MNI Eurozone Inflation Preview – July 2025

Jul-29 15:55By: Moritz Arold and 1 more...

Inflation+ 1

Few Fireworks Expected In July

- The Eurozone inflation round will be split across three days in July. Spain kicks off proceedings on Wednesday, with France, Germany and Italy to all follow Thursday. The Netherlands rounds off the main national-level releases on Friday morning ahead of the Eurozone-wide release later that day.

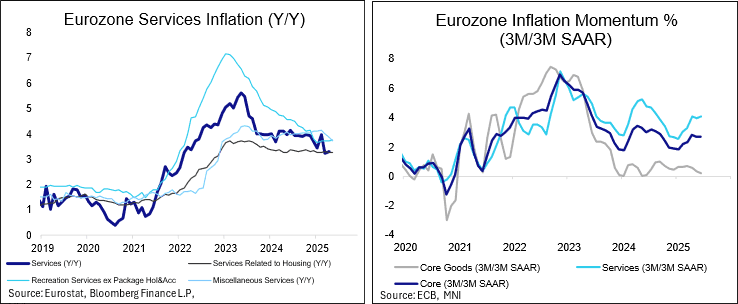

- Consensus is for the core rate to remain unchanged at 2.3% Y/Y, while headline is seen to slightly decelerate to 1.9% amid expectations for a softer energy Y/Y print.

- The hawkish aspects of last week’s post-decision press conference from President Lagarde centred on familiar themes like tariffs (“the sooner this trade uncertainty is resolved the less uncertainty we will have to deal with”) and growth (Q1 GDP print was "not just front loading", but also "increased consumption and increased investment, and not only attributable to Ireland").

- Comments around the inflation outlook were broadly unchanged compared to June. The ECB expects headline inflation to fall below target from Q3 2025 and into 2026, before returning back towards 2% by 2027. Meanwhile, easing compensation pressures should continue to contribute to services disinflation in the coming quarters.

- That should leave markets focusing more on this week’s Q2 flash GDP prints and ongoing EU-US tariff headline flow. However, with ECB-dated OIS pricing just 16bps of easing through the year, we think there is still scope for a decent reaction in either direction should the July round bring a notable (e.g. 0.2pp or more) surprise on the core metric.