, led by the two largest population centers: 31k came from California and 9.5k from Texas before 8k from Minnesota and 7.6k from Massachusetts.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 70.58 points (0.16%) at 42938.1

S&P E-Mini Future up 15.25 points (0.25%) at 6044.5

Nasdaq up 35.6 points (0.2%) at 19652.04

US 10-Yr yield is down 6.5 bps at 4.3553%

US Sep 10-Yr futures are up 11.5/32 at 111-1.5

EURUSD up 0.0089 (0.77%) at 1.1576

USDJPY down 1 (-0.69%) at 143.56

WTI Crude Oil (front-month) down $0.01 (-0.01%) at $68.14

Gold is up $31.71 (0.95%) at $3386.94

European bourses closing levels:

EuroStoxx 50 down 32.33 points (-0.6%) at 5360.82

FTSE 100 up 20.57 points (0.23%) at 8884.92

German DAX down 177.45 points (-0.74%) at 23771.45

French CAC 40 down 10.79 points (-0.14%) at 7765.11

US TREASURY FUTURES CLOSE

3M10Y -7.945, -2.272 (L: -5.422 / H: 4.847)

2Y10Y -1.701, 44.768 (L: 43.725 / H: 47.827)

2Y30Y -2.999, 93.158 (L: 92.2 / H: 97.656)

5Y30Y -1.876, 87.596 (L: 86.849 / H: 91.207)

Current futures levels:

Sep 2-Yr futures up 2.5/32 at 103-22.875 (L: 103-19.75 / H: 103-24.75)

Sep 5-Yr futures up 6.5/32 at 108-7.75 (L: 107-31.5 / H: 108-11.75)

Sep 10-Yr futures up 11.5/32 at 111-1.5 (L: 110-19.5 / H: 111-06)

Sep 30-Yr futures up 34/32 at 114-11 (L: 113-03 / H: 114-12)

Sep Ultra futures up 42/32 at 117-25 (L: 116-06 / H: 117-27)

MNI US 10YR FUTURE TECHS: (U5) Recovery Extends

- RES 4: 111-30 76.4% retracement of the May 1 - 22 downleg

- RES 3: 111-20 1.0% 10-dma envelope

- RES 2: 111-14+ High Jun 5 & 61.8% of the May 1 - 22 downleg

- RES 1: 111-06 Intraday High Jun 12

- PRICE: 111-01 @ 1520 ET Jun 12

- SUP 1: 109-26 Low May 29

- SUP 2: 109-12+ Low May 22 and the bear trigger

- SUP 3: 109-09+ Low Apr 11 and key support

- SUP 4: 108-25+ 0.764 proj of the Apr 7 - 11 - May 1 price swing

Treasury futures are trading higher today, extending the recovery from Wednesday’s low. This cancels - for now - a recent bearish threat. Attention is on key short-term resistance at 111-14+, a Fibonacci retracement and the Jun 5 high. Clearance of this hurdle would be bullish. On the downside, a reversal lower would refocus sights on 109-26, the May 29 low, where a break would open key support and the bear trigger, at 109-12+, May 22 low.

SOFR FUTURES CLOSE

Jun 25 +0.005 at 95.693

Sep 25 +0.025 at 95.920

Dec 25 +0.030 at 96.185

Mar 26 +0.035 at 96.405

Red Pack (Jun 26-Mar 27) +0.050 to +0.055

Green Pack (Jun 27-Mar 28) +0.050 to +0.055

Blue Pack (Jun 28-Mar 29) +0.050 to +0.055

Gold Pack (Jun 29-Mar 30) +0.055 to +0.060

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.28% (+0.00), volume: $2.600T

- Broad General Collateral Rate (BGCR): 4.27% (+0.00), volume: $1.075T

- Tri-Party General Collateral Rate (TCR): 4.27% (+0.00), volume: $1.042T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $111B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $282B

FED Reverse Repo Operation

RRP usage retreats to $181.417B this afternoon from $204.625B yesterday, total number of counterparties at 34. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

MNI PIPELINE: Corporate Bond Update: $1.5B Analog Devices 2Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 06/12 $2B *Export Development Canada (EDC) 5Y SOFR+41

- 06/12 $1.5B #Analog Devices $850M 3Y +40, $650M 5Y +55

- 06/12 $Benchmark HA Sustainable 5.5Y +225, 10Y +215

MNI BONDS: EGBs-GILTS CASH CLOSE: Multiple Factors Drive Bull Flattening

Bund and Gilt yields dropped Thursday for the 3rd time in 4 sessions this week.

