US DATA: PPI Trends Largely Benign, But Trade Margins Bounce Back

Jun-12 13:07

May's Producer Price inflation report provided some relief to concerns that tariff-related factors would significantly push up pipeline pressures in the month. Instead, the broader trend in pipeline pressures appears to be slowing rather than accelerating.

- The headline final demand PPI reading of 0.13% M/M was below the 0.2% expectation, and while that's offset by a decent upward revision to April (-0.24% from -0.47%), the overall index remains below its January level in seasonally adjusted terms, and up just 2.6% Y/Y. Ex-food/energy rose 0.14% (0.3% expected), after an upwardly revised -0.21% (was -0.44%), but the 3M annualized run rate remained below 1% (0.9%) for a second month and the 3.0% Y/Y rate was the slowest since August 2024.

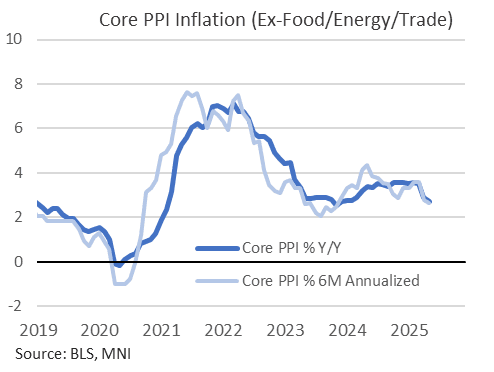

- The main measure of core PPI has effectively ground to a halt: ex-food/energy/trade 0f 0.05% M/M follows -0.13% in April (slight downward rev from -0.11%), bringing the 3M annualized rate down to 0.5% - the slowest since June 2020. The 6-month annual rate is down to 2.6%, lowest since November 2023, with the Y/Y rate clocking in at 2.7%, lowest (unrounded) since December 2023.

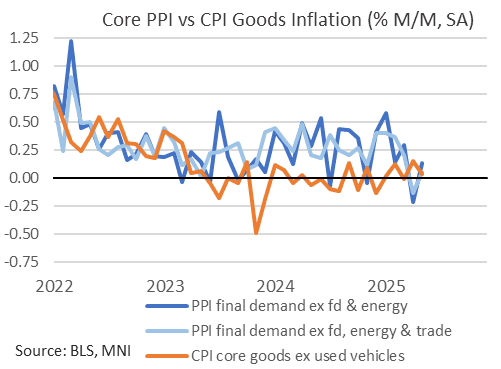

- Some less benign metrics from an inflationary perspective: final demand goods ex-food/energy prices were up 0.2% M/M, continuing a string of 5 months (and 7 of 8) of a 0.2 or 0.3% run rate, looking a little hotter than H2 2024 when readings were in the 0.1- 0.2% range.

- And in final demand services, there was some evidence of margins picking up, though again evidence here was mixed: total final demand services PPI was up 0.1% after -0.4%, with trade services rebounding to 0.4% after -0.5%, but transportation/warehousing (-0.2%) and "other" (0.0%) not contributing.

- As the figures imply, final demand services were a solid contributor to overall PPI - but the overall rise of 0.1% would have been negative were it not for an "imputed" figure of margins for final demand trade services (20% of the PPI basket) which rose 0.44%. That's potentially a sign that wholesalers and retailers tried to increase margins on sales directly to households in the month, with the SA index hitting an all-time high. At the very least there was a rebound in margins after March's 0.5% drop.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: Little To Suggest Major PCE-CPI Gap From Report Components

May-13 13:06

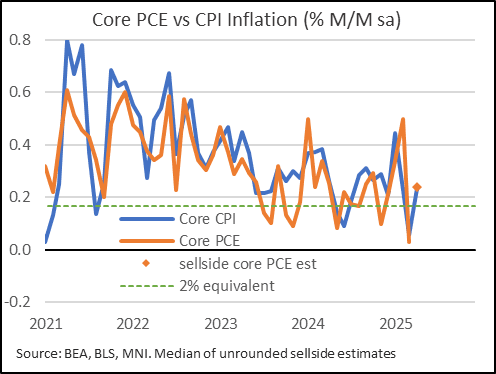

There is little in this report alone to suggest a meaningful gap between CPI and PCE - in other words, the slight downside miss in core CPI doesn't carry a major re-interpretation for PCE via the components. Note April core PCE consensus was 0.24% M/M coming into today, and while this may dip slightly we doubt forecasts will be radically changed (core CPI came in at 0.22% M/M).

- For the usual suspects: as noted, airfares (taken from PPI for PCE) were a little softer than expected, but basically in line - and in the same camp, auto insurance rebounded more or less as expected (again, this is taken from PPI for PCE).

- CPI medical care services were if anything stronger than expected, rising 0.5% M/M for a second consecutive month, equaling March's rise which was the biggest since September 2024 - with higher professional and dental care inflation offset by slower hospital care inflation.

- On a side note on services: communications fell by 0.4% M/M, the softest in 5 months after being a stronger-than-expected contributor in the earlier months of the year.

US DATA: Health Insurance Reset Stronger Than Expected But Marginal

May-13 13:01

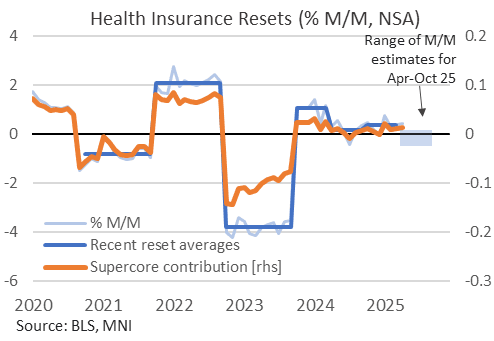

- Touching on one small area that usually doesn’t get attention, health insurance was a little stronger than some expectations we had seen for its reset that will set the tone for the next six months.

- Specifically, CPI health insurance increased 0.43% M/M in April vs TD Securities expectations of an average 0.2% M/M increase through Apr-Sep and Goldman Sachs eyeing -0.5% M/M for April.

- It’s within the 0.5% M/M in Oct’24 and 0.35% averaged through Oct-Mar, to continue to broadly add 0.01pp to supercore CPI over the next six months (as opposed to dragging -0.01pp in the case of the GS figures).

- This doesn’t feed into core PCE.

STIR: Little Net Change In Fed Pricing Over CPI, 57bp Cuts Showing Through Dec

May-13 12:56

Little net change in Fed pricing in the wake of the CPI release.

- Softer-than-expected to inline headline and core CPI readings countered by the “high” unrounded figures and inline supercore release.

- 2.5bp of cuts priced into Fed funds for June, 10.5bp through July, 27bp through September, 41bp through October & 57bp through year-end. All within 1bp of pre-data levels.

- Market happy to consolidate the tariff reprieve-driven hawkish repricing seen on Monday at this stage, albeit with economic uncertainty remaining elevated vs. normal levels.