PIPELINE: Corporate Bond Update: $1.5B Analog Devices 2Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 06/12 $2B *Export Development Canada (EDC) 5Y SOFR+41

- 06/12 $1.5B #Analog Devices $850M 3Y +40, $650M 5Y +55

- 06/12 $Benchmark HA Sustainable 5.5Y +225, 10Y +215

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: FED Reverse Repo Operation

RRP usage recedes to $144.214B this afternoon from $147.505B yesterday, total number of counterparties at 32. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

GBPUSD TECHS: Monitoring Support At The 50-Day EMA

- RES 4: 1.3550 High Feb 24 ‘22

- RES 3: 1.3510 1.236 proj of the Feb 28 - Apr 3 - 7 price swing

- RES 2: 1.3402/3444 High May 6 / High Apr 28 / 29 and the bull trigger

- RES 1: 1.3323 High May 9

- PRICE: 1.3276 @ 16:48 BST May 13

- SUP 1: 1.3140 Low May 12

- SUP 2: 1.3087 50-day EMA

- SUP 3: 1.3041 Low Apr 14

- SUP 4: 1.2968 Low Apr 11

GBPUSD traded lower Monday as the pair extended the correction that started Apr 29. The 20-day EMA has been breached. Furthermore, a minor head and shoulders formation on the daily chart highlights a reversal and reinforces the likelihood of a corrective pullback near-term. Key support to watch is 1.3087, the 50-day EMA. The bull trigger is unchanged at 1.3444, the Apr 28 / 29 high. A break of this level would resume the uptrend.

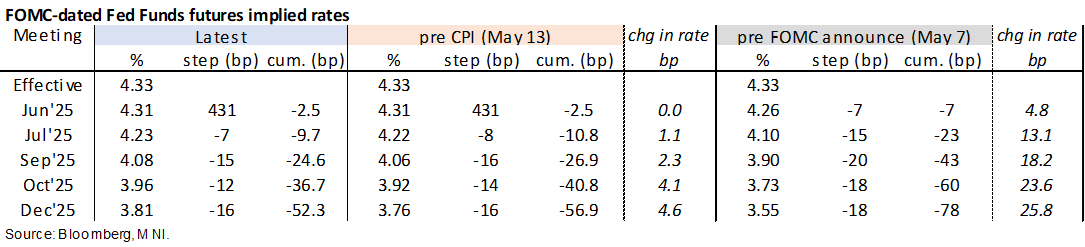

STIR: Getting Closer To More Seriously Considering Oct For Next Fed Cut

- The climb in Fed Funds implied rates has steadied along with equities after climbing solidly since the US cash equity open.

- The Fed rate path was initially little changed for an hour after the April CPI report, which was close to expectations with core CPI at 0.24% (unrounded analyst av 0.27%) and supercore CPI at 0.21% M/M (exactly in line with the average of admittedly just four estimates).

- Cumulative cuts from 4.33% effective: 2.5bp Jun, 9.5bp Jul, 24.5bp Sep, 36.5bp Oct and 52.5bp Dec.

- The ~52bp of cuts priced for 2025 is the least since late February and leaves it close to the median FOMC dot pencilling in 50bp of cuts in what seems like a long while ago since the March SEP.

- The SOFR implied terminal yield of 3.445% is (SFRU6) is 3.5bp higher post-CPI for 1.5bp on the day and 5bp above pre Apr 2 Liberation Day tariff announcement levels. It stands out less on a relative basis though, at what would be its highest close since Mar 27.