- UK monthly activity came in weaker than expected, boosting Gilts early, while EGB curves bull flattened on news of proposal for a 12-month phase-in period for Dutch pension reforms.

- Weak US jobless claims and soft producer prices saw core instruments hit the best levels of the session, with momentum largely carrying through to the cash close.

- Both the German and UK curves held bull flatter, with Gilts outperforming Bunds.

- Periphery / semi-core EGB spreads closed a little wider.

- Friday's calendar includes UK consumer survey and Eurozone industrial production / trade balance figures, while there will also be appearances by ECB's Nagel and Cipollone.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.9bps at 1.816%, 5-Yr is down 4.7bps at 2.079%, 10-Yr is down 5.7bps at 2.478%, and 30-Yr is down 7.3bps at 2.932%.

- UK: The 2-Yr yield is down 4.7bps at 3.866%, 5-Yr is down 5.8bps at 3.985%, 10-Yr is down 7.5bps at 4.477%, and 30-Yr is down 8.5bps at 5.193%.

- Italian BTP spread up 1.6bps at 92.7bps / Greek up 3.1bps at 74.5bps

MNI FOREX: Soft Data Further Weighs on USD, Weaker Theme Prevailing

- A returning soft-USD theme continued to dictate proceedings in the FX space on Thursday, with markets extending the post US-CPI trend, bolstered by Trump's confirmation of incoming unilateral tariffs on countries without a trade deal. Furthermore, soft PPI readings for May and a high jobless claims figure further dented greenback sentiment, allowing the USD index to reach bearish cycle extremes.

- Most notable was the strengthening impact on the Euro, as EURUSD broke the bull trigger at 1.1573 and rose to a fresh high of 1.1631, the highest level since late 2021. Above here, 1.1685 provides the next target for the move, the 76.4% retracement of the Jan ‘21 - Sep ‘22 downleg.

- Softer risk sentiment stemming from increased geopolitical tensions around Iran have relatively weighed on the high beta currencies, and the likes of AUD and NZD in G10 and the emerging market FX basket have relatively underperformed. President Trump talked down the likelihood of a nuclear deal with Iran, and reports continue to circulate of a potential Israeli operation on the region to stem Tehran's nuclear ambitions.

- A poor monthly GDP release from the UK works further in favour of a sell-on-rallies theme for GBP, but this appears most beneficial for the crosses given the broad dollar weakness. This has prompted the EURGBP recovery to briefly extend to as much as 1.42% in just three sessions. Price action has been exacerbated by a break of resistance at 0.8442, the 50-day EMA, and the cross briefly pierced the May 2 high, printing 0.8547.

- Friday’s data focus will be on the UK quarterly consumer BOE/Ipsos Inflation Attitudes Survey, before Eurozone IP and trade balance figures. US prelim UMich sentiment and inflation expectations are also due.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 13/06/2025 | 0600/0800 | *** | Final Inflation Report | |

| 13/06/2025 | 0600/0800 | *** | HICP (f) | |

| 13/06/2025 | 0645/0845 | *** | HICP (f) | |

| 13/06/2025 | 0700/0900 | *** | HICP (f) | |

| 13/06/2025 | 0830/0930 | ** | Bank of England/Ipsos Inflation Attitudes Survey | |

| 13/06/2025 | 0900/1100 | ** | Industrial Production | |

| 13/06/2025 | 0900/1100 | * | Trade Balance | |

| 13/06/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 13/06/2025 | 1230/0830 | ** | Wholesale Trade | |

| 13/06/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 13/06/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 13/06/2025 | 1500/1700 | ECB Elderson At Senior Supervisor's Conference | ||

| 13/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 13/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